From Heard to Lived Opinions: Simulating Opinion Dynamics with Grounded LLM Agents in Economic Environments

Opinion dynamics (OD) studies how individual opinions evolve and generate collective patterns such as consensus and polarization. While recent work explores OD using populations of LLM-based agents focusing on opinion exchange, it typically does not …

Authors: Ryuji Hashimoto, Masahiro Kaneko, Ryosuke Takata

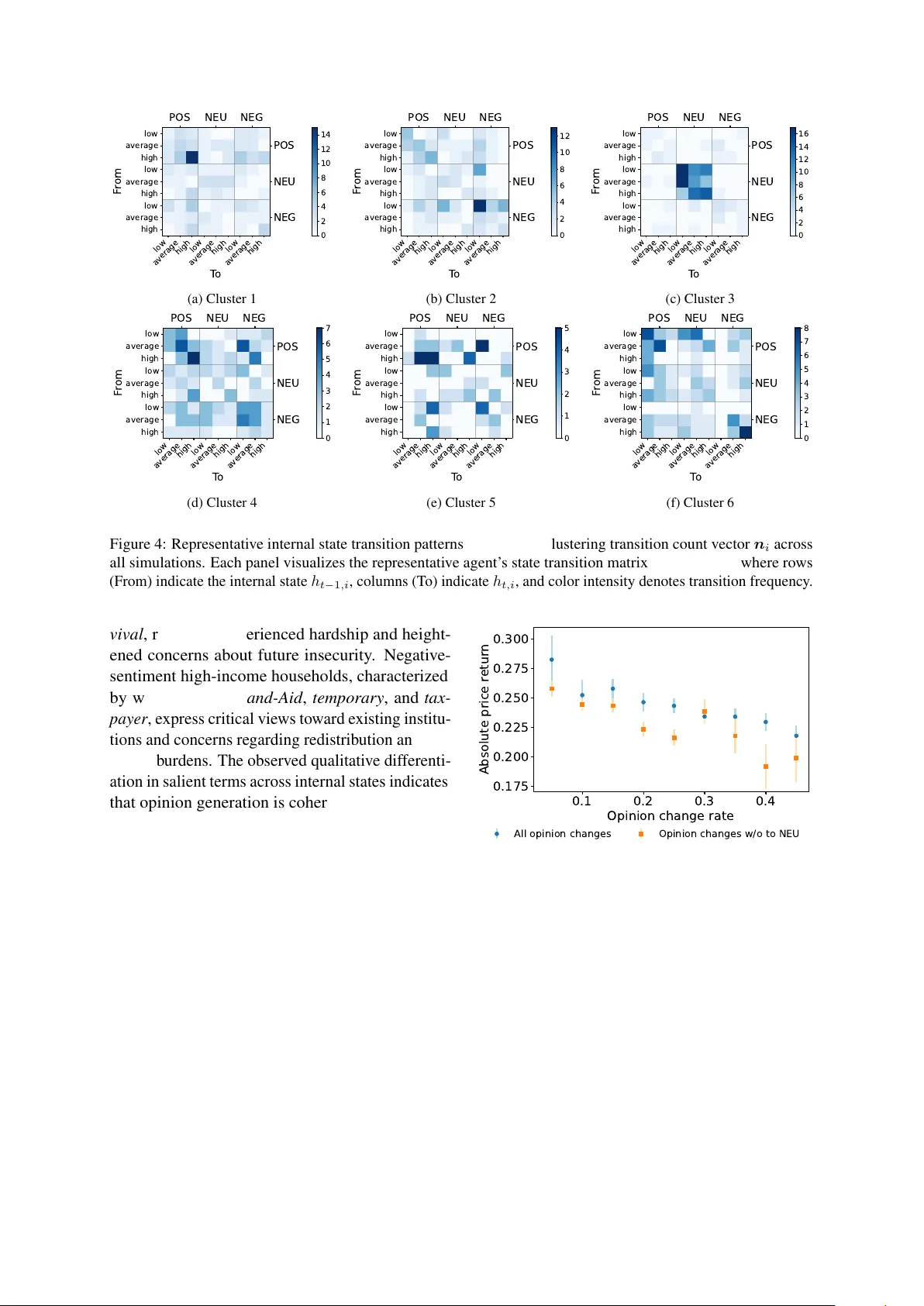

Fr om Heard to Liv ed Opinions: Simulating Opinion Dynamics with Gr ounded LLM Agents in Economic En vir onments Ryuji Hashimoto 1,2 , Masahiro Kanek o 1,3 , Ry osuke T akata 1,2 , T akehiro T akayanagi 1,2 , Kiy oshi Izumi 1,2 , 1 Simulacra Inc., 2 The Uni versity of T okyo, 3 MBZU AI Correspondence: r_hashimoto@simulacra.co.jp Abstract Opinion dynamics (OD) studies how individ- ual opinions ev olve and generate collectiv e pat- terns such as consensus and polarization. While recent work explores OD using populations of LLM-based agents focusing on opinion e x- change, it typically does not incorporate indi- viduals’ liv ed experiences, such as economic outcomes of past decisions, which play a crit- ical role in shaping opinions. W e propose a nov el OD simulation frame work that grounds LLM-based agents in an economic en viron- ment, allowing them to act and receive envi- ronmental feedback. Our simulations exhibit coherent OD at both indi vidual and popula- tion le vels: individual opinions follo w struc- tured trajectories shaped by economic experi- ences, with adverse conditions inducing opin- ion rigidity , while at the population le vel, col- lectiv e opinions co-move with economic con- ditions, with inequality amplifying polariza- tion and price instability driving larger distri- butional shifts. These results highlight the im- portance of grounding LLM-based agents in en vironments to capture collective OD. 1 Introduction Research in opinion dynamics (OD) examines ho w indi vidual opinions form and update through inter- actions, giving rise to collecti ve patterns ( DeGroot , 1974 ; Hegselmann and Krause , 2002 ). Collecti ve opinion distributions are not mere aggre gations of indi vidual opinions; rather, they emerge through nonlinear interactions among individuals ( Castel- lano et al. , 2009 ). Because such dynamics influence political decision-making and the stability of eco- nomic and social institutions, understanding opin- ion formation and distribution is fundamental to social analysis ( T ucker , 2023 ). Recently , large language models (LLMs) ha ve been applied to OD simulations ( Cau et al. , 2025 ; Chuang et al. , 2024 ; Cisneros-V elarde , 2025 ) due to their ability to update opinions through lan- guage–le vel semantic understanding, to represent multifaceted opinions without predefining top- ics, and to naturally capture human-like values. Prior studies demonstrate that LLM-based OD are shaped by confirmation bias and framing ef- fects ( Chuang et al. , 2024 ), as well as by the content and style of dialogue ( Cau et al. , 2025 ). Ho we ver , most existing OD studies focus pri- marily on opinion exchange, with opinion change dri ven largely by linguistic interaction. In con- trast, real-world opinion formation is also shaped by lived experiences, such as economic actions and their consequences, which are largely absent from language-only simulations. For example, exposure to economic threat can induce rigidity in attitudes ( Staw et al. , 1981 ). Like wise, eco- nomic inequality has been shown to foster polar - ization ( Ste wart et al. , 2020 ). Prior work lacks an explicit en vironment in which agents’ actions gen- erate economic experiences and feedback; as a re- sult, phenomena such as threat-induced rigidity or inequality-dri ven polarization cannot be modeled as endogenous outcomes of interaction dynamics. T o fill this gap, we propose a nov el OD simu- lation frame work in which LLM-based agents are grounded within an economic en vironment and up- date their opinions through feedback arising from their own actions and experiences. Specifically , LLM-based agents are modeled as households that make economic decisions while also exchanging opinions about the society . These decisions endoge- nously af fect the en vironment, leading to changes in prices, wages, and asset positions, which con- stitute agents’ li ved e xperiences. The accumulated experiences, in turn, shape subsequent decision- making and opinion formation. T o demonstrate that grounding LLM-based agents in an economic en vironment enables the ob- serv ation of OD driv en by actions and environmen- tal feedback, we examine whether this approach produces coherent OD at both the indi vidual and population lev els. T o this end, we inv estigate a sequence of research questions. RQ1: Do LLM-based agents grounded in an economic en vironment exhibit envir onment- consistent actions and opinions? W e first assess the basic v alidity of the framework at the individ- ual lev el by examining whether agents’ actions are appropriate to their en vironment and whether dif- ferences in experience lead to plausible qualitati ve dif ferences in expressed opinions. RQ2: How do histories of action and feedback shape individual OD? Then, we e xamine ho w each agent’ s history of actions and en vironmental feedback influence the way their opinions ev olve ov er time. This allows us to characterize indi vidual OD as experience-dependent processes. RQ3: How do indi vidual-lev el economic interac- tions scale up to population-lev el OD? Finally , we analyze how population-level opinion distri- butions co-e volv e with macroeconomic dynamics, focusing on the relationship between economic in- equality and opinion polarization, as well as be- tween macroeconomic instability and temporal in- stability in opinion distributions. Our results sho w that introducing an economic en vironment in LLM-based OD simulations makes OD grounded, endogenous, and experience-dri ven. At the individual le vel, agents exhibit economi- cally plausible behavior and experience-dependent opinion trajectories, including increased rigidity under macroeconomic instability . At the popula- tion le vel, opinion distrib utions co-e volve with eco- nomic conditions, with greater inequality associ- ated with polarization and higher price volatility associated with greater opinion instability . 