The spectrum of the stochastic Bessel operator at high temperature

Ramírez and Rider (2009) established that the hard edge of the spectrum of the $β$-Laguerre ensemble converges, in the high-dimensional limit, to the bottom of the spectrum of the stochastic Bessel operator. Using stochastic analysis tools, we prove …

Authors: Laure Dumaz, Hugo Magaldi

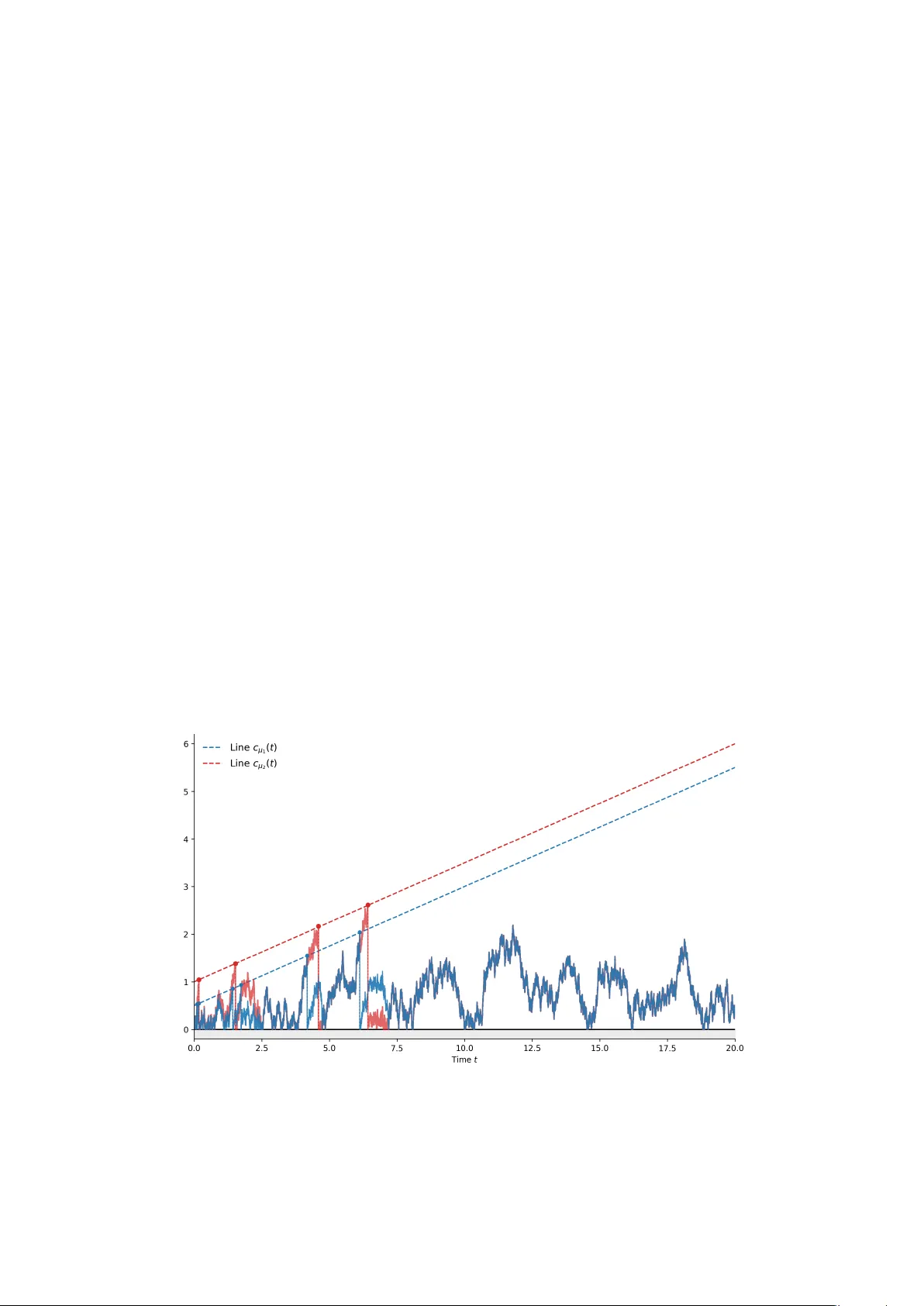

THE SPECTR UM OF THE STOCHASTIC BESSEL OPERA TOR A T HIGH TEMPERA TURE LA URE DUMAZ AND HUGO MA GALDI A B S T R AC T . Ram ´ ırez and Rider [ 15 ] established that the hard edge of the spectrum of the β - Laguerre ensemble con ver ges, in the high-dimensional limit, to the bottom of the spectrum of the stochastic Bessel operator . Using stochastic analysis tools, we prov e that, in the high-temperature limit ( β → 0 ), the rescaled eigen value point process of this operator con ver ges to a non-tri vial lim- iting point process. This limit is characterized by a family of coupled diffusions and dif fers from a Poisson point process due to its interaction with the hard edge. Exploiting this dif fusion charac- terization, we establish exact large deviation asymptotics for the largest eigenv alues. Furthermore, for an explicit range of the parameters, we relate this limiting process to the finite- n β -Laguerre ensemble, conjecturing an e xact distributional match with the infinite sum of its independent e xpo- nential gaps. As a byproduct of our analysis, we also formulate a conjecture regarding an explicit integral formula for the probability that a reflected Bro wnian motion with a constant drift hits an affine line, generalizing a formula of Salminen and Y or [ 17 ]. C O N T E N T S 1. Introduction 1 2. Strategy of proof 9 3. Con vergence of the e xplosion times 11 4. Asymptotics for the k largest eigen values 17 References 23 1. I N T RO D U C T I O N ( β , a ) -Laguerre ensembles. In this paper , we study the high-temperature limit of the spectrum of the Stochastic Bessel Operator (SBO). Its finite-dimensional counterpart is the famous ( β , a ) - Laguerre ensemble, a probability measure on the set of ordered points in R n + with density 1 Z n,β ,a Y i − 1 , β > 0 and Z n,β ,a is the normalization constant. For the specific values β = { 1 , 2 , 4 } and integer a ∈ N , this joint law describes the eigenv alue distribution of W ishart matrices. These matrices take the form X X ⊺ , where X is a rectangular matrix of size n × ( n + a ) with independent real ( β = 1 ), complex ( β = 2 ), or quaternionic ( β = 4 ) Gaussian entries of mean zero and v ariance 1 . Note that the matrix ( n + a ) − 1 X X ⊺ represents the sample covariance matrix of n independent data vectors, each of them containing n + a i.i.d. standard Gaussian entries. Date : March 31, 2026. 1 2 LA URE DUMAZ AND HUGO MAGALDI Dumitriu and Edelman [ 6 ] constructed a tridiagonal random matrix model for general β > 0 , kno wn as the β -W ishart ensemble, whose eigen values are distributed according to the density (1). The matrix is written as L β ,a L ⊺ β ,a , where L β ,a = 1 √ β χ ( a + n ) β χ ( n − 1) β χ ( a + n − 1) β χ ( n − 2) β . . . . . . χ ( a +2) β χ β χ ( a +1) β (2) The entries χ r appearing in the matrix are independent χ -distributed random variables with the indicated parameter r . While the construction for the classical cases β = 1 , 2 , 4 relies on bidiag- onalizing the initial W ishart matrices via Householder reflections, the resulting tridiagonal matrix naturally generalizes to all v alues of β > 0 , providing a matrix model to study (1) for general β . Physically , the particles distributed according to the law (1) can be interpreted as a log-gas at in verse temperature β confined to the half-line R + by a log-Gamma potential [ 8 ]. The n particles are positiv ely charged and repel each other . The interaction with the hard edge at the origin can be modeled by an additional particle fixed at 0 . The ef fectiv e sign of this ghost charge depends on the parameters: when a ≥ 2 /β − 1 , the hard edge is repulsiv e (positiv ely charged), whereas when a < 2 /β − 1 , the hard edge becomes attractiv e (negati vely charged), causing particles to accumulate near the origin. T o rigorously capture the microscopic beha vior of these particles near the hard edge and decouple the system from finite- n effects, we turn to the continuous limit. The Stochastic Bessel Operator . The simple tridiagonal structure of the matrix (2) provides a po werful tool for deri ving se veral important statistical properties. In particular , as noticed by Edelman and Sutton [ 7 ], it acts as a discrete dif ferential operator , providing a way to take its limit at the lev el of self-adjoint dif ferential operators. Ram ´ ırez and Rider implemented this approach for the matrix (2), and pro ved in [ 15 ] that the point process of the smallest rescaled eigen values nλ ( n ) i has a limit as n → ∞ . These rescaled eigen values con ver ge towards the smallest eigen values of the stochastic Bessel operator (SBO). For all β > 0 and a > − 1 , the SBO is defined as G β ,a = − exp ( a + 1) x + 2 √ β b ( x ) · d dx exp − ax − 2 √ β b ( x ) d dx , where b is a standard Brownian motion. It formally corresponds to the dif ferential operator e x − d 2 dx 2 + ( a + 2 √ β b ′ ( x )) d dx . This operator acts as the infinitesimal generator (modulo the time change e x ) of a diffusion e volv- ing in a white noise potential given by b ′ . It is defined on a suitable domain of L 2 ( R + , m ) where m ( dx ) = exp( − ( a + 1) x − 2 √ β b ( x )) dx with Dirichlet boundary condition at the origin. The operator G β ,a has a discrete spectrum of simple eigen values: 0 < λ ∞ β ,a (1) < λ ∞ β ,a (2) < · · · . Moreov er , applying Riccati’ s map to the solution of the eigenv alue equation with Dirichlet boundary condition at 0 , Ram ´ ırez and Rider introduced a family of dif fusions characterizing the point process of SBO’ s eigen values which will be instrumental in our proof (see paragraph 2.1 belo w). THE SPECTR UM OF THE STOCHASTIC BESSEL OPERA TOR A T HIGH TEMPERA TURE 3 Con vergence in the high-temperature limit ( β → 0 ). W e focus here on the small β regime, often referred to as the high-temperature limit. Specifically , we in vestigate the microscopic scale— where the spacing between particles is of order 1 —within the universal scaling limits N → ∞ of finite- n β ensembles. The high-temperature regime of finite- n β -ensembles has been the subject of se veral recent studies. In the double limit n → ∞ and β → 0 such that β n conv erges to a constant, the global fluctuations and macroscopic limits were studied in [ 1 ], [ 12 ], [ 18 ], [ 9 ]. Under the same scalings, at the microscopic level, con vergence to a Poisson point process has been established in [ 14 ], [ 13 ]. This decorrelation phenomenon extends to the univ ersal scaling limits—namely Sine β in the bulk and Airy β at the edge. For these, it was sho wn in [ 3 , 2 , 4 ], that under an appropriate rescaling, the eigen value point process con ver ges towards a Poisson point process. For SBO’ s eigenv alues, when β tends to 0 , the smallest eigen values approach the hard edge at 0 at an e xponential rate due to the strong attraction at the origin. Specifically , the smallest eigen values are of order exp( − Θ(1) /β ) . T o obtain a non-trivial limit, we consider the rescaled eigen values: β ln(1 /λ ∞ β ,a ( i )) , i ≥ 1 . Under this rescaling, the spacing between the first points is of order O (1) . This transformation re verses the ordering, meaning the rescaled point process is bounded from abov e. Furthermore, the in verse mapping µ 7→ exp( − µ/β ) has a sharp transition near µ = 0 . In the small β limit, for any fixed µ > 0 , there are only finitely many eigenv alues below exp( − µ/β ) . Con versely , for µ ≤ 0 , the number of eigen values explodes as β → 0 , as we are no longer exponentially close to the hard edge. Let us first state our con vergence theorem: Theorem 1 (Con vergence of the eigen values) . As β → 0 , the r escaled eigen value point pr ocess of the SBO ( β ln(1 /λ ∞ β ,a ( i )) , i ≥ 1) con ver ges in law towards a random simple point pr ocess on R + with an accumulation point at 0+ . W e denote this point process, ordered in a decreasing order, by ( µ ∞ a ( i ) , i ≥ 1) . The con- ver gence holds for a well-chosen topology of Radon measures on R + , corresponding to a left- v ague/right-weak topology . Characterization of the limiting point process via coupled diffusions. W e characterize the limiting process using a family of dif fusions ( r ( a ) µ ) µ> 0 , a construction similar in spirit to the one used for the SBO eigen values. Construction of the diffusions. This construction relies on a family of Brownian motions with drift reflected at 0 . Recall that a reflected Bro wnian motion with drift δ starting at 0 , denoted R ( δ ) , admits the Skorokhod representation: R ( δ ) ( t ) = B ( t ) + δ t + L ( t ) , where B is a Brownian motion and L ( t ) = sup 0 ≤ s ≤ t max( − B ( s ) − δ s, 0) . Recall the classical Skorokhod reflection problem: for any continuous path y : [0 , ∞ ) → R with y (0) ≥ 0 , there exists a unique pair of continuous functions ( x, ℓ ) such that • x ( t ) = y ( t ) + ℓ ( t ) ≥ 0 for all t ≥ 0 , • ℓ is non-decreasing with ℓ (0) = 0 , • ´ t 0 x ( s ) dℓ ( s ) = 0 for all t ≥ 0 . 