Learn to Bid as a Price-Maker Wind Power Producer

Wind power producers (WPPs) participating in short-term power markets face significant imbalance costs due to their non-dispatchable and variable production. While some WPPs have a large enough market share to influence prices with their bidding decisions, existing optimal bidding methods rarely account for this aspect. Price-maker approaches typically model bidding as a bilevel optimization problem, but these methods require complex market models, estimating other participants’ actions, and are computationally demanding. To address these challenges, we propose an online learning algorithm that leverages contextual information to optimize WPP bids in the price-maker setting. We formulate the strategic bidding problem as a contextual multi-armed bandit, ensuring provable regret minimization. The algorithm’s performance is evaluated against various benchmark strategies using a numerical simulation of the German day-ahead and real-time markets.

💡 Research Summary

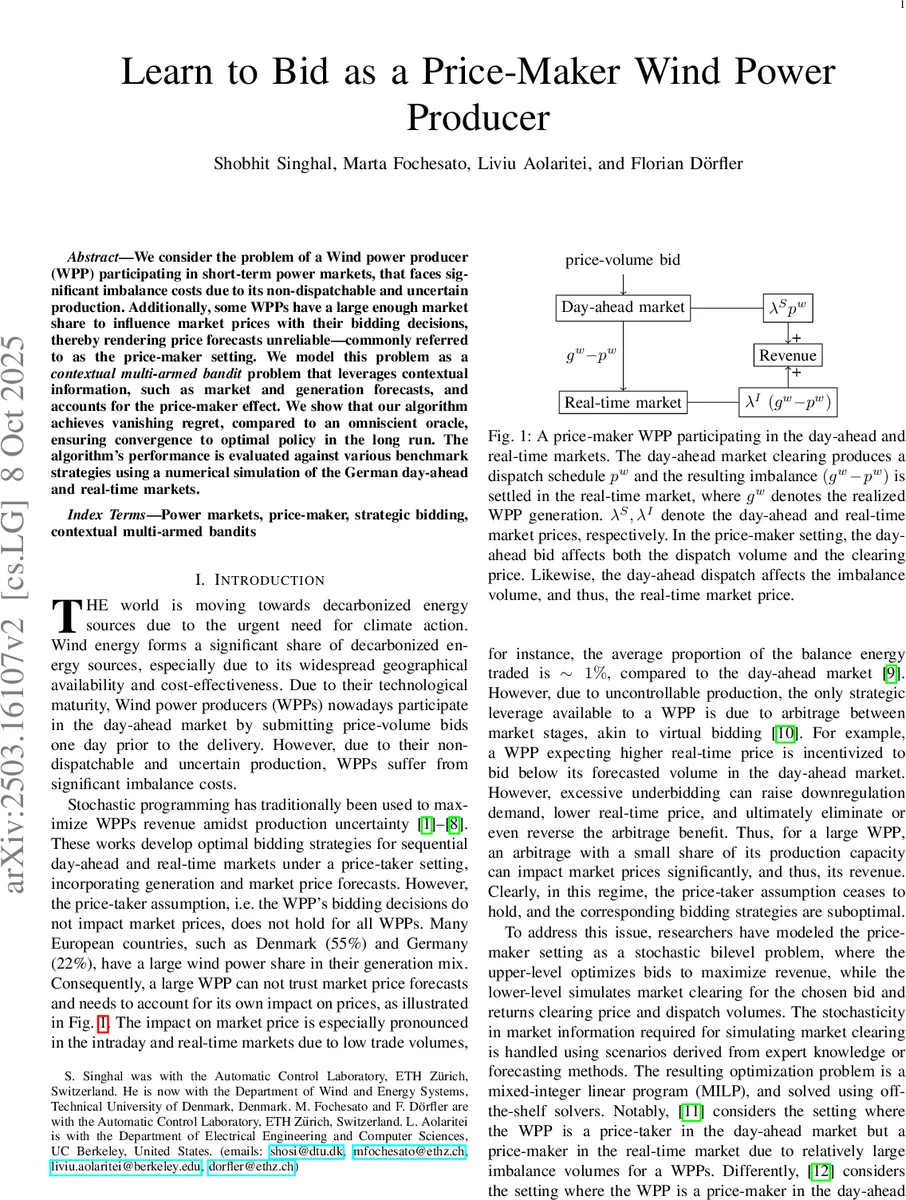

The paper addresses the strategic bidding problem of a wind power producer (WPP) that is large enough to influence market prices—a “price‑maker” in short‑term electricity markets. Traditional approaches either assume a price‑taker setting, using stochastic programming with exogenous forecasts, or model the price‑maker situation as a bilevel optimization problem in which the upper level selects bids and the lower level simulates market clearing. The latter requires detailed knowledge of other participants’ bids, marginal costs, and network constraints, leading to massive mixed‑integer linear programs (MILPs) that become computationally prohibitive when many scenarios are introduced. Moreover, much of the required information is private or only revealed after the market clears, making such methods impractical for real‑time decision making.

To overcome these limitations, the authors reformulate the bidding problem as a contextual multi‑armed bandit (CMAB) task with decision‑dependent uncertainty. At each bidding round t, the WPP observes a context vector xₜ (e.g., wind forecast, demand forecast, fuel prices, and a first‑stage revenue‑sensitivity metric that captures the price‑maker effect). Based on xₜ, the algorithm selects a bid fₜ from a finite set of admissible price‑volume offers. The market clearing process (day‑ahead and real‑time) together with the realized wind generation gₜ produce a revenue πₜ, which is a random variable drawn from a distribution Q(fₜ, xₜ) that depends on both the chosen bid and the context. The objective is to maximize the expected revenue μ(f, x) = E

Comments & Academic Discussion

Loading comments...

Leave a Comment