2 LLM-based OD Simulation with Economic En vironments Assume n ∈ N LLM-based agents operate in a single macroeconomic en vironment setting, with each simulation consisting of T ∈ N time steps. As illustrated in Figure 1 , the LLM-based agents are modeled as households, while the firm and the gov ernment are implemented as rule-based agents. At each time step t ∈ { 1 , . . . , T } , house- hold agents are iterated ov er sequentially . After each household i ∈ { 1 , . . . , n } makes its labor, consumption, and opinion decisions, the macroeco- nomic en vironment—comprising the firm and the 𝑂 !,# : Safety net J 𝑂 !,$ : Lose motivation to work L LLM Household Firm Labor 𝐿 !,# Consumption 𝐶 !,# Wag e 𝑤 % !,# 𝐿 !,# Payme nt 𝑝 ' !,# 𝐶 !,# Government Ta x 𝜏 !,# Subsidy 𝑠 !,# Goods production 𝑌 !,# = ℱ(𝐾 !,# , 𝐿 !,# ) Wag e & p ri ce up da te 𝑤 % !,# , 𝑝' !,# Basic income Progressive taxa tion Figure 1: Structure of the LLM-based OD simulations. At each time step t ∈ { 1 , ..., T } , LLM-based household i ∈ { 1 , ..., n } sequentially makes economic decisions regarding labor supply L t,i and consumption C t,i . A rule-based firm produces goods Y t,i using household’ s labor and sets wage ¯ w t,i and price ¯ p t,i according to demand-supply imbalance. A gov ernment le vies taxes τ t,i and provides subsidies s t,i to households. In par - allel, LLM-based agents exchange their opinions O t,i about the societal and economic en vironment. gov ernment—transitions according to rule-based update rules, and the updated state is observ ed by the subsequent household agent. In the following, we detail the sequence of operations at time step t during the turn of household i , describing in order the actions of the household, firm, and government. LLM Household During the decision turn of household i at time step t , the LLM outputs cat- egorical actions a L t,i and a C t,i , where a L t,i , a C t,i ∈ { lo w , medium , high } , together with a natural- language opinion O t,i . The categorical actions are subsequently mapped to numerical v alues via a post-processing step. For labor and consumption, we define continuous interv als I L · and I C · , respec- ti vely . The realized labor L t,i and consumption C t,i are obtained by uniform sampling from the interv als associated with the selected categories: L t,i ∼ U ( I L a L t,i ) , C t,i ∼ U ( I C a C t,i ) (1) The interval boundaries are predefined and remain constant throughout the simulation. After complet- ing its decision-making at stage ( t, i ) , the house- hold’ s cash holding M t,i ∈ R is updated according to the labor supply and consumption choices as: M t,i ← M t − 1 ,i − ¯ p t,i C t,i + ¯ w t,i L t,i (2) where ¯ p t,i and ¯ w t,i denotes the price per unit of goods and wage per unit of labor . The LLM’ s outputs are conditioned on a struc- tured prompt. The prompt consists of: (i) a role in- struction specifying the household’ s decision task; (ii) a persona description for role-play; (iii) pub- lic information such as historical wages, prices, taxes and subsidies; (i v) observed opinions of other households; (v) the household’ s own financial his- tory; and (vi) the household’ s o wn opinion ex- pressed in the previous time step. The household’ s financial history is summarized in terms of its rel- ati ve financial status within the population. Us- ing the mean µ t and standard de viation σ t of all households at time t , the relati ve financial posi- tion of household i is measured by its standardized de viation from the mean, z t,i = ( M t,i − µ t ) /σ t . The household’ s financial status f t,i takes one of fi ve cate gories: very high, abov e-average, around- av erage, below-a verage or very low , determined according to predefined thresholds on z t,i . Firm Follo wing the household decision-making described abov e, the macroeconomic en vironment is updated through the actions of a rule-based firm. The firm updates production, prices, and wages based on the current intermediate state of the economy . The firm produces a homogeneous consumption good using agent i ’ s labor at time t and capital. Production follows a Cobb–Douglas technology function ( Cobb and Douglas , 1928 ). Let K t,i denote the firm’ s effecti ve capital stock at the beginning of stage ( t, i ) . Production of goods Y t,i = F ( K t,i , L t,i ) is giv en by F ( K t,i , L t,i ) = A (min( K max , K t,i )) α ( L t,i ) (1 − α ) (3) where A > 0 is the total factor producti vity , α ∈ (0 , 1) is the capital share, and K max is the maximum amount of capital used for one-time production. The produced output is consumed by the household and added to the firm’ s in ventory: K t,i +1 ← (1 − d ) K t,i + Y t,i − C t,i (4) , which depreciate between stages with rate d ∈ (0 , 1) . After observing household i ’ s demand C t,i and supply Y t,i at the current stage, the firm updates the price of unit of the good ¯ p t,i . The price is ad- justed according to the imbalance between demand C t,i and supply Y t,i : ¯ p t,i +1 ← ¯ p t,i 1 + η p C t,i − Y t,i Y t,i (5) where η p is a price elasticity . After providing w age to the household ¯ w t,i L t,i , the firm updates the wage per unit of labor ¯ w t,i in response to productivity conditions implied by the current production state. The wage is adjusted to ward the marginal product of labor MPL t,i = ∂ Y t,i /∂ L t,i using a wage elasticity η w > 0 : ¯ w t,i +1 ← ¯ w t,i + η w ( MPL t,i − ¯ w t,i ) (6) MPL t,i = (1 − α ) A (min( K max , K t,i )) α L − α t,i (7) Gover nment Follo wing the firm update, a rule- based government implements a simplified basic income and progressiv e taxation scheme. The gov- ernment publicly announces the current policy to households at each stage ( t, i ) . Each household recei ves a fixed amount of basic income as subsi- dies: ∀ ( t, i ) s t,i = b . The basic income payment is unconditional and does not depend on the house- hold’ s current labor supply or consumption choices. Also, the gov ernment levies a tax that depends on the household’ s relati ve financial status. ¯ τ ∈ [0 , 1) denote the base tax rate, which serves as the ref- erence rate for taxation. For household i at stage ( t, i ) , the effecti ve tax τ t,i is determined as τ t,i = 0 if f t,i = very lo w 2 ¯ τ M t,i if f t,i = very high ¯ τ M t,i otherwise (8) As a result, after stage ( t, i ) , the household’ s in- come is updated as M t,i ← M t,i + s t,i − τ t,i . 3 Experimental Settings 3.1 Simulation Configuration W e run 30 trials of simulations with T = 150 and n = 20 . LLM-based agents are implemented using Llama 3.1 8B ( Meta , 2024 ) with a sampling tem- perature of 0.7. F or each agent, a persona prompt is constructed using demographic attributes dra wn from a publicly av ailable persona dataset ( Meyer and Corneil , 2025 ) and personality traits based on the Big Fiv e personality model ( Goldberg , 1990 ). All other hyperparameters, as well as detailed sim- ulation procedure and computing infrastructure are provided in Appendices A and B . 