Leveraging LLMS for Top-Down Sector Allocation In Automated Trading

This paper introduces a methodology leveraging Large Language Models (LLMs) for sector-level portfolio allocation through systematic analysis of macroeconomic conditions and market sentiment. Our framework emphasizes top-down sector allocation by processing multiple data streams simultaneously, including policy documents, economic indicators, and sentiment patterns. Empirical results demonstrate superior risk-adjusted returns compared to traditional cross momentum strategies, achieving a Sharpe ratio of 2.51 and portfolio return of 8.79% versus -0.61 and -1.39% respectively. These results suggest that LLM-based systematic macro analysis presents a viable approach for enhancing automated portfolio allocation decisions at the sector level.

💡 Research Summary

The paper presents a novel, LLM‑driven framework for top‑down sector allocation in automated trading, aiming to fuse macro‑economic analysis with market sentiment in a single systematic pipeline. The authors begin by highlighting a gap in the literature: while many recent studies have applied large language models to bottom‑up stock selection, few have explored how LLMs can enhance macro‑driven, sector‑level decisions. They formulate the research question “How can LLMs be leveraged to improve top‑down sector allocation by integrating macroeconomic analysis with market sentiment for automated portfolio construction?” and propose a solution that treats LLMs as multi‑stream intelligence agents rather than simple predictors.

The related‑work section reviews four strands: (i) cross‑sectional momentum strategies, (ii) macro‑based top‑down investing, (iii) LLM trading agents (news‑driven and reflection‑driven), and (iv) finance‑specific aspect‑based sentiment analysis (ABSA). The authors note that recent advances in memory and reflection modules help mitigate hallucinations and provide a higher‑level understanding of the environment, which motivates their architecture.

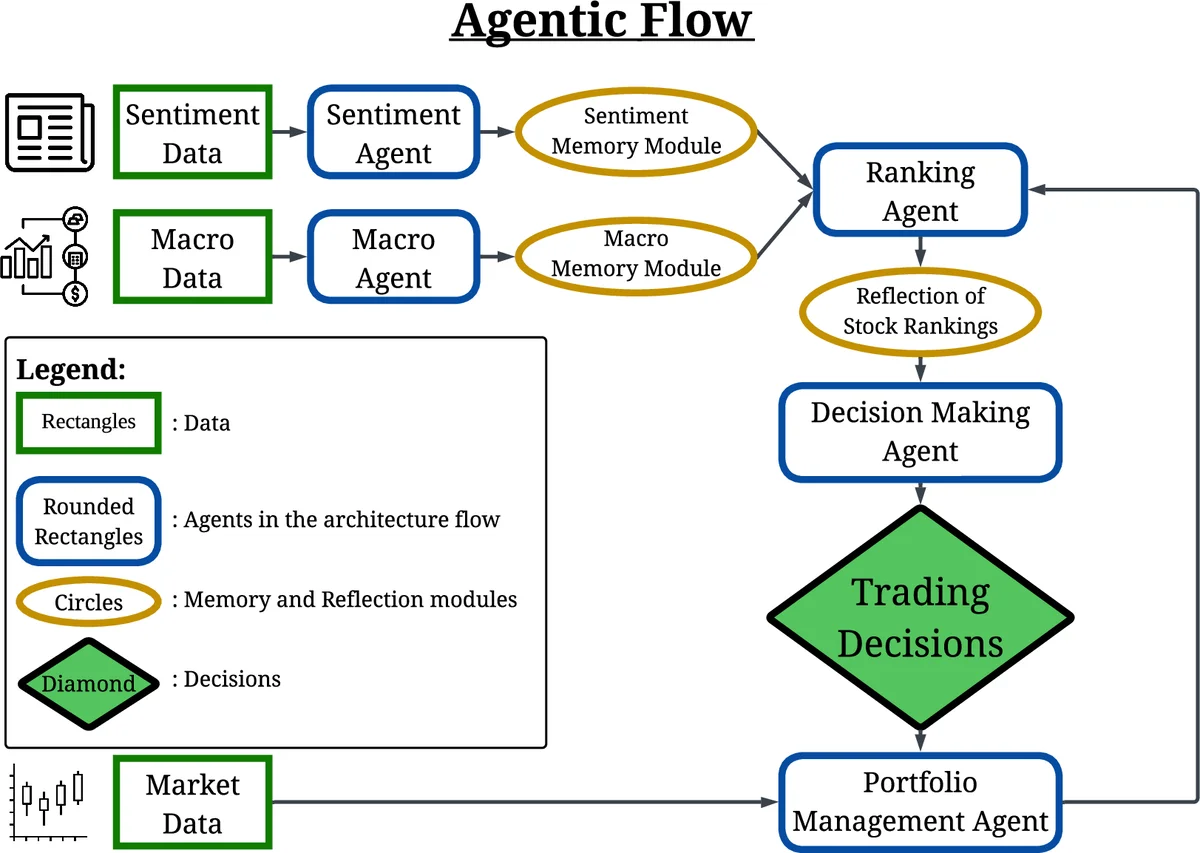

Data collection covers a six‑month back‑testing window (January–June 2019) on the S&P 500 universe, with dynamic updates to avoid survivorship bias. Market data (OHLC, volume) are sourced from AlphaVantage; macro indicators include CPI, PPI, PCE, non‑farm payrolls, PMI, and FOMC minutes. News articles (≈300 k) are scraped via NewsAPI. All sources are time‑stamped to enforce a strict no‑look‑ahead policy.

The system architecture consists of two parallel streams—Sentiment and Macro—feeding a central Ranking Agent. The Sentiment Agent uses the open‑source DeepSeek‑7B‑Chat model to perform Named Entity Recognition (NER) and ABSA on each article, extracting (ticker, aspect, sentiment) triples that are stored in a Sentiment Memory. The Macro Agent converts raw macro numbers into month‑over‑month percentage changes and summarizes FOMC minutes, storing the results in a Macro Memory.

The Ranking Agent executes a three‑phase top‑down allocation: (1) macroeconomic assessment (inflation, growth, policy stance) to infer sector‑level expectations; (2) sector allocation across the 11 GICS sectors using a portfolio optimization routine that aligns target weights with current exposures; (3) sentiment integration, where aspect‑specific sentiment scores refine stock selection within each target sector, allowing the model to amplify positive macro‑aligned sentiment and dampen negative signals. Temporal filtering ensures only information that would have been publicly available at the decision time is used.

Back‑testing compares the proposed LLM‑based strategy against a conventional cross‑sectional momentum benchmark. The LLM approach achieves an 8.79 % annualized return and a Sharpe ratio of 2.51, whereas the benchmark posts a –1.39 % return and a –0.61 Sharpe ratio. Risk analysis shows lower volatility and more balanced sector contributions, indicating that the macro‑sentiment fusion improves both return and risk‑adjusted performance.

The authors acknowledge several limitations: the short six‑month horizon, the modest size of the DeepSeek‑7B‑Chat model, and the computational overhead of memory and reflection modules. They propose future work that includes longer multi‑year evaluations, scaling to larger LLMs (e.g., GPT‑4), incorporating multimodal inputs (charts, images, numeric tables), and developing online learning and advanced risk‑management components.

In conclusion, the study demonstrates that large language models, when equipped with structured memory, reflection, and dual‑stream processing of macroeconomic and textual data, can substantially enhance top‑down sector allocation. The empirical evidence suggests that LLM‑driven systematic macro‑sentiment analysis offers a viable, superior alternative to traditional momentum‑based sector strategies, opening new avenues for AI‑augmented portfolio management.

Comments & Academic Discussion

Loading comments...

Leave a Comment