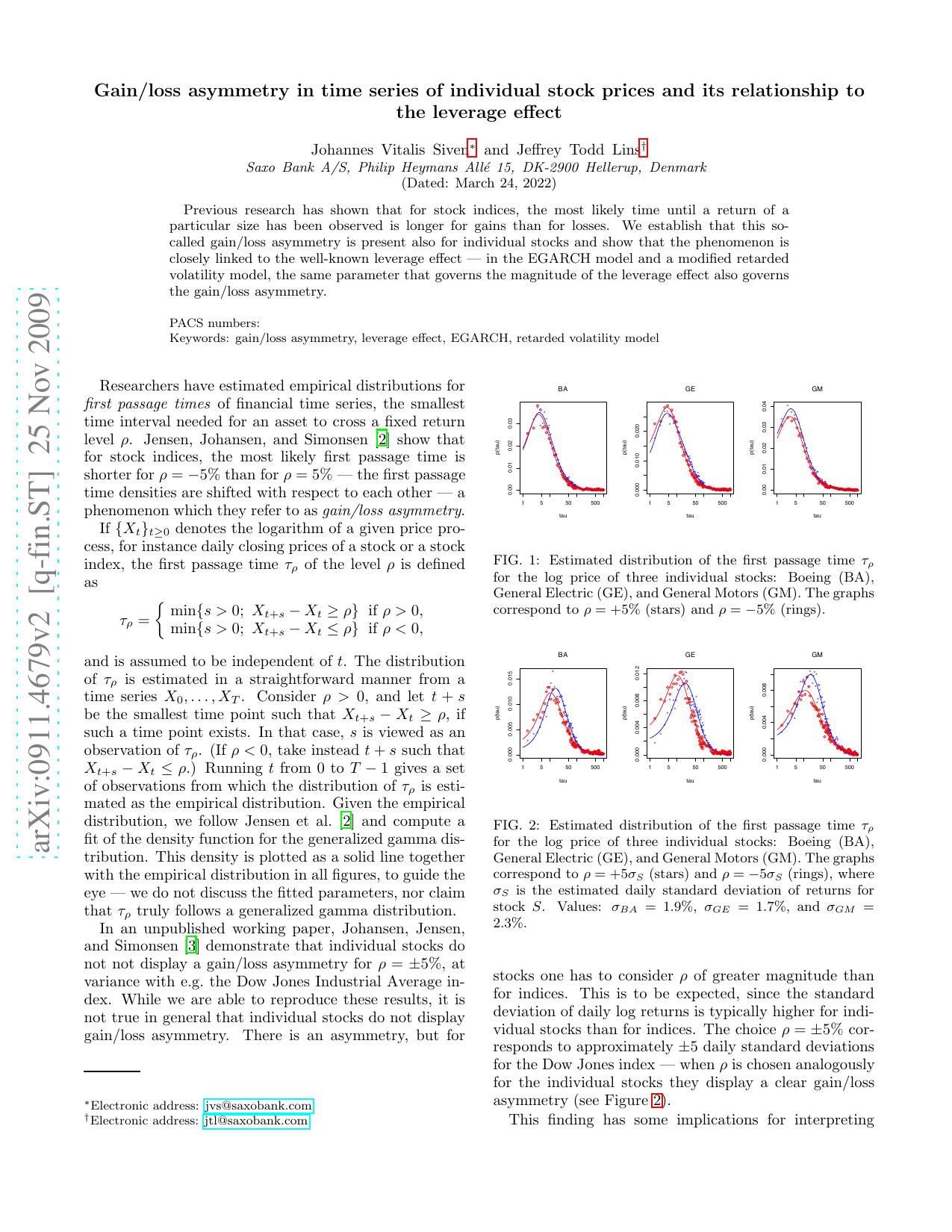

Statistical analysis of the overnight and daytime return

We investigate the two components of the total daily return (close-to-close), the overnight return (close-to-open) and the daytime return (open-to-close), as well as the corresponding volatilities of the 2215 NYSE stocks from 1988 to 2007. The tail distribution of the volatility, the long-term memor

Analysis

Quantitative Finance

![Correction to 'Leverage and volatility feedback effects in high-frequency data' [J. Financial Econometrics 4 (2006) 353--384]](/images/papers/0902.0713/cover.png)