Grassroots Bonds: A Grassroots Foundation for Market Liquidity

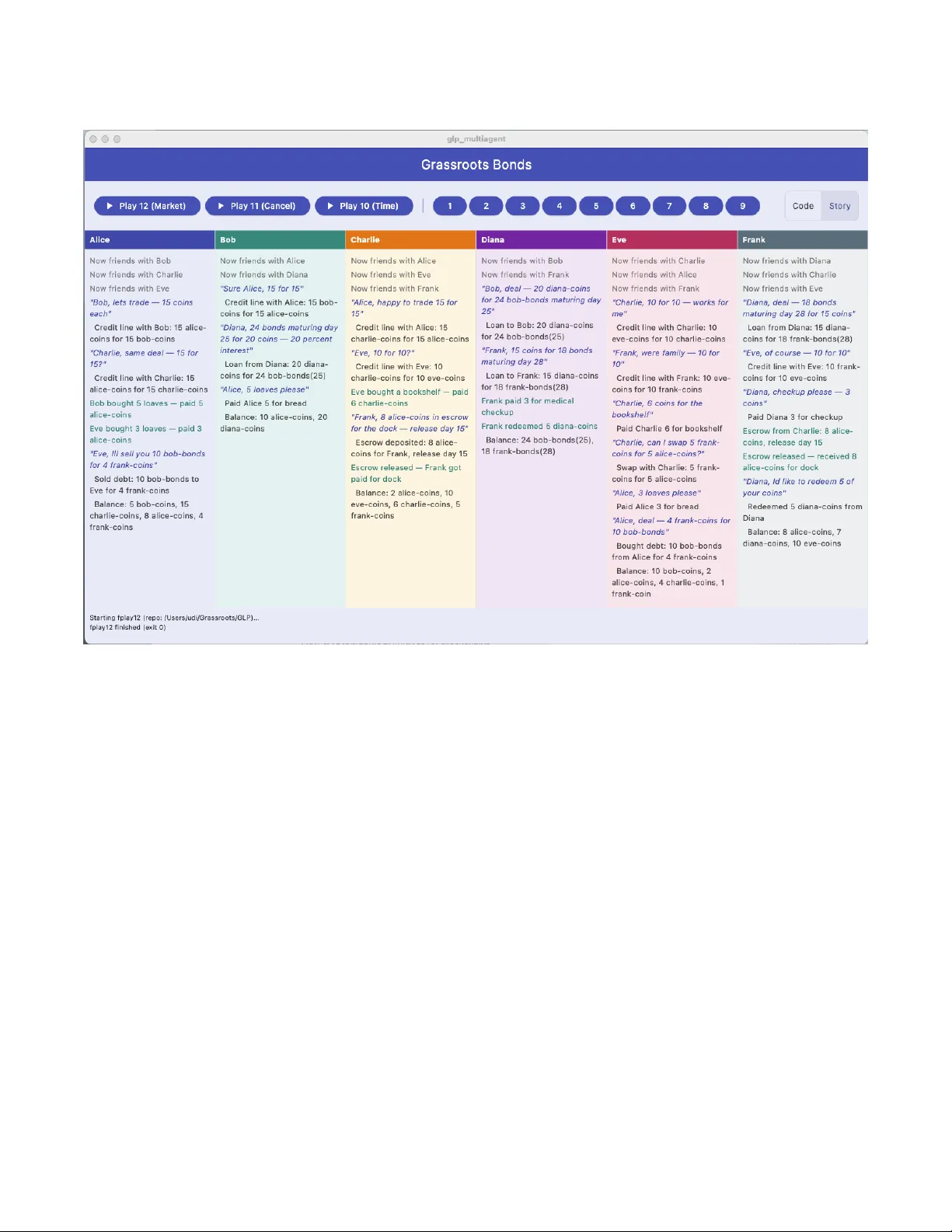

Global cryptocurrencies are unbacked and have high transaction cost incurred by global consensus. In contrast, grassroots cryptocurrencies are backed by the goods and services of their issuers -- any person, natural or legal -- and have no transactio…

Authors: Ehud Shapiro