3.2 Data Collection and Processing W e remov e the first 10 time steps ( t ≤ 10 ) of each simulation run to eliminate transient effects arising from the initial conditions. At the end of each stage ( t, i ) , we record all v ariables including agent’ s ac- tions L t,i , C t,i , opinion O t,i , and en vironmental contexts ¯ w t,i , ¯ p t,i , f t,i . In addition, we compute and record the time- t av erages of wages and prices, ¯ w t and ¯ p t . The textual opinion O t,i is further trans- formed into a numerical embedding o t,i ∈ R 384 using pretrained sentence transformer ( W ang et al. , 2020 ), and a scalar sentiment score ψ t,i ∈ [ − 1 , 1] using pretrained sentiment analysis model ( Liu et al. , 2020 ). The sentiment score provides a nor- malized measure of the agent’ s expressed attitude, where − 1 and +1 correspond to maximally ne ga- ti ve and positi ve sentiment, respecti vely . Individual States Agents in our simulation ex- hibit heterogeneous and continuously e volving economic conditions and generate free-form tex- tual opinions. Directly analyzing such high- dimensional and unstructured information makes it dif ficult to identify common patterns in opinion formation. T o address this challenge, we introduce a compact representation of an agent’ s situation at each time step, termed the internal state . T o characterize agents’ internal states in a structured manner , we discretize both expressed sentiment and financial status into coarse-grained cate gories and record their joint configuration at each stage ( t, i ) . First, the continuous sentiment score ψ t,i is mapped into three sentiment classes using fixed threshold θ ψ : ˜ ψ t,i = NEG , ψ t,i < − θ ψ NEU , − θ ψ ≤ ψ t,i ≤ θ ψ POS , θ ψ < ψ t,i (9) where NEG , NEU , and POS mean negati ve, neu- tral, and positiv e, respectiv ely . Using this represen- tation, we can analyze the sentiment change rates, defined as the fraction of agents whose sentiment class changes between consecuti ve time steps: δ t = 1 n X i 1 ( ˜ ψ t,i = ˜ ψ t − 1 ,i ) , (10) δ ′ t = 1 n X i 1 ( ˜ ψ t,i = ˜ ψ t − 1 ,i ∧ ˜ ψ t,i = NEU ) (11) Next, the agent’ s financial status f t,i , originally drawn from fi ve qualitati ve cate gories, is coarsened into three aggregate le vels: ˜ f t,i = lo w , f t,i ∈ { very lo w , below-a verage } av erage , f t,i ∈ { around-average } high , f t,i ∈ { very high , above-a verage } (12) W e then define the state of agent i at time t as the Cartesian product of sentiment and economic categories: h t,i = ( ˜ ψ t,i , ˜ f t,i ) ∈ H (13) where H denotes a finite internal state space: H = { NEG , NEU , POS } × { lo w , av erage , high } (14) Furthermore, we record the temporal transitions of internal states for each indi vidual, h t − 1 ,i → h t,i , throughout the simulation. As all internal state tran- sitions are represented by ordered pairs ( h, h ′ ) ∈ H × H , the total number of distinct transition types is 9 × 9 = 81 . For each indi vidual i , we define the number of occurrences of a giv en transition ( h, h ′ ) ov er the entire simulation as N i ( h, h ′ ) = X t 1 ( h t − 1 ,i = h, h t,i = h ′ ) (15) where 1 ( · ) denotes the indicator function. By ar- ranging the counts of all 81 transition types in a fixed order , we obtain a transition feature vector n i ∈ N 81 for indi vidual i , n i = ⊤ N i ( h 1 , h 1 ) . . . N i ( h 9 , h 9 ) (16) where { h 1 , ..., h 9 } denotes an arbitrary but fixed ordering of the elements of H . By considering a finite internal state space, we can 1)abstract away indi vidual-le vel variability , making it easier to identify representati ve beha v- ioral patterns, and 2)gain structured link between agents’ economic experiences and their expressed opinions. This representation enables us to ex- plicitly trace how indi vidual economic experiences shape opinion and, in turn, driv e the dynamics of population-le vel opinion distrib utions, which are examined in RQ1–RQ3. F or example, In RQ2, we apply KMeans clustering to the collection of state- transition count vectors { n i } across all agents and simulation runs, grouping individuals according to the similarity of their OD transition patterns. Population-le vel descriptors T o assess internal states and trajectories as collective phenomena, we next introduce population-le vel descriptors that summarize the collecti ve state of the system at each time step t . First, to quantify the degree of eco- nomic inequality in the population, we define Gini coef ficient at time t as: G t = 1 2 n 2 ¯ M t n X i =1 n X j =1 | M t,i − M t,j | (17) 𝑓 " !,# = low 𝑓 " !,# = avera ge 𝑓 " !,# = high Figure 2: Household labor supply and consumption choices across economic conditions. Each panel reports the distribution of cate gorical actions ( a L t,i and a C t,i ) for labor and consumption. where ¯ M t denotes the av erage income. T o characterize population-lev el OD, we con- sider two-types of opinion distributions—sentiment scores Ψ t = { ψ t,i } n i =1 and opinion embeddings O t = { o t,i } n i =1 . T o complement the standard devi- ation of sentiment as an indicator of opinion disper- sion, we define a polarization inde x P ∆ t , which is defined based on the dif ference between the mean sentiment of positive and negati ve group, while explicitly incorporating group-size balance: P ∆ t ( θ ψ ) = 4 | µ POS t − µ NEG t | r POS t r NEG t (18) µ ˜ ψ t = 1 n ˜ ψ t X i 1 ( ˜ ψ t,i = ˜ ψ ) ψ t,i (19) r ˜ ψ t = n ˜ ψ t n , n ˜ ψ t = X i 1 ( ˜ ψ t,i = ˜ ψ ) (20) 4 Results and Discussions 4.1 RQ1: Beha vioral V alidation In RQ1, we conduct a sanity check to verify that LLM-based households are behaviorally grounded in the economic en vironment. This analysis ex- amines whether agents’ economic actions and ex- pressed opinions respond coherently and consis- tently to their experienced financial conditions, providing a necessary validation for subsequent trajectory- and population-le vel analyses. Figure 2 illustrates household labor supply and consumption choices, conditioned on relative in- (a) h t,i = ( POS , lo w ) (b) h t,i = ( POS , high ) (c) h t,i = ( NEG , lo w ) (d) h t,i = ( NEG , high ) Figure 3: TF-IDF-based w ord clouds of household opin- ion texts across four internal states. come status. The distributions of categorical ac- tions (lo w , medium, high) are aggregated across all simulation runs. As sho wn in Figure 2 , lo w-income households predominantly select high labor supply and lo w consumption, whereas high-income house- holds exhibit the opposite tendency , with lower labor supply and higher consumption. Middle- income households display intermediate beha vior . These shifts across income groups are consistent with basic economic intuition under dif ferent bud- get constraints, indicating that agents adapt their economic behavior in response to their financial conditions. In Appendix C , we further assess the robustness of these observations by adjusting the