Optimal Storage Arbitrage under Net Metering using Linear Programming

We formulate the optimal energy arbitrage problem for a piecewise linear cost function for energy storage devices using linear programming (LP). The LP formulation is based on the equivalent minimization of the epigraph. This formulation considers ra…

Authors: Md Umar Hashmi, Arpan Mukhopadhyay, Ana Buv{s}ic

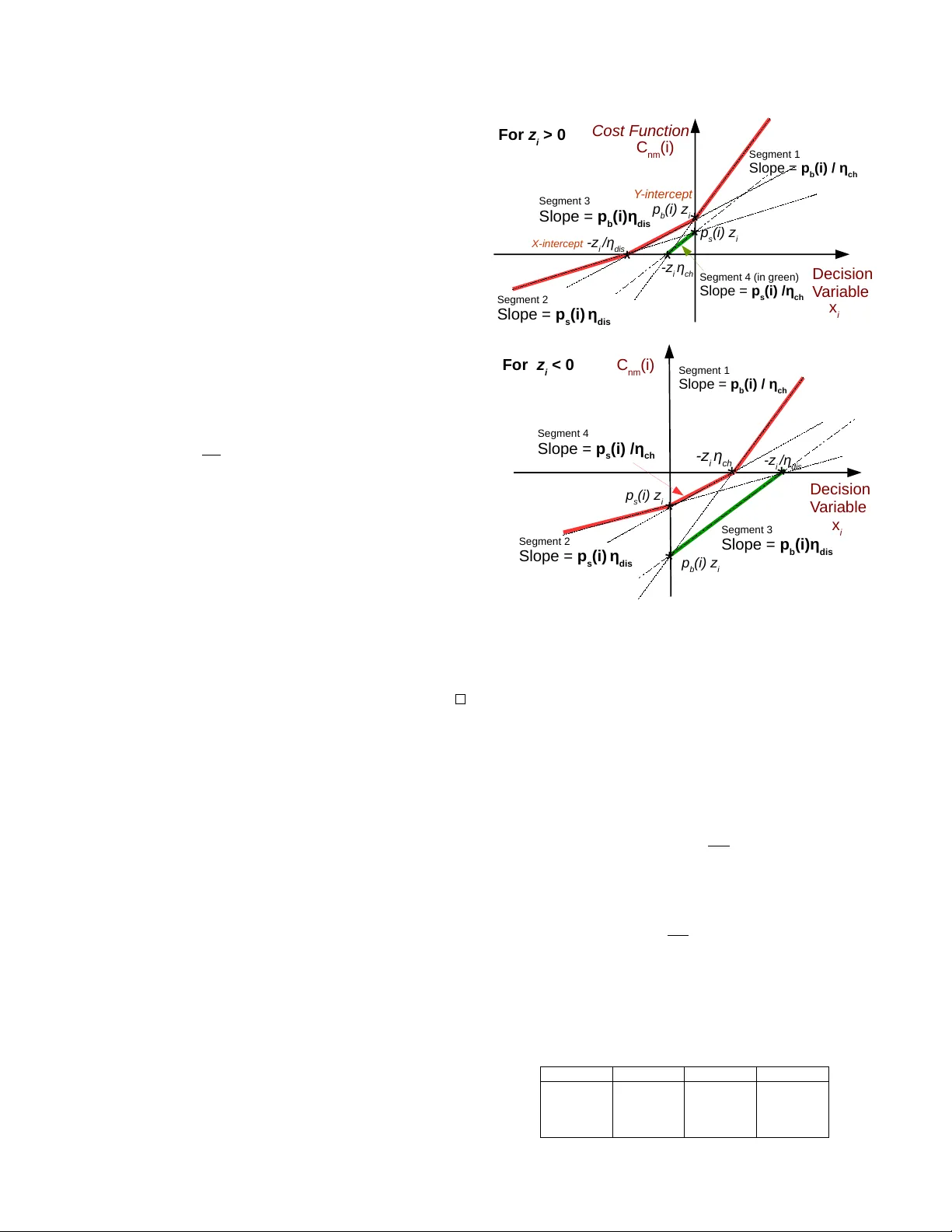

Optimal Storage Arbitrage under Net Metering using Linear Programming Md Umar Hashmi ∗ , Arpan Mukhopadhyay † , Ana Bu ˇ si ´ c ∗ , Jocelyne Elias ‡ , and Diego Kiedanski § ∗ INRIA and the Computer Science Dept. of Ecole Normale Sup ´ erieure, CNRS, PSL Research Univ ersity , P aris, France † the Department of Computer Science, Univ ersity of W arwick, the UK ‡ Laboratoire d’Informatique P Aris Descartes (LIP ADE), Uni versit ´ e Paris Descartes, P aris, France § T ´ el ´ ecom Paristech, 23 A venue d’Italie, P aris, France Abstract —W e formulate the optimal energy arbitrage problem for a piecewise linear cost function for energy storage devices using linear programming (LP). The LP formulation is based on the equiv alent minimization of the epigraph. This f ormula- tion considers ramping and capacity constraints, charging and discharging efficiency losses of the storage, inelastic consumer load and local renewable generation in presence of net-metering which facilitates selling of energy to the grid and incentivizes consumers to install r enewable generation and energy storage. W e consider the case where the consumer loads, electricity prices, and renewable generations at different instances are uncertain. These uncertain quantities are predicted using an A uto-Regressive Moving A verage (ARMA) model and used in a model predictive control (MPC) framework to obtain the arbitrage decision at each instance. In numerical results we pr esent the sensitivity analysis of storage performing arbitrage with varying ramping batteries and different ratio of selling and buying price of electricity . Index T erms —Energy arbitrage, Battery , Linear programming, Net-metering, Model Predictive Control I . I N T RO D U C T I O N Energy storage devices pro vide flexibility to alter the con- sumption behavior of an electricity consumer . Storage owners at the consumer side could participate in demand response, ener gy arbitrage, peak demand shaving, power backup to name a fe w [1], [2]. These features of storage devices will be more lucrati ve for storage o wners with the growth of intermittent generation sources which increase volatility on the generation side in power network [3]. Furthermore, batteries are becoming more afford- able making se veral applications of storage de vices financially viable. Storage devices can perform arbitrage of energy with time varying consumer load, distributed generation production and electricity price. Furthermore, utilities promote inclusion of distributed generation and storage deployment by introducing net-metering. Net energy metering (NEM) or net-metering refers to the rate consumers receive for feeding power back to the grid. Most NEM policies indicate that consumers recei ve a rate at best equal to the buying price of electricity [4]. Authors in [5] consider storage operation under equal buy and sell price case. This framework is generalized in [6], covering cases where the ratio of buy and sell price could arbitrarily vary between 0 and 1. For equal buying and selling price, the storage control becomes independent of inelastic load and renew able generation of the consumer [5], [7]. The cost function considered in this work includes inelastic load, renew able generation and storage charging and discharging efficienc y , and ramping and capacity constraints. W e first show that the cost function, based on the selection of the optimization variable, is con ve x and piecewise linear . Then, we formulate the optimal arbitrage problem for an electricity consumer with renewable generation adopting NEM by using Linear Programming (LP). Authors in [8] provide a summary of storage control method- ologies used in power distribution networks among which LP based formulations can be solved efficiently using commercially av ailable solvers. Therefore, these algorithms can be used to efficiently solve the arbitrage problem for the duration of a day divided into smaller time steps ranging from 5 minutes to an hour . A day is the typical time horizon over which arbitrage is performed [9], [10]. Authors in [11] formulate the optimal arbitrage problem for a strictly con ve x cost function and observe that for a piecewise linear con ve x cost function, as in [5], LP-based tools can be