📝 Original Info

- Title: Orchestration Framework for Financial Agents: From Algorithmic Trading to Agentic Trading

- ArXiv ID: 2512.02227

- Date: 2025-12-01

- Authors: Researchers from original ArXiv paper

📝 Abstract

The financial market is a mission-critical playground for AI agents due to its temporal dynamics and low signal-to-noise ratio. Building an effective algorithmic trading system may require a professional team to develop and test over the years. In this paper, we propose an orchestration framework for financial agents, which aims to democratize financial intelligence to the general public. We map each component of the traditional algorithmic trading system to agents, including planner, orchestrator, alpha agents, risk agents, portfolio agents, backtest agents, execution agents, audit agents, and memory agent. We present two in-house trading examples. For the stock trading task (hourly data from 04/2024 to 12/2024), our approach achieved a return of $20.42\%$, a Sharpe ratio of 2.63, and a maximum drawdown of $-3.59\%$, while the S&P 500 index yielded a return of $15.97\%$. For the BTC trading task (minute data from 27/07/2025 to 13/08/2025), our approach achieved a return of $8.39\%$, a Sharpe ratio of $0.38$, and a maximum drawdown of $-2.80\%$, whereas the BTC price increased by $3.80\%$. Our code is available on \href{https://github.com/Open-Finance-Lab/AgenticTrading}{GitHub}.

💡 Deep Analysis

Deep Dive into Orchestration Framework for Financial Agents: From Algorithmic Trading to Agentic Trading.

The financial market is a mission-critical playground for AI agents due to its temporal dynamics and low signal-to-noise ratio. Building an effective algorithmic trading system may require a professional team to develop and test over the years. In this paper, we propose an orchestration framework for financial agents, which aims to democratize financial intelligence to the general public. We map each component of the traditional algorithmic trading system to agents, including planner, orchestrator, alpha agents, risk agents, portfolio agents, backtest agents, execution agents, audit agents, and memory agent. We present two in-house trading examples. For the stock trading task (hourly data from 04/2024 to 12/2024), our approach achieved a return of $20.42\%$, a Sharpe ratio of 2.63, and a maximum drawdown of $-3.59\%$, while the S&P 500 index yielded a return of $15.97\%$. For the BTC trading task (minute data from 27/07/2025 to 13/08/2025), our approach achieved a return of $8.39\%$, a

📄 Full Content

Orchestration Framework for Financial Agents:

From Algorithmic Trading to Agentic Trading

Jifeng Li1, Arnav Grover2, Abraham Alpuerto3, Yupeng Cao4, Xiao-Yang Liu1∗

1SecureFinAI Lab, Columbia University, 2Purdue University,

3Rensselaer Polytechnic Institute, 4Stevens Institute of Technology

Abstract

The financial market is a mission-critical playground for AI agents due to its tem-

poral dynamics and low signal-to-noise ratio. Building an effective algorithmic

trading system may require a professional team to develop and test over the years.

In this paper, we propose an orchestration framework for financial agents, which

aims to democratize financial intelligence to the general public. We map each com-

ponent of the traditional algorithmic trading system to agents, including planner,

orchestrator, alpha agents, risk agents, portfolio agents, backtest agents, execu-

tion agents, audit agents, and memory agent. We present two in-house trading

examples. For the stock trading task (hourly data from 04/2024 to 12/2024), our

approach achieved a return of 20.42%, a Sharpe ratio of 2.63, and a maximum

drawdown of −3.59%, while the S&P 500 index yielded a return of 15.97%. For

the BTC trading task (minute data from 27/07/2025 to 13/08/2025), our approach

achieved a return of 8.39%, a Sharpe ratio of 0.38, and a maximum drawdown of

−2.80%, whereas the BTC price increased by 3.80%. Our code is available on

GitHub.

1

Introduction

From floor trading with chalkboards and open outcry to telephone order routing, and then to algo-

rithmic trading, the market microstructure has reorganized how orders are created, conveyed, and

executed [24, 3, 9]. The algorithmic trading (AT) system [24] follows a pipeline from processing

financial data, extracting trading signals, portfolio management to execution and evaluation. Design-

ing an effective AT system may require a professional team to develop and test over years. Recent

works have demonstrated the great potential of AI agents: reasoning-and-acting [29], self-teaching

for using tools [20], generative agents [19], reflection and memory [21], and multi-agent role coor-

dination [10]. The financial market is a particularly challenging playground for AI agents due to its

unique features of temporal dynamics and low signal-to-noise ratio. In particular, agentic trading

is a mission-critical task in a high-stakes domain.

In this paper, we propose an end-to-end orchestration framework for financial agents, which maps

the components of the traditional AT system to agents and democratizes financial intelligence to

the general public. First, we map each component of the AT system to agents, including planner,

orchestrator, alpha agents, risk agents, portfolio agents, backtest agents, execution agents, audit

agents, and memory agent. Second, we use the Model Context Protocol (MCP) for control messages

between the orchestrator and agents and the Agent-to-Agent protocol (A2A) for communication

among agents, while a memory agent records states, prompts, tool calls, and decisions.

Finally, we develop two homegrown trading examples. For the stock trading task backtested from

04/2024 to 01/2025 (hourly data), our agents achieve a return of 20.42%, volatility of 11.83% and

∗Corresponding author.

