Robust Sequential Search

Notice: This research summary and analysis were automatically generated using AI technology. For absolute accuracy, please refer to the [Original Paper Viewer] below or the Original ArXiv Source.

💡 Research Summary

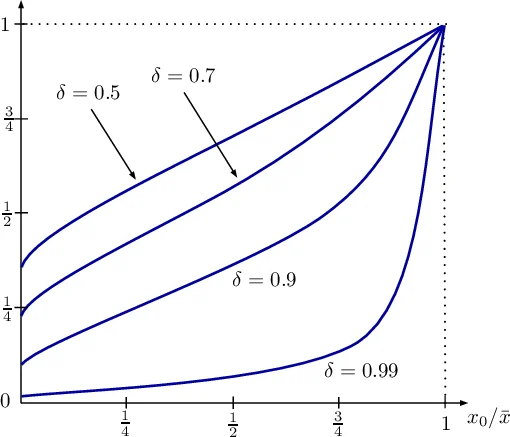

The paper tackles the classic sequential search problem in a setting where the decision‑maker does not possess a reliable prior over the distribution of future alternatives. Traditional Bayesian approaches assume a prior µ, update it by Bayes’ rule after each observation, and then choose a stopping rule that maximizes expected discounted payoff under the current posterior. Such solutions are fragile: they depend critically on the correctness of µ and on the decision‑maker’s ability to solve a complex dynamic programming problem.

To overcome these limitations, the authors introduce the notion of dynamic robustness. For any prior µ (which may be a mixed environment) and any history hₜ = (x₀,…,xₜ) of observed values, they compute the ratio

\

Comments & Academic Discussion

Loading comments...

Leave a Comment