4 LA URE DUMAZ AND HUGO MAGALDI For a detailed proof of existence and uniqueness of this mapping, see e.g. [ 11 , Lemma 3.6.14] or [ 16 , Chapter IX, Theorem 2.3]. In our conte xt, we apply the Sk orokhod mapping to the Bro wnian motion with drift δ , which yields the pair of the reflected process R ( δ ) and L (corresponding to the local time up to a constant factor). Let us first define the diffusion r ( a ) µ for a single fixed parameter µ > 0 . T o ease the presentation, we will drop in the following the superscript a . W e define the critical line as c µ ( t ) = µ + t/ 4 for t ≥ 0 . The process is constructed recursi vely . W e refer to Figure 1 for an illustration. • Initialization: Set r µ (0) = 0 . • Phase − : The process ev olves as a reflected Bro wnian motion with drift − a/ 4 until it hits the critical line c µ . Let ξ − µ (1) denote this hitting time. • Reset: Immediately upon hitting c µ , the process jumps to 0 . • Phase + : It then evolv es as a reflected Brownian motion with drift ( a + 1) / 4 until it hits c µ again. Let ξ + µ (1) denote this second hitting time. • Recursion: This cycle repeats, alternating between the drifts − a/ 4 and ( a + 1) / 4 after each hit of the critical line. W e denote the hitting times as ξ − µ ( i ) and ξ + µ ( i ) for i ≥ 2 . F I G U R E 1 . Simulation of the diffusion r µ for µ = 0 . 8 and a = 1 . Since the critical line t 7→ µ + t/ 4 grows linearly , the probability that the reflected Brownian motion with drift reaches it in finite time is strictly less than one for at least one of the two phases (see Remark 1.1 belo w). Consequently , the total number of completed cycles is finite almost surely (it is stochastically dominated by a geometric distribution). Remark 1.1 (Drifts versus critical line) . A r eflected Brownian motion with drift δ hits the critical line t 7→ µ + t/ 4 almost sur ely if and only if δ ≥ 1 / 4 . • F or the phase with drift − a/ 4 : Since we assume a > − 1 , this drift is always strictly less than 1 / 4 . • F or the phase with drift ( a + 1) / 4 : If a ≥ 0 , the drift is ≥ 1 / 4 : a hit holds almost sur ely . If a ∈ ( − 1 , 0) , the drift is less than 1 / 4 , so the hit occurs with pr obability strictly less than 1 . Thus, for a ∈ ( − 1 , 0) , both phases have a pr obability strictly less than 1 to hit the critical line . THE SPECTR UM OF THE STOCHASTIC BESSEL OPERA TOR A T HIGH TEMPERA TURE 5 W e now define the family of diffusions ( r µ ) µ simultaneously for all µ > 0 by coupling them through a single dri ving Brownian motion B . For any drift δ and starting time s ≥ 0 , let us define the path R ( δ,s ) starting at 0 at time s , dri ven by B : R ( δ, s ) ( t ) = Y δ,s ( t ) + sup s ≤ u ≤ t max(0 , − Y δ,s ( u )) , t ≥ s , where Y δ,s ( t ) = δ ( t − s ) + ( B ( t ) − B ( s )) is the non-reflected path. Gi ven this coupling of reflected Bro wnian motion, we define the family ( r µ ) µ as follows. Let ξ + µ (0) := 0 . For all i ≥ 1 , we set r µ ( t ) := R ( − a/ 4 , ξ + µ ( i − 1)) ( t ) , for t ∈ [ ξ + µ ( i − 1) , ξ − µ ( i )) , where the hitting time is ξ − µ ( i ) := inf { t ≥ ξ + µ ( i − 1) , R ( − a/ 4 , ξ + µ ( i − 1)) ( t ) = c µ ( t ) } . Subsequently , r µ ( t ) := R (( a +1) / 4 , ξ − µ ( i )) ( t ) , for t ∈ [ ξ − µ ( i ) , ξ + µ ( i )) , where ξ + µ ( i ) := inf { t ≥ ξ − µ ( i ) , R (( a +1) / 4 ,ξ − µ ( i )) ( t ) = c µ ( t ) } . An illustration of the coupled dif fusions r µ for two different values of µ can be found in Figure 2. F I G U R E 2 . Simulation of two diffusions r µ for µ = 0 . 5 (blue) and µ = 1 (red), with a = 1 (color online). 6 LA URE DUMAZ AND HUGO MAGALDI Characterization of the limiting point pr ocess. W e associate a random counting measure to the completion times of the + phases only ν µ := X i ≥ 1 δ ξ + µ ( i ) . The mass ν µ ( R + ) corresponds to the total number of full cycles completed by the diffusion r µ . It is easy to see that the total mass is finite almost surely: as observed in Remark 1.1, at least one of the two phases has a drift strictly less than 1 / 4 . Since the probability for a reflected Brownian motion to hit an af fine line growing strictly faster than its drift is strictly less than 1 , the number of points of ν µ is stochastically dominated by a geometric random v ariable. As µ increases, the barrier c µ shifts upwards, making it harder to hit. Thus, the map µ 7→ ν µ ( R + ) is non-increasing almost surely and takes values in N ∪ { 0 } . W e define the limiting point process M a on (0 , ∞ ) via its cumulative count: for an y µ > 0 , the number of points in M a greater than µ is giv en exactly by the number of c ycles of r µ : M a ([ µ, ∞ )) := ν µ ( R + ) . W e can no w state the characterization of the limiting point process P i ≥ 1 δ µ ∞ a ( i ) defined in Theorem 1: Theorem 2 (Characterization of the limiting point process) . The limiting point pr ocess P i ≥ 1 δ µ ∞ a ( i ) has the same distribution as M a . Comments and further results. This characterization allows us to compute sev eral statistics for the limiting point process. Lar gest eigen value. For a ≥ 0 , the distribution of the largest eigen v alue is related to the hitting time of an af fine boundary and takes a simple form: Theorem 3 (First eigen value limit for a ≥ 0 ) . Let R ( − a/ 4) ( t ) be a r eflected Br ownian motion (at 0 ) with drift − a/ 4 . Then the pr obability that the lar gest point µ ∞ a (1) exceeds µ equals the pr obability that R ( − a/ 4) hits the affine line t 7→ µ + t/ 4 in a finite time. For a = 0 , using Corollary 5 of [ 17 ], this probability is gi ven by P ( ∃ t ≥ 0 , R (0) ( t ) ≥ µ + t/ 4) = 2 X k ≥ 1 ( − 1) k − 1 exp( − µk 2 / 2) . (3) W e hav e a conjecture for an explicit expression of the largest eigen v alue for all a > 0 , see the equation (5). Lar ge a limit conjectur e. Moreover , we expect that one recovers a Poisson point process in the large a limit. This is due to the fact that the coupled diffusions will hav e to move against a strong drift to hit the critical line, and therefore will typically hits it very quickly when the hitting time is finite: this compensates the growth of the critical line. This expected transition to Poissonian statistics mirrors the behavior observ ed in the high-temperature b ulk or edge [ 2 , 3 , 4 ]. This can be linked as well to the transition of the Stochastic Bessel Operator to the Stochastic Airy Operator as a → ∞ prov ed in [ 5 ]. W e formalize this as a conjecture. Conjecture 1.2. When a → ∞ , the r escaled point pr ocess M a con ver ges towar ds a P oisson point pr ocess. THE SPECTR UM OF THE STOCHASTIC BESSEL OPERA TOR A T HIGH TEMPERA TURE 7 F inite- n scaling. Finally , consider the finite- n ( β , a ) -Laguerre ensemble. When β → 0 , we obtain the follo wing density for the rescaled particles µ ( n ) k = β ln(1 /λ ( n ) k ) . 