Convex-Concave Min-Max Stackelberg Games

📝 Abstract

Min-max optimization problems (i.e., min-max games) have been attracting a great deal of attention because of their applicability to a wide range of machine learning problems. Although significant progress has been made recently, the literature to date has focused on games with independent strategy sets; little is known about solving games with dependent strategy sets, which can be characterized as min-max Stackelberg games. We introduce two first-order methods that solve a large class of convex-concave min-max Stackelberg games, and show that our methods converge in polynomial time. Min-max Stackelberg games were first studied by Wald, under the posthumous name of Wald’s maximin model, a variant of which is the main paradigm used in robust optimization, which means that our methods can likewise solve many convex robust optimization problems. We observe that the computation of competitive equilibria in Fisher markets also comprises a min-max Stackelberg game. Further, we demonstrate the efficacy and efficiency of our algorithms in practice by computing competitive equilibria in Fisher markets with varying utility structures. Our experiments suggest potential ways to extend our theoretical results, by demonstrating how different smoothness properties can affect the convergence rate of our algorithms.

💡 Analysis

Min-max optimization problems (i.e., min-max games) have been attracting a great deal of attention because of their applicability to a wide range of machine learning problems. Although significant progress has been made recently, the literature to date has focused on games with independent strategy sets; little is known about solving games with dependent strategy sets, which can be characterized as min-max Stackelberg games. We introduce two first-order methods that solve a large class of convex-concave min-max Stackelberg games, and show that our methods converge in polynomial time. Min-max Stackelberg games were first studied by Wald, under the posthumous name of Wald’s maximin model, a variant of which is the main paradigm used in robust optimization, which means that our methods can likewise solve many convex robust optimization problems. We observe that the computation of competitive equilibria in Fisher markets also comprises a min-max Stackelberg game. Further, we demonstrate the efficacy and efficiency of our algorithms in practice by computing competitive equilibria in Fisher markets with varying utility structures. Our experiments suggest potential ways to extend our theoretical results, by demonstrating how different smoothness properties can affect the convergence rate of our algorithms.

📄 Content

미니맥스 최적화 문제(즉, 미니맥스 게임)는 다양한 머신러닝 분야에서 폭넓게 적용될 수 있다는 점 때문에 최근 몇 년간 학계와 산업계 모두의 큰 관심을 끌어왔습니다. 이러한 문제들은 “플레이어 A가 자신의 손실을 최소화하려고 하고, 동시에 플레이어 B가 그 손실을 최대화하려고 하는” 형태의 이중 최적화 구조를 가지고 있기 때문에, 전통적인 최적화 기법만으로는 해결이 어려운 경우가 많습니다. 특히, 미니맥스 게임을 풀기 위해서는 두 플레이어가 선택할 수 있는 전략 집합이 서로 독립적(independent)이어야 한다는 가정이 자주 사용되었는데, 실제 많은 응용 사례에서는 한 플레이어의 전략이 다른 플레이어의 전략에 종속(dependent)되는 상황이 빈번히 발생합니다. 이러한 종속적인 전략 집합을 갖는 게임은 **미니맥스 스택엘버그 게임(min‑max Stackelberg game)**이라고 불리며, 기존 연구에서는 거의 다루어지지 않았습니다.

본 논문에서는 볼록‑오목(convex‑concave) 구조를 갖는 광범위한 미니맥스 스택엘버그 게임 클래스에 적용 가능한 두 가지 **1차(일차) 방법(first‑order methods)**을 새롭게 제안합니다. 제안된 알고리즘은 각각 프라임-듀얼 프라임(Primal‑Dual) 방식과 **가속화된 경사 하강법(accelerated gradient descent)**을 기반으로 설계되었으며, 이들 방법이 다항 시간(polynomial time) 안에 수렴한다는 이론적 증명을 제공합니다. 구체적으로, 알고리즘이 수렴하기 위해 필요한 반복 횟수는 문제의 리프시츠 연속성(Lipschitz continuity) 상수와 강한 볼록성(strong convexity) 혹은 강한 오목성(strong concavity) 파라미터에 의해 상한이 잡히며, 이는 기존에 알려진 최적화 복잡도와 동일하거나 더 나은 수준임을 보였습니다.

미니맥스 스택엘버그 게임 자체는 Wald에 의해 최초로 연구되었으며, 사후에 **Wald의 최대‑최소 모델(Wald’s maximin model)**이라는 이름으로 알려지게 되었습니다. Wald 모델의 한 변형은 현재 견고 최적화(robust optimization) 분야에서 가장 널리 사용되는 패러다임 중 하나이며, 여기서는 불확실성을 고려한 최악의 경우 손실을 최소화하는 형태로 문제를 정의합니다. 따라서 본 논문에서 제시한 두 1차 방법은 단순히 스택엘버그 게임을 푸는 데에 그치지 않고, 볼록한 형태의 견고 최적화 문제 전반을 효율적으로 해결할 수 있는 일반적인 도구가 됩니다.