applied. LP techniques for energy storage arbitrage ha ve been used in sev eral prior works: [12], [13], [14], [15], [16], [17], [18]. Authors in [16], [13], [18] consider storage operation in presence of time-varying electricity price. Howe ver , in these formulations no renewable energy source or consumer load is assumed to be present. Authors in [14], [15] consider optimal scheduling of storage battery for maximizing energy arbitrage rev enue in presence of distributed ener gy resources and variable electricity price. Formulations presented in [17], [12] consider storage performing arbitrage in a residential setting with inelastic load and local generation. Most common LP formulations for energy arbitrage such as in [12], [18], [15], [13] consider separation of charging and discharging components of storage ramping variable. In these formulations, they do not include constraint enforcing only one of the charging or the discharging component to be acti ve at any particular time as the inclusion of such a constraint makes these formulations nonlinear . In the absence of such a constraint charging and discharging component can compensate each other which can lead to suboptimal solution. Authors in [14], [16] do not consider energy storage charging and dischar ging ef ficiencies in the cost minimization, making it straightforward to apply LP . Authors in [17] consider a special case of optimization with zero-sum aggreg ate storage po wer output. For such a case LP tools could be used, howe ver , generalizing the formulations needs to be explored further . The key contributions of this paper are as follo ws: • LP formulation for storag e contr ol : W e formulate the LP opti- 978-1-5386-8099-5/19/$31.00 c 2019 IEEE mization problem for piecewise linear con ve x cost function, for storage with ef ficiency losses, ramping and capacity constraints and a consumer with inelastic load and renew able generation. The buying and selling price of electricity are varying over time. The selling price is assumed to be at best equal to buying price for each time instant, this assumption is in sync with most net- metering policies worldwide. Based on the conv ex and piece wise linear structure of the cost function we apply an epigraph based minimization described in [19] to the arbitrage problem. The reduction of this formulation for (a) lossless battery with equal buying and selling price of electricity and (b) lossy battery with selling price less than or equal to buying price, is trivial and not included in this paper . • Real-time implementation: W e implement an auto-regressiv e based forecast model along with model predictiv e control and numerically analyze their ef fect on arbitrage gains using real data from a household in Madeira in Portugal and electricity price from California ISO [20]. The effect of parameter uncertainty on arbitrage gains is more pronounced for cases where selling price is comparable to buying price. • Sensitivity of ratio of selling and buying price : W e numerically analyze the effect of the ratio of buying and selling price of electricity on the value of storage with inelastic load and renew able generation. W e observe that the v alue of storage performing arbitrage significantly increases in the presence of load and renew able generation with the increasing dif ference of selling and buying price of electricity , compared to only storage performing arbitrage. Inclusion of storage in the presence of load and renewable generation can be profitable even for cases where the selling price is zero or small compared to buying price. For the same case, only storage performing arbitrage would not be profitable. The paper is organized as follows. Section II provides the description of the system. Section III presents the LP formulation of storage performing arbitrage with inelastic load, renewable generation and net-metering based compensation. Section IV presents an online algorithm using the proposed optimal arbi- trage algorithm along with auto-regressiv e forecasting in the MPC framework. Section V discusses numerical results. Finally , Section VI concludes the paper . I I . S Y S T E M D E S C R I P T I O N W e consider a consumer of electricity over a fixed period of time. The consumer is assumed to be equipped with a rooftop solar photov oltaic and a battery to store excess generation. It is also connected to the electricity grid from where it can b uy or to which it can sell energy . The total duration, T , of operation is divided into N steps index ed by { 1 , ..., N } . The duration of step i ∈ { 1 , ..., N } is denoted as h i . Hence, T = P N i =1 h i . The price of electricity , p elec ( i ) , equals