1 Z n,a n Y i =1 exp( − ( i − 1 + ( a + 1) / 2) µ ( n ) i )1 µ ( n ) 1 >µ ( n ) 2 > ··· >µ ( n ) n > 0 . This point process is naturally described through its gaps g j := µ ( n ) j − µ ( n ) j +1 , for j ∈ { 1 , . . . , n } ) (where µ ( n ) n +1 := 0 ). These gaps are n independent random v ariables, where g j follo ws an ex- ponential distribution with parameter j ( j + a ) / 2 . Therefore, one can construct the point process from the smallest point to the largest by successively adding independent gaps. Reconstructing the points from the gaps requires working backwards: the largest point is µ ( n ) 1 = P n j =1 g j , and the subsequent points are gi ven by the tail sums µ ( n ) i = P n j = i g j . One can check that the largest points of this point process have a well-defined limit as n → ∞ . This limit can be constructed recursively: first generate an infinite sequence of independent gaps ( g j , j ≥ 1) following exponential distributions with parameters j ( j + a ) / 2 . The largest point is then gi ven by the infinite sum ˆ µ ∞ a (1) := P ∞ j =1 g j , and subsequent points are found by successi vely remo ving gaps: ˆ µ ∞ a ( k ) := ∞ X j = k g j . (4) T aking the double limit —first as β → 0 and then as n → ∞ — we see that the repulsion does not disappear b ut its nature changes. It is no longer local as the g aps are gi ven by e xponential la ws (which allo w for small distances between the points), rather , the repulsion induces a deterministic shift in the exponential rates. It turns out that in the case a = 0 , one can sho w that the largest point µ ∞ 0 (1) of M 0 and the largest point ˆ µ ∞ 0 (1) coincide. Proposition 1.3 (Exact matching for a = 0 ) . The distribution of µ ∞ 0 (1) and ˆ µ ∞ 0 (1) ar e equal. Pr oof. The distribution of ˆ µ ∞ 0 (1) is that of an infinite sum of independent exponential random v ariables of parameter j 2 / 2 . Its Laplace transform is giv en by E [exp( − θ ˆ µ ∞ 0 (1))] = ∞ Y j =1 1 (1 + 2 θ j 2 ) . This product has an explicit simple e xpression in this case: ∞ Y j =1 1 1 + 2 θ j 2 = π √ 2 θ sinh( π √ 2 θ ) . In verting this Laplace transform, we obtain for the density: ∞ X k =1 ( − 1) k − 1 k 2 exp( − k 2 t/ 2) , which integrates to gi ve the tail probability (3). □ W e conjecture that this correspondence remains v alid for a > 0 across the entire point process. If true, this would imply a striking diffusion representation for (4) — a connection that is, to the best of our kno wledge, entirely unexpected. As a byproduct, establishing this conjecture would 8 LA URE DUMAZ AND HUGO MAGALDI provide an exact integral formula for the probability that a reflected Brownian motion with negati ve drift hits an af fine line. Conjecture 1.4 (Matching for all a ≥ 0 ) . F or all a ≥ 0 , the joint distribution of ( ˆ µ ∞ a ( i ) , i ≥ 1) and ( µ ∞ a ( i ) , i ≥ 1) ar e equal. As a cor ollary , using the explicit expr ession for the density of ˆ µ ∞ a (1) given by: ∞ X j =1 ( − 1) j − 1 j (2 j + a ) 2 j + a j e − j ( j + a ) 2 x . (5) This matching yields the following explicit integr al expr ession for the pr obability that a r eflected Br ownian motion with drift − a hits the affine line µ + bt : P ∃ t ≥ 0 , R − a ( t ) ≥ µ + bt = ∞ X j =1 ( − 1) j − 1 j + a/b j + j + a/b − 1 j − 1 e − 2 µj ( j b + a ) . (6) A natural pathway to prove the integral expression (6) would be to generalize the approach of Salminen and Y or to a reflected Brownian motion with ne gativ e drift. Remark 1.5 (Breakdown in the regime a ∈ ( − 1 , 0) ) . W e emphasize that Conjectur e 1.4 is re- stricted to a ≥ 0 . F or a ∈ ( − 1 , 0) , this exact matching is no longer true, as the asymptotic tails do not coincide, as we will see below . This pr ovides an explicit example where the limits do not commute, illustrating why the exchang e of such limits is usually a quite subtle issue in the literatur e. Non-poissonian limit. Thanks to its interpretation with reflected Brownian motions, one can com- pute the asymptotic of finding more than k points above some large lev el µ when µ ≫ 1 , which has an explicit e xpression. Proposition 1.6 (Asymptotics for the largest k eigen values) . F ix a ≥ − 1 . F or any fixed integ er k ≥ 1 , we have as µ → ∞ , P [ M a [ µ, ∞ ) ≥ k ] = exp − k ( | a | + k ) 2 µ (1 + o (1)) . The motiv ation to prov e such an asymptotic is twofold. Firstly , it will easily provide a proof that the limiting point process is not a Poisson point process as we will see just below . Secondly , it provides strong evidence that the point process ( µ ∞ a ( k ) , k ≥ 1) coincides with ( ˆ µ ∞ a ( k ) , k ≥ 1) for a ≥ 0 since their asymptotic decay rates are identical. As mentioned abov e, it also confirms that the limits do not commute when a ∈ ( − 1 , 0) , giving an example where the infinite uni versal limit captures “more repulsion” than the finite- n limit. An easy w ay to check that our limiting point process is not a Poisson point process is to look at the behavior of P [ M a [ µ, ∞ ) ≥ 2] P [ M a [ µ, ∞ ) ≥ 1] 2 , in the large µ limit, which should be equal to 1 / 2 for a Poisson point process. The proposition abov e directly prov es that this is not the case, as indeed, we obtain for µ ≫ 1 , P [ M a [ µ, ∞ ) ≥ 2] P [ M a [ µ, ∞ ) ≥ 1] 2 = exp( − µ (1 + o (1))) . THE SPECTR UM OF THE STOCHASTIC BESSEL OPERA TOR A T HIGH TEMPERA TURE 9 Local level repulsion when a ≥ 0 . Let us conclude with a few words about the local level r epulsion for a ≥ 0 . Consider the gap between the first and second limiting points, h 1 := µ ∞ a (1) − µ ∞ a (2) . Conditional on the largest eigen value being macroscopic, say µ ∞ a (1) ≥ µ 0 > 0 , one can in vestigate the probability that this gap is atypically small, namely P ( h 1 ≤ ε | µ ∞ a (1) ≥ µ 0 ) . In classical β -ensembles, strong local repulsion yields a probability scaling as O ( ε 1+ β ) . Here, ho wev er, a back-of-the-en velope computation provided belo w suggests that this probability scales linearly as O ( ε ) . This confirms that the strong microscopic repulsion v anishes in the limit, match- ing the behavior of the independent e xponential gaps observed in the finite- n scaling. T o see this, recall that the first eigen value corresponds to µ 1 := µ ∞ a (1) = max { µ > 0 : ∃ t ≥ 0 , r µ ( t ) = c µ ( t ) } . Let us look at the unconstrained diffusion r 1 := r µ 1 +1 , which ev olves simply as a reflected Brownian motion with drift − a/ 4 without undergoing any resetting procedure (the shift by +1 is arbitrary to ensure it nev er hits its critical line). No w , consider the shifted lev el ˜ µ 1 := µ 1 − ε and its associated path r ˜ µ 1 . For the e vent { h 1 ≤ ε } to occur , r ˜ µ 1 must complete a full cycle and hit c ˜ µ 1 again. Because the paths are coupled via the same dri ving Brownian motion, once r ˜ µ 1 completes its short resetting + phase, its trajectory must coincide with r 1 (unless when r 1 remains trapped within the narro w macroscopic strip [ c µ 1 − ε , c µ 1 ] whose probability is exponentially small). This implies that r 1 hits its maximal line c µ 1 and then, after a macroscopic amount of time, returns to within a distance ε of it. By classical path decomposition theorems, the trajectory of a Brownian motion with drift, conditioned on its overall maximum, behav es locally like a Bessel process (with drift). The probability that such a process returns to within a distance ε of its macroscopic maximum scales exactly as O ( ε ) . Acknowledgements. Special thanks are due to Djalil Chafai for many helpful discussions and for his in valuable support throughout this project. L.D. acknowledges the support of ANR RANDOP ANR-24-CE40-3377 and LOCAL ANR-22-CE40-0012. 2. S T R A T E G Y O F P R O O F 2.1. Rescaled diffusions. Our approach relies on the characterization of SBO spectrum via a family of coupled dif fusions ( p β λ , λ ∈ R ∗ + ) with initial condition p β λ (0) = + ∞ : dp β λ ( t ) = 2 √ β p β λ ( t ) db ( t ) + ( a + 2 β ) p β λ ( t ) − p β λ ( t ) 2 − λe − t dt . The dif fusion p β λ may explode to −∞ ; in this case it immediately restarts from + ∞ . These diffusions correspond to the Riccati transform p β λ = ψ ′ /ψ of the eigenv alue equation G β ,a ψ = λψ with initial condition ψ (0) = 0 , see (1.5) in [ 15 ]. It is crucial to note that the same Brownian motion b driv es the whole family of SDEs. It implies important properties such as the monotonicity of the number of explosions of p β λ (which turns out to be finite). In fact, the number of explosions of p β λ ov er R + corresponds to N β λ the counting function of the eigen values of the SBO. W e will study the small β limit of the family ( p β λ ) when λ is properly rescaled with β , that is when β ln(1 /λ ) is of order 1 . More precisely , we focus on the number of explosion times of p β λ on R + . Let us fix µ ∈ R . Notice that when p β λ reaches 0 , the term in front of the noise v anishes and the drift is negati ve. It implies that p β λ ne ver reaches 0 from belo w . It is easy to check 10 LA URE DUMAZ AND HUGO MAGALDI that the hitting times of 0 form a discrete point process. The first key idea of our analysis is to introduce the rescaled diffusion q β µ ( t ) , defined piecewise depending on the sign of p β λ β ( t/ (4 β )) , where λ β := exp( − µ/β ) . When the process is positiv e, we define q − µ ( t ) := − β ln( p β λ β ( t/ (4 β ))) . When it is negati ve, we define q + µ ( t ) := β ln( − p β λ β ( t/ (4 β ))) + µ + t/ 4 . A simple computation using It ˆ o formula sho ws that they follo