Black-Scholes Model, comparison between Analytical Solution and Numerical Analysis

The main purpose of this article is to give a general overview and understanding of the first widely used option-pricing model, the Black-Scholes model. The history and context are presented, with the

The main purpose of this article is to give a general overview and understanding of the first widely used option-pricing model, the Black-Scholes model. The history and context are presented, with the usefulness and implications in the economics world. A brief review of fundamental calculus concepts is introduced to derive and solve the model. The equation is then resolved using both an analytical (variable separation) and a numerical method (finite differences). Conclusions are drawn in order to understand how Black-Scholes is employed nowadays. At the end a handy appendix (A) is written with some economics notions to ease the reader’s comprehension of the paper; furthermore a second appendix (B) is given with some code scripts, to allow the reader to put in practice some concepts.

💡 Research Summary

The paper provides a comprehensive overview of the Black‑Scholes option‑pricing model, tracing its historical origins, mathematical foundations, and contemporary relevance. It begins with a concise history, noting the seminal 1973 work of Fischer Black and Myron Scholes and the parallel contribution by Robert Merton, establishing the model as the cornerstone of modern financial engineering. The authors then introduce essential economic concepts—risk‑free rate, dividend yield, volatility, strike price, and maturity—to ensure readers from diverse backgrounds can follow the subsequent derivations.

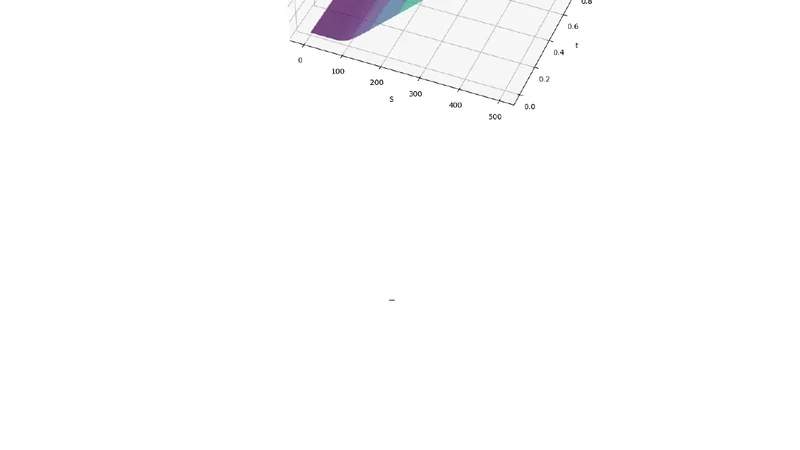

The core of the manuscript is the derivation of the Black‑Scholes partial differential equation (PDE). Starting from a stochastic differential equation for the underlying asset price, the authors apply Itô’s lemma and construct a risk‑neutral hedged portfolio, leading to the well‑known PDE:

\

📜 Original Paper Content

🚀 Synchronizing high-quality layout from 1TB storage...