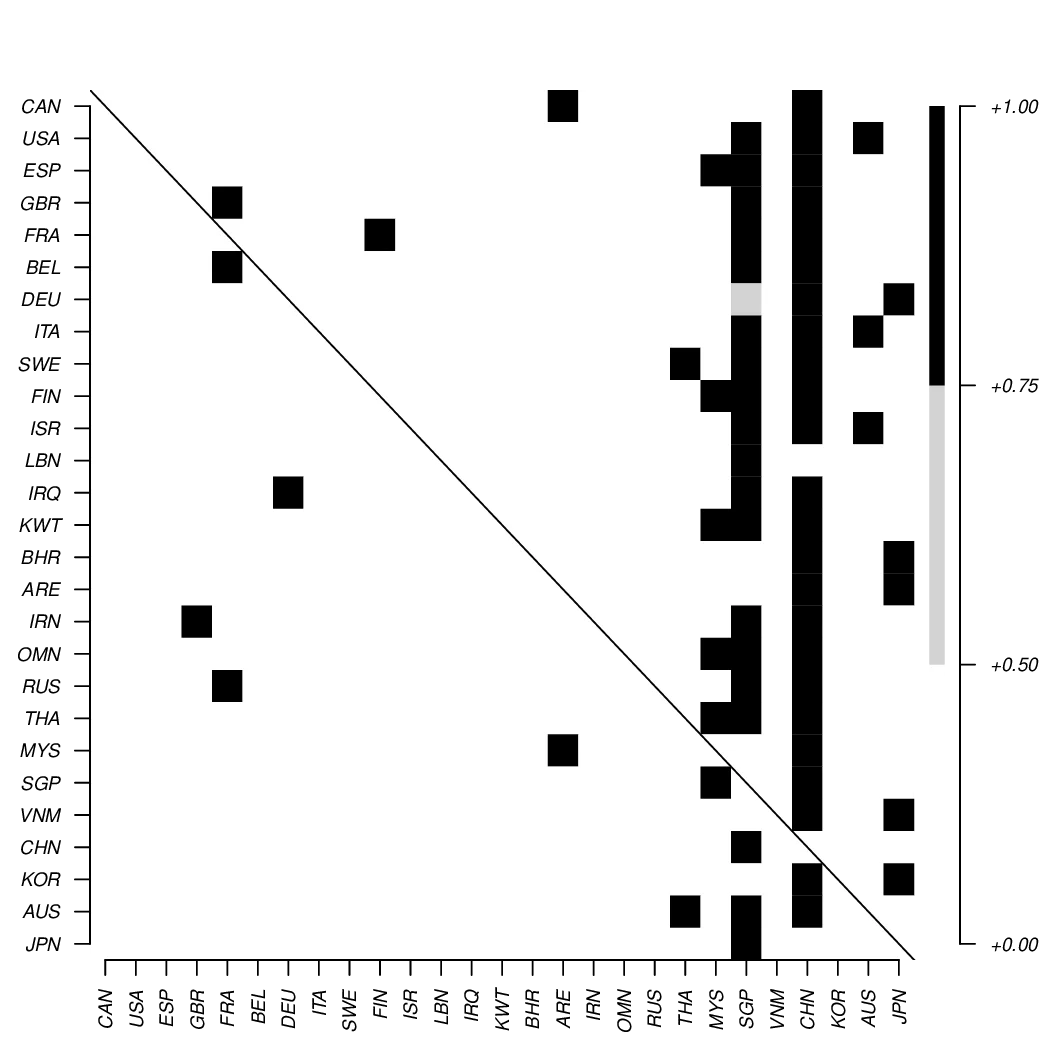

A Bayesian approach for estimation of weight matrices in spatial autoregressive models

We develop a Bayesian approach to estimate weight matrices in spatial autoregressive (or spatial lag) models. Datasets in regional economic literature are typically characterized by a limited number of time periods T relative to spatial units N. When