Intrinsic Geometry of the Stock Market from Graph Ricci Flow

We use the discrete Ollivier-Ricci graph curvature with Ricci flow to examine the intrinsic geometry of financial markets through the empirical correlation graph of the NASDAQ 100 index. Our main result is the development of a technique to perform surgery on the neckpinch singularities that form during the Ricci flow of the empirical graph, using the behavior and the lower bound of curvature of the fully connected graph as a starting point. We construct an algorithm that uses the curvature generated by intrinsic geometric flow of the graph to detect hidden hierarchies, community behavior, and clustering in financial markets despite the underlying challenges posed by a highly connected geometry.

💡 Research Summary

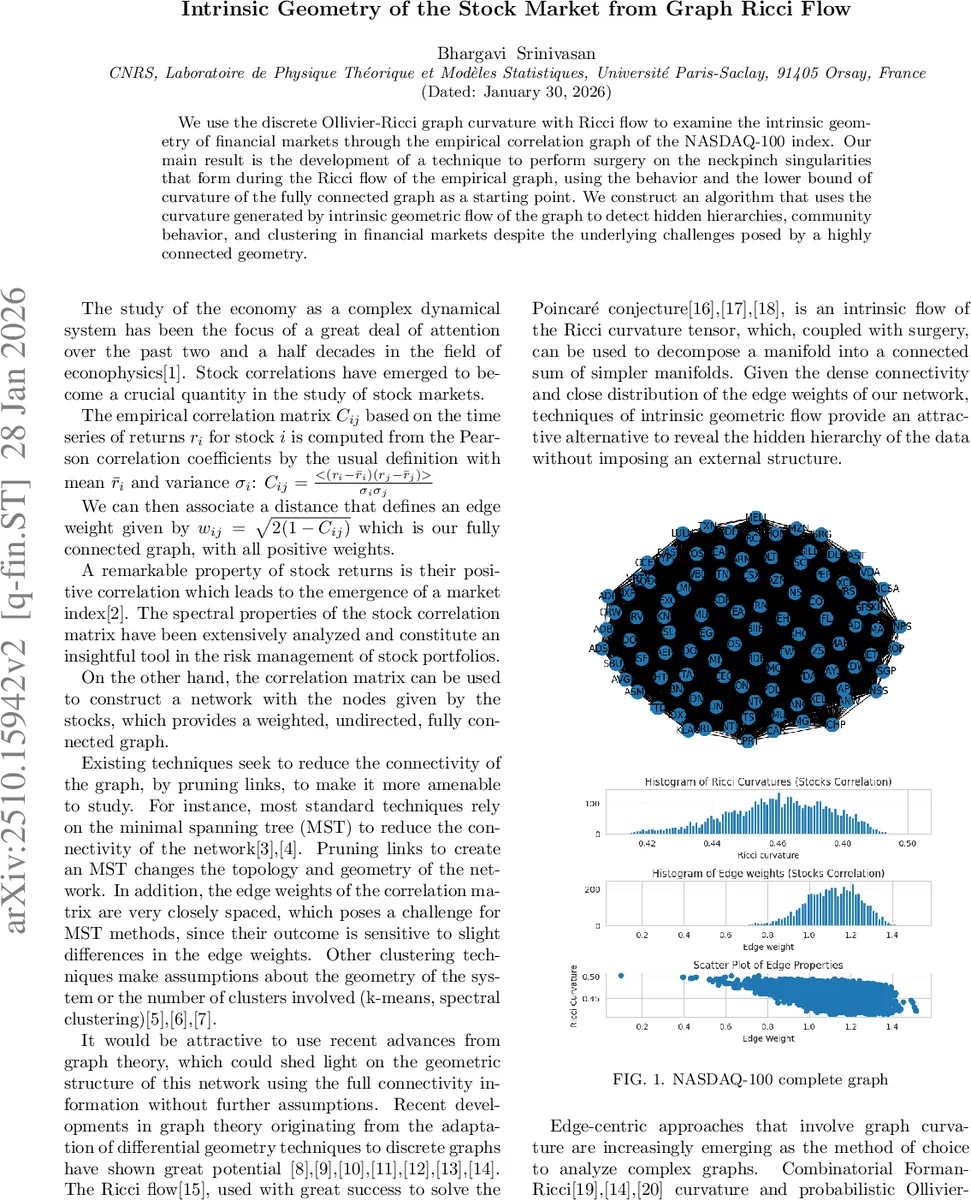

The paper investigates the intrinsic geometry of financial markets by applying discrete Ollivier‑Ricci curvature (ORC) and Ricci flow to the empirical correlation graph of the NASDAQ‑100 index. Starting from daily returns of the index constituents over a five‑year period (2020‑2024), the authors compute the Pearson correlation matrix Cij and transform it into a distance metric wij = √(2(1‑Cij)). This yields a fully connected, weighted, undirected graph where each node represents a stock and each edge encodes the similarity of returns.

Traditional network‑analysis techniques in econophysics, such as Minimal Spanning Tree (MST) pruning or k‑means clustering, deliberately discard edges to simplify topology, often at the cost of losing subtle structural information. In contrast, the authors retain the complete connectivity and exploit the geometric information encoded in the graph’s curvature. ORC is defined by assigning a lazy random‑walk probability measure mi to each vertex (idleness parameter α = ½) and measuring the Wasserstein distance W(mi, mj) between neighboring vertices. The curvature of edge (i, j) is κij = 1 – W(mi, mj)/d(i, j), where d(i, j) is the shortest‑path distance under the current edge weights. Positive curvature indicates that the two vertices share many common neighbors (i.e., belong to the same community), while negative curvature signals sparse overlap (different communities). The curvature values are bounded between –2 and 1, with complete graphs attaining a uniform positive curvature κ = (1‑α)·n/(n‑1).

