The Blockchain Risk Parity Line: Moving From The Efficient Frontier To The Final Frontier Of Investments

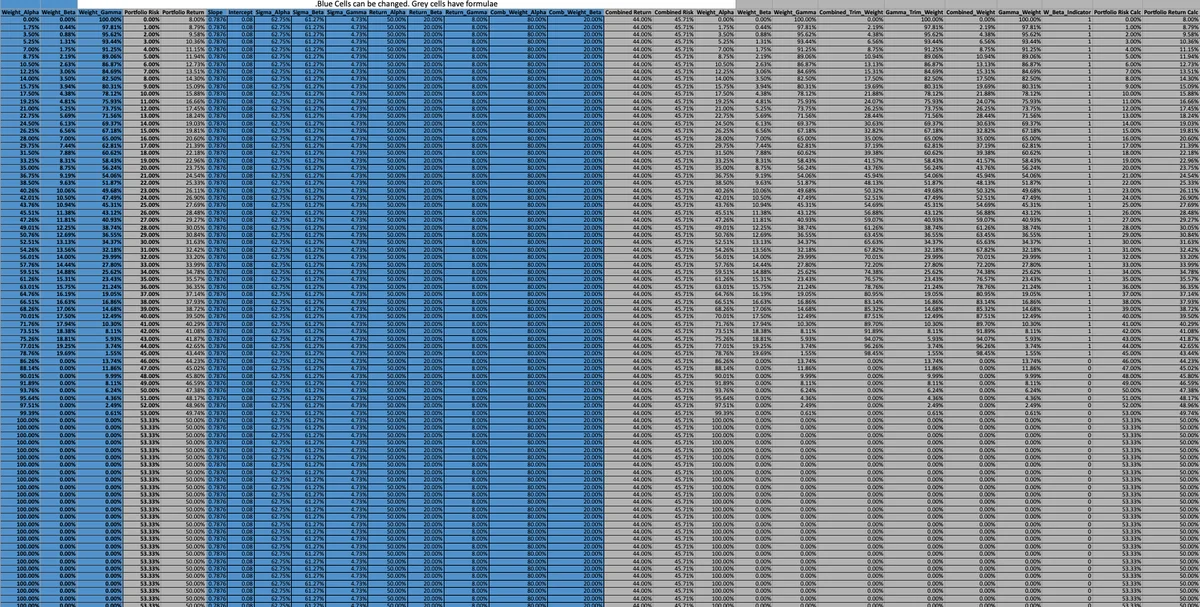

We engineer blockchain based risk managed portfolios by creating three funds with distinct risk and return profiles: 1) Alpha - high risk portfolio; 2) Beta - mimics the wider market; and 3) Gamma - represents the risk free rate adjusted to beat inflation. Each of the sub-funds (Alpha, Beta and Gamma) provides risk parity because the weight of each asset in the corresponding portfolio is set to be inversely proportional to the risk derived from investing in that asset. This can be equivalently stated as equal risk contributions from each asset towards the overall portfolio risk. We provide detailed mechanics of combining assets - including mathematical formulations - to obtain better risk managed portfolios. The descriptions are intended to show how a risk parity based efficient frontier portfolio management engine - that caters to different risk appetites of investors by letting each individual investor select their preferred risk-return combination - can be created seamlessly on blockchain. Any Investor - using decentralized ledger technology - can select their desired level of risk, or return, and allocate their wealth accordingly among the sub funds, which balance one another under different market conditions. This evolution of the risk parity principle - resulting in a mechanism that is geared to do well under all market cycles - brings more robust performance and can be termed as conceptual parity. We have given several numerical examples that illustrate the various scenarios that arise when combining Alpha, Beta and Gamma to obtain Parity. The final investment frontier is now possible - a modification to the efficient frontier, thus becoming more than a mere theoretical construct - on blockchain since anyone from anywhere can participate at anytime to obtain wealth appreciation based on their financial goals.

💡 Research Summary

The paper proposes a novel investment framework called the “Blockchain Risk Parity Line,” which adapts the classic risk‑parity concept to a decentralized ledger environment. The authors construct three sub‑funds—Alpha, Beta, and Gamma—each representing a distinct risk‑return profile. Alpha is a high‑risk, high‑return fund composed of volatile crypto assets and leveraged tokens. Beta mimics the broader market by blending major cryptocurrencies with a modest exposure to traditional assets, aiming to track market‑average performance. Gamma is positioned as a “risk‑free” component, built from stablecoins, tokenized gold, and on‑chain interest‑bearing protocols, with the explicit goal of delivering an inflation‑adjusted real return.

Within each sub‑fund, asset weights are set inversely proportional to the asset’s estimated volatility (σi). The weight formula w_i = (1/σ_i) / Σ_j (1/σ_j) guarantees equal risk contribution (ERC) from every asset, a core tenet of risk‑parity theory. The overall portfolio risk is expressed as √(wᵀ Σ w), where Σ is the covariance matrix derived from on‑chain price feeds and oracle data that are refreshed in real time.

The blockchain implementation relies on smart contracts that accept a single “risk parameter” from the investor (a value between 0 and 1). This parameter is mapped to a blend of Alpha, Beta, and Gamma, allowing users to express any point along a continuum from pure “risk‑free” exposure (Gamma) to pure high‑risk exposure (Alpha). The contracts automatically rebalance the portfolio at predefined intervals, using gas‑efficient optimization algorithms (e.g., ADMM‑based distributed optimization) to minimize transaction costs and slippage. All trades, rebalancing actions, and state changes are immutably recorded on the chain, providing full transparency and auditability.

Through a series of simulations, the authors demonstrate three key findings. First, compared with the traditional efficient frontier, the risk‑parity portfolios achieve higher expected returns for the same level of portfolio volatility. Second, during market stress events (e.g., the 2022 crypto crash), Alpha and Beta experience sharp losses, but Gamma’s stable‑value assets offset much of the drawdown, resulting in a markedly lower overall portfolio volatility. Third, in high‑inflation scenarios, Gamma’s inflation‑adjusted returns preserve real purchasing power, while Alpha and Beta suffer nominal losses. These results motivate the introduction of a “Final Frontier,” an extension of the efficient frontier that incorporates the three sub‑funds and claims to deliver robust performance across all market cycles.

The paper also acknowledges several limitations. Relying solely on volatility to measure risk may ignore tail‑risk, liquidity shocks, and smart‑contract vulnerabilities, potentially leading to excessive leverage in turbulent periods. The assumption that Gamma is risk‑free overlooks systemic blockchain risks such as oracle manipulation, stablecoin de‑pegging, and regulatory uncertainty. Moreover, the cost of on‑chain rebalancing (gas fees, network congestion) and the latency of price oracles can erode the theoretical advantages of continuous ERC. The authors suggest that a more comprehensive multi‑risk framework—incorporating liquidity, counterparty, and operational risks—would be necessary for real‑world deployment.

In summary, the manuscript offers an intriguing blend of risk‑parity theory and decentralized finance, presenting a clear mathematical foundation, a smart‑contract‑driven allocation engine, and illustrative numerical examples. While the conceptual contribution is solid, practical adoption will require deeper risk modeling, cost‑efficient rebalancing mechanisms, and thorough regulatory compliance assessments. The “Blockchain Risk Parity Line” thus represents a promising step toward democratized, risk‑aware investing, but its ultimate success hinges on addressing the identified technical and systemic challenges.