the buying price, p b ( i ) , if the consumption is positiv e; otherwise p elec ( i ) equals the selling price, p s ( i ) ; denoted as p elec ( i ) = p b ( i ) , if consumption ≥ 0 , p s ( i ) , otherwise, (1) Note p elec is ex-ante and the consumer is a price taker . The ratio of selling and buying price at time i is denoted as κ i = p s ( i ) /p b ( i ) . (2) The end user inelastic consumption in time step i is denoted as d i and renew able generation as r i . Net energy consumption without storage is denoted as z i = d i − r i ∈ R . Fig. 1 shows the block diagram of the system, i.e., an electricity consumer with renew able generation and battery . The efficienc y of char ging and discharging of the battery are denoted by η ch , η dis ∈ (0 , 1] , respectiv ely . W e denote the change in the energy lev el of the battery at i th instant by x i = h i δ i , where δ i denotes the storage ramp rate at i th instant such that δ i ∈ [ δ min , δ max ] ∀ i and δ min ≤ 0 , δ max ≥ 0 are the minimum and the maximum ramp rates (kW); δ i > 0 implies charging and δ i < 0 implies discharging. Energy consumed by the storage in the i th instant is giv en by s i = f ( x i ) = 1 η ch [ x i ] + − η dis [ x i ] − , (3) where x i must lie in the range from X i min = δ min h i to X i max = δ max h i . Note [ x i ] + = max(0 , x i ) and [ x i ] − = max(0 , − x i ) . Alternativ ely , we can write x i = η ch [ s i ] + − 1 η dis [ s i ] − . The limits on s i are given as s i ∈ [ S i min , S i max ] , where S i min = η dis δ min h i and S i max = δ max h i η ch . Let b i denote the energy stored in the battery at the i th step. The battery capacity is defined as b i = b i − 1 + x i , b i ∈ [ b min , b max ] , ∀ i, (4) where b min , b max are the minimum and the maximum battery capacity . The total energy consumed between time step i and i + 1 is giv en as L i = z i + s i . E n e rg y Mete r L i End User Consumpti on d i Storage x i Renew abl e G enerati on r i End - Us er Pow er G rid + s i Fig. 1: Behind-the-meter electricity consumer with inelastic consump- tion, renewable generation and ener gy storage. The battery operational life is often quantified using cycle and calendar life which decides the cycles a battery should perform ov er a time period. Friction coef ficient, denoted as η fric ∈ [0 , 1] , and introduced in [21] assists in reducing the operational life of the battery such that low returning transactions of charging and discharging are eliminated, thus increasing the operational life of the battery . In subsequent work, authors in [22], [23] propose a framew ork to tune the value of friction coef ficient for increasing operational life of battery by eliminating low returning transactions. A. Arbitrag e under Net-Metering The optimal arbitrage problem is defined as the minimization of the cost of total energy consumption subject to the battery constraints. It is giv en as follows: ( P NEM ) min N X i =1 C i nm ( x i ) , subject to, b min − b 0 ≤ i X j =1 x j ≤ b max − b 0 , ∀ i ∈ { 1 , .., N } , x i ∈ X i min , X i max ∀ i ∈ { 1 , .., N } , where C i nm ( x i ) denotes the energy consumption cost function at instant i and is giv en by C i nm ( x i ) = [ z i + f ( x i )] + p b ( i ) − [ z i + f ( x i )] − p s ( i ) . (5) Now we will show that the optimal arbitrage problem is con ve x in x = ( x i , i = 1 : N ) . For this con ve xity to hold we require p b ( i ) ≥ p s ( i ) for all i = 1 : N , i.e., κ i ∈ [0 , 1] . The proposed framework is applicable for the case where selling price of electricity for the end user is lo wer than the b uying price. This assumption is quite realistic as this is generally the case in most practical net metering policies [4]. Theorem II.1. If p b ( i ) ≥ p s ( i ) for all i = 1 : N , then pr oblem ( P NEM ) is con vex in x . Pr oof. Let ψ ( t ) = a [ t ] + − b [ t ] − with a ≥ b ≥ 0 . Using t = [ t ] + − [ t ] − we have ψ ( t ) = ( a − b )[ t ] + + bt . Since both [ t ] + and t are con ve x in t and a − b, b ≥ 0 we hav e that ψ is con vex since it is the positiv e sum of two con ve x functions. Now let f ( x ) = 1 η ch [ x ] + − η dis [ x ] − and G i ( s ) = [ z i + s ] + p b ( i ) − [ z i + s ] − p s ( i ) . Then by the above reasoning we have that for p b ( i ) ≥ p s ( i ) ≥ 0 and η ch , η dis ∈ (0 , 1] , G i is con ve x in s and f is con v ex in x . Also, note that G i is non-decreasing in s . Hence, for λ ∈ [0 , 1] we hav e G i f ( λx + (1 − λ ) y ) ≤ G i λf ( x ) + (1 − λ ) f ( y ) (6) ≤ λG i ( f ( x )) + (1 − λ ) G i ( f ( y )) (7) In the above, the first inequality follo ws from the con ve xity of f and non-decreasing nature of G i and the second inequality follows from con vexity of G i . Therefore, we have that G i ◦ f = G i ( f ()) is a con ve x function in x . This shows that the objective function of ( P NEM ) is conv ex in x since C i nm = G i ◦ f . Since the constraints are linear in x thus problem ( P NEM ) is con ve x. I I I . O P T I M A L A R B I T R A G E W I T H L I N E A R P R O G R A M M I N G The optimal arbitrage problem, ( P NEM ), can be solved using linear programming as the cost function is (i) con vex and (ii) piecewise linear , and (iii) the associated ramping and capacity constraints are linear . In this section, we provide an LP formu- lation for the optimal arbitrage of the storage de vice under net- metering and consumer inelastic load and renewable generation, lev eraging the epigraph based minimization presented in [19]. A summary of the epigraph based formulation for a piecewise linear con ve x cost function is presented in Appendix A. The optimal arbitrage formulation for storage under net-metering and consumer inelastic load and renew able generation using the epigraph formulation is presented in this section. Fig. 2 shows the optimal arbitrage cost function depending on the net-load without storage output, i.e. for z i ≥ 0 and z i < 0 . Notice that the cost function C nm ( i ) is formed of 4 unique segments whose slopes, x-intercept and y-intercept are shown in Fig. 2 and listed in T able I. Fig. 2 shows that the inactive segment of the cost function denoted in green lies below the cost function denoted in red. Due to the con vexity property of the cost function, it can be denoted as C nm ( i ) = m ax Segment 1, Se gment 2 , Segment 3, Se gment 4 . (8) Fo r z i > 0 D ecisi on V a ria ble C ost Fun ct i on Y - i n t er c ept p b ( i ) z i Se g m e n t 1 S l o pe = p b ( i ) / η c h Se g m e n t 3 Sl ope = p b (i ) η d i s X-i n t e rce p t - z i / η d i s Se g m e n t 2 Sl ope = p s (i ) η d i s C n m (i) x i p s ( i ) z i - z i η c h * * * * Se g m e n t 4 ( i n g r e e n ) S l o pe = p s ( i ) / η c h D ecisi on V a ria ble C n m (i) x i Fo r z i < 0 -z i η ch Se g m e n t 4 Sl ope = p s ( i) / η c h S e g me n t 1 S l ope = p b ( i ) / η c h Se g me n t 2 S lop e = p s (i) η d i s p s ( i ) z i p b ( i ) z i - z i / η d i s Se g m e n t 3 Sl ope = p b (i ) η d i s * * * * Fig. 2: The cost function segment wise for positive and neg ative net load z [6]. The decision variable is storage change in charge lev el, x i , and cost function, C nm ( i ) is formed with 4 unique line se gments. The epigraph based LP formulation is possible as irrespective of the sign of the load ( z ) the cost function can be represented as the maximum of the segments, shown in Eq.8. Using the epigraph equi valent formulation for piecewise linear con vex cost function we formulate the optimal arbitrage problem using linear programming, denoted as P LP ( P LP ) min { t 1 + t 2 + ... + t N } , subject to, (a) Segment 1: p i b η ch x i + z i p i b ≤ t i , ∀ i (b) Segment 2: p i s η dis x i + z i p i s ≤ t i , ∀ i (c) Segment 3: p i b η dis x i + z i p i b ≤ t i , ∀ i (d) Segment 4: p i s η ch x i + z i p i s ≤ t i , ∀ i (e) Ramp constraint: x i ∈ [ X i min , X i max ] , ∀ i (f) Capacity constraint: X x i ∈ [ b min − b 0 , b max − b 0 ] , ∀ i. T ABLE I: Cost function for storage with load under NEM Segment Slope x-intercept y-intercept Segment 1 p b ( i ) /η ch − z i η ch z i p b ( i ) Segment 2 p s ( i ) η dis − z i /η dis z i p s ( i ) Segment 3 p b ( i ) η dis − z i /η dis z i p b ( i ) Segment 4 p s ( i ) /η ch − z i η ch z i p s ( i ) The cost function for only lossy storage operation under NEM has tw o-piecewise linear segments and it is linear for equal buying and selling price of electricity with lossless battery . Authors in [14], [16] present this case in their LP formulation. This case can be obtained by simplifying the more general case depicted as P LP for cost function presented in Fig. 2. The LP based optimal arbitrage code de- scribed in this paper are publicly av ailable at github.com/umar-hashmi/linearprogrammingarbitrage . I V . R E A L - T I M E I M P L E M E N TA T I O N The pre vious section discussed optimal storage arbitrage under complete kno wledge of future net loads and prices. In this section, we consider the setting where future values may be unknown. T o that end, we first develop a forecast model for net load without storage (which includes inelastic consumer load and consumer distrib uted generation) and electricity price for future times, where the forecast is updated after each time step. Then, we develop the forecasting model for net load with solar gen- eration using AutoRegressiv e Moving A v erage (ARMA) model and electricity price forecast using AutoRegressiv e