Fair Regression for Health Care Spending

The distribution of health care payments to insurance plans has substantial consequences for social policy. Risk adjustment formulas predict spending in health insurance markets in order to provide fair benefits and health care coverage for all enrollees, regardless of their health status. Unfortunately, current risk adjustment formulas are known to underpredict spending for specific groups of enrollees leading to undercompensated payments to health insurers. This incentivizes insurers to design their plans such that individuals in undercompensated groups will be less likely to enroll, impacting access to health care for these groups. To improve risk adjustment formulas for undercompensated groups, we expand on concepts from the statistics, computer science, and health economics literature to develop new fair regression methods for continuous outcomes by building fairness considerations directly into the objective function. We additionally propose a novel measure of fairness while asserting that a suite of metrics is necessary in order to evaluate risk adjustment formulas more fully. Our data application using the IBM MarketScan Research Databases and simulation studies demonstrate that these new fair regression methods may lead to massive improvements in group fairness (e.g., 98%) with only small reductions in overall fit (e.g., 4%).

💡 Research Summary

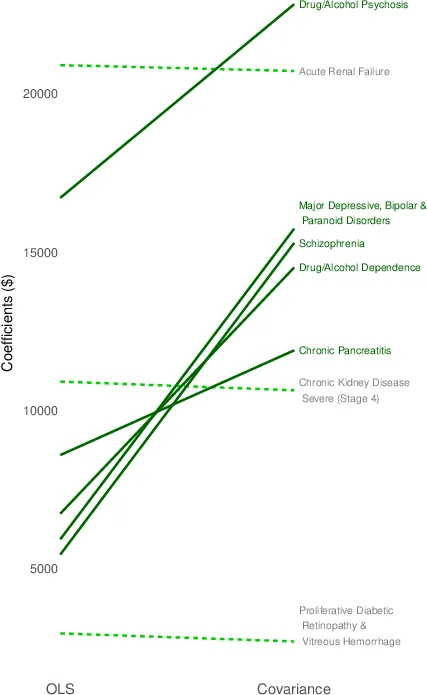

The paper addresses a critical fairness problem in health‑care risk adjustment: current OLS‑based formulas systematically underpredict spending for certain high‑cost groups, most notably individuals with mental health and substance use disorders (MHSUD). This underprediction leads to “undercompensation” of insurers, incentivizing them to design benefit packages that deter enrollment by these groups, thereby worsening access to care.

To remedy this, the authors first formalize several group‑fairness metrics that are relevant to risk adjustment: (1) Mean Residual Difference (the average prediction error gap between a protected group and its complement), (2) Net Compensation (the absolute average error for the protected group), (3) Predictive Ratio (predicted total spend divided by actual total spend for the group), and (4) a newly proposed Fair Covariance that measures the covariance between the protected‑group indicator and the residuals for continuous outcomes. They also retain the traditional R² as a global fit measure, acknowledging the policy need to balance fairness with overall predictive accuracy.

Building on these metrics, the paper proposes five regression approaches that embed fairness directly into the estimation objective:

- Average Constrained Regression (ACR) – imposes a hard constraint that the predicted average spending for the protected group equals its observed average, guaranteeing zero net compensation for that group.

- Weighted Average Constrained Regression (WACR) – relaxes ACR by allowing the group’s predicted average to be a convex combination of the unconstrained OLS prediction and the observed average, controlled by a weight α∈

Comments & Academic Discussion

Loading comments...

Leave a Comment