prompt. Figure 3 provides qualitative evidence on ho w households’ expressed opinions v ary with their in- ternal states. The TF-IDF ( Salton and Buckley , 1988 )-based word clouds visualize salient terms extracted from household opinion texts under com- binations of sentiment ˜ ψ t,i and income status ˜ f t,i . For positiv e-sentiment households with low in- come, frequently appearing terms such as safety , gratitude , and helpful suggest appreciation for the provided of a safety net. Positive-sentiment high-income households emphasize words includ- ing balance , opportunity , and upgrade , indicating an understanding of the trade-off between insti- tutional support and labor opportunities, along- side an opportunity-oriented perspectiv e. In con- trast, negati ve-sentiment low-income households focus on terms such as unfair , insufficient , and sur- POS NEU NEG POS NEU NEG low average high low average high low average high T o low average high low average high low average high F r om 0 2 4 6 8 10 12 14 (a) Cluster 1 POS NEU NEG POS NEU NEG low average high low average high low average high T o low average high low average high low average high F r om 0 2 4 6 8 10 12 (b) Cluster 2 POS NEU NEG POS NEU NEG low average high low average high low average high T o low average high low average high low average high F r om 0 2 4 6 8 10 12 14 16 (c) Cluster 3 POS NEU NEG POS NEU NEG low average high low average high low average high T o low average high low average high low average high F r om 0 1 2 3 4 5 6 7 (d) Cluster 4 POS NEU NEG POS NEU NEG low average high low average high low average high T o low average high low average high low average high F r om 0 1 2 3 4 5 (e) Cluster 5 POS NEU NEG POS NEU NEG low average high low average high low average high T o low average high low average high low average high F r om 0 1 2 3 4 5 6 7 8 (f) Cluster 6 Figure 4: Representative internal state transition patterns obtained by clustering transition count vector n i across all simulations. Each panel visualizes the representati ve agent’ s state transition matrix as a heatmap, where ro ws (From) indicate the internal state h t − 1 ,i , columns (T o) indicate h t,i , and color intensity denotes transition frequency . vival , reflecting experienced hardship and height- ened concerns about future insecurity . Negati ve- sentiment high-income households, characterized by words such as Band-Aid , temporary , and tax- payer , express critical vie ws tow ard e xisting institu- tions and concerns regarding redistribution and per- cei ved burdens. The observ ed qualitativ e differenti- ation in salient terms across internal states indicates that opinion generation is coherently grounded in agents’ experienced economic situations, verifying cross-modal consistency between economic condi- tions, actions, and opinion content. 4.2 RQ2: Individual OD In RQ2, we examine ho w individual opinions e volv e in response to en vironmental experiences. Figure 4 visualizes representati ve patterns of in- di vidual internal state transitions from the KMeans clustering of state-transition count vectors { n i } n i =1 from entire set of simulations. For each cluster , we identify a representativ e agent whose state- transition count vector is closest to the correspond- ing cluster centroid in Euclidean distance. T o as- sess clustering robustness, we repeated KMeans with 50 random seeds and obtained a mean Ad- justed Rand Index (ARI) of 0 . 716( ± 0 . 073) across runs, indicating a stable clustering structure beyond 0.1 0.2 0.3 0.4 Opinion change rate 0.175 0.200 0.225 0.250 0.275 0.300 Absolute price r etur n All opinion changes Opinion changes w/o to NEU Figure 5: Relationship between different types of opin- ion change rates δ t , δ ′ t and price fluctuations. Absolute price return means the corresponding a verage absolute log price change | log p t,i /p t − 1 ,i | . Blue circles count all sentiment changes δ t , whereas orange squares exclude transitions to the neutral (NEU) class δ ′ t . Only bins with more than 100 observations are sho wn. Error bars indi- cate the standard error of the mean (SEM). random agreement. Figure 4 provides e vidence that OD is dri ven by indi vidual, history-dependent responses to e xperienced economic feedback. Clus- ters 1 and 2 are characterized by transition patterns concentrated in (POS, high) and (NEG, lo w), in- dicating that both economic status and expressed opinions remain largely stable over time. Cluster G t v .s. | log ( ¯ p t / ¯ p t − 1 ) | v .s. P ∆ t (0 . 2) P ∆ t (0 . 4) P ∆ t (0 . 6) Std. of Ψ t W 1 (Ψ t − 1 , Ψ t ) W 1 ( O t − 1 , O t ) Pearson 0 . 149 ∗∗ (0.016, 0.272) 0 . 192 ∗∗∗ (0.087, 0.280) 0 . 222 ∗∗∗ (0.120, 0.333) 0 . 145 ∗∗∗ (0.072, 0.234) 0 . 145 ∗∗ (0.009, 0.264) 0 . 148 ∗∗ (0.010, 0.267) Spearman 0 . 144 ∗∗ (0.012, 0.271) 0 . 181 ∗∗∗ (0.085, 0.281) 0 . 221 ∗∗∗ (0.133, 0.358) 0 . 155 ∗∗∗ (0.073, 0.232) 0 . 142 ∗∗ (0.004, 0.202) 0 . 118 ∗∗ (0.002, 0.199) T able 1: Correlation between (i) economic inequality and collective opinion measures, and (ii) macroeconomic instability and opinion dynamics. Each cell reports the correlation coef ficient with the 95% bootstrap confidence interval ( 200 resamples) shown belo w in parentheses. T o ensure independence and av oid pseudo-replication, bootstrap correlations are computed at the run level: for each of the 30 independent simulation runs, we sample one time snapshot and ev aluate correlations across these 30 samples. Note. * p < 0 . 10 , ** p < 0 . 05 , *** p < 0 . 01 . 3 represents agents whose opinions remain neutral regardless of changes in economic status. In con- trast, Clusters 4 and 5 display transitions between (POS, high) and (NEG, lo w), indicating that eco- nomic feedback dri ves opinion change. Cluster 6 sho ws that opinion changes are like wise driven by macroeconomic feedback, but through a qualita- ti vely dif ferent transition structure in volving (POS, lo w) and (NEG, high). T ogether , these observa- tions indicate that LLM-based agents exhibit het- erogeneous response patterns to macroeconomic feedback, which shape their individual opinion tra- jectories ov er time. Figure 5 illustrates the relationship between sen- timent change rates δ t , δ ′ t and contemporaneous price fluctuations. Figure 5 rev eals a negati ve asso- ciation between sentiment change rates and price fluctuations. Periods characterized by larger price changes tend to exhibit lower fractions of agents re vising their sentiment, whereas higher rates of sentiment change are observed when price fluctua- tions are relativ ely modest. This pattern is robust to excluding transitions to neutrality , indicating that the effect is not dri ven by neutralization un- der normal conditions. This pattern suggests that agents’ sentiment orientations become more sta- ble or reinforced under macroeconomic instability , indicating a form of rigidity in opinion formation. Such behavior is consistent with the threat–rigidity hypothesis ( Staw et al. , 1981 ), which posits that under percei ved threats, cogniti ve and beha vioral responses tend to narro w . 