Integrated Moving A verage (ARIMA). The forecast models based on ARMA and ARIMA model dev eloped in [24] are used in this work. The forecast val- ues are fed to a Model Predictiv e Control (MPC) scheme to identity the optimal modes of operation of storage for the current time-instance. These steps (forecast and MPC) are repeated sequentially and highlighted in online Algorithm 1: ForecastMPClinearProgram . Algorithm 1 ForecastMPClinearProgram Storage Parameters : η ch , η dis , δ max , δ min , b max , b min , b 0 . Inputs : h, N , T , i = 0 , Rolling horizon optimization time period N opt , Historical inelastic load, renewable generation and electricity price data. 1: Use historical data to tune ARMA and ARIMA models, 2: while i < N do 3: Increment i = i + 1 , 4: Real-time electricity price v alue p elec ( i ) and load z i , 5: Forecast ˆ z from time step i + 1 to i + N opt using ARMA, 6: Forecast ˆ p b and ˆ p s from time i + 1 to i + N opt using ARIMA, 7: Calculate ˆ κ as the ratio of ˆ p s and ˆ p b , 8: Build LP matrices for time step i to N , 9: Solve the Linear Optimization problem for forecast vectors, 10: Calculate b i ∗ = b i − 1 + ˆ x ∗ (1) , 11: Update b 0 = b i ∗ , the initial capacity of battery is updated. 12: Return b i ∗ , x i ∗ . 13: end while V . N U M E R I C A L R E S U LT S For the numerical ev aluation, we use battery parameters listed in T able II. The performance indices used for ev aluating simulations are: • Arbitrage Gains: denotes the gains (in absence of load and renew able) or reduction in the cost of consumption (made in presence of load and renew able) due to storage performing energy arbitrage under time-v arying electricity prices, • Cycles of operation : In our prior work [22] we develop a mechanism to measure the number of c ycles of operation based on depth-of-dischar ge (DoD) of energy storage operational cycles. Equi v alent cycles of 100% DoD are identified. This index provides information about ho w much the battery is operated. W e use xC-yC notation to represent the relationship between ramp rate and battery capacity . xC-yC implies battery takes 1/x hours to charge and 1/y hours to discharge completely . W e perform sensitivity analysis with (a) four battery models with the different ramping capability listed in T able II and (b) 5 lev els of the ratio of selling price and buying price of electricity , i.e., κ ∈ { 1 , 0 . 75 , 0 . 5 , 0 . 25 , 0 } . The optimization problem, P LP , is T ABLE II: Battery P arameters b min , b max , b 0 200Wh, 2000 Wh, 1000 Wh η ch = η dis 0.95 δ max = − δ min 500 W for 0.25C-0.25C, (4 battery model) 1000 W for 0.5C-0.5C 2000 W for 1C-1C, 4000 W for 2C-2C solved using linprog in MA TLAB 1 . linprog uses dual- simplex [25] (default) algorithm. A. Deterministic Simulations The price data for our simulations in this subsection is taken from NYISO [26]. The load and generation data is taken from data collected at Madeira, Portugal. Fig. 3 shows the electric- ity price and energy consumption (includes inelastic load and rooftop solar generation) data used for deterministic simulations. T able III and T able IV lists the energy storage arbitrage without 0 4 8 12 16 20 24 4 6 8 10 12 $ cents/ kWh Price of electricity 0 4 8 12 16 20 24 Hour Index -200 0 200 400 600 800 1000 Watt-hour Energy Consumption Fig. 3: Electricity price and consumer net load data used for determin- istic simulations. and with energy consumption load for the electricity price data shown in Fig. 3. The observations are: • The value of storage in presence of load and rene wable increases as κ decreases. Note that for κ = 0 , the only storage operation provides zero gain (see T able III), howe ver , for the same buying and selling le vels, the consumer would make significant gains when operated with inelastic load and renew able generation (see T able IV), 1 https://www .mathworks.com/help/optim/ug/linprog.html • The cycles of operation for faster ramping batteries are higher compared to slower ramping batteries. This implies that faster ramping batteries should be compared in terms of gains per c ycle with slower ramping batteries. Observing only gains could be misleading. • As κ decreases, the c ycles of operation decrease, thus the ef fect on storage operation in the cases presented is similar to η fric in reducing cycles of operation. • Note that for κ = 1 , the arbitrage gains with and without load are the same. This observation is in sync with claims made in [5]. Authors in [5] observe that storage operation becomes independent of load and renewable variation for equal buying and selling case. T ABLE III: Performance indices for only storage κ 2C-2C 1C-1C 0.5C-0.5C 0.25C-0.25C