Workshop on Generative AI in Finance, at 39th Conference on Neural Information Processing Systems

(NeurIPS 2025).

arXiv:2512.02227v1 [cs.MA] 1 Dec 2025

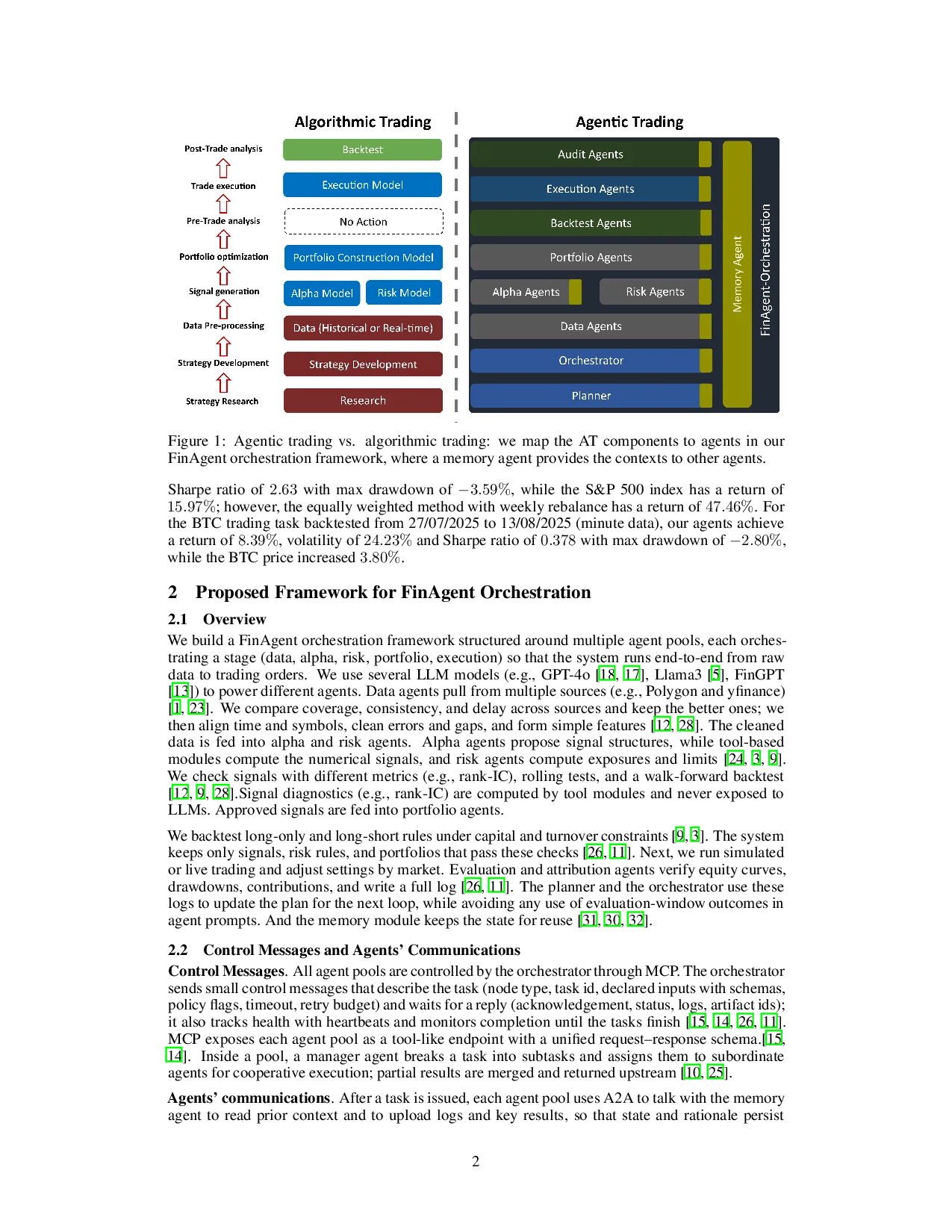

Figure 1: Agentic trading vs. algorithmic trading: we map the AT components to agents in our

FinAgent orchestration framework, where a memory agent provides the contexts to other agents.

Sharpe ratio of 2.63 with max drawdown of −3.59%, while the S&P 500 index has a return of

15.97%; however, the equally weighted method with weekly rebalance has a return of 47.46%. For

the BTC trading task backtested from 27/07/2025 to 13/08/2025 (minute data), our agents achieve

a return of 8.39%, volatility of 24.23% and Sharpe ratio of 0.378 with max drawdown of −2.80%,

while the BTC price increased 3.80%.

2

Proposed Framework for FinAgent Orchestration

2.1

Overview

We build a FinAgent orchestration framework structured around multiple agent pools, each orches-

trating a stage (data, alpha, risk, portfolio, execution) so that the system runs end-to-end from raw

data to trading orders. We use several LLM models (e.g., GPT-4o [18, 17], Llama3 [5], FinGPT

[13]) to power different agents. Data agents pull from multiple sources (e.g., Polygon and yfinance)

[1, 23]. We compare coverage, consistency, and delay across sources and keep the better ones; we

then align time and symbols, clean errors and gaps, and form simple features [12, 28]. The cleaned

data is fed into alpha and risk agents. Alpha agents propose signal structures, while tool-based

modules compute the numerical signals, and risk agents compute exposures and limits [24, 3, 9].

We check signals with different metrics (e.g., rank-IC), rolling tests, and a walk-forward backtest

[12, 9, 28].Signal diagnostics (e.g., rank-IC)

…(Full text truncated)…

📸 Image Gallery

Reference

This content is AI-processed based on ArXiv data.