Matching in size: How market impact depends on the concentration of trading

We show that filling an order with a large number of distinct counterparts incurs additional market impact, as opposed to filling the order with a small number of counterparts. For best execution, therefore, it may be beneficial to opportunistically fill orders with as few counterparts as possible in Large-in-scale (LIS) venues. This article introduces the concept of concentrated trading, a situation that occurs when a large fraction of buying or selling in a given time period is done by one or a few traders, for example when executing a large order. Using London Stock Exchange data, we show that concentrated trading suffers price impact in addition to impact caused by (smart) order routing. However, when matched with similarly concentrated counterparts on the other side of the market, the impact is greatly reduced. This suggests that exposing an order on LIS venues is expected to result in execution performance improvement.

💡 Research Summary

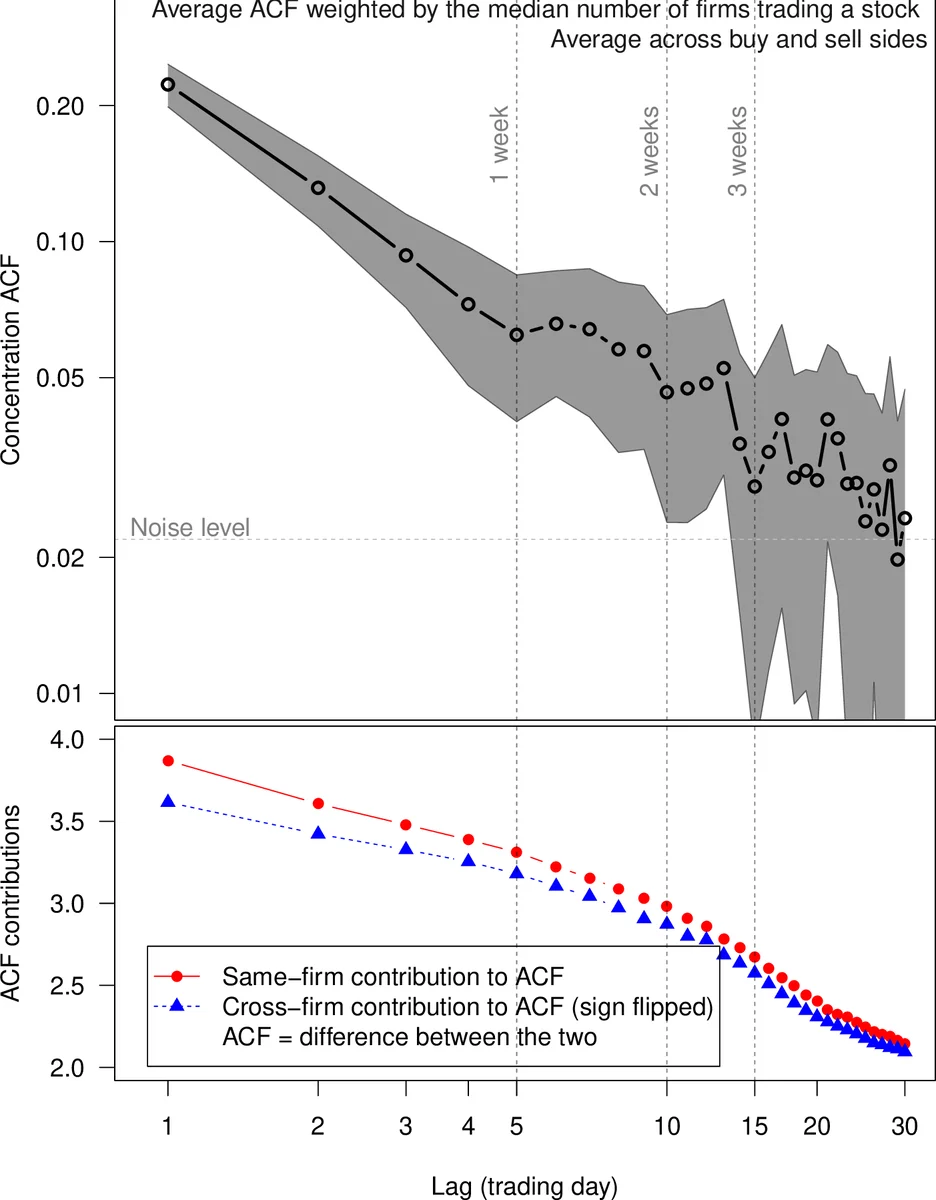

The paper introduces the notion of “concentration of trading” and empirically investigates how this concentration influences market price impact. Using a unique dataset from the London Stock Exchange (LSE) on‑book market covering May 2000 to December 2002, the authors reconstruct, for each trading day and each of 46 stocks, the exact participation of exchange member firms in every trade. This granularity allows them to compute, for both the buy‑side and the sell‑side, the distribution of volume across firms and to quantify its inequality with two classic measures: the Gini coefficient and a normalized entropy index. The difference between the buy‑side and sell‑side values (δG or δE) is defined as the “concentration imbalance”.

To isolate the pure effect of concentration from the well‑known order‑flow drivers, the authors also construct three order‑flow imbalance variables: (i) the imbalance in the number of aggressive trades (δM), (ii) the imbalance in aggressive notional volume (δV), and (iii) the imbalance in the number of active firms on each side (δN). All imbalances are calculated as (buy‑sell)/(buy+sell) and then standardized by each stock’s daily standard deviation, enabling a pooled regression across stocks.

The dependent variable is the daily price return, measured as the percentage difference between the volume‑weighted average price (VWAP) of the first 10 % and the last 10 % of trades in a day. This return is market‑adjusted by subtracting the FTSE 100 return and the stock’s own long‑run mean, leaving a normalized daily price movement.

A linear regression model is then estimated:

ΔPₜ = β₁·δEₜ + β₂·δMₜ + β₃·δVₜ + β₄·δNₜ + εₜ

