AI in Finance: Challenges, Techniques and Opportunities

AI in finance broadly refers to the applications of AI techniques in financial businesses. This area has been lasting for decades with both classic and modern AI techniques applied to increasingly broader areas of finance, economy and society. In contrast to either discussing the problems, aspects and opportunities of finance that have benefited from specific AI techniques and in particular some new-generation AI and data science (AIDS) areas or reviewing the progress of applying specific techniques to resolving certain financial problems, this review offers a comprehensive and dense roadmap of the overwhelming challenges, techniques and opportunities of AI research in finance over the past decades. The landscapes and challenges of financial businesses and data are firstly outlined, followed by a comprehensive categorization and a dense overview of the decades of AI research in finance. We then structure and illustrate the data-driven analytics and learning of financial businesses and data. The comparison, criticism and discussion of classic vs. modern AI techniques for finance are followed. Lastly, open issues and opportunities address future AI-empowered finance and finance-motivated AI research.

💡 Research Summary

The paper provides a comprehensive roadmap of artificial intelligence (AI) research as it pertains to finance, covering the evolution of challenges, techniques, and opportunities over several decades. It begins by outlining the distinctive characteristics of financial businesses and their data ecosystems. Financial data are highly heterogeneous, encompassing high‑frequency trade logs, credit histories, market prices, news articles, social‑media sentiment, and even multimedia content. This data is marked by real‑time requirements, regulatory constraints, privacy concerns, and the presence of both structured and unstructured formats, which together create a demanding environment for analytical models.

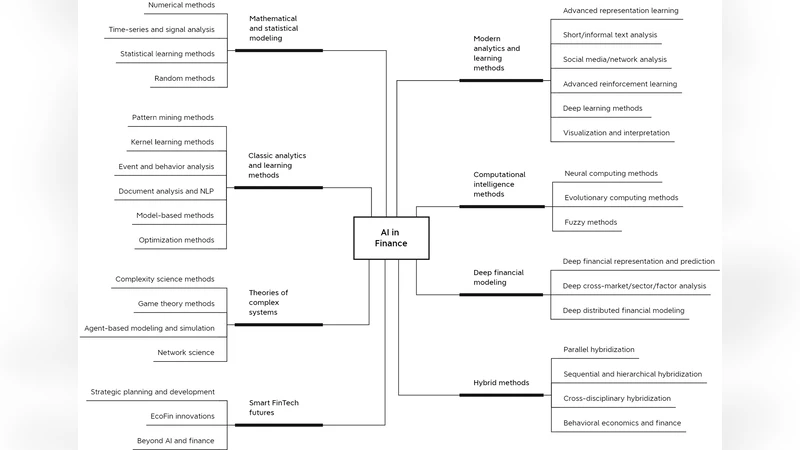

The authors then present a chronological taxonomy of AI research in finance. In the early 1990s and early 2000s, rule‑based expert systems and classic machine‑learning algorithms such as linear regression, support vector machines, and decision trees dominated. These methods were applied to portfolio optimization, risk measurement, credit scoring, and fraud detection, benefiting from relatively low data requirements and high interpretability. As data volumes grew and computational resources expanded in the mid‑2000s, ensemble techniques (random forests, boosting), reinforcement learning, and graph‑based models entered the scene, especially for high‑frequency trading and algorithmic strategy refinement.

The last decade has witnessed a paradigm shift toward deep learning and generative AI. Recurrent architectures (LSTM, GRU) and attention‑based Transformers dominate time‑series forecasting, while convolutional networks handle image‑related tasks such as document verification. Transformer‑based language models (e.g., GPT‑series) have been leveraged for sentiment analysis of news and social media, automated report generation, contract review, and conversational customer service. Multimodal models that fuse text, audio, and visual signals enable more holistic market insights. Moreover, synthetic data generation, federated learning, and differential privacy are discussed as ways to mitigate data scarcity and privacy regulations while preserving model performance.

A central contribution of the review is the systematic comparison of “classic” AI versus “modern” AI for finance. Classic AI offers transparency, lower computational cost, and easier regulatory compliance, but struggles with complex non‑linear relationships and large‑scale unstructured data. Modern AI delivers superior representation power and scalability but introduces black‑box opacity, higher energy consumption, and challenges in explainability and auditability. The paper surveys emerging solutions such as Explainable AI (XAI), model compression, pruning, and post‑hoc interpretation techniques that aim to reconcile performance with regulatory demands.

The authors also map the end‑to‑end data‑driven workflow: data acquisition, preprocessing, feature engineering, model training, deployment, and continuous monitoring. They highlight practical issues such as data quality, label scarcity, concept drift in time‑series, and the need for automated model retraining pipelines.

In the final sections, the paper identifies open research questions and future opportunities. Unresolved challenges include robust privacy‑preserving methods under GDPR/CCPA, achieving regulatory‑ready explainability, reducing the carbon footprint of large models, and developing domain‑adaptive transfer learning that can generalize across markets, asset classes, and geographies. On the opportunity side, AI is poised to create new financial products (AI‑generated derivatives, personalized wealth‑management advisors), real‑time systemic‑risk monitoring platforms, and to inspire finance‑driven AI research such as market‑mechanism design via reinforcement learning.

Overall, the review synthesizes decades of AI‑finance literature into a dense, structured overview, offering both scholars and practitioners a clear view of past achievements, current state‑of‑the‑art techniques, and a forward‑looking agenda for AI‑empowered finance.

Comments & Academic Discussion

Loading comments...

Leave a Comment