Arbitrage gains in $ cents for 1 day 1 44.445 33.760 25.636 17.536 0.75 18.842 17.668 14.077 9.921 0.5 7.682 7.088 6.253 5.219 0.25 2.513 2.502 2.483 2.422 0 0 0 0 0 Cycles of operation for 1 day 1 6.586 3.856 2.237 1.620 0.75 2.401 1.742 1.484 0.795 0.5 1.539 1.099 0.714 0.386 0.25 0.182 0.171 0.164 0.160 0 0 0 0 0 T ABLE IV: Performance indices for storage + load κ 2C-2C 1C-1C 0.5C-0.5C 0.25C-0.25C Arbitrage gains in $ cents for 1 day 1 44.445 33.760 25.636 17.536 0.75 37.848 33.023 26.469 18.337 0.5 39.045 34.105 27.696 19.344 0.25 40.272 35.332 28.923 20.351 0 41.500 36.560 30.150 21.358 Cycles of operation for 1 day 1 6.586 3.835 2.263 1.620 0.75 5.986 4.039 2.338 1.652 0.5 5.986 4.033 2.364 1.660 0.25 5.986 4.033 2.364 1.660 0 5.986 4.033 2.364 1.660 Fig. 4 and Fig. 5 show the arbitrage gains, gains per cycle and cycles of operation with v arying κ for storage performing arbi- trage without and with inelastic load and rene wable generation. The gains per cycle are nearly flat with varying κ . Slow ramping batteries, 0.25C-0.25C and 0.5C-0.5C, have significantly higher gains per cycle compared to faster ramping batteries, 1C-1C and 2C-2C. B. Results with Uncertainty The forecast model is generated for load with solar generation and for electricity price. The ARMA based forecast uses 9 weeks of data (starting from 29th May , 2019) for training and generates forecast for the next week. ForecastMPClinearProgram is implemented in receding horizon. The electricity price data used for this numerical e xperiment is tak en from CAISO [27] for the 0 0.2 0.4 0.6 0.8 1 = Selling price / Buying Price 0 2 4 6 No. of cycles Cycles of operation Battery 2C-2C Battery 1C-1C Battery 0.5C-0.5C Battery 0.25C-0.25C 0 0.2 0.4 0.6 0.8 1 0 10 20 30 40 $ cents Arbitrage gains in $ cents Battery 2C-2C Battery 1C-1C Battery 0.5C-0.5C Battery 0.25C-0.25C 0 0.2 0.4 0.6 0.8 1 0 5 10 15 20 cents/cycle $ cents per cycle Fig. 4: Performance indices for only storage performing arbitrage with varying κ for 1 day . 0 0.2 0.4 0.6 0.8 1 20 30 40 $ cents Arbitrage gains in $ cents 2C-2C 1C-1C 0.5C-0.5C 0.25C-0.25C 0 0.2 0.4 0.6 0.8 1 6 8 10 12 cents/cycle $ cents per cycle 0 0.2 0.4 0.6 0.8 1 = Selling price / Buying Price 2 4 6 No. of cycles Cycles of operation Fig. 5: Storage along with inelastic load and renew able generation with varying κ for 1 day . same days of load data. T o compare the effect of forecasting net load and electricity prices with perfect information, we present av erage arbitrage gains and cycles of operation starting from 1st June 2019. Rolling horizon time-period of optimization, N opt , is selected as 1 day . This implies at 13:00 h today , the storage control decisions are based on parameter variation forecasts till 13:00 h tomorrow . The deterministic results for without and with load are pre- sented in T able V and T able VI. Compare the deterministic results with stochastic results presented in T able VII and T a- ble VIII. The primary numerical observations are: T ABLE V: Deterministic arbitrage gains for only storage κ 2C-2C 1C-1C 0.5C-0.5C 0.25C-0.25C Arbitrage gains in $ for 1 week 1 9.411 7.059 4.784 3.065 0.75 5.729 4.491 3.168 2.082 0.5 3.166 2.550 1.833 1.217 0.25 1.124 0.941 0.688 0.456 0 0 0 0 0 Cycles of operation for 1 week 1 58.729 37.257 21.324 12.107 0.75 23.462 16.341 10.746 7.519 0.5 12.689 9.770 7.579 6.174 0.25 7.727 6.229 4.558 3.464 0 0 0 0 0 T ABLE VI: Deterministic arbitrage gains for storage with load κ 2C-2C 1C-1C 0.5C-0.5C 0.25C-0.25C Arbitrage gains in $ for 1 week 1 9.411 7.059 4.784 3.065 0.75 7.462 6.269 4.540 3.025 0.5 6.641 5.987 4.468 3.019 0.25 6.350 5.904 4.451 3.019 0 6.313 5.902 4.451 3.019 Cycles of operation for 1 week 1 58.700 37.294 21.324 12.107 0.75 28.583 20.809 14.382 10.229 0.5 19.296 16.629 13.007 9.971 0.25 16.591 15.348 12.498 9.968 0 16.041 15.201 12.484 9.968 T ABLE VII: Real-time implementation for only storage κ 2C-2C 1C-1C 0.5C-0.5C 0.25C-0.25C Arbitrage gains in $ for 1 week 1 6.035 4.684 3.469 3.000 0.75 5.024 4.118 3.081 1.904 0.5 3.004 2.367 1.692 1.110 0.25 1.067 0.891 0.618 0.442 Cycles of operation for 1 week 1 64.323 38.979 22.622 12.850 0.75 24.870 16.169 10.570 7.733 0.5 11.393 8.891 7.013 6.099 0.25 6.429 5.557 4.359 3.395 • Effect of uncertainty on arbitrage gains for a faster ramping battery is greater compared to a slower ramping battery , this observation is in sync with conclusions drawn in [28]. • Combining storage with inelastic load with renew able gener- ation provides greater gains for decreasing κ . Furthermore, the effect of uncertainty for lower κ is lower compared to higher values of κ . • Profitability of operating only storage deteriorates