4.3 RQ3: Collective OD In RQ3, we shift our focus from individual-le vel OD to their collective manifestation at the pop- ulation lev el. Building on the findings of RQ2, where we observed that a subset of individuals ac- ti vely update their opinions in response to their economic feedback and opinion flexibility varies with macroeconomic conditions, we no w examine ho w such indi vidually driv en dynamics shape the collecti ve opinion distrib ution. T able 1 sho ws correlations relating the Gini co- ef ficient G t to two measures of opinion dispersion: the standard de viation of sentiment score distribu- tion Ψ t at time t and the polarization index P ∆ t . Across simulation runs, both the sentiment stan- dard de viation and polarization index e xhibit pos- iti ve correlations with the Gini coefficient, which are statistically significant at the 5% le vel based on Pearson correlation tests. These results indi- cate that widening economic disparities amplify not only the overall spread of opinions but also the degree of bimodal separation within the population. Importantly , this relationship mirrors empirical ob- serv ations reported in the U.S., where increasing income inequality has been linked to heightened polarization ( Ste wart et al. , 2020 ). T able 1 also reports correlations between macroeconomic instability , measured by the abso- lute log return of the av erage price | log ( ¯ p t / ¯ p t − 1 ) | , and the magnitude of collectiv e opinion change. Specifically , both the W asserstein distance between consecuti ve sentiment distrib utions W 1 (Ψ t − 1 , Ψ t ) and that between opinion embedding distributions W 1 ( O t − 1 , O t ) exhibit positi ve and statistically sig- nificant correlations with price fluctuations. These results suggest that periods of heightened economic volatility are associated not merely with more dis- persed opinions at a giv en time, but with larger reconfigurations of collecti ve opinions o ver time. Overall, our results indicate that widening eco- nomic inequality is associated with structural po- larization, whereas macroeconomic volatility is linked to temporal instability in opinion distrib u- tions. Such relationships between macroeconomic dynamics and OD become observable only when LLM-based agents are modeled as decision-makers situated within, and directly affected by , the eco- nomic en vironments they experience. 5 Related W ork OD Modeling In studies of OD, a wide range of social interactions hav e been abstracted in order to theoretically characterize collecti ve phenomena such as consensus formation, polarization, and the spread of misinformation. In the most fundamental models, including the DeGroot model ( DeGroot , 1974 ) and Friedkin–Johnsen model ( Friedkin and Johnsen , 1990 ), the process by which an individ- ual updates their opinion as a weighted a verage of others’ opinions is formalized, enabling analysis of ho w social influence and trust structures shape collecti ve opinion formation. Subsequently , models such as the bounded con- fidence models ( Deffuant et al. , 2000 ; Hegselmann and Krause , 2002 ), threshold models ( Granovetter , 1978 ; W atts , 2002 ), and Axelrod’ s model ( Axel- rod , 1997 ) introduce constraints on interactions based on social distance, providing explanations for phenomena such as opinion con ver gence within homogeneous groups, emergence of echo cham- bers, and self-organization of polarization. Fur - thermore, research grounded in social impact the- ory ( Latané , 1981 ) focus on psychological biases, modeling the influence of non-rational factors such as majority ef fects and conformity on opinion for- mation ( No wak et al. , 1990 ; Galam , 2002 ). Recent studies ha ve e xplored OD using LLM- based agents. Cau et al. ( 2025 ) highlights a dis- tincti ve adv antage of LLMs by demonstrating that agents both generate and are influenced by argu- mentati ve f allacies during discussions, thereby in- ternalizing rhetorical and reasoning-related phe- nomena that are abstracted aw ay in classical OD models. Also, recent studies report that popula- tions of LLM-based agents are strongly influenced by framing and confirmation bias ( Chuang et al. , 2024 ), and tend to con verge to ward equity-oriented consensus ( Cisneros-V elarde , 2025 ). While these studies demonstrate the potential of LLMs to enrich OD through linguistically grounded interaction and cogniti ve bias, they largely retain a view of OD as a process dri ven by communication alone. In contrast, we empha- size the role of non-linguistic factors such as eco- nomic conditions, liv ed experiences, and structural constraints in shaping opinion. Building on this perspecti ve, we introduce the agent–en vironment coupling into OD modeling by grounding opinion formation in agents’ actions, economic feedback, and ev olving constraints, enabling the bottom-up emergence of macro-le vel opinion patterns. LLM-based Social Simulations Recent stud- ies demonstrate that LLMs provide a foundation for social simulation by enabling psychologically grounded beha vior , persona-driv en heterogeneity , and te xt-based interaction at scale. F or e xample, Park et al. ( 2023 ) propose Generative Agents that exhibit human-lik e daily beha viors and social inter - actions, demonstrating ho w language-based cogni- tion support emergent social phenomena. In the economic domain, both macroeconomic and financial market simulations suggest that LLM- based agents reproduce aggregate economic pat- terns. LLM-empo wered agents are shown to generate macroeconomic regularities ( Li et al. , 2024 ), while similar emer gent patterns are ob- served in LLM-based financial mark et simulations ( Hashimoto et al. , 2026 ; Hirano , 2026 ). Extending this direction, recent large-scale simulations aim to model complex societies composed of man y inter- acting LLM-based agents. For instance, Piao et al. ( 2025 ) present a large-scale agent society to study collecti ve behaviors and social dynamics, while Zhang et al. ( 2025 ) introduce a world model for social simulation that integrates LLM-based agents with data from millions of real-world users. This work deepens prior attempts to construct so- cial simulacra by reexamining the role of the envi- ronment in LLM-based social simulations. Rather than serving as a descripti ve context, the en viron- ment in our framework provides feedback as future action constraints and updates aggregated macro- le vel order , thereby endogenously generating col- lecti ve and temporal heterogeneity . As a result, socioeconomic couplings such as inequality-driv en polarization and the co-mov ement of economic in- stability and opinion distribution v olatility emerge bottom-up from indi vidual actions. 