OneCast: Structured Decomposition and Modular Generation for Cross-Domain Time Series Forecasting

Reading time: 2 minute

...

📝 Original Info

- Title: OneCast: Structured Decomposition and Modular Generation for Cross-Domain Time Series Forecasting

- ArXiv ID: 2510.24028

- Date: 2025-10-28

- Authors: ** 논문에 명시된 저자 정보가 제공되지 않았습니다. **

📝 Abstract

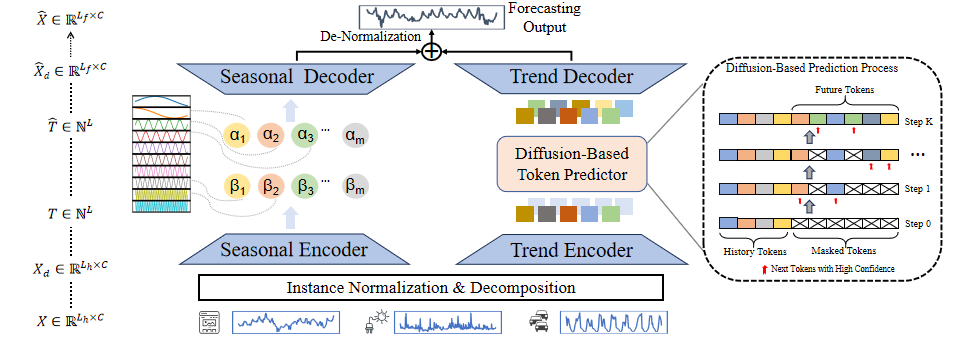

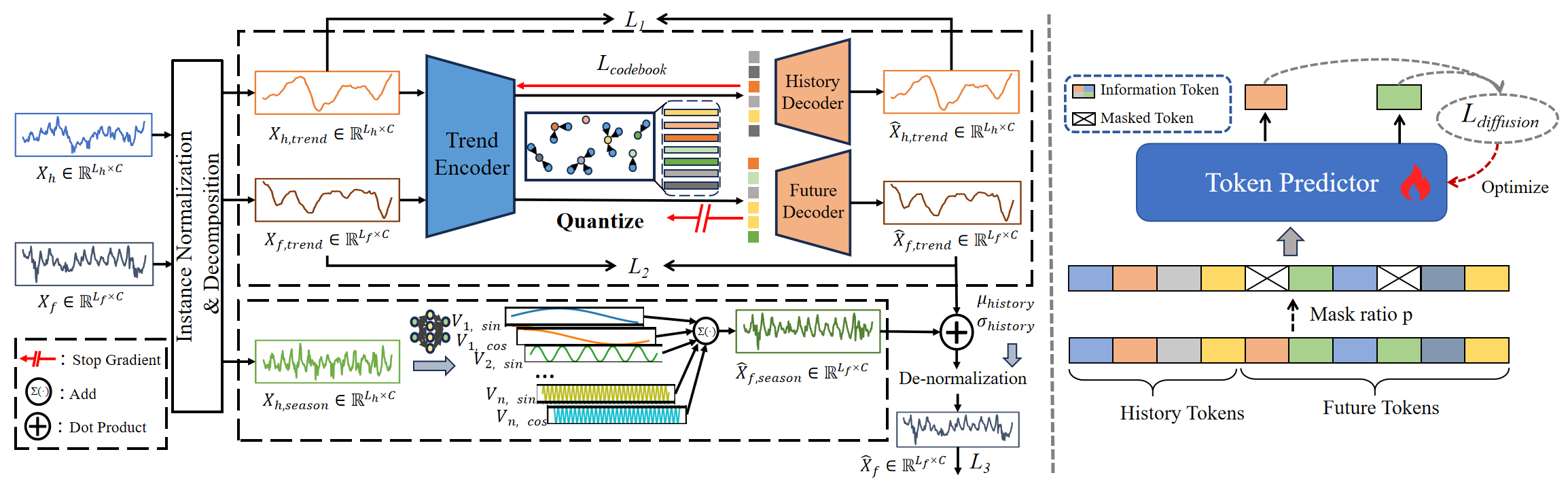

Cross-domain time series forecasting is a valuable task in various web applications. Despite its rapid advancement, achieving effective generalization across heterogeneous time series data remains a significant challenge. Existing methods have made progress by extending single-domain models, yet often fall short when facing domain-specific trend shifts and inconsistent periodic patterns. We argue that a key limitation lies in treating temporal series as undifferentiated sequence, without explicitly decoupling their inherent structural components. To address this, we propose OneCast, a structured and modular forecasting framework that decomposes time series into seasonal and trend components, each modeled through tailored generative pathways. Specifically, the seasonal component is captured by a lightweight projection module that reconstructs periodic patterns via interpretable basis functions. In parallel, the trend component is encoded into discrete tokens at segment level via a semantic-aware tokenizer, and subsequently inferred through a masked discrete diffusion mechanism. The outputs from both branches are combined to produce a final forecast that captures seasonal patterns while tracking domain-specific trends. Extensive experiments across eight domains demonstrate that OneCast mostly outperforms state-of-the-art baselines.💡 Deep Analysis

📄 Full Content

📸 Image Gallery

Reference

This content is AI-processed based on open access ArXiv data.