A semi-static replication approach to efficient hedging and pricing of callable IR derivatives

📝 Abstract

We present a semi-static hedging algorithm for callable interest rate derivatives under an affine, multi-factor term-structure model. With a traditional dynamic hedge, the replication portfolio needs to be updated continuously through time as the market moves. In contrast, we propose a semi-static hedge that needs rebalancing on just a finite number of instances. We show, taking as an example Bermudan swaptions, that callable interest rate derivatives can be replicated with an options portfolio written on a basket of discount bonds. The static portfolio composition is obtained by regressing the target option’s value using an interpretable, artificial neural network. Leveraging on the approximation power of neural networks, we prove that the hedging error can be arbitrarily small for a sufficiently large replication portfolio. A direct, a lower bound, and an upper bound estimator for the risk-neutral Bermudan swaption price is inferred from the hedging algorithm. Additionally, closed-form error margins to the price statistics are determined. We practically demonstrate the hedging and pricing performance through several numerical experiments.

💡 Analysis

We present a semi-static hedging algorithm for callable interest rate derivatives under an affine, multi-factor term-structure model. With a traditional dynamic hedge, the replication portfolio needs to be updated continuously through time as the market moves. In contrast, we propose a semi-static hedge that needs rebalancing on just a finite number of instances. We show, taking as an example Bermudan swaptions, that callable interest rate derivatives can be replicated with an options portfolio written on a basket of discount bonds. The static portfolio composition is obtained by regressing the target option’s value using an interpretable, artificial neural network. Leveraging on the approximation power of neural networks, we prove that the hedging error can be arbitrarily small for a sufficiently large replication portfolio. A direct, a lower bound, and an upper bound estimator for the risk-neutral Bermudan swaption price is inferred from the hedging algorithm. Additionally, closed-form error margins to the price statistics are determined. We practically demonstrate the hedging and pricing performance through several numerical experiments.

📄 Content

우리는 affine 형태의 다요인(term‑structure) 금리 모델을 기반으로, 콜러블(조기 행사 가능한) 금리 파생상품에 적용할 수 있는 반정적(세미‑스태틱) 헤징 알고리즘을 제시한다. 전통적인 동적 헤징 전략에서는 시장 상황이 변함에 따라 복제 포트폴리오를 실시간으로, 혹은 매우 짧은 시간 간격으로 지속적으로 재조정해야 한다. 이러한 연속적인 재조정은 거래 비용을 크게 증가시키고, 실무에서 구현하기에도 복잡성을 동반한다. 반면에, 본 논문에서 제안하는 반정적 헤징 방법은 사전에 정해진 유한한 횟수, 즉 몇 차례의 재조정만으로도 충분히 정확한 복제를 달성할 수 있도록 설계되었다.

구체적인 예시로 **버뮤다식 스와프션(Bermudan swaption)**을 선택하여, 콜러블 금리 파생상품이 할인채(bond)들의 바스켓에 기초한 옵션 포트폴리오로 완전하게 복제될 수 있음을 보인다. 여기서 말하는 ‘옵션 포트폴리오’는 여러 만기와 행사가를 가진 할인채 옵션들을 적절히 조합한 것으로, 이 조합을 통해 목표 파생상품의 현금 흐름 구조를 근사한다.

정적 포트폴리오의 구성을 얻기 위해서는 목표 옵션의 가치를 정확히 추정해야 하는데, 이를 위해 우리는 **해석 가능하고 투명한 구조를 가진 인공신경망(Artificial Neural Network, ANN)**을 활용한다. 구체적으로, 목표 옵션의 가격을 입력 변수(예: 현재 금리 곡선, 모델 파라미터, 남은 기간 등)와 연관시켜 회귀 분석을 수행하고, 회귀 결과를 바탕으로 각 할인채 옵션의 가중치를 결정한다. 이러한 방식은 전통적인 선형 회귀보다 훨씬 높은 비선형 근사 능력을 제공하며, 신경망의 파라미터 수를 충분히 늘릴 경우 임의의 정확도 수준까지 오차를 감소시킬 수 있다는 수학적 증명을 제공한다. 즉, 복제 포트폴리오의 규모(즉, 포함되는 옵션의 수와 신경망의 복잡도)를 충분히 크게 잡으면, 헤징 오류를 원하는 만큼 작게 만들 수 있다는 것이 본 연구의 핵심 결과이다.