sharply with decrease of κ . For only storage case under zero selling price case ( κ = 0 ) no arbitrage would be possible and the gain remains zero. V I . C O N C L U S I O N W e formulate energy storage arbitrage problem using linear programming. The linear programming formulation is possible due to piecewise linear con vex cost functions. In this formulation T ABLE VIII: Real-time implementation for storage with load κ 2C-2C 1C-1C 0.5C-0.5C 0.25C-0.25C Arbitrage gains in $ for 1 week 1 6.034 4.684 3.496 3.000 0.75 4.827 4.075 3.400 2.987 0.5 4.168 3.711 3.292 2.975 0.25 4.204 3.943 3.348 3.002 0 4.427 3.896 3.396 3.009 Cycles of operation for 1 week 1 64.322 38.979 22.622 12.850 0.75 41.613 30.322 19.948 11.980 0.5 34.658 27.627 18.744 11.348 0.25 31.429 26.370 18.476 11.396 0 32.958 28.255 19.845 11.372 we consider: (a) net-metering compensation (with selling price at best equal to buying price) i.e. κ i ∈ [0 , 1] , (b) inelastic load, (c) consumer renew able generation, (d) storage charging and discharging losses, (e) storage ramping constraint and (f) storage capacity constraint. By conducting extensi ve numerical simulations, we analyze the sensitivity of ener gy storage for varying ramp rates and varying ratio of selling and b uying price of electricity . W e observe that the value of storage in presence of load and renewable increases as the ratio of selling and buying price decreases. W e also perform real-time implementation of the proposed LP formulation and compare the deterministic results with net-load and electricity price uncertainties. Net-load and electricity price are modeled with AutoRegressiv e models for model predictiv e control. The effect of uncertainty on slow ramping batteries is observed to be lower compared to faster ramping batteries. Furthermore, as κ decreases, arbitrage gains becomes less sensitiv e to uncertainty . In a future work, we aim to control the cycles of operation of the battery by tuning the friction coefficient with different κ values, such that the battery is not over -used, otherwise this would lead to reduction in battery operational life. R E F E R E N C E S [1] X. Xi, R. Sioshansi, and V . Marano, “ A stochastic dynamic programming model for co-optimization of distributed energy storage, ” Energy Systems , vol. 5, no. 3, pp. 475–505, 2014. [2] M. U. Hashmi, L. Pereira, and A. Bu ˇ si ´ c, “Energy storage in madeira, portugal: Co-optimizing for arbitrage, self-sufficienc y , peak shaving and energy backup, ” arXiv pr eprint arXiv:1904.00463 , 2019. [3] M. U. Hashmi, D. Muthirayan, and A. Bu ˇ si ´ c, “Effect of real-time electricity pricing on ancillary service requirements, ” in Proceedings of the Ninth International Conference on Future Ener gy Systems . A CM, 2018, pp. 550–555. [4] “Net metering, wikipedia, ” Online, https://tinyurl.com/ybgzerct, 2017. [5] M. U. Hashmi, A. Mukhopadhyay , A. Bu ˇ si ´ c, and J. Elias, “Optimal control of storage under time varying electricity prices, ” in 2017 IEEE Inter- national Confer ence on Smart Grid Communications (SmartGridComm) . IEEE, 2017, pp. 134–140. [6] M. Hashmi, A. Mukhopadhyay , A. Busic, and J. Elias, “Storage optimal control under net metering policies, ” to be submitted IEEE T ransactions on Smart Grid . [7] Y . Xu and L. T ong, “Optimal operation and economic value of energy storage at consumer locations, ” IEEE T ransactions on Automatic Control , vol. 62, no. 2, pp. 792–807, 2017. [8] M. Zidar , P . S. Georgilakis, N. D. Hatziargyriou, T . Capuder, and D. ˇ Skrlec, “Revie w of energy storage allocation in power distribution networks: applications, methods and future research, ” IET Generation, T ransmission & Distribution , vol. 10, no. 3, pp. 645–652, 2016. [9] P . Mokrian and M. Stephen, “ A stochastic programming framework for the valuation of electricity storage, ” in 26th USAEE/IAEE North American Confer ence . Citeseer, 2006, pp. 24–27. [10] W . Hu, Z. Chen, and B. Bak-Jensen, “Optimal operation strategy of battery energy storage system to real-time electricity price in denmark, ” in P ower and Ener gy Society General Meeting . IEEE, 2010. [11] J. Cruise, L. Flatley , R. Gibbens, and S. Zachary , “Control of energy stor- age with market impact: Lagrangian approach and horizons, ” Operations Resear ch , vol. 67, no. 1, pp. 1–9, 2019. [12] Y .-G. Park, J.