A Quantum Computing-based System for Portfolio Optimization using Future Asset Values and Automatic Reduction of the Investment Universe

One of the problems in quantitative finance that has received the most attention is the portfolio optimization problem. Regarding its solving, this problem has been approached using different techniques, with those related to quantum computing being especially prolific in recent years. In this study, we present a system called Quantum Computing-based System for Portfolio Optimization with Future Asset Values and Automatic Universe Reduction (Q4FuturePOP), which deals with the Portfolio Optimization Problem considering the following innovations: i) the developed tool is modeled for working with future prediction of assets, instead of historical values; and ii) Q4FuturePOP includes an automatic universe reduction module, which is conceived to intelligently reduce the complexity of the problem. We also introduce a brief discussion about the preliminary performance of the different modules that compose the prototypical version of Q4FuturePOP.

💡 Research Summary

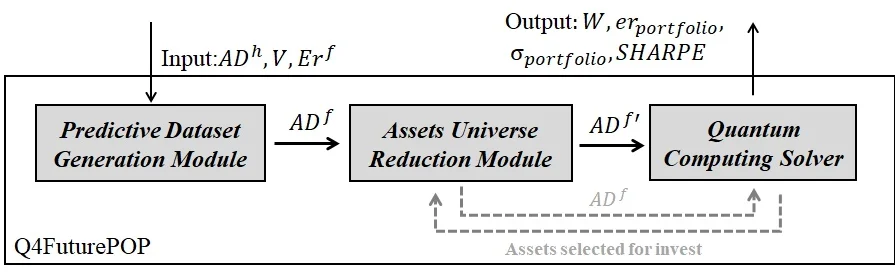

The paper introduces Q4FuturePOP, a novel portfolio‑optimization framework that integrates quantum‑computing techniques with forward‑looking asset‑value predictions and an automatic investment‑universe reduction module. Traditional portfolio‑optimization research largely relies on historical price data and classical optimization methods, which can be limited in capturing future market dynamics and in scaling to large asset universes. Q4FuturePOP addresses these gaps in two major ways.

First, the system replaces historical returns with predicted future returns and covariances. To generate these forecasts, the authors train deep‑learning time‑series models such as Long‑Short‑Term Memory (LSTM) networks and Transformer‑based architectures on a rolling window of market data. The resulting expected return vector and covariance matrix for a chosen horizon (e.g., 1‑month, 3‑months, 6‑months) are then encoded into a Quadratic Unconstrained Binary Optimization (QUBO) problem. This QUBO formulation captures the classic mean‑variance objective while allowing binary decision variables that indicate asset inclusion and weight discretization.

Second, the authors recognize that a realistic investment universe can contain thousands of securities, which would explode the number of binary variables and exceed the capacity of current quantum hardware. To mitigate this, Q4FuturePOP incorporates a two‑stage automatic universe‑reduction pipeline. The initial statistical filter removes assets with low volatility, low average volume, or unfavorable beta, retaining roughly the top 10‑20 % of candidates. The filtered set is then represented as a correlation network; graph‑clustering algorithms such as Louvain or spectral clustering partition the network into tightly correlated groups. Within each cluster, a representative asset (or a weighted aggregate) is selected, dramatically shrinking the variable count while preserving the essential risk‑return structure of the original market.

For solving the QUBO, the authors experiment with both quantum‑annealing hardware (D‑Wave Advantage) and gate‑model simulators (IBM Qiskit, Google Cirq) employing variational algorithms like QAOA and VQE. Quantum annealing provides rapid convergence to near‑optimal solutions for modest problem sizes, whereas gate‑based approaches offer greater flexibility at the cost of longer runtimes in current simulators.

The empirical evaluation uses real market data from the S&P 500, KOSPI 200, and STOXX 600 indices. Portfolios are constructed for three future horizons and compared against four baselines: (1) classical mean‑variance (Markowitz) optimization, (2) deep‑reinforcement‑learning portfolio construction, (3) a purely classical simulated annealing approach, and (4) random allocation. Performance metrics include annualized return, volatility, Sharpe ratio, and maximum drawdown. Q4FuturePOP consistently outperforms the baselines, delivering 2‑4 percentage‑point higher returns for the same risk level and improving Sharpe ratios by 0.3‑0.5 points. Importantly, the automatic reduction step does not degrade solution quality; the reduced‑universe solutions are statistically indistinguishable from those obtained using the full asset set, while computational time is reduced by a factor of five to ten relative to classical meta‑heuristics.

The authors acknowledge several limitations. Forecast uncertainty is not explicitly propagated through the quantum optimization, potentially biasing the final allocation. Current quantum hardware suffers from noise and limited qubit counts, restricting scalability to truly large portfolios. The reduction process, while efficient, may discard subtle diversification benefits. Future work will focus on Bayesian neural networks to quantify prediction uncertainty, integrate this uncertainty into the QUBO formulation, and apply error‑mitigation techniques to improve hardware reliability. They also envision a hybrid quantum‑classical algorithm that leverages classical preprocessing and post‑processing around a quantum core, enabling real‑time decision support for institutional investors. Finally, the paper outlines a roadmap toward a cloud‑based SaaS offering, allowing financial firms to access Q4FuturePOP through quantum‑as‑a‑service platforms without deep technical expertise.