Ricci flow deforms the edge weights according to the curvature: dwij/dt = – κij·wij. In practice the authors discretize time, updating all edge weights simultaneously at each iteration: wij(t+1) = (1 – κij(t))·d(t)(i, j). Positive‑curvature edges shrink, negative‑curvature edges expand, and flat edges remain unchanged. This process naturally amplifies the separation between communities, creating a “neck‑pinch” singularity reminiscent of the continuous Ricci‑flow theory on manifolds with positive curvature.

The key methodological contribution is a surgery procedure adapted from the manifold setting. By monitoring the curvature distribution during the flow, the authors identify edges whose curvature approaches zero—these are the thin “necks” linking emerging clusters. Using the theoretical lower bound for ORC, κmin = 2/(n‑1) – 1, they set an objective criterion for when and where to cut. After cutting the zero‑curvature edges, the original graph decomposes into a connected sum of simpler subgraphs, each representing a distinct market community.

Empirically, after five iterations of Ricci flow the weight histogram already broadens, and the curvature histogram begins to split into two peaks. By ten iterations a clear dumbbell shape appears, with a narrow neck separating two dense regions. After twenty iterations the curvature distribution is bimodal, and the zero‑curvature edges are readily identifiable. Performing surgery at this stage yields two clusters containing 66 and 35 stocks respectively. The larger cluster is dominated by technology firms (FAANG‑type), while the smaller cluster aggregates more traditional sectors such as finance and industrials.

The authors argue that this curvature‑driven approach preserves the full information of the correlation matrix, avoids arbitrary choices of the number of clusters, and provides a mathematically grounded way to detect hierarchical structure. They also note that the lower curvature bound remains respected even when edge weights are heterogeneous, confirming the robustness of the method.

Limitations include the computational cost of Wasserstein distance calculations for large graphs, the lack of a formal convergence proof for the discrete Ricci flow, and the need for systematic validation against benchmark clustering methods. Future work is outlined to extend the technique to other asset classes (e.g., S&P 500, cryptocurrency networks), to explore multi‑scale flows, and to develop real‑time surgery algorithms for dynamically evolving financial networks.

Overall, the paper demonstrates that intrinsic geometric flows, originally devised for smooth manifolds, can be successfully transferred to discrete financial networks, offering a novel lens for uncovering hidden market hierarchies and community structures.

Comments & Academic Discussion

Loading comments...

Leave a Comment