-B. Park, N. Kim, and K. Lee, “Linear formulation for short- term operational scheduling of energy storage systems in power grids, ” Ener gies , vol. 10, no. 2, p. 207, 2017. [13] R. H. Byrne and C. A. Silva-Monroy , “Potential revenue from electrical energy storage in ercot: The impact of location and recent trends, ” in 2015 IEEE P ower & Energy Society General Meeting . IEEE, 2015, pp. 1–5. [14] S. Chouhan, D. Tiwari, H. Inan, S. Khushalani-Solanki, and A. Feliachi, “Der optimization to determine optimum bess charge/discharge schedule using linear programming, ” in 2016 IEEE P ower and Energy Society General Meeting (PESGM) . IEEE, 2016, pp. 1–5. [15] A. A. Thatte, L. Xie, D. E. V iassolo, and S. Singh, “Risk measure based robust bidding strate gy for arbitrage using a wind farm and energy storage, ” IEEE T ransactions on Smart Grid , vol. 4, no. 4, pp. 2191–2199, 2013. [16] K. Bradbury , L. Pratson, and D. Pati ˜ no-Echev erri, “Economic viability of energy storage systems based on price arbitrage potential in real-time us electricity markets, ” Applied Energy , vol. 114, pp. 512–519, 2014. [17] T . A. Nguyen, R. H. Byrne, B. R. Chalamala, and I. Gyuk, “Maximizing the rev enue of energy storage systems in mark et areas considering nonlinear storage efficiencies, ” in 2018 International Symposium on P ower Electr on- ics, Electrical Drives, Automation and Motion (SPEED AM) . IEEE, 2018, pp. 55–62. [18] H. W ang and B. Zhang, “Energy storage arbitrage in real-time markets via reinforcement learning, ” in 2018 IEEE P ower & Energy Society Gener al Meeting (PESGM) . IEEE, 2018, pp. 1–5. [19] S. Boyd and L. V andenberghe, Con vex optimization . Cambridge university press, 2004. [20] “Energy prices, ” Online, http://www .energyonline.com/Data/, 2016. [21] M. U. Hashmi and A. Busic, “Limiting energy storage cycles of operation, ” in Green T echnologies Conference (GreenT ech), 2018 . IEEE, 2018, pp. 71–74. [22] M. U. Hashmi, W . Labidi, A. Bu ˇ si ´ c, S.-E. Elayoubi, and T . Chahed, “Long- term revenue estimation for battery performing arbitrage and ancillary services, ” in 2018 IEEE International Conference on Communications, Contr ol, and Computing T echnologies for Smart Grids (SmartGridComm) . IEEE, 2018, pp. 1–7. [23] M. U. Hashmi, D. Deka, A. Busic, L. Pereira, and S. Backhaus, “Co- optimizing ener gy storage for prosumers using con vex relaxations, ” sub- A P P E N D I X Epigraph formulation of Linear Programming An unconstrained minimization problem of a con ve x piecewise-linear function, h ( x ) , could be transformed to an equiv alent linear programming problem by forming the epigraph problem [19], [29]. Consider the conv ex piecewise cost function minimization problem is denoted as ( P org ) min h ( x ) , where h ( x ) = max i =1 ,...,m ( a T i x + b i ) . For cases where the decision mitted to 20th IEEE Intelligent Systems Applications to P ower Systems 2019 . [24] ——, “ Arbitrage with power factor correction using energy storage, ” arXiv pr eprint arXiv:1903.06132 , 2019. [25] E. D. Andersen and K. D. Andersen, “Presolving in linear programming, ” Mathematical Pr ogramming , vol. 71, no. 2, pp. 221–245, 1995. [26] “Real Time LMP , New Y ork ISO. ” [Online]. A vailable: https://tinyurl. com/2flow o6 [27] “Energy online california iso real-time price, ” Online, https://tinyurl.com/ p2ac2lh, 2019. [28] Y . Chen, M. U. Hashmi, D. Deka, and M. Chertko v , “Stochastic battery operations using deep neural networks, ” in in IEEE ISGT , NA W ashington DC , 2019. [29] P . L. V andenberghe, Online, https://tinyurl.com/yytfnmnx. variable x is scaler , a T i is also a scaler . Thus, a i x + b i is a two- dimensional line with b i denoting the y-intercept and a i the slope of the line. The equiv alent epigraph problem for the original problem P org is denoted as ( P epi ) min t, subject to, a i x + b i ≤ t, i = 1 , ..., m, where t denotes auxiliary scalar variable. The LP matrix notation for the optimization problem P epi is represented as: minimize ˜ f T ˜ x , subject to ˜ A ˜ x ≤ ˜ b ; where ˜ f = 0 1 , ˜ x = x t , ˜ A = a 1 − 1 : : a m − 1 , ˜ b = − b 1 : − b m . Now consider extending this minimization problem for two time instants with a unique cost function for each time instant. The optimization problem is denoted as ( P epi ) min t 1 + t 2 , s.t., (i) a 1 i x + b 1 i ≤ t 1 , (ii) a 2 i x + b 2 i ≤ t 2 , i = 1 , ..., m, The equiv alent LP matrices are denoted as ˜ f = 0 0 1 1 , ˜ x = x 1 x 2 t 1 t 2 , ˜ A = a 11 0 − 1 0 : : : : a 1 m 0 − 1 0 0 a 21 0 − 1 : : : : 0 a 1 m 0 − 1 , ˜ b = − b 11 : − b 1 m − b 21 : − b 2 m . A similar LP formulation for N time steps with piecewise linear cost function can be formulated. A C K N O W L E D G E M E N T The numerical results use the Madeira electricity consumer data collected under the framew ork of the H2020 SMILE project (GA 731249). W e would like to thank Dr Lucas Pereira for providing the data.

Original Paper

Loading high-quality paper...

Comments & Academic Discussion

Loading comments...

Leave a Comment