w the SDEs: dq − µ = dW ( t ) + 1 4 − a + exp( − q − µ ( t ) /β ) + exp( − ( t/ 4 + µ − q − µ ( t )) /β ) dt , (7) dq + µ = dW ( t ) + 1 4 ( a + 1) + exp( − q + µ ( t ) /β ) + exp( − ( t/ 4 + µ − q + µ ( t )) /β ) dt , (8) where W is a standard Brownian motion obtained by rescaling the initial Brownian motion b (more precisely W ( t ) = − √ 4 β b ( t/ (4 β )) during the − phase and W ( t ) = √ 4 β b ( t/ (4 β )) during the + phase). The diffusions q ± µ may explode to −∞ in a finite time. By definition, the diffusion q β µ alternates between q + µ and q − µ : it starts to follow q + µ and each time q β µ = q + µ (resp. q − µ ) reaches −∞ , q β µ immediately restarts from + ∞ and follow q − µ (resp. q + µ ) . Let us define the critical line: c µ ( t ) := µ + t/ 4 , t ≥ 0 . (9) Roughly , the dif fusion q − µ behav es as follows for small v alues of β and after time 0 or an explosion time of q + µ : It starts at −∞ and first quickly goes up to 0 due to the strong drift term exp( − q − µ ( t ) /β ) . Then it spends some time between 0 and the affine line c µ ( t ) where it behav es approximately as a reflected Brownian motion with drift − a/ 4 . If it reaches the line t 7→ c µ ( t ) in a finite time then it quickly explodes to + ∞ after this hitting time due to the strong drift term exp( − ( t/ 4 + µ ) /β − q − µ ( t )) and it immediately restarts from −∞ , switching to q + µ . The behavior of the diffusion q + µ is similar except that, it behav es approximately as a reflected Bro wnian motion with drift ( a + 1) / 4 in the re gion { ( t, x ) , 0 ≤ t, 0 ≤ x ≤ c µ ( t ) } . Therefore, it almost surely hits c µ ( t ) when a ≥ 0 . There are two types of explosions for q β µ . Either q β µ explodes at a time ξ such that q β µ ( ξ − ) = q − µ ( ξ − ) , which corresponds to the (rescaled) hitting times of 0 by the initial diffusion p β λ β . Alter- nati vely , q β µ explodes at time ξ such that q β µ ( ξ − ) = q + µ ( ξ − ) , which corresponds to the (rescaled) explosion times of the initial dif fusion p β λ β . In the following, we denote by ξ − µ,β (1) < ξ + µ,β (1) < ξ − µ,β (2) < ξ + µ,β (2) < · · · the explosion times of the dif fusion q β µ and by ν β µ := X i ≥ 1 δ ξ + µ,β ( i ) , (10) the measure corresponding to the (rescaled) explosions of p β λ β . From the discussion above, it is natural to expect that as β → 0 , the trajectory of the diffusion q β µ con verges in law (under a well-chosen topology that smooths out the explosions parts) towards the diffusion r µ described in the introduction. Furthermore, notice that the diffusions are all driv en by the same underlying Bro wnian motion W which rigorously motiv ates our choice of coupling for r µ . 2.1.1. Con ver gence towards the limiting measur es. W e can now state the desired con ver gence result: THE SPECTR UM OF THE STOCHASTIC BESSEL OPERA TOR A T HIGH TEMPERA TURE 11 Proposition 2.1 (Con vergence of the explosion times) . When β → 0 , the measure ν β µ con ver ges in law to the measur e ν µ under the topology of weak con ver gence. From our construction, it is straightforward to e xtend this proposition to the joint law of ( ν β µ 1 , · · · , ν β µ k ) for fix ed positi ve numbers µ 1 < · · · < µ k , since the limiting candidates are defined through dif fusions dri ven by the same underlying Brownian motion. This directly implies con vergence for the finite-dimensional distrib utions of the point process { µ β ,a ( i ) , i ≥ 1 } . Let M β ,a := P i ≥ 1 δ µ β ,a ( i ) denote the measure associated to this point process. Recalling that M β ,a [ µ, + ∞ ) = ν β µ ( R + ) and M a [ µ, + ∞ ) = ν µ ( R + ) for any µ > 0 , we obtain the following result. Proposition 2.2 (Con ver gence of finite-dimensional distribution) . F ix 0 < µ 1 < · · · < µ k . When β → 0 , the random vector M β ,a [ µ 1 , + ∞ ) , · · · , M β ,a [ µ k , + ∞ ) , con ver ges to M a [ µ 1 , + ∞ ) , · · · , M a [ µ k , + ∞ ) . Theorems 1 and 2 are a direct consequence of this proposition. W e consider the point process as a random measure on the locally compact space (0 , + ∞ ] . W e endow the space of Radon measures with the vague topology . Note that this is equiv alent to vague con vergence near 0 and weak con vergence near + ∞ . More precisely , it corresponds to the topology that makes continuous the maps m 7→ ⟨ f , m ⟩ for any continuous function f : (0 , + ∞ ] → R supported in some [ δ, + ∞ ] . Using Kallenber g’ s tightness condition (see e.g. [ 10 ], Lemma 14.15), the family ( M β ,a ) β is tight if for all δ > 0 and ε > 0 , there exists c > 0 such that sup 0 <β ≤ β 0 P h M β ,a ([ δ, + ∞ )) > c i < ε . As M β ,a ([ δ, + ∞ )) con ver ges in distribution towards M a [ δ, + ∞ ) , which is almost surely fi- nite as observed abov e (we hav e seen that it is stochastically dominated by a geometric random v ariable), the condition abov e is satisfied. Since the finite-dimensional distributions of any subsequential limit are uniquely identified, we deduce the con ver gence of the eigen value point process stated in Theorem 1 as well as the identification of the limit provided in Theorem 2. W e conclude this section by outlining the remainder of the paper . Section 3 is dev oted to the proof of Proposition 2.1. In subsection 3.1, we will first control the first explosion time of the dif fusion q β µ and deduce the weak con vergence of the first k explosions times. Then, in subsection 3.2, we establish the tightness of the family ( ν β µ ) β > 0 . Finally , in the last section 4, we provide the proof of Proposition 1.6. 3. C O N V E R G E N C E O F T H E E X P L O S I O N T I M E S The goal of this section is to pro vide a proof of the con ver gence result stated in Proposition 2.1. W e will first control the explosion times until some lar ge fixed time T . 12 LA URE DUMAZ AND HUGO MAGALDI 3.1. Con vergence of the explosion times until a fixed time T . In this subsection, we fix µ > 0 . Let us first consider the first explosion time ξ 1 := ξ − µ,β (1) of the dif fusion q β = q β µ . By definition q β (0) = −∞ and q β ( t ) = q − ( t ) follows the SDE (7) until this first e xplosion time. W e define its first hitting time of 0 by τ 0 and its first hitting time of the critical line c µ by τ µ . W e decompose the trajectory of q − into three phases: (A) Ascent from −∞ . First it reaches the axis x = 0 in a short time. (B) Diffusion. Then it spends some time of order O (1) in the region [0 , c µ ( t )] , beha ving essentially like a reflected Bro wnian motion (above 0 ) with a constant drift − a/ 4 . (C) Explosion to + ∞ . If it reaches the critical line t 7→ c µ ( t ) then it will explode with high probability within a short time. In the next lemma, we e xamine the phases ( A ) and ( C ) . Lemma 3.1 (Ascent from −∞ and explosion to + ∞ ) . W ith pr obability going to 1 as β → 0 , we have τ 0 ≤ β and on the event { τ µ < + ∞} , ξ 1 − τ µ ≤ β . Pr oof. Let us first examine the ascent fr om −∞ of the diffusion q − . Notice that q − is stochasti- cally bounded from belo w (until its first explosion time) by the solution ˜ q − of the SDE: d ˜ q − ( t ) = dW ( t ) + 1 4 − a + exp( − ˜ q − ( t ) /β ) dt , ˜ q − (0) = −∞ . Define ˆ q − ( t ) := ˜ q − ( t ) − W ( t ) + at/ 4 . It solves the random ODE: d ˆ q − ( t ) = 1 4 exp( − ˆ q − µ ( t ) /β ) exp( − ( W ( t ) − at/ 4) /β ) dt For any c > 0 , let g denote the solution of the deterministic ODE g ′ ( t ) = c exp( − g ( t ) /β ) with initial condition g (0) = −∞ . It is given by g ( t ) = β ln( c β t ) , which is increasing with respect to the parameter c . Define the event E 0 := {∀ t ∈ [0 , β 5 ] , | W ( t ) | ≤ β 2 } , whose probability goes to 1 as β → 0 . On this e vent, we ha ve the follo wing lower bound: exp( − ( W ( t ) + at/ 4) /β ) / 4 ≥ exp( − ( β 2 + | a | β 5 / 4) /β ) / 4 > 1 / 8 , when β is small enough. Therefore, on E 0 , for suf ficiently small β , the diffusion ˜ q − rises faster than the deterministic solution with parameter c = 1 / 8 , reaching the lev el 5 β ln β before time β 5 . After reaching 5 β ln β , the exponential drift remains positiv e, so ˜ q − is bounded from below by a Brownian motion with drift − a/ 4 starting at 5 β ln β . This Brownian motion reaches 0 with probability going to 1 within any time interval ≫ β 2 (ln β ) 2 (note that the drift plays a negligible role here since we are dealing with tiny interv als). W e conclude that τ 0 ≤ β . For the e xplosion after τ µ , the proof follo ws the same lines. W e first compare the diffusion with a Bro wnian motion with drift to sho w it reaches c µ ( τ µ ) + 5 β ln