Optimal Transport and Risk Aversion in Kyle's Model of Informed Trading

💡 Research Summary

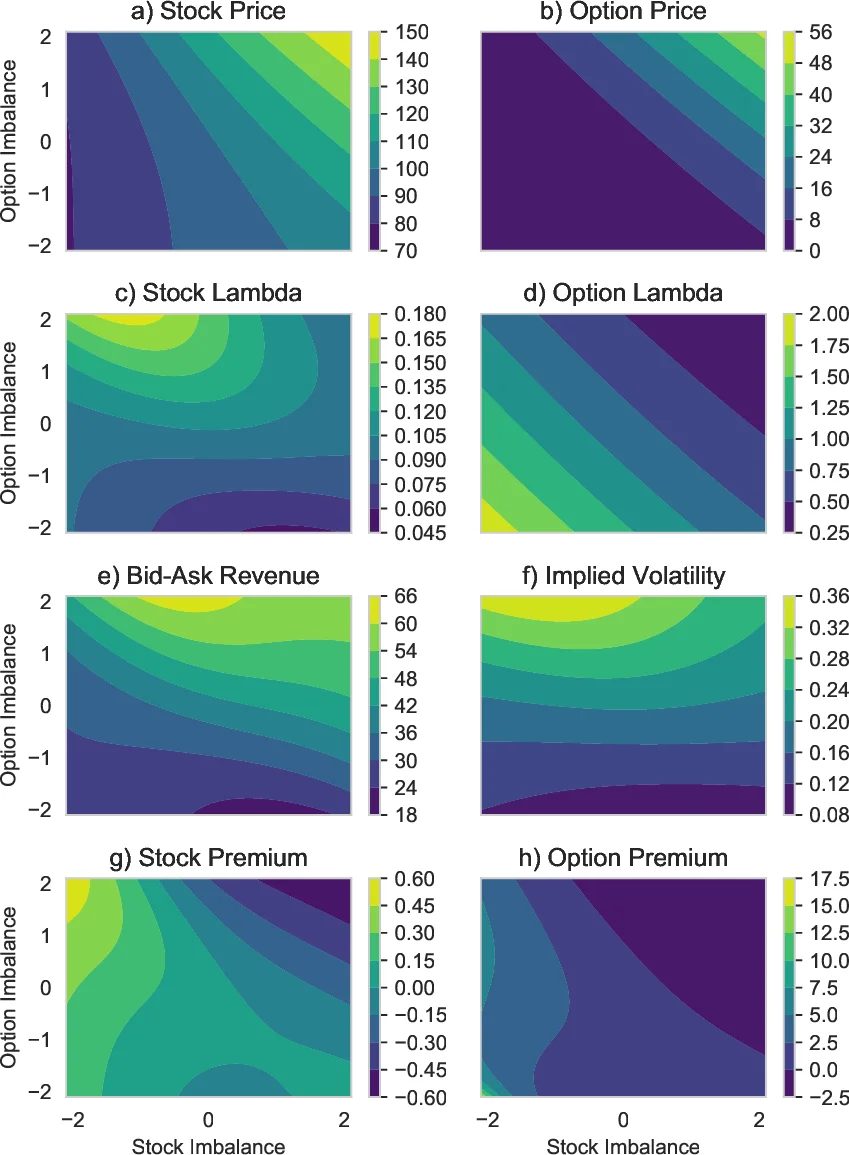

The paper establishes a novel bridge between optimal transport theory and the continuous‑time Kyle model of informed trading, thereby extending the classic framework in three important directions. First, by invoking a generalized Brenier theorem, the authors construct a convex potential Γ whose gradient ∇Γ transports the distribution of the noise‑trader’s cumulative order Z_T (distribution G) to the distribution of the asset value ˜v (distribution F). This construction works for any finite‑covariance distribution, including discrete and lower‑dimensional cases, and yields a Monge‑Kantorovich dual representation of the informed trader’s expected profit: the maximal conditional profit equals the convex conjugate Γ* (˜v). The pricing rule is then given by the heat‑kernel convolution H(t,y)=∫∇Γ(z)k(t,y,z)dz, and the price dynamics satisfy dP_t=Λ_t dY_t with Λ_t=∇²Γ(t,Y_t), a symmetric positive‑semidefinite matrix that generalizes Kyle’s λ.

Second, the model incorporates risk‑averse market makers by treating a representative dealer’s marginal utility as a stochastic discount factor evaluated at aggregate dealer wealth. This modification enlarges λ: higher risk aversion leads to larger λ in the positive‑definite ordering, implying lower market liquidity. Moreover, dealer inventories become mean‑reverting rather than a random walk, and the inventory dynamics generate risk premia that feed back into price changes. Consequently, the model predicts excess volatility (quadratic variation exceeding long‑run variance) and short‑term return reversals, phenomena observed in empirical studies of inventory‑risk models.

Third, the authors extend the framework to a multi‑asset setting that includes both an underlying stock and a European call option. When market makers are risk‑averse, the option’s implied volatility influences the dealer’s inventory hedge (e.g., long the stock when short a call), and the resulting risk premia cause higher implied volatilities to predict higher future stock returns. This prediction disappears under risk‑neutral makers, where expected returns equal the risk‑free rate. The paper thus reconciles adverse‑selection and inventory‑risk theories of liquidity, quantifies each’s contribution to λ, and provides a unified explanation for observed market phenomena such as short‑term reversals and the predictive power of option‑implied volatility. All results are derived analytically, and proofs are relegated to the appendix.

Comments & Academic Discussion

Loading comments...

Leave a Comment