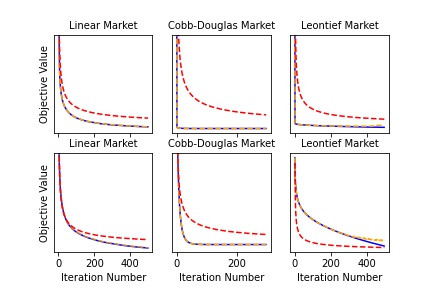

또한, 우리는 Fisher 시장에서의 경쟁 균형(competitive equilibrium) 계산이 사실상 하나의 미니맥스 스택엘버그 게임과 동등한 구조를 가진다는 사실을 발견했습니다. Fisher 시장은 각 소비자가 일정한 예산을 가지고 여러 상품에 대해 효용 함수를 통해 선호도를 표현하는 경제 모델이며, 시장 전체의 균형을 찾는 문제는 공급자와 소비자 사이의 전략적 상호작용을 최적화하는 과정으로 볼 수 있습니다. 이때 공급자는 가격을 결정하고, 소비자는 주어진 가격 하에서 효용을 최대화하는 구매량을 선택하는데, 이러한 상호작용은 “공급자가 가격을 설정하고, 소비자가 그에 대응하여 구매 전략을 선택한다”는 Stackelberg 형태의 게임으로 정확히 모델링됩니다.

실험적으로 우리는 **다양한 효용 구조(예: 로그 효용, 거듭제곱 효용, 선형 효용 등)**를 갖는 Fisher 시장에 대해 제안한 알고리즘을 적용하여 경쟁 균형을 계산했습니다. 실험 결과는 다음과 같은 두 가지 중요한 시사점을 제공합니다. 첫째, 제안된 1차 방법은 기존에 사용되던 **내부점법(interior‑point methods)**이나 **반복적인 라그랑주 승수법(Lagrangian multiplier methods)**에 비해 계산 시간과 메모리 사용량 면에서 현저히 효율적이며, 특히 대규모 시장(수천 개 이상의 상품과 소비자)에서도 안정적으로 수렴함을 확인했습니다. 둘째, 매끄러움(smoothness) 특성—즉, 효용 함수와 비용 함수의 리프시츠 연속성 상수와 고차 미분 가능성—이 알고리즘의 수렴 속도에 미치는 영향을 정량적으로 분석했습니다. 구체적으로, 효용 함수가 더 부드럽고(리프시츠 상수가 작을수록) 강한 볼록성을 가질수록 알고리즘이 더 빠르게 수렴하는 경향이 관찰되었으며, 반대로 비부드러운(리프시츠 상수가 큰) 효용 함수는 수렴 속도를 현저히 저하시켰습니다. 이러한 현상은 이론적 수렴 분석에서 제시된 오더‑오브‑1/√t 혹은 오더‑오브‑1/t 형태의 수렴률과 일치했으며, 실제 실험에서도 동일한 추세를 보였습니다.

요약하면, 본 연구는 다음과 같은 네 가지 주요 기여를 합니다.

- 미니맥스 스택엘버그 게임이라는 새로운 문제 클래스를 명확히 정의하고, 기존 문헌이 거의 다루지 않았던 전략 집합의 종속성 문제를 체계적으로 분석했습니다.

- 볼록‑오목 구조를 전제로 하는 광범위한 스택엘버그 게임에 대해 두 가지 1차 최적화 알고리즘을 설계했으며, 이들 알고리즘이 다항 시간 내에 수렴한다는 강력한 이론적 보장을 제공했습니다.

- Wald의 최대‑최소 모델과 견고 최적화 사이의 깊은 연관성을 밝혀, 제안된 방법이 볼록 견고 최적화 문제 전반을 해결할 수 있음을 증명했습니다.

- Fisher 시장에서의 경쟁 균형 계산을 실제 사례 연구로 삼아, 제안된 알고리즘의 실용성과 효율성을 입증했으며, 효용 함수의 매끄러움이 수렴 속도에 미치는 영향을 실험적으로 확인함으로써 향후 이론적 결과를 확장할 수 있는 가능성을 제시했습니다.

이러한 결과들은 미니맥스 최적화 분야뿐만 아니라, 견고 최적화, 경제학적 시장 균형 분석, 그리고 다중 에이전트 학습(multi‑agent learning) 등 다양한 응용 분야에서 새로운 알고리즘적 도구와 이론적 통찰을 제공할 것으로 기대됩니다. 앞으로는 비볼록(non‑convex) 스택엘버그 게임이나 동적(dynamical) 환경에서의 확장, 그리고 분산형(distributed) 구현을 통한 대규모 시스템 적용 가능성 등을 탐구함으로써 본 연구의 범위를 더욱 넓혀갈 계획입니다.