β (starting from time τ µ ) within a time smaller than β / 2 . Then we bound from belo w our diffusion by d ˜ q − ( t ) = dW ( t ) + 1 4 − a + exp( − ( t/ 4 + µ − ˜ q − ( t )) /β ) dt . Comparing again this dif fusion with the deterministic solution of the ODE g ′ ( t ) = c exp( − ( c µ ( ξ µ ) − g ( t )) /β ) , with g (0) = c µ ( τ µ ) + 5 β ln β . By working on the high probability ev ent where the Brownian motion ( W ( t ) − W ( τ µ ) , t ≥ τ µ ) does not reach high values, we can pick some well chosen constant c such that this deterministic lower bound explodes within a time β 5 , concluding the proof. □ THE SPECTR UM OF THE STOCHASTIC BESSEL OPERA TOR A T HIGH TEMPERA TURE 13 W e no w focus on the region between the line x = 0 and the critical line t 7→ c µ ( t ) i.e. phase ( B ) . T o simplify the proof, we couple the dif fusions under consideration. Here the coupling is quite simple: the Brownian motion driving q − in (7) and the one dri ving its limiting counterpart r − hav e to be equal. Proposition 3.2 (Comparison with a reflected Brownian motion) . F ix T > 1 (independent of β ). W ith pr obability going to 1 when β → 0 , we have that for all t ∈ [ τ 0 , τ µ ∧ T ] , | q − ( t ) − r − ( t ) | ≤ β 1 / 8 . Pr oof. Note that τ 0 < β with probability going to 1 thanks to the previous lemma; we work on this e vent in the follo wing. Let δ 1 := β 1 / 4 . W e first consider the diffusions up to time τ µ − δ 1 . W e first define two auxiliary dif fusions r 1 and r 2 such that, on an ev ent with probability tending to 1, as β → 0 , the processes q − and r − are squeezed between them: ∀ t ∈ [ τ 0 , τ µ − δ 1 ∧ T ] , r 2 ( t ) ≤ q − ( t ) ≤ r 1 ( t ) , r 2 ( t ) ≤ r − ( t ) ≤ r 1 ( t ) . (11) Let us start with the upper bound . Define ε 1 := exp( − δ 1 /β ) / 2 , and let r 1 be a Brownian motion with drift − a/ 4 + ε 1 , reflected at δ 1 , with starting point r 1 ( τ 0 ) := δ 1 dri ven by the same Bro wnian motion as r − and q − . In the time interval [ τ 0 , τ µ − δ 1 ] , q − is bounded from above by r 1 . Observe indeed that the drift induced by the two exponential terms in (7) in the region { ( t, x ) , t ≥ τ 0 , x ∈ [ δ 1 , c µ − δ 1 ( t )] } is bounded from abov e by ε 1 . Moreov er , we also hav e r − ( t ) ≤ r 1 ( t ) for all t ≥ τ 0 on the ev ent { τ 0 ≤ β , r − ( τ 0 ) ≤ δ 1 } (which has probability tending to 1 ). For the lower bound , let us define r 2 starting from − δ 1 at time τ 0 , following a Bro wnian motion with drift − a/ 4 reflected at − δ 1 dri ven by the same Brownian motion. As long as q − does not reach − δ 1 , the dif fusion r 2 is a lo wer bound for q − . W e must v erify that the probability of q − reaching − δ 1 before τ µ tends to 0 . This is guaranteed by the strong positive drift of q − strictly below 0 . More precisely , consider the stationary diffusion starting at 0 , satisfying d ˜ q ( t ) = ( − a/ 4 + exp( − ˜ q ( t ) /β ) / 4) dt + dW ( t ) . Since ˜ q has a smaller drift than q − , it is more likely to hit − δ 1 . W e compute the probability that ˜ q hits − δ 1 before µ using the scale function. P [ ˜ q hits − δ 1 before µ ] = ´ µ 0 exp( − 2 ´ y 0 ( − a/ 4 + e − x/β / 4) dx ) dy ´ µ − δ 1 exp( − 2 ´ y 0 ( − a/ 4 + e − x/β / 4) dx ) dy . Splitting the integral in the denominator into its integral from − δ 1 to 0 and from 0 to µ , one can see that the numerator term is of order O (1) whereas the denominator gro ws exponentially as β → 0 . Thus this probability tends to 0 . It is also immediate to check that r − is bounded belo w by r 2 as long as r − ( τ 0 ) ≥ − δ 1 , which happens with probability going to 1 . Gathering the bounds, with probability going to 1 , we hav e the inequalities (11). Finally , we bound the difference between r 1 and r 2 . Define the shifted space/time versions ˜ r 1 ( t ) := r 1 ( t + τ 0 ) − δ 1 and ˜ r 2 ( t ) := r 2 ( t + τ 0 ) + δ 1 of r 1 and r 2 so that both are now reflected abov e 0 and start at 0 at time t = 0 . Let s ( t ) := ˜ r 1 ( t ) − ˜ r 2 ( t ) ≥ 0 be their dif ference. W e ha ve: ds ( t ) = ε 1 dt + dL 1 ( t ) − dL 2 ( t ) 14 LA URE DUMAZ AND HUGO MAGALDI where L 1 and L 2 are the local time at 0 of ˜ r 1 and ˜ r 2 respecti vely . It gi ves: d ( s 2 ( t )) = 2 s ( t )( ε 1 dt + dL 1 ( t ) − dL 2 ( t )) Note that L 1 increases only when ˜ r 1 ( t ) = 0 , implying s ( t ) = ˜ r 2 ( t ) ≥ 0 , thus 2 s ( t ) dL 1 ( t ) ≤ 0 . Similarly , − s ( t ) dL 2 ( t ) ≤ 0 . Therefore: s ( t ) 2 ≤ 2 ε 1 ˆ t 0 s ( u ) du . (12) If we define S ( t ) := ´ t 0 s ( u ) du . Since s ( t ) = S ′ ( t ) ≥ 0 , we hav e ( S ′ ( t )) 2 ≤ 2 ε 1 S ( t ) , which implies S ′ ( t ) ≤ √ 2 ε 1 p S ( t ) . Using Bihari LaSalle inequality 1 , we obtain for t ≥ 0 , s ( t ) ≤ ε 1 t . Returning to the original processes for t ≥ τ 0 , we hav e | r 1 ( t ) − r 2 ( t ) | ≤ | ˜ r 1 ( t − τ 0 ) − ˜ r 2 ( t − τ 0 ) + 2 δ 1 | ≤ ε 1 T + 2 δ 1 . Since δ 1 = β 1 / 4 and ε 1 = exp( − β − 3 / 4 ) / 2 , this quantity is bounded by 2 β 1 / 4 for small enough β . Combined with the ordering (11), this concludes the proof up to the time T ∧ τ µ − δ 1 . It remains to extend this bound up to the time τ µ . Suppose that τ µ − δ 1 < T . By comparing q − with a Brownian motion with constant drift − a/ 4 , we see that q − hits the affine line c µ within an additional time of order β 3 / 8 ≫ δ 2 1 with probability going to 1 (note that the drift is irrelev ant o ver such a short interval). Over a time interval β 3 / 8 , the process r − fluctuates less than β 1 / 8 / 2 ≫ β 3 / 16 with ov erwhelming probability . This yields the desired bound up to time τ µ ∧ T . □ Note that the e xact same proofs as Lemma 3.1 and Proposition 3.2 can be applied for the re gime q β = q + as we did not use the specific value of the drift − a/ 4 . In particular , we deduce the follo wing proposition: Proposition 3.3. F ix k ≥ 1 and µ > 0 . W ith pr obability going to 1 , we have: ∀ i ∈ { 1 , · · · , k } , | ξ ± µ,β ( i ) ∧ T − ξ ± µ ( i ) ∧ T | ≤ β 1 / 8 2 k . Pr oof. Note that our control on the trajectories of Proposition 3.2 is a priori not sufficient to control hitting times as two trajectories can be very close in uniform norm but hav e well-separated hitting times of an affine line. It ne vertheless gi ves that if τ µ ≤ T , | q − ( τ µ ) − r − ( τ µ ) | ≤ β 1 / 8 . Therefore, r − should hit µ − β 1 / 8 before τ µ . Moreov er, if again this hitting time ξ − µ − β 1 / 8 (1) is smaller than T ∧ τ µ , we hav e that q − should hit µ − 2 β 1 / 8 before ξ − µ (1) . This giv es: τ µ − 2 β 1 / 8 ∧ T ≤ ξ − µ − β 1 / 8 (1) ∧ T ≤ τ µ ∧ T . But the probability that τ µ − τ µ − 2 β 1 / 8 ≤ β 1 / 8 / 4 tends to 1 when τ µ − 2 β 1 / 8 < ∞ as we can bound from belo w the process q − again by a Bro wnian motion with constant drift starting at c µ − 2 β 1 / 8 ( τ µ − 2 β 1 / 8 ) which has an o verwelming probability to hit c µ within short time (notice again that the drifts are irrelev ant here as we work on a small time-interval). And similarly , for the dif fusion r − , we obtain ξ − µ (1) − ξ − µ − β 1 / 8 (1) ≤ β 1 / 8 / 4 when ξ − µ − β 1 / 8 (1) < ∞ . W e obtain that with probability tending to 1 , we hav e | ξ − µ,β (1) ∧ T − ξ − µ (1) ∧ T | ≤ β 1 / 8 (13) 1 One could av oid using this inequality by introducing the time t 0 := inf { u ≥ 0 , S ( u ) > 0 } which leads to d dt p S ( t ) ≤ √ 2 ε 1 / 2 for t ≥ t 0 . THE SPECTR UM OF THE STOCHASTIC BESSEL OPERA TOR A T HIGH TEMPERA TURE 15 For the next explosion, we work on the ev ent that the ascent of q β = q + from −∞ (right after the explosion time ξ − µ,β (1) ) is smaller than β . This ev ent occurs with overwelming probability thanks to Lemma 3.1. W e also work on the ev ent (13). W e hav e now two dif fusions q + and r + starting at 0 , but at two different starting times τ ′ 0 and τ ′′ 0 separated by at most β 1 / 8 / 2 + β . It suf fices to apply the proof of the previous proposition, using as an imput β 1 / 8 instead of β . W e obtain that | q + ( t ) − r + ( t ) | ≤ β 1 / 64 . for t ∈ [( τ ′ 0 ∨ τ ′′ 0 ) ∧ T , τ ′ µ ∧ T ] where τ ′ µ is the first hitting time of the critical time by q β = q + after time ξ − µ,β (1) . Iterating the proof giv es the result. □ This proposition in particular implies that the explosion times of q β are “macroscopic” (of order O (1) ) as β → 0 with overwelming probability . Indeed, it takes a strictly positiv e time (indepen- dent of β ) for r ± to reach the critical line c µ and the explosion times of q β are all close to these limiting hitting times with high probability . Consequently , the number of explosions occuring before any fixed