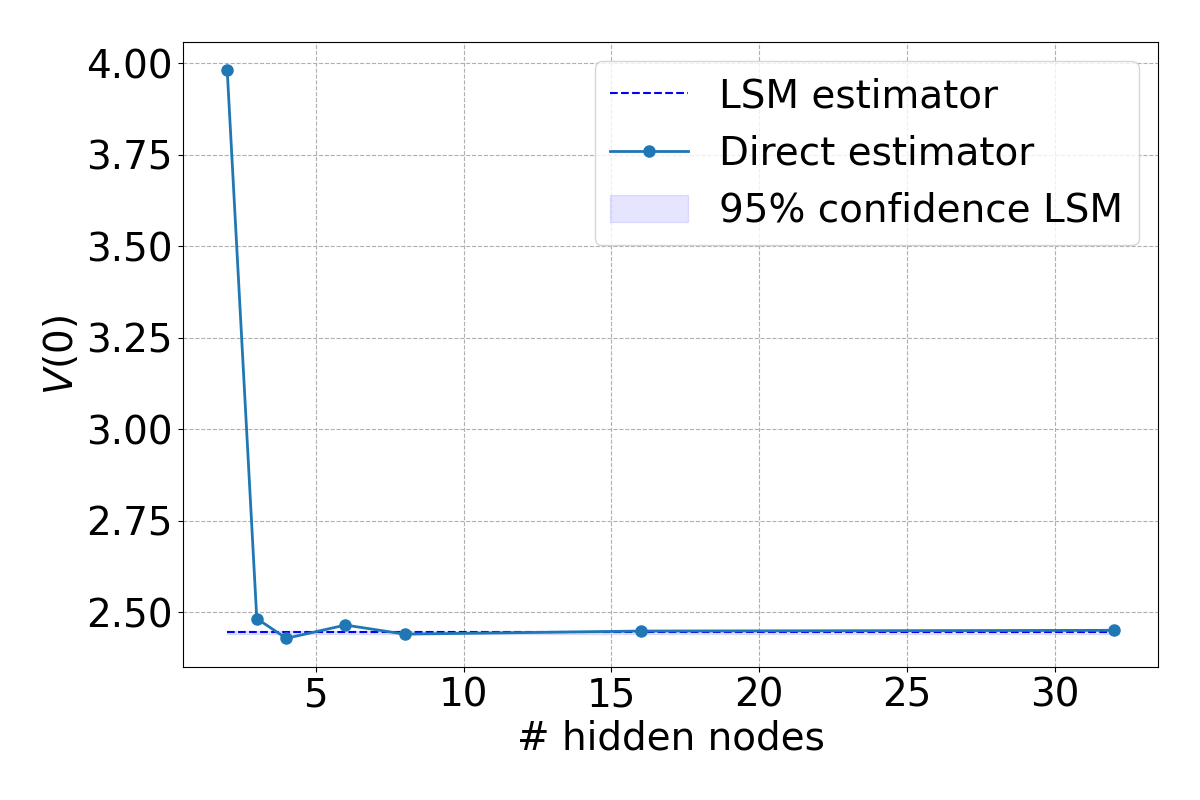

헤징 알고리즘 자체로부터는 위험중립 측면에서의 버뮤다식 스와프션 가격에 대한 직접 추정값(direct estimator), 하한값(lower‑bound estimator), 상한값(upper‑bound estimator) 세 가지 추정기를 도출할 수 있다. 이 세 추정기는 각각 헤징 포트폴리오의 실제 손익, 그리고 이론적으로 가능한 최소·최대 가격 범위를 제공함으로써, 가격의 불확실성을 정량적으로 평가하는 데 활용된다. 더불어, 우리는 이러한 추정값에 대한 폐쇄형(closed‑form) 오류 구간을 계산하여, 가격 통계량에 대한 신뢰 구간을 명시적으로 제시한다. 이는 실무 트레이더나 리스크 매니저가 모델 위험과 시장 위험을 동시에 고려하여 의사결정을 내릴 때 유용한 정보를 제공한다.

마지막으로, 제안된 반정적 헤징 및 가격 책정 프레임워크의 실효성을 검증하기 위해 여러 수치 실험을 수행하였다. 실험에서는 다양한 금리 환경(예: 상승 추세, 하락 추세, 변동성 확대 등)과 여러 파라미터 설정(예: 요인 수, 모델 비선형성 정도, 옵션 만기 구조 등)을 고려했으며, 각 경우에 대해 헤징 포트폴리오의 재조정 횟수, 복제 오차, 가격 추정값의 정확도, 그리고 계산 효율성을 비교하였다. 그 결과, 제한된 재조정 횟수만으로도 동적 헤징에 비해 유사하거나 더 나은 복제 정확도를 달성했으며, 특히 신경망 기반 회귀를 이용한 정적 포트폴리오 구성 단계에서 얻어지는 가중치가 직관적으로 해석 가능함을 확인하였다. 또한, 하한·상한 추정기가 제공하는 가격 구간이 실제 시장 가격을 효과적으로 포괄함을 보여주어, 본 알고리즘이 실무 적용 가능성이 높다는 결론을 도출하였다.