6 Conclusion In this work, we in vestigated OD of LLM-based agents by connecting them to an en vironment that requires action and generates consequential feed- back. By enacting LLMs as economic agents in a macroeconomic system, we sho wed that opinions are not formed solely through linguistic interac- tion, but are acti vely driv en by agents’ own actions and the experiences that follow from them. Our results re veal a structured coupling between en vi- ronmental dynamics and OD. Interactions with an action-demanding en vironment driv e ho w indi vid- ual opinions are formed through liv ed economic experiences. Furthermore, the resulting collecti ve OD ev olve in close alignment with the dynamics of the en vironment itself, giving rise to population- le vel patterns such as inequality-link ed polarization that are inaccessible in language-only settings. Limitations Simplified linguistic interaction mechanisms T o isolate the effects of action-mediated environ- mental feedback on opinion formation, interactions among agents are intentionally simplified in the present framew ork. Agents are exposed to lim- ited textual opinions, and information provided by institutions such as firms and the go vernment is symmetric across households. Consequently , richer social processes—such as deliberati ve dis- cussion, persuasion, networked communication, or voting—are not modeled. These mechanisms may interact in complex ways with experience-dri ven opinion change. Extending the frame work to in- corporate more structured and heterogeneous inter- action designs remains an important direction for future work. Fixed institutional rules and exogenous policy design The macroeconomic en vironment is gov- erned by fixed, rule-based institutions, including taxation and redistribution schemes that do not adapt in response to agents’ opinions. While this design choice enables a clean analysis of ho w en- vironmental dynamics dri ve opinion formation, it precludes the study of institutional change driven by collectiv e beliefs or political pressure. Allow- ing institutional rules to change over time would enable the study of how OD interact with dynamic policy en vironments. Moreov er, policy interventions are not systemati- cally compared across counterfactual regimes (e.g., with versus without interv ention). Extending the frame work to support controlled polic y variations across otherwise identical en vironments would en- able quasi-experimental analyses in the spirit of dif ference-in-dif ferences (DiD). Limited bidirectionality between opinions and actions Although the framew ork explicitly cap- tures how action-conditioned experiences dri ve OD, it does not yet realize fully bidirectional dynamics between opinions and the en vironment. In par- ticular , opinions in the current setting do not di- rectly influence agents’ subsequent economic de- cisions. W e ar gue that achie ving such bidirection- ality crucially depends on the design of linguistic interaction mechanisms: in real societies, decision- making is shaped not only by individual experi- ences but also by the percei ved opinion climate formed through social communication. Designing interaction structures in which socially e xpressed opinions systematically affect agents’ choices may enable co-e volutionary dynamics between collec- ti ve opinions and en vironmental trajectories. In- vestigating such socially mediated feedback loops remains an important challenge for future research. References Robert Axelrod. 1997. The dissemination of culture: A model with local con vergence and global polarization. Journal of Conflict Resolution , 41(2):203–226. Claudio Castellano, Santo Fortunato, and V ittorio Loreto. 2009. Statistical physics of social dynam- ics. Reviews of Modern Physics , 81:591–646. Erica Cau, V alentina Pansanella, Dino Pedreschi, and Giulio Rossetti. 2025. Language-driv en opinion dynamics in agent-based simulations with LLMs . Pr eprint , Y un-Shiuan Chuang, Agam Goyal, Nikunj Harlalka, Siddharth Suresh, Robert Hawkins, Sijia Y ang, Dha- van Shah, Junjie Hu, and Timothy Rogers. 2024. Simulating opinion dynamics with networks of LLM- based agents. In Findings of the Association for Com- putational Linguistics: N AA CL 2024 , pages 3326– 3346. Pedro Cisneros-V elarde. 2025. Biases in opinion dy- namics in multi-agent systems of large language mod- els: A case study on funding allocation. In F indings of the Association for Computational Linguistics: N AA CL 2025 , pages 1889–1916. Charles W . Cobb and Paul H. Douglas. 1928. A the- ory of production. The American Economic Review , 18(1):139–165. Guillaume Def fuant, David Neau, Frederic Amblard, and Gérard W eisbuch. 2000. Mixing beliefs among interacting agents. Advances in Comple x Systems , 03(01n04):87–98. Morris H. DeGroot. 1974. Reaching a consensus. Journal of the American Statistical Association , 69(345):118–121. Noah E. Friedkin and Eugene C. Johnsen. 1990. Social influence and opinions. The J ournal of Mathematical Sociology , 15(3-4):193–206. Serge Galam. 2002. Minority opinion spreading in random geometry . The Eur opean Physical Journal B - Condensed Matter and Comple x Systems , 25:403– 406. Le wis R. Goldberg. 1990. An alternati ve ”description of personality”: The big-fi ve factor structure. Journal of P ersonality and Social Psychology , 59(6):1216– 1229. Mark S. Granovetter . 1978. Threshold models of col- lectiv e behavior . American Journal of Sociology , 83:1420–1443. Ryuji Hashimoto, T akehiro T akayanagi, Masahiro Suzuki, and Kiyoshi Izumi. 2026. Agent-based simu- lation of a financial market with large language mod- els. In The International Conference on Principles and Practice of Multi-Agent Systems (PRIMA 2025) , pages 20–28. Rainse Hegselmann and Ulrich Krause. 2002. Opinion dynamics and bounded confidence: Models, analysis, and simulation. Journal of Artificial Societies and Social Simulation , 5(3):1–33. Masanori Hirano. 2026. Building LLM-based artificial market simulations: Can LLMs function as agents in multi-agent simulations for finance? In The Inter- national Confer ence on Principles and Practice of Multi-Agent Systems (PRIMA 2025) , pages 56–71. Bibb Latané. 