COVID-19 response needs to broaden financial inclusion to curb the rise in poverty

The ongoing COVID-19 pandemic risks wiping out years of progress made in reducing global poverty. In this paper, we explore to what extent financial inclusion could help mitigate the increase in poverty using cross-country data across 78 low- and lower-middle-income countries. Unlike other recent cross-country studies, we show that financial inclusion is a key driver of poverty reduction in these countries. This effect is not direct, but indirect, by mitigating the detrimental effect that inequality has on poverty. Our findings are consistent across all the different measures of poverty used. Our forecasts suggest that the world’s population living on less than $1.90 per day could increase from 8% to 14% by 2021, pushing nearly 400 million people into poverty. However, urgent improvements in financial inclusion could substantially reduce the impact on poverty.

💡 Research Summary

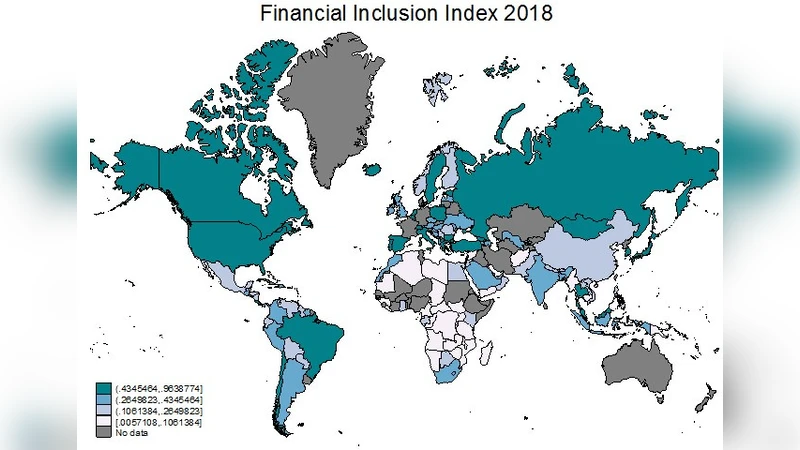

The paper investigates how expanding financial inclusion (FI) can mitigate the surge in global poverty triggered by the COVID‑19 pandemic, focusing on 78 low‑ and lower‑middle‑income countries. Using a panel dataset spanning 2010‑2020, the authors construct a composite FI index from three dimensions—bank account ownership, mobile‑payment usage, and access to micro‑credit. Poverty is measured with three complementary indicators: the $1.90‑a‑day headcount ratio, the absolute number of people below the poverty line, and the poverty gap. Inequality is captured by the Gini coefficient.

The empirical strategy combines stepwise regressions with structural equation modeling (SEM) to test a mediation hypothesis: FI reduces poverty indirectly by dampening inequality. Direct regressions find no statistically significant effect of FI on poverty, but the SEM reveals a robust indirect pathway. A one‑percentage‑point increase in the FI index lowers the Gini coefficient by roughly 0.15 percentage points, which in turn reduces the poverty headcount by about 0.07 percentage points. These estimates hold across alternative specifications, including fixed‑effects OLS, Tobit, and two‑stage least squares (2SLS) models that employ lagged mobile‑network coverage and reductions in international remittance costs as instrumental variables to address endogeneity.

Scenario analysis projects the pandemic’s impact on extreme poverty. In a baseline “no‑FI‑improvement” case, the share of the world population living on less than $1.90 per day is forecast to rise from 8 % in 2020 to 14 % by 2021, adding roughly 400 million people to extreme poverty. Introducing modest FI gains—raising the FI index by 5 percentage points—cuts the projected increase by about half, limiting the additional poor to roughly 200 million. Larger improvements (10–15 percentage‑point gains) could further shrink the excess poverty to under 100 million people.

The authors argue that these findings have clear policy implications. First, rapid expansion of digital financial infrastructure (mobile banking, electronic payments) is essential to broaden access. Second, scaling up micro‑credit and micro‑insurance can strengthen households’ risk‑management capacity. Third, financial literacy programs and consumer‑protection frameworks must accompany service expansion to ensure that inclusion translates into real income security. Fourth, multilateral development banks and international agencies should prioritize financing FI projects and provide technical assistance tailored to country‑specific contexts. Finally, the paper calls for future research that leverages household‑level longitudinal data to refine causal estimates and to assess the resilience of FI‑driven poverty reduction under post‑pandemic economic shocks.