time T is bounded almost surely . This shows that Proposition 3.3 controls all explosion times of q β up to time T with probability tending to 1 , rather than merely the first k ones. 3.2. Tightness of the explosion times of the diffusion q . W e would like to prov e that for all ε > 0 , there exists T > 0 such that inf β ≤ β 0 P [ ν β [ T , ∞ ) = 0] ≥ 1 − ε . Recall the dynamics of q β µ gi ven by (7) and (8). In the following, we drop the subscript µ to simplify the notations. W e would like to prov e the following lemma: Lemma 3.4 (No explosions after large times) . F or any ε > 0 , ther e exists a time T > 0 and β 0 > 0 , such that after time T , for all β < β 0 , ther e is no explosion of the diffusion q β with pr obability gr eater than 1 − ε . The main difficulty for this part is that we do not know where the diffusion is at time T : in a worst-case scenario, it could be close to the critical line, which would then lead to an explosion after time T . Pr oof. Let us first suppose that a ≥ 0 and take some small β (the argument below will work for all β smaller than some fixed deterministic β 0 ). W e analyze the trajectory starting from time T and show that, on an ev ent of probability tending to 1 when T goes to infinity while at most two explosions may occur in the interval [ T , T 9 ] , there will be no explosion after time T 9 . First, note that if q β is in the q + phase at time T , its drift is bounded from belo w by ( a + 1) / 4 ≥ 1 / 4 . Therefore, it will hit the critical line almost surely . The time it takes to explode is O ( T ) if a > 0 and O ( T 2 ) if a = 0 . In the worst-case scenario ( a = 0 and q + ( T ) = −∞ ), it explodes before time T 3 with high probability (for some large T ), since a Brownian motion with drift 1 / 4 hits the critical line µ + t/ 4 before T 3 with high probability . Therefore, the process is in the q − phase at some time prior to T 3 . Using the strong Markov property , we can restrict our analysis to the case where the process is in the q − phase at time T , b ut we must now prov e that there is no explosion after time T 3 , to ensure there is no explosion after time T 9 for our original process. Fix δ ∈ (0 , 1 / 8) . W e introduce two auxiliary diffusions r 1 and r 2 , driv en by the same Brownian motion as q − . The dif fusion r 1 starts at time T from position 1 and is a reflected Bro wnian motion 16 LA URE DUMAZ AND HUGO MAGALDI abov e 1 with drift − a/ 4 + δ . The diffusion r 2 starts at time 2 T from c µ ( T ) + 3 T / 16 and follo ws a reflected Bro wnian motion with drift − a/ 4 + δ abov e 1 . W e divide the analysis according to the position of q β at time T . • If q β ( T ) ≤ 1 . If β is small enough, the drift of the diffusion q β is bounded from above by the drift of r 1 for all values in [1 , c µ ( t )] (as q β is in its q − phase). Therefore q β stays belo w r 1 as long as r 1 does not hit the critical line. • If q β ( T ) ≥ c µ ( T ) . Then with high probability , q β explodes rapidly thanks to Lemma 3.1. After this explosion time, q β is in its q + phase, which explodes with high probability before time T 3 / 2 using the same arguments as above. Then it is back to its q − phase starting at −∞ . In particular , it stays below r 1 as long as r 1 does not hit the critical line. • If 1 < q β ( T ) < c µ ( T ) . Let τ T := inf { t ≥ T , q β ( t ) = c µ ( t ) } be the next hitting time of the critical line. – If τ T < 2 T , then the diffusion q β explodes quickly after τ T thanks to Lemma 3.1. It then enters the q + phase, explodes again (before time T 3 / 2 ) and re-enters the q − phase at −∞ . It will therefore stay belo w r 1 as long as r 1 does not hit the critical line. – If τ T ≥ 2 T , then during the time interv al [ T , 2 T ] , q β is bounded from above by a reflected Brownian motion with drift − a/ 4 + δ starting at time T at position c µ ( T ) : with probability tending to 1 when T ≫ 1 , it will be belo w c µ ( T ) + 3 T / 16 at time 2 T . (Indeed, the probability that a Bro wnian motion with drift smaller than 1 / 8 ends abov e its starting point plus 3 T / 16 decays exponentially with T ). After time 2 T , on this high probability ev ent, the diffusion q β is therefore bounded by r 2 as long as r 2 does not hit the critical line. In all cases, before time T 9 , the process q − becomes trapped belo w either r 1 or r 2 . Those two dif fusions ha ve a drift smaller than 1 / 8 . Since this is strictly less than the slope of the critical line, the probability that they hit the critical line is exponentially decaying with T (see e.g. Proposition 4.1 which is a more precise statement that implies this fact). Therefore whatev er its phase or position at time T , the diffusion q β will nev er explode after time T 9 on this high probability e vent. The case a < 0 follo ws the exact same lines, except it is simpler as we no longer hav e a phase with a probability of explosion equal to 1 . For either phase, we can bound our dif fusion with reflected Bro wnian motions with drift in a similar way than abov e. □ 3.3. Proof of Proposition 2.1. W e now hav e all the ingredients to conclude the proof of Proposi- tion 2.1, namely the con vergence in law of the random measures ν β µ → ν µ for the weak topology . W e will prov e in fact the stronger con vergence in probability thanks to our coupling. The argument is very standard b ut we chose to include it here for completeness. Recall that ν β µ = P i ≥ 1 δ ξ + µ,β ( i ) and ν µ = P i ≥ 1 δ ξ + µ ( i ) . As the space of finite measures on R + equipped with the weak topology is separable and metrizable, it suffices to show that for any bounded continuous function f : R + → R and any δ > 0 , lim β → 0 P h ⟨ ν β µ , f ⟩ − ⟨ ν µ , f ⟩ > δ i = 0 . Fix such a function f and let ε > 0 . As the total mass ν µ ( R + ) is finite almost surely and its atoms are finite, we can choose a large inte ger K and a large time T such that P ν µ ( R + ) ≤ K and ξ + µ ( K ) ≤ T ≥ 1 − ε/ 3 . (14) THE SPECTR UM OF THE STOCHASTIC BESSEL OPERA TOR A T HIGH TEMPERA TURE 17 By the tightness of the explosion times (Lemma 3.4), we may increase T and K if necessary so that for all β sufficiently small, P ν β µ ([ T , ∞ )) = 0 and ν β µ ( R + ) ≤ K ≥ 1 − ε/ 3 . (15) Let A β denote the intersection of these two ev ents. On A β , both point processes have at most K points, all strictly confined to [0 , T ] , which implies N β := ν β µ ( R + ) = ν µ ( R + ) =: N ≤ K . By Proposition 3.3, the first K hitting times are pathwise close. That is, there exists β 0 > 0 such that for all β < β 0 , the e vent B β := n max 1 ≤ i ≤ K ξ + µ,β ( i ) ∧ T − ξ + µ ( i ) ∧ T ≤ β 1 / 8 K o has probability at least 1 − ε/ 3 . Let ω f ,T denote the modulus of continuity of f on [0 , T ] . On the e vent A β ∩ B β , we hav e ⟨ ν β µ , f ⟩ − ⟨ ν µ , f ⟩ ≤ N X i =1 f ( ξ + µ,β ( i )) − f ( ξ + µ ( i )) ≤ K · ω f ,T β 1 / 8 K . Since ω f ,T ( β 1 / 8 K ) → 0 deterministically as β → 0 , this upper bound is strictly less than δ for β sufficiently small. As P [( A β ∩ B β ) c ] ≤ ε , the desired con vergence in probability follo ws. □ 4. A S Y M P T O T I C S F O R T H E k L A R G E S T E I G E N V A L U E S The goal of this section is to pro vide the proof of Proposition 1.6. Let R ( b ) denote the reflected Bro wnian motion with drift b . Recall that it is given by R ( b ) ( t ) = Y ( b ) ( t ) + sup 0 ≤ u ≤ t max(0 , − Y ( b ) ( u )) where Y ( b ) ( t ) = bt + B ( t ) is a (non-reflected) Bro wnian motion with drift b . In our procedure, we deal with reflected Brownian motions whose drift alternates between − a/ 4 (the − phase) and ( a + 1) / 4 (the + phase). W e define the respectiv e drift parameters as: a 1 := − a/ 4 , a 2 := ( a + 1) / 4 . (16) W e are interested in the e vent where there exist at least k hitting times of c µ by the + phase, which corresponds to 2 k alternating phases hitting the line. When a ≥ 0 , since the final + phase hits the critical line almost surely , the ev ent is a.s. equal to the one where we have at least 2 k − 1 hitting times. When a ∈ ( − 1 , 0) , both e vents are rare e vents, and we need indeed 2 k hitting times. Let τ (1) µ and τ (2) µ denote the first hitting times of c µ by R ( a 1 ) and R ( a 2 ) respecti vely . Note that typically , the diffusions R ( a 1 ) and R ( a 2 ) when a ∈ ( − 1 , 0) do not reach the critical line c µ in a finite time when µ ≫ 1 . Con versely , when a ≥ 0 , R ( a 2 ) reaches it in a finite time almost surely in a typical time of order 4 µ/a (for a > 0 ). 