Profit Puzzles or: Public Firm Profits Have Fallen

We show that public firm profit rates fell by half since 1980. Inferred as the residual from the rise of US corporate profit rates in aggregate data, private firm profit rates doubled since 1980. Public firm financial returns matched their fall in profit rates, while public firm representativeness increased from 30% to 60% of the US capital stock. These results imply that time-varying selection biases in extrapolating public firms to the aggregate economy can be severe.

💡 Research Summary

The paper “Profit Puzzles or: Public Firm Profits Have Fallen” investigates the divergent trajectories of profit rates for publicly listed firms and private (non‑public) firms in the United States from 1980 to 2020. Using two complementary data sources, the authors construct parallel measures of profit‑to‑capital ratios. The macro‑level series is derived from the Bureau of Economic Analysis (BEA) National Income and Product Accounts (NIPA) and Fixed Asset tables, where profits are defined as gross value added minus taxes and labor compensation, and capital is taken from the non‑residential private capital stock. The micro‑level series comes from Compustat merged with CRSP, after dropping utilities, financial institutions, foreign‑incorporated firms, and observations with missing values. In this sample, profits are measured as cash earnings after taxes but before interest and depreciation (the sum of income before extraordinary items, extraordinary items, deferred taxes, interest expense, and depreciation/amortization). Capital is measured as book capital, i.e., long‑term debt plus short‑term debt plus book equity (total assets minus total liabilities plus deferred tax credits).

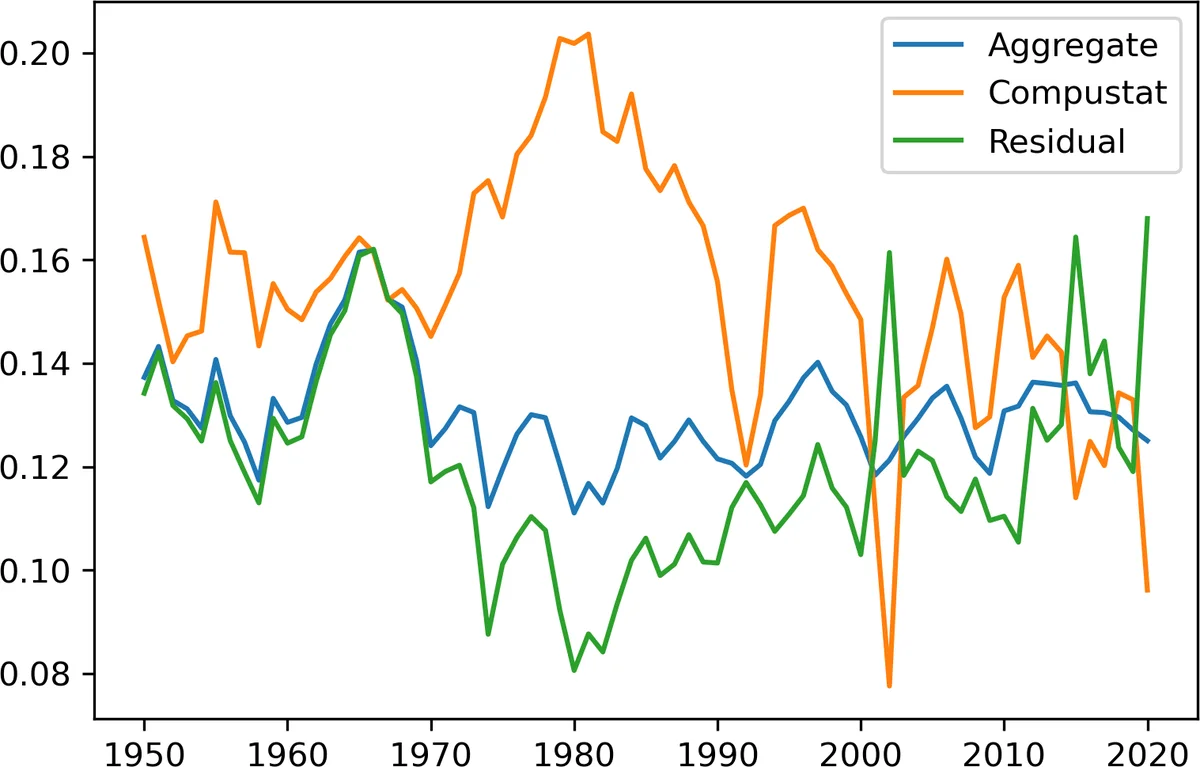

The authors define the profit‑to‑capital ratio π = X/K, which is invariant to inflation and other dynamic scaling issues. They compute π for public firms (π_public) and for the aggregate economy (π_macro). The share of aggregate capital represented in the Compustat sample, w = K_Compustat / K_macro, rises from roughly 0.1 in the 1950s to about 0.6 by 2020, reflecting the dramatic expansion of listed firms and the increasing weight of public firms in the U.S. capital stock. By solving the identity

π_macro = w·π_public + (1 − w)·π_private

they back out the implied private‑firm profit‑to‑capital ratio (π_private). The results show a clear divergence: π_public peaked around 20 % in the 1970s, fell to roughly 12 % by the 2010s—a roughly 50 % decline—while π_private has roughly doubled over the same period. The aggregate ratio π_macro, in contrast, is relatively flat after the early 1970s, confirming that the rise in private‑firm profitability offsets the decline in public‑firm profitability.

Robustness checks include: (i) alternative capital definitions (market value of equity V instead of book capital), which yields an even steeper decline in the profit‑to‑market‑capital ratio; (ii) alternative weighting schemes (w = 0.3, 0.5) that still preserve the divergent trends; (iii) 10‑year moving averages of returns on capital (r_K) and returns on market value (r_V), showing that while r_K declines sharply, r_V is more volatile and partially offset by capital gains; (iv) adjustments for cash holdings (X/(K‑cash)) and goodwill (X/GDW) to rule out the possibility that rising cash balances or goodwill accumulation drive the profit decline. None of these adjustments alter the core finding.

The paper situates its contribution within two strands of literature. First, it challenges the narrative that rising market power and mark‑ups have universally increased aggregate profit shares, as suggested by recent macro studies (e.g., De Loecker et al., 2020; Barkai, 2020). The authors argue that any aggregate increase in profit shares must be coming from the private sector, not the public sector. Second, it adds to the growing evidence that public and private firms behave differently in terms of growth dispersion, concentration measures, and response to macro shocks (David et al., 2006; Ali et al., 2008).

The policy and methodological implications are significant. Researchers who extrapolate findings from public‑firm data to the whole economy—such as estimates of discount rates, market power, or the effective interest rate on capital—risk severe bias because the composition of the sample changes over time. The paper recommends explicitly accounting for the time‑varying representativeness of public‑firm data, perhaps by weighting observations with the evolving w ratio or by incorporating private‑firm data where possible.

In summary, the study provides compelling evidence that U.S. public‑firm profit rates have halved since 1980, while private‑firm profit rates have roughly doubled, and that public firms now represent a much larger share of the capital stock. These dynamics generate substantial selection bias when public‑firm data are used as a proxy for the aggregate economy, urging caution and methodological adjustments in macro‑financial research.

Comments & Academic Discussion

Loading comments...

Leave a Comment