1981. The psychology of social impact. American Psychologist , 36(4):343–356. Nian Li, Chen Gao, Mingyu Li, Y ong Li, and Qing- min Liao. 2024. EconAgent: Large language model- empowered agents for simulating macroeconomic activities. In Pr oceedings of the 62nd Annual Meet- ing of the Association for Computational Linguistics , pages 15523–15536. Zhuang Liu, Degen Huang, Kaiyu Huang, Zhuang Li, and Jun Zhao. 2020. FinBER T : A pre-trained finan- cial language representation model for financial text mining. In Pr oceedings of the T wenty-Ninth Inter- national J oint Confer ence on Artificial Intelligence, IJCAI-20 , pages 4513–4519. Meta. 2024. The Llama 3 herd of models . Preprint , Y e v Meyer and Dane Corneil. 2025. Nemotron- Personas-USA: Synthetic personas aligned to real- world distrib utions . Andrzej Now ak, Jacek Szamrej, and Bibb Latané. 1990. From pri v ate attitude to public opinion: A dynamic theory of social impact. Psychological Review , 97(3):362–376. Joon Sung Park, Joseph O’Brien, Carrie Jun Cai, Mered- ith Ringel Morris, Percy Liang, and Michael S. Bern- stein. 2023. Generativ e agents: Interacti ve simulacra of human behavior . In Pr oceedings of the 36th An- nual A CM Symposium on User Interface Softwar e and T echnolo gy . Jinghua Piao, Y uwei Y an, Jun Zhang, Nian Li, Junbo Y an, Xiaochong Lan, Zhihong Lu, Zhiheng Zheng, Jing Y i W ang, Di Zhou, Chen Gao, Fengli Xu, Fang Zhang, Ke Rong, Jun Su, and Y ong Li. 2025. AgentSociety: Large-scale simulation of LLM-dri ven generativ e agents advances understanding of human behaviors and society . Pr eprint , Gerard Salton and Christopher Buckley . 1988. T erm- weighting approaches in automatic text retrie val. In- formation Pr ocessing & Management , 24(5):513– 523. Barry M. Staw , Lance E. Sandelands, and Jane E. Dut- ton. 1981. Threat rigidity effects in organizational behavior: A multile vel analysis. Administrative Sci- ence Quarterly , 26(4):501–524. Alexander J. Stewart, Nolan McCarty , and Joanna J. Bryson. 2020. Polarization under rising inequal- ity and economic decline. Science Advances , 6(50):eabd4201. Joshua Tuck er . 2023. Computational social science for policy and quality of democracy: Public opinion, hate speech, misinformation, and for eign influence campaigns , pages 381–403. W enhui W ang, Furu W ei, Li Dong, Hangbo Bao, Nan Y ang, and Ming Zhou. 2020. Minilm: deep self- attention distillation for task-agnostic compression of pre-trained transformers. In Pr oceedings of the 34th International Confer ence on Neural Information Pr ocessing Systems . Duncan J. W atts. 2002. A simple model of global cas- cades on random networks. Pr oceedings of the Na- tional Academy of Sciences of the United States of America , 99:5766–5771. Xinnong Zhang, Jiayu Lin, Xinyi Mou, Shiyue Y ang, Xiawei Liu, Libo Sun, Hanjia L yu, Y ihang Y ang, W eihong Qi, Y ue Chen, Guanying Li, Ling Y an, Y ao Hu, Siming Chen, Y u W ang, Xuanjing Huang, Jiebo Luo, Shiping T ang, Libo W u, and 2 others. 2025. SocioVerse: A world model for social simulation powered by LLM agents and a pool of 10 million real-world users . Pr eprint , arXi v:2504.10157. A Detailed Simulation Configurations T able 2 summarizes the e xperimental setup of our simulation of OD with LLM-based households. Each simulation was conducted ov er T = 150 time steps with n = 20 agents. The household economic status category f t,i is determined by thresholding Parameter Notation V alue Gov ernment Base tax rate ¯ τ 0 . 010 Basic income b 5 . 000 Firm Capital share α 0 . 100 Depreciation rate d 0 . 005 Producti vity A 0 . 950 Initial price ¯ p 1 , 1 1 . 000 Initial wage ¯ w 1 , 1 1 . 500 Initial in ventory K 1 , 1 20 . 000 Max capital for production K max 50 . 000 Price elasticity η p 0 . 200 W age elasticity η w 0 . 030 Household Initial cash ∀ i M 1 ,i U (0 , 100) Lo w labor range I L low [4 , 5) Medium labor range I L medium [5 , 6) High labor range I L high [6 , 7) Lo w consumption range I C low [5 , 6) Medium consumption range I L medium [6 , 7) High consumption range I L high [7 , 8) T able 2: Full list of hyperparameters in our simulation of OD with LLM-based households. the normalized income z t,i . Thresholds − 1 . 282 , − 0 . 524 , 0 . 524 , and 1 . 282 correspond to the bound- aries between the fiv e categories: very lo w , below- av erage, around-average, abo ve-av erage, and very high. These thresholds correspond to the upper 10th and 30th percentiles of a standard normal dis- tribution. Algorithm 1 shows the detailed procedure of a simulation. Below , we describe the structure of the prompt used in our experiments, introduc- ing its components step by step. W e first specify the agent’ s role and the basic economic setting in which it operates. Prompt Example 1: Role and economic set- ting You are a household in an economy. In this economy, there is only one good. Your money can be used only to buy the good or to pay tax. You will be happy if you consume the good. In order to buy a good, you have to earn money in some ways. One way to earn money is to work. Next, we condition each agent on a persona that specifies basic demographic attributes and person- ality traits. Specifically , the attributes sex, age, marital status, education lev el, occupation, and Algorithm 1: LLM-based OD simulation with macroeconomic en vironment. Input: n household personas f or i = 1 to n do Initialize financial state M t =0 ,i ; Initialize opinion trajectory ⟨ O i ⟩ = {} ; f or t = 1 to T do f or i = 1 to n do Compute relativ e financial status f t,i from { M t,j } n j =1 ; Construct prompt from persona, history , en vironment state, and peer opinions; Query LLM with the prompt to obtain ( L t,i , C t,i , O t,i ) ; Update household income Eq.( 2 ); Update firm state (price ¯ p and wage ¯ w of a unit of good and labor , and in ventory K t,i ) Eq.( 4 , 5 , 6 ); Append O t,i to ⟨ O i ⟩ ; city are assigned via stratified sampling. In ad- dition to demographic attrib utes, each agent is en- do wed with personality traits based on the Big Fi ve personality model ( Goldberg , 1990 ). For each of the fi ve dimensions—e xtroversion, agreeableness, conscientiousness, neuroticism, and openness to experience—one of two opposing trait descriptors (e.g., extro verted vs. intro verted) is randomly sam- pled and assigned to the agent. Prompt Example 2: P ersona conditioning Your persona to role-play is as follows: sex: Female, age: 29, ..., trait1: introverted, trait2: agreeable, ... W e next present the macroeconomic en viron- ment observ able to agents. Prices, wages, and pol- icy v ariables are provided exogenously as compo- nents of the en vironmental state. Prompt Example 3: Public inf ormation You have the following information: Firm Announcement: Current price per a unit of goods: 1.64, Current wage per a unit of labor: 1.46 The price has been strongly increasing in the long term. Recently, the price has been moderately increasing in the short term. The wage has been stable in the long term. Recently, the wage