4.1. Large deviation events. W e start by establishing the asymptotic probability that the − phase hits the critical line in a finite time which implies Proposition 1.6 for k = 1 and a ≥ 0 . Proposition 4.1. Let a > − 1 . There e xist a constant C 0 ( a ) > 0 suc h that for all µ > 0 , C − 1 0 ( a ) exp − µ 1 + a 2 ≤ P τ (1) µ < ∞ ≤ C 0 ( a ) exp − µ 1 + a 2 . 18 LA URE DUMAZ AND HUGO MAGALDI Pr oof. W e apply the Girsanov formula to change the drift of the reflected Brownian motion from a 1 = − a/ 4 to a constant drift b > 1 / 4 so that the line is hit almost surely . Denote by τ b the first hitting time of c µ by R ( b ) . W e have P τ (1) µ < ∞ = E [exp( G τ b ( Y ( b ) ))1 { τ b < ∞} ] , (as the change of drift is constant, Novikov’ s condition is tri vially satisfied on finite interv als: one applies the change of measure up τ b ∧ T and passes to the limit as T → ∞ ). At the hitting time τ b , the exponent of the Radon-Nik odym deriv ativ e is: G τ b ( Y ( b ) ) = ( a 1 − b )( µ + τ / 4 − L ( b ) ( τ b )) − 1 2 τ b ( a 2 1 − b 2 ) = ( a 1 − b ) µ + ( b − a 1 ) L ( b ) ( τ b ) + τ b a 1 − b 4 − a 2 1 − b 2 2 . (17) Let us choose b such that the coefficient in front of the time τ b v anishes. It gives b ∗ := ( a + 2) / 4 . W ith this choice, the exponent is equal to G τ b ∗ ( Y ( b ∗ ) ) = − µ a + 1 2 + a + 1 2 L ( b ∗ ) ( τ b ∗ ) . One can simply bound the local time by: 0 ≤ L ( b ∗ ) ( τ b ∗ ) ≤ L ( b ∗ ) ( ∞ ) . The random v ariable L ( b ∗ ) ( ∞ ) = sup t ≥ 0 ( − B ( t ) − b ∗ t ) follo ws an exponential distribution with parameter 2 b ∗ = ( a + 2) / 2 . Therefore, E [exp((( a + 1) / 2) L ( b ∗ ) ( ∞ ))] = a + 2 2 ˆ ∞ 0 exp( − x/ 2) dx . The expectation E [exp( a +1 2 L ( b ∗ ) (+ ∞ ))] is bounded abov e by a + 2 > 0 , which giv es the desired upper bound. The lower bound follows directly from the fact that L ( b ∗ ) ≥ 0 and P [ τ b ∗ < ∞ ] = 1 . □ The exact same proof gi ves the follo wing asymptotics for R ( a 2 ) when a ∈ ( − 1 , 0) . Proposition 4.2. Let a > − 1 . There e xist a constants C 0 ( a ) > 0 suc h that for all µ > 0 , C − 1 0 ( a ) exp − µ | a | 2 ≤ P τ (2) µ < ∞ ≤ C 0 ( a ) exp − µ | a | 2 . T o compute the probability of n successiv e hitting times, we must optimize the trajectory , and choose appropriate duration for each of the hitting times. Proposition 4.3. Let a > − 1 and i ∈ { 1 , 2 } . F ix ε > 0 and δ > 0 . Recall fr om (16) the definition of a i . Define t ∗ i := 1 / | a i − 1 / 4 | and the rate functions: I i ( t ) := (1 + (1 / 4 − a i ) t ) 2 2 t . Then, ther e exists a constant C := C ( δ, ε, a ) depending only on a , δ and ε such that, for all time t ∈ [ ε, t ∗ i − ε ] , and all µ > 0 , C − 1 µ − 1 / 2 exp − µ I i ( t ) ≤ P τ ( i ) µ ∈ [ µt, µt + δ ] ≤ C exp − µ I i ( t ) . Furthermor e, for the initial interval [0 , µ ε ] , there exists C 0 ( a ) depending only on a such that for i = 1 , 2 , and for all µ > 0 , P τ ( i ) µ ∈ [0 , µ ε ] ≤ C 0 ( a ) exp − µ I i ( ε ) . Remark 4.4. Note that the pr obabilities are increasing with the time t up to their optimal value at t ∗ i = 4 / ( a + 1) for i = 1 and t ∗ i = 4 / | a | for i = 2 . THE SPECTR UM OF THE STOCHASTIC BESSEL OPERA TOR A T HIGH TEMPERA TURE 19 Pr oof. T ake i ∈ { 1 , 2 } . One can again apply Girsanov’ s formula to change the drift of Y ( a i ) to Y ( b ) . Note that by construction, we will always accelerate time meaning we take b > a i . Denote by τ b the first hitting time of c µ by R ( b ) . W e have P τ ( i ) µ /µ ∈ [ t, t + δ /µ ] = E [exp( G τ b ( Y ( b ) ))1 { τ b /µ ∈ [ t,t + δ /µ ] } ] , with G T ( Y ( b ) ) = ( a i − b )( Y T − Y 0 ) − 1 2 T ( a 2 i − b 2 ) . At time T = τ b , we get G τ b ( Y ( b ) ) = ( a i − b )( Y ( τ b ) − Y 0 ) − 1 2 τ ( a 2 i − b 2 ) = ( a i − b )( µ + τ b / 4 − L ( b ) ( τ b )) − 1 2 τ ( a 2 i − b 2 ) = − ( b − a i ) µ − τ b ( b − a i ) / 4 + τ b ( b − a i )( a i + b ) / 2 + ( b − a i ) L ( b ) ( τ b ) . Denote I ( b, s ) := ( b − a i ) 1 + s 4 − s 2 ( b − a i )( a i + b ) . W e hav e G τ b ( Y ( b ) ) = − µI ( b, τ b /µ ) + ( b − a i ) L ( b ) ( τ b ) . W e want to minimize the exponent by taking the supremum over b of the quadratic function I ( b, s ) . The unconstraint maximum of I ( b, s ) is reached at b ∗ = 1 / 4 + 1 /s and its value is I ( b ∗ , s ) = 1 + ( 1 4 − a i ) s 2 2 s Moreov er , we can bound L ( b ) ( τ b ) by L ( b ) ( ∞ ) . The random variable L ( b ) ( ∞ ) = sup t ≥ 0 ( − B ( t ) − bt ) follows an e xponential distribution with parameter 2 b . Therefore, E [exp(( b − a i ) L ( b ) ( ∞ ))] = (2 b ) ˆ ∞ 0 exp( − bx − a i x ) dx . The last integral is finite iff b + a i > 0 and equals 2 b/ ( b + a i ) . When we choose b = b ∗ , this always holds for i = 2 . It also holds for i = 1 since we restricted the times to t ≤ t ∗ 1 = 4 / ( a + 1) < 4 / ( a − 1) for a > 1 (when a ∈ ( − 1 , 1) , it is alw ays satisfied). Let us first examine the case i = 2 . Then we obtain the upper bound P τ (2) µ /µ ∈ [ t, t + δ /µ ] ≤ C exp − µ 1 2( t + δ /µ ) + 1 2 ( a 4 ) 2 t − a 4 where C is some constant depending only on a . For the lo wer bound, using that L ( b ) ( τ b ) ≥ 0 , we obtain P τ (2) µ /µ ∈ [ t, t + δ /µ ] ≥ p 0 ( µ ) exp − µ 1 2 t + 1 2 ( a 4 ) 2 ( t + δ /µ ) − a 4 , where p 0 ( µ ) := P R ( b ∗ ) reaches c µ in the time interv al [ µt, µt + δ ] . 20 LA URE DUMAZ AND HUGO MAGALDI Recall that the drift is b ∗ = 1 / 4 + 1 /t and R ( b ∗ ) ( s ) = B ( s ) + b ∗ s + L ( b ∗ ) ( s ) . Let l > 0 . On the e vent L ( b ∗ ) ( µt ) ≤ l , we ha ve L ( b ∗ ) ( s ) ≤ l for all s , and we obtain: p 0 ( µ ) ≥ P L ( b ∗ ) ( µt ) ≤ l , sup s ≤ µt ( B ( s ) + s/t ) ≤ µ − l , B ( µt + δ ) ≥ − δ t . Using Marko v property at time µt , we obtain the product p 0 ( µ ) ≥ P L ( b ∗ ) ( µt ) ≤ l , sup s ≤ µt ( B ( s ) + s/t ) ≤ µ − l , B ( µt ) ∈ [ − l − 1 , − l ] (18) × i nf l 0 ∈ [ l,l +1] P B ( δ ) ≥ l 0 − δ t . (19) The probability (18) is bounded by the intersection of three e vents: • { B ( µt ) ∈ [ − l − 1 , − l ] } . By Gaussian scaling, it is of order O (1 / √ µ ) . • Conditioned on the endpoint B ( µt ) + µ t/t = x ∈ [ µ − l − 1 , µ − l ] , the process Y x ( s ) := B ( s ) + s/t is a Brownian bridge of length µt from 0 to x . W e require sup s ≤ µt Y x ( s ) ≤ µ − l . The probability that a bridge of length T ending at y stays belo w a barrier A ≥ y is exactly 1 − exp( − 2 A ( A − y ) /T ) (see e.g. Proposition 8.1 in [ 11 ]). Substituting A = µ − l , y = x , and T = µt , we obtain A − y = µ − l − x := ˜ x ∈ [0 , 1] . The conditional probability is therefore: 1 − exp − 2( µ − l ) ˜ x µt − → µ →∞ 1 − exp − 2 ˜ x t > 0 . Thus, the probability of the path staying below the line is bounded belo w by a strictly positi ve constant. • { L ( b ∗ ) ( µt ) ≤ l } for the conditioned bridge Y x , which holds if inf s ≤ µt ( Y x ( s ) + s/ 4) ≥ − l . Adding the linear drift s/ 4 to the Brownian bridge Y x ( s ) simply yields a new Bro w- nian bridge of length µt , starting at 0 and ending at y ′ := x + µt/ 4 . By symmetry , the probability that its infimum stays abo ve − l is equiv alent to the supremum of a bridge end- ing at − y ′ staying belo w l . Using the same identity as above from [ 11 ], this probability is exactly 1 − exp( − 2 l ( l + y ′ ) /µt ) . Substituting y ′ , the e xponent con verges asymptotically: 2 l ( l + x + µt/ 4) µt − → µ →∞ 2 l 1 t + 1 4 = 2 b ∗ l . Thus, this conditional probability con verges to 1 − e − 2 b ∗ l . By taking l large enough so that the last probability is sufficiently close to 1 , we obtain a strictly positi ve probability for the intersection of the three ev ents. Then we get a positiv e probability for the e vent (19) (decreasing with l , but this is a fix ed parameter), completing the proof. Let us now examine the case i = 1 that is a i = − a/ 4 . As we ask that t < 4 / ( a + 1) − ε , this implies that 1 /t + 1 / 4 > a/ 4 , therefore we can choose b = b ∗ and we obtain the upper bound: P τ (1) µ /µ ∈ [ t, t + δ /µ ] ≤ C exp − µ 1 2( t + δ /µ ) + 1 2 ( 1 + a 4 ) 2 t + 1 + a 4 ! . where C is some absolute constant depending only on a . The lo wer bound is similar to the case i = 2 . For the initial interval [0 , µε ] , the upper bound is obtained by e valuating the supremum of the exponentially small probabilities at t = ε . □ THE SPECTR UM OF THE STOCHASTIC BESSEL OPERA TOR A T HIGH TEMPERA TURE 21 4.2. Proof of Proposition 1.6 for a ≥ 0 . Let us now prove the desired proposition for a ≥ 0 . W e discretize the time intervals to bound the probability of multiple hitting times. For clarity , we write it in the case n = 3 (which corresponds to the e vent { λ 2 ≥ µ } ) although it naturally extends to any