Long-only cryptocurrency portfolio management by ranking the assets: a neural network approach

Reading time: 2 minute

...

📝 Original Info

- Title: Long-only cryptocurrency portfolio management by ranking the assets: a neural network approach

- ArXiv ID: 2512.08124

- Date: 2025-12-09

- Authors: Zijiang Yang

📝 Abstract

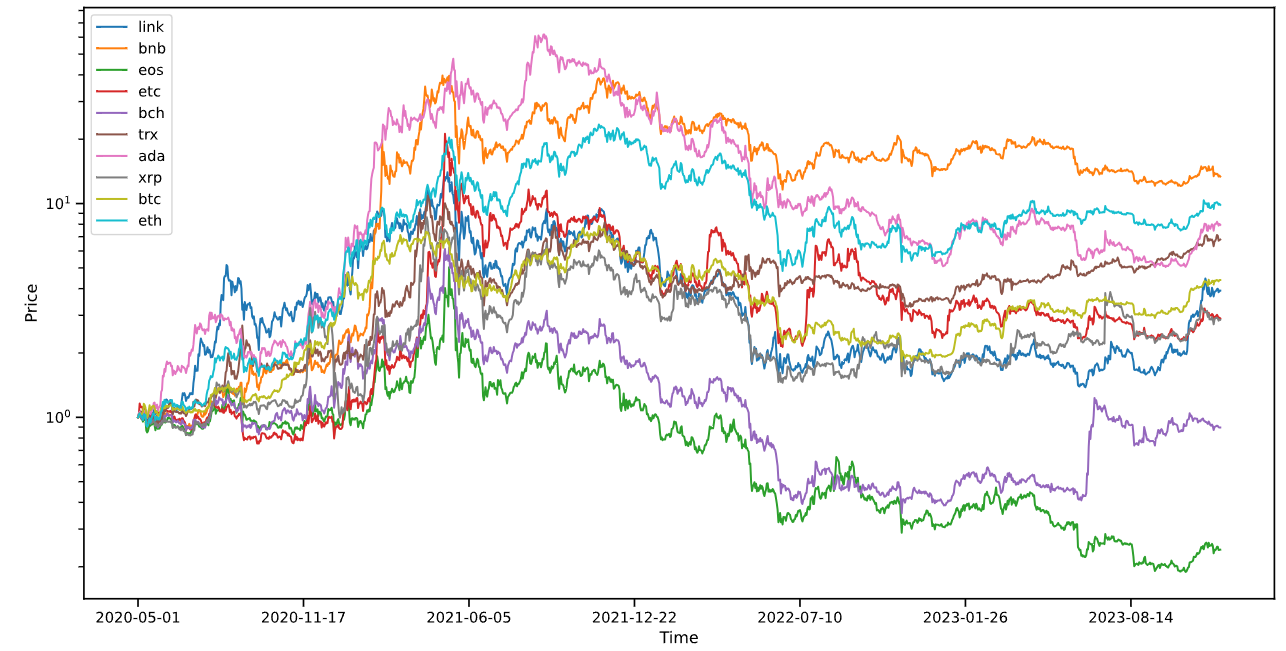

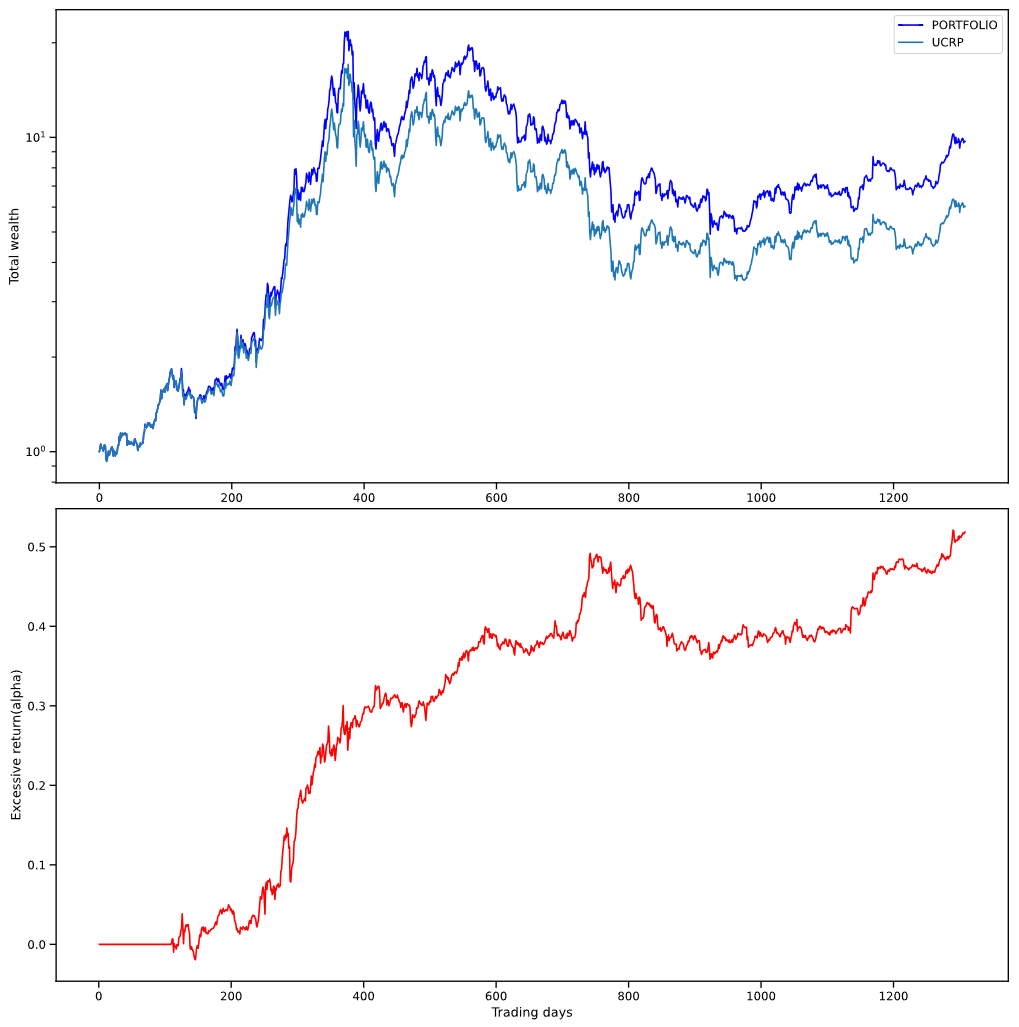

This paper will propose a novel machine learning based portfolio management method in the context of the cryptocurrency market. Previous researchers mainly focus on the prediction of the movement for specific cryptocurrency such as the bitcoin(BTC) and then trade according to the prediction. In contrast to the previous work that treats the cryptocurrencies independently, this paper manages a group of cryptocurrencies by analyzing the relative relationship. Specifically, in each time step, we utilize the neural network to predict the rank of the future return of the managed cryptocurrencies and place weights accordingly. By incorporating such cross-sectional information, the proposed methods is shown to profitable based on the backtesting ex...📄 Full Content

📸 Image Gallery

Reference

This content is AI-processed based on open access ArXiv data.