has been slightly increasing in the short term. Government Announcement: We keep the current basic income policy in order to ensure a minimum standard of living and support households currently facing financial difficulties. Each household receives 5 unit of cash as a basic income. The funding for basic income is covered by taxes paid by households with very high income. Tax rate is set to 20.0 percent for households with very high income, and 10.0 percent for other households, while households with very low income are exempt from taxation. In our experiments, opinion exchange among agents is simplified as follows. At each stage ( t, i ) , agents are provided with the opinions expressed by other agents up to the two most recent preceding stages as part of the prompt. Prompt Example 4: Others’ opinions Other households’ opinions: - The current system is unfair to those who ... - ... Next, we pro vide agents with information about their o wn past economic e xperiences and state tran- sitions. This component constitutes the core of our frame work, as it e xplicitly conditions agents on their li ved experiences. By incorporating this information, expressed opinions are not merely re- flections of the assigned persona, b ut are formed as outcomes of past actions and environmental feed- back. Prompt Example 5: Individual economic history Your individual information: Holding cash: 33.69 Latest paid tax: 3.19 Latest received subsidy: 5.00 You received subsidy larger than the tax you paid. You were a net recipient of subsidies last time. Your financial status was initially below-average income, last time below-average income and is currently below-average income Your cash holding is currently slightly increasing compared to the last time. In addition, agents are pro vided with their own pre viously expressed opinion from an earlier time step. This information serves as a short-term mem- ory that introduces temporal continuity in opinion expression, allo wing opinions to ev olve in relation to past beliefs while remaining responsi ve to newly experienced economic conditions. Prompt Example 6: Own last opinion Your last opinion: This society seems to ... Finally , agents are asked to simultaneously choose their actions and express an opinion. Re- sponses are strictly constrained to a predefined JSON format. This design ensures that non- linguistic actions (labor and consumption) and lin- guistic outputs (opinions) are generated jointly on the basis of the same underlying economic experi- ences. Prompt Example 7: Decision and opinion task Based on this information, please provide the following decisions. Take all information into account. 1. How much do you work? The more you work, the higher you earn money to buy goods. You only spend your time to work, no additional resource is required. In general, those who are financially struggling should work hard. Answer must be either "low", "medium", "high". 2. How much do you consume goods? You will be happy if you consume more. Answer must be either "low", "medium", "high". 3. Clearly state your opinion in your words about this society. Take your financial situation and your work-consumption decision made above into account. But you must not be ambiguous even if you are not sure. Try to offer your own distinct perspective. Decide your responses in the following JSON format. Do not deviate from the format, and do not add any additional words to your response outside of the format. Here are the answer format. "work": "low"/"medium"/"high", "consume": "low"/"medium"/"high", "opinion": , "stance": B Computing Infrastructure The e xperiment w as conducted on a workstation equipped with the follo wing hardw are and software configurations: • CPU : AMD Ryzen 9 3950X 16-Core Pro- cessor (32 threads, base clock 3.5 GHz, max boost 4.76 GHz) • GPU : 2 × NVIDIA R TX 6000 Ada Genera- tion (48 GB VRAM each) • Memory : 64 GB DDR4 RAM • Operating System : Ubuntu 22.04.5 L TS (Jammy Jellyfish) • CUDA T oolkit : 11.5 • NVIDIA Driver V ersion : 560.35.03 • CUDA Runtime V ersion : 12.6 The complete source code used for the experi- ment, along with a full list of Python library ver - sions and en vironment specifications, is pro vided in the supplementary material. C Prompt Ablation W e examine whether the beha vioral differentiation observed in RQ1 is driven by explicit prompt in- struction or by the economic feedback mechanism itself. T o isolate the ef fect of this instruction, we construct an ablated prompt by remo ving the sen- tence: In gener al, those who ar e financially strug- gling should work har d. The full prompt specifica- tion is provided in Appendix A . ∆ L (low) ∆ C (low) ∆ L (high) ∆ C (high) Baseline 0 . 682 − 0 . 931 − 0 . 086 0 . 463 w/o inst. 0 . 644 − 0 . 872 − 0 . 083 0 . 437 T able 3: Behavioral dif ferentiation under prompt ab- lation. Baseline refers to the main simulation setting described in the paper . The w/o inst. condition cor- responds to a modified prompt in which the sentence In general, those who are financially struggling should work har d. is remov ed. W e rerun the simulation under identical condi- tions using the modified prompt, aggregating re- sults over 30 independent runs. T o quantify be- havioral differentiation, we define the following normalized dif ference measure for labor supply: ∆ L ( ˜ f ) = N L high ( ˜ f ) − N L low ( ˜ f ) N L high ( ˜ f ) + N L low ( ˜ f ) (21) where ˜ f denotes a financial status defined in Eq. ( 3.2 ). Here, N L high ( ˜ f ) is the total number of time steps across all agents and simulation runs in which agents in state ˜ f choose the high labor action, and N L low ( ˜ f ) is defined analogously for the low labor . Similarly , we define ∆ C ( ˜ f ) for consumption deci- sions: ∆ C ( ˜ f ) = N C high ( ˜ f ) − N C low ( ˜ f ) N C high ( ˜ f ) + N C low ( ˜ f ) (22) where N C high ( ˜ f ) and N C low ( ˜ f ) denote the counts of high (lo w) consumption actions, respecti vely . T able 3 summarizes the results. The results sho w that the direction of behavioral differentiation re- mains unchanged across conditions. Lo w-income households continue to exhibit higher labor sup- ply and lower consumption, while high-income households display the opposite pattern. Although the magnitude of differentiation decreases slightly (approximately 5–6%), the qualitati ve structure is preserved. These findings indicate that the e xplicit instruction strengthens, b ut does not generate, the observed beha vioral patterns. Instead, the differen- tiation primarily arises from the economic feedback mechanism embedded in the en vironment rather than from direct prompt compliance.

Original Paper

Loading high-quality paper...

Comments & Academic Discussion

Loading comments...

Leave a Comment