n . Let us fix a sufficiently large constant M > a + 2 such that the probabilities P ( τ ( i ) µ ≥ µM ) become exponentially negligible in front of the expected decay . Note as well that when ε is small enough, we also hav e that P ( τ ( i ) µ ≤ µε ) is exponentially negligible. W e then partition [ µε, µM ] into a grid of size δ = 1 , letting the integers k i ∈ K := {⌊ εµ ⌋ , · · · , ⌈ M µ ⌉} for i = 1 , 2 . W e define the successi ve boundary heights at the end of each phase: H 1 ( k 1 ) := µ + k 1 / 4 , H 2 ( k 1 , k 2 ) := H 1 ( k 1 ) + k 2 / 4 . Using the strong Markov property and the union bound over the elements, we obtain the upper bound P ( λ 2 ≥ µ ) ≤ µM 2 sup k 1 ,k 2 ∈ K h P τ (1) µ ∈ [ k 1 , k 1 + 1] P τ (2) H 1 ∈ [ k 2 , k 2 + 1] P τ (1) H 2 < ∞ i + E ( ε, M ) where E ( ε, M ) contains the exponentially negligible terms. Similarly , restricting the trajectory to the most probable combination k 1 , k 2 gi ves a v ery close lower bound: P ( λ 2 ≥ µ ) ≥ sup k 1 ,k 2 ∈ K h P τ (1) µ ∈ [ k 1 , k 1 + 1] P τ (2) H 1 ∈ [ k 2 , k 2 + 1] P τ (1) H 2 < ∞ i . By substituting the e xponential estimates from Proposition 4.3 and Proposition 4.1, up to poly- nomial factors in µ , the probability scales e xponentially as: exp − inf k 1 ,k 2 ∈ K µ I 1 ( k 1 /µ ) + H 1 I 2 ( k 2 /H 1 ) + H 2 a + 1 2 . Let s 1 = k 1 /µ and s 2 = k 2 /H 1 (note that k 2 ≤ M /µ implies s 2 ≤ M µ/H 1 ≤ M ). Because the rate functions I 1 and I 2 are uniformly continuous on the compact domain [ ε, M ] , ev aluating this discrete infimum over the fine grid con verges exactly to the continuum infimum ov er the real- v alued relativ e times s 1 , s 2 ∈ [ ε, M ] . Furthermore, because the heights scale multiplicativ ely as H 1 = µ (1 + s 1 / 4) and H 2 = H 1 (1 + s 2 / 4) , we can factor the height v ariables out of the exponent which giv es for the minimal cost: µ inf s 1 ,s 2 ∈ [ ε,M ] h I 1 ( s 1 ) + 1 + s 1 / 4 inf s 2 I 2 ( s 2 ) + 1 + s 2 / 4 a + 1 2 i . For the probability { λ k ≥ µ } , applying the exact same grid discretization, leads to an expo- nential decay of the form exp( − µC k ) , where the sequence of optimal costs C k is defined by the follo wing recursion. Let V n ( H ) be the cost starting at boundary height H to have more than n hitting times of the critical line. It is giv en by V n ( H ) = C n H and we hav e the recursion relation: V n ( H ) = H min t h 1 + (1 / 4 − a n ) t 2 2 t + C n − 1 (1 + t/ 4) i , where a n := − a/ 4 if n is odd, and a n := ( a + 1) / 4 if n is ev en. Using the f act that the minimum of t 7→ A/t + B t when A > 0 and B > 0 is reached at p A/B and its value is equal to 2 √ AB , this gi ves the recursi ve relation: C n = (1 / 4 − a n ) + C n − 1 + p (1 / 4 − a n ) 2 + C n − 1 / 2 . (20) The sequence C n admits a closed-form solution, which we prov e by induction. 22 LA URE DUMAZ AND HUGO MAGALDI Lemma 4.5 (Explicit Exponential Costs) . F or all n ≥ 1 , the sequence defined by (20) satisfies: C 2 n − 1 = n ( a + n ) 2 , C 2 n = n ( a + n + 1) 2 . Pr oof. W e proceed by induction on n . W e already know that C 0 = 0 and C 1 = ( a + 1) / 2 from Proposition 4.1. Assume the formula holds for 2 k − 1 , then for the e ven step 2 k , the term inside the square root of (20) becomes: a 2 16 + C 2 k − 1 2 = ( a + 2 k ) 2 16 . Substituting this back into the recurrence gi ves: C 2 k = k ( a + k + 1) 2 . Similarly , for the odd step 2 k + 1 , using C 2 k = k ( a + k +1) 2 , C 2 k +1 = a + 1 4 + C 2 k + r ( a + 1) 2 16 + C 2 k 2 . W e focus on the term inside the square root: ( a + 1) 2 16 + k ( a + k + 1) 4 = ( a + 2 k + 1) 2 16 . T aking the square root and adding the remaining terms yields: C 2 k +1 = ( k + 1)( a + k + 1) 2 . This concludes the induction. □ T o conclude the proof of Proposition 1.6, we recall that observing k points above the lev el µ strictly requires completing 2 k − 1 alternating phases of the diffusions (starting and ending with the − a/ 4 drift phase hitting the critical line). Therefore, the asymptotic probability is precisely gov erned by C 2 k − 1 : lim µ →∞ 1 µ ln P [ M a [ µ, ∞ ) ≥ k ] = − C 2 k − 1 = − k ( a + k ) 2 . 4.3. Extension to a ∈ ( − 1 , 0) . W e briefly detail how the previous analysis naturally extends to the regime a ∈ ( − 1 , 0) . In this regime, recall that the drift of the + phase is a 2 = ( a + 1) / 4 < 1 / 4 , meaning both the − and + phases are strictly slo wer than the critical line. Because the final + phase no longer hits the critical line almost surely , observing k points abo ve the le vel µ requires ev aluating the lar ge de viation cost of all 2 k phases. Let ˜ C n denote the optimal cost of a trajectory with n phases ending in the + phase. The sequence satisfies the exact same recurrence as (20), but with shifted parity: the final phase is a + phase, so ˜ a n = ( a + 1) / 4 for odd n , and − a/ 4 for even n . For n = 1 , substituting ˜ a 1 = ( a + 1) / 4 and ˜ C 0 = 0 into the recurrence yields: ˜ C 1 = − a 4 + r a 2 16 = − a 4 + | a | 4 = − a 2 , where we used the fact that a < 0 . THE SPECTR UM OF THE STOCHASTIC BESSEL OPERA TOR A T HIGH TEMPERA TURE 23 Iterating the recurrence (20), an induction similar to Lemma 4.5 yields the exact closed-form sequence for n = 2 k : ˜ C 2 k = k 2 − k a 2 = k ( k + | a | ) 2 . Thus, the asymptotic probability is gov erned by: lim µ →∞ 1 µ ln P [ M a [ µ, ∞ ) ≥ k ] = − k ( k + | a | ) 2 . Notice that substituting a ≥ 0 into our previous result C 2 k − 1 = k ( k + a ) / 2 giv es the expression k ( k + | a | ) / 2 . R E F E R E N C E S [1] Romain Allez, Jean-Philippe Bouchaud, and Alice Guionnet. In variant β -ensembles and the Gauss-Wigner crossov er . Physical Review Letters , 109(9):094102, 2012. [2] Romain Allez and Laure Dumaz. From sine kernel to Poisson statistics. Electr onic J ournal of Pr obability , 19(114):1–25, 2014. [3] Romain Allez and Laure Dumaz. Tracy-Widom at high temperature. J ournal of Statistical Physics , 156(6):1146– 1183, 2014. [4] Laure Dumaz and Cyril Labb ´ e. The stochastic Airy operator at large temperature. The Annals of Applied Pr oba- bility , 32(6):4481–4534, 2022. [5] Laure Dumaz, Y un Li, and Benedek V alk ´ o. Operator level hard-to-soft transition for β -ensembles. Electr onic Journal of Pr obability , 26:1–28, 2021. [6] I. Dumitriu and A. Edelman. Matrix models for beta ensembles. Journal of Mathematical Physics , 43:5830–5847, 2002. [7] Alan Edelman and Brian D. Sutton. From Hermitian matrices to stochastic operators. Journal of Statistical Physics , 127(6):1121–1165, 2007. [8] Peter J. Forrester . Log-Gases and Random Matrices . London Mathematical Society Monographs. Princeton Uni- versity Press, Princeton, 2010. [9] Adrien Hardy and Gaultier Lambert. CL T for circular beta-ensembles at high temperature. Journal of Functional Analysis , 280(7):108869, 2021. [10] O. Kallenberg. Random Measur es . Academic Press, New Y ork, 4th edition, 1986. [11] I. Karatzas and S. E. Shreve. Brownian Motion and Stochastic Calculus . Graduate T exts in Mathematics. Springer , 2nd edition, 1991. [12] Fumihiko Nakano and Khanh Duy T rinh. Gaussian beta ensembles at high temperature: eigen value fluctuations and bulk statistics. J ournal of Statistical Physics , 173(2):295–321, 2018. [13] Fumihiko Nakano and Khanh Duy T rinh. Poisson statistics for beta ensembles on the real line at high temperature. Journal of Statistical Physics , 179(3):632–649, 2020. [14] Cambyse Pakzad. Poisson statistics at the edge of Gaussian β -ensemble at high temperature. ALEA, Latin Ameri- can Journal of Pr obability and Mathematical Statistics , 16:871–892, 2019. [15] Jos ´ e A. Ram ´ ırez and Brian Rider . Dif fusion at the random matrix hard edge. Communications in Mathematical Physics , 288(3):887–906, 2009. [16] D. Revuz and M. Y or . Continuous Martingales and Br ownian Motion . Springer, 3rd edition, 1999. [17] Paav o Salminen and Marc Y or . On hitting times of af fine boundaries by reflecting Brownian motion and Bessel processes. P eriodica Mathematica Hungarica , 62(2):187–201, 2011. [18] Hoang Dung T rinh and Khanh Duy Trinh. Beta Laguerre ensembles in global regime. Osaka Journal of Mathe- matics , 58(2):435–450, 2021. C N R S & D E PA RT M E N T O F M ATH E M AT I C S A N D A P P L I C A T I O N S , ´ E C O L E N O R M A L E S U P ´ E R I E U R E ( P A R I S ) , 4 5 RU E D ’ U L M , 7 5 0 0 5 P A R I S , F R A N C E Email addr ess : laure.dumaz@ens.fr Email addr ess : magaldi.hugo@gmail.com

Original Paper

Loading high-quality paper...

Comments & Academic Discussion

Loading comments...

Leave a Comment