The results (Table 1) show that the concentration imbalance coefficient β₁ is +24.9 basis points (p < 0.01). In other words, when buying is more concentrated than selling (few buyers absorb a large share of volume), the price tends to move upward, creating an additional impact beyond that explained by order‑flow variables. The aggressive‑notional imbalance β₃ is –81.8 bp (p < 0.01), confirming the classic finding that a surplus of aggressive buy orders pushes price up (or, equivalently, a surplus of aggressive sells pushes it down). The number‑of‑firms imbalance β₄ is –61.2 bp (p < 0.01), indicating that a side dominated by a small number of firms suffers a larger adverse price move. The aggressive‑trade‑count imbalance β₂ is statistically insignificant, suggesting that the notional amount, rather than the sheer count of trades, drives price pressure. The overall model explains about 33 % of the variance in daily price returns (R² = 0.33).

Beyond the regression, the authors conduct a focused test: they compare three stylised scenarios (illustrated in Figure 1) – (a) concentrated buying matched with dilute selling, (b) both sides concentrated, and (c) both sides dilute. Empirically, the “both‑sides‑concentrated” case exhibits markedly lower price impact than the other two, implying that matching a large order with an equally large counterpart mitigates the adverse effect of concentration.

The paper’s implications are clear for execution strategy. Under MiFID II, “Large‑in‑Scale” (LIS) venues have been created to enable traders to match large orders with as few counterparties as possible, ideally in a single clip. The findings support the intuition that minimizing the number of distinct counterparties reduces slippage, and that deliberately seeking a counterpart of comparable size (i.e., a concentrated opposite side) can further improve execution quality.

Limitations are acknowledged. Member‑firm identifiers are anonymised and reshuffled each month, preventing longitudinal tracking of individual firms’ behavior. The dataset is dated and limited to the LSE on‑book market, so the results may not directly transfer to modern, highly fragmented, high‑frequency markets. Moreover, the linear specification may not capture extreme market conditions where non‑linear dynamics dominate.

In summary, the study demonstrates that: (1) trading concentration independently raises market impact; (2) the impact is comparable in magnitude to traditional order‑flow effects; (3) matching concentrated orders with similarly concentrated counterparts substantially dampens the impact; and (4) execution algorithms should incorporate concentration metrics and, where possible, route orders through LIS or other mechanisms that limit the number of distinct counterparties. This adds a new dimension to optimal execution theory, complementing existing models that focus solely on order size, aggressiveness, and market impact functions.

Comments & Academic Discussion

Loading comments...

Leave a Comment