Ordering Power is Sanctioning Power: Sanction Evasion-MEV and the Limits of On-Chain Enforcement

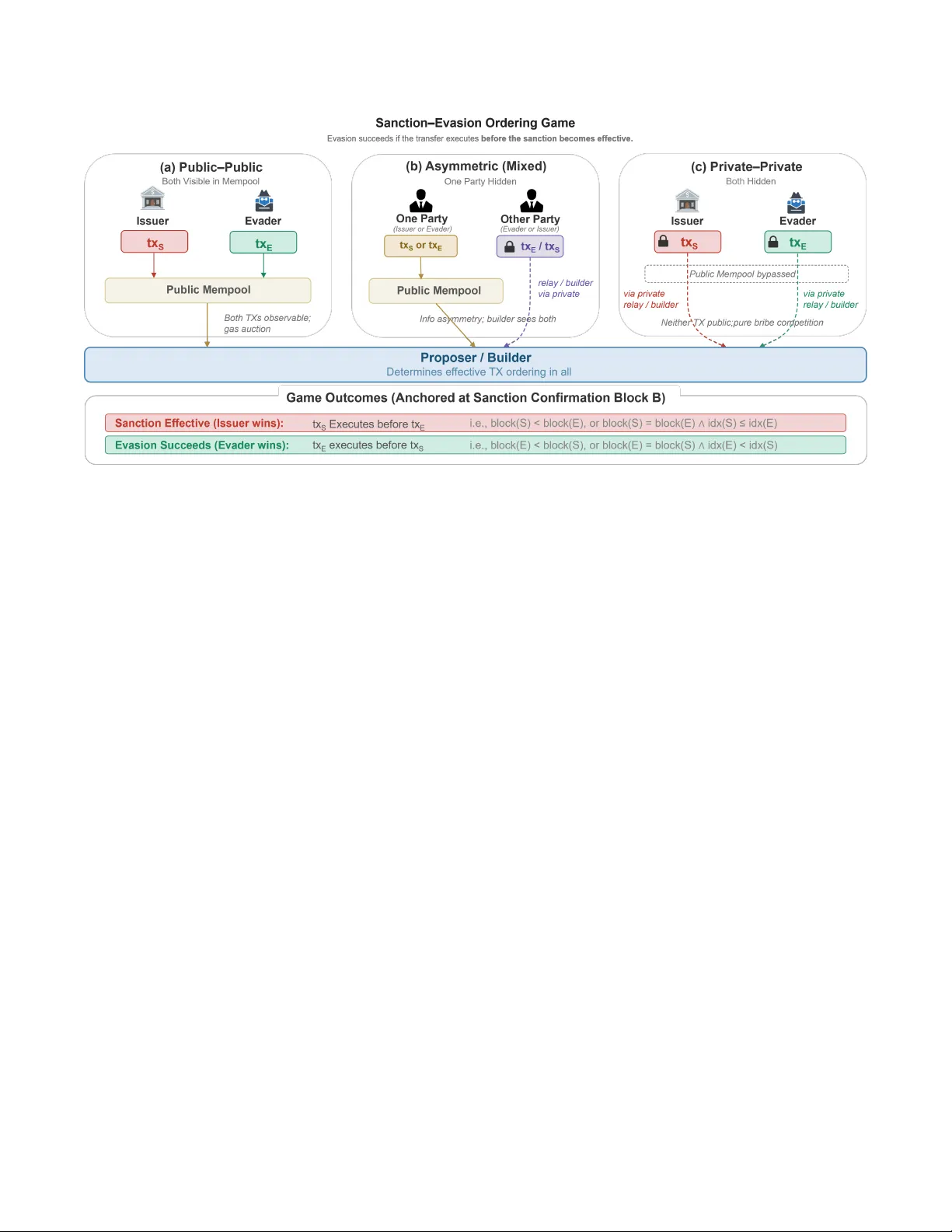

Centralized stablecoins such as USDT and USDC enforce financial sanctions through contract-layer blacklist functions, yet on public blockchains a freeze is merely an ordinary transaction that must compete for execution priority. We identify a fundame…

Authors: Di Wu, Yuman Bai, Shoupeng Ren