Wealth distribution under the spread of infectious diseases

We develop a mathematical framework to study the economic impact of infectious diseases by integrating epidemiological dynamics with a kinetic model of wealth exchange. The multi-agent description leads to study the evolution over time of a system of kinetic equations for the wealth densities of susceptible, infectious and recovered individuals, whose proportions are driven by a classical compartmental model in epidemiology. Explicit calculations show that the spread of the disease seriously affects the distribution of wealth, which, unlike the situation in the absence of epidemics, can converge towards a stationary state with a bimodal form. Furthermore, simulations confirm the ability of the model to describe different phenomena characteristics of economic trends in situations compromised by the rapid spread of an epidemic, such as the unequal impact on the various wealth classes and the risk of a shrinking middle class.

💡 Research Summary

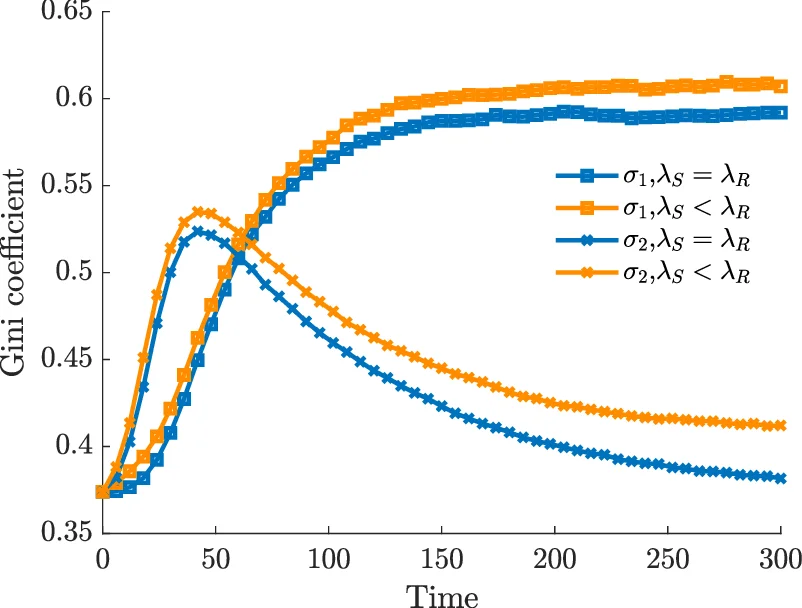

The paper presents a novel mathematical framework that couples a classic SIR epidemiological model with a kinetic description of wealth exchange among agents, aiming to quantify how the spread of an infectious disease reshapes the distribution of wealth in a society. The authors consider a population divided into three health states—susceptible (S), infected (I), and recovered (R)—and assume that each individual is fully described by a non‑negative wealth variable w. The corresponding probability densities f_S(w,t), f_I(w,t) and f_R(w,t) evolve in time under two concurrent mechanisms: (i) the usual SIR transitions driven by a contact rate β(w,w*) that may depend on the wealth of the interacting agents, and a recovery rate γ(w); (ii) binary wealth‑exchange interactions modelled after the CPT (Conservative‑Preserving‑Trading) scheme introduced in earlier kinetic‑theory works.

In the kinetic part, agents from any pair of health classes engage in a trade described by w′ = (1−λ_J) w + λ_K w* + η_{J K} w, w*′ = (1−λ_K) w* + λ_J w + \tilde η_{J K} w*, where λ_J∈(0,1) is the saving propensity of class J (different for S, I, R) and η_{J K}, \tilde η_{J K} are zero‑mean random variables with a common, time‑dependent variance σ²(t). The variance is assumed to increase with the fraction of infected individuals, σ²(t)=σ₀²(1+α I(t)), thereby capturing the heightened market volatility observed during real epidemics such as COVID‑19.

Combining the epidemiological fluxes with the Boltzmann‑type collision operator Q(f_J,f_K) yields a system of three nonlinear integro‑differential equations for the densities f_S, f_I, f_R. The authors perform a formal asymptotic expansion in the quasi‑elastic limit (small λ_J, small σ) and obtain a coupled system of Fokker‑Planck equations. Each equation contains a diffusion term proportional to ∂²/∂w²

Comments & Academic Discussion

Loading comments...

Leave a Comment