Robust Transmission Network Expansion Planning under Correlated Uncertainty

This paper addresses the transmission network expansion planning problem under uncertain demand and generation capacity. A two-stage adaptive robust optimization framework is adopted whereby the worst-case operating cost is accounted for under a given user-defined uncertainty set. This work differs from previously reported robust solutions in two respects. First, the typically disregarded correlation of uncertainty sources is explicitly considered through an ellipsoidal uncertainty set relying on their variance-covariance matrix. In addition, we describe the analogy between the corresponding second-stage problem and a certain class of mathematical programs arising in structural reliability. This analogy gives rise to a relevant probabilistic interpretation of the second stage, thereby revealing an undisclosed feature of the worst-case setting characterizing robust optimization with ellipsoidal uncertainty sets. More importantly, a novel nested decomposition approach based on results from structural reliability is devised to solve the proposed robust counterpart, which is cast as an instance of mixed-integer trilevel programming. Numerical results from several case studies demonstrate that the effect of correlated uncertainty can be captured by the proposed robust approach.

💡 Research Summary

This paper tackles the transmission network expansion planning (TNEP) problem under uncertain demand and generation capacity, explicitly accounting for the statistical correlation between these uncertain parameters. While most existing robust TNEP models rely on cardinality‑based or polyhedral uncertainty sets that treat uncertainties as independent, the authors introduce an ellipsoidal uncertainty set defined by the mean vector and the variance‑covariance matrix of the uncertain parameters. The set is expressed as a Mahalanobis‑distance constraint ‖d‑d̄‖_{Σ^{-1}} ≤ β, where β is a single conservativeness parameter that controls the size of the uncertainty region. This formulation captures correlation in a mathematically rigorous yet computationally tractable way.

The planning problem is cast as a two‑stage adaptive robust optimization model, which naturally leads to a mixed‑integer trilevel program: the first stage decides binary investment variables v subject to a budget Π; the second (middle) stage maximizes the operating cost over all realizations d inside the ellipsoidal set, thereby identifying the worst‑case scenario; the third (lower) stage minimizes the operating cost for the given v and d. The lower‑level problem is a linear program parameterized by v and d, while the middle‑level problem becomes nonlinear because of the ellipsoidal constraint.

A key methodological contribution is the observation that the middle‑level max‑problem is mathematically equivalent to a class of problems encountered in structural reliability, specifically the determination of a “limit state” under probabilistic constraints. Leveraging this analogy, the authors devise a nested decomposition algorithm. The outer loop implements a column‑and‑constraint generation (C&CG) scheme that separates the master problem (investment decisions) from the subproblem (worst‑case identification). The inner loop solves the max‑min subproblem using a decomposition technique originally developed for structural reliability, which yields an analytical solution for the inner maximization when the ellipsoidal set is active. To mitigate the risk of converging to local optima, a multi‑start strategy is employed, and the quality of the obtained solution is assessed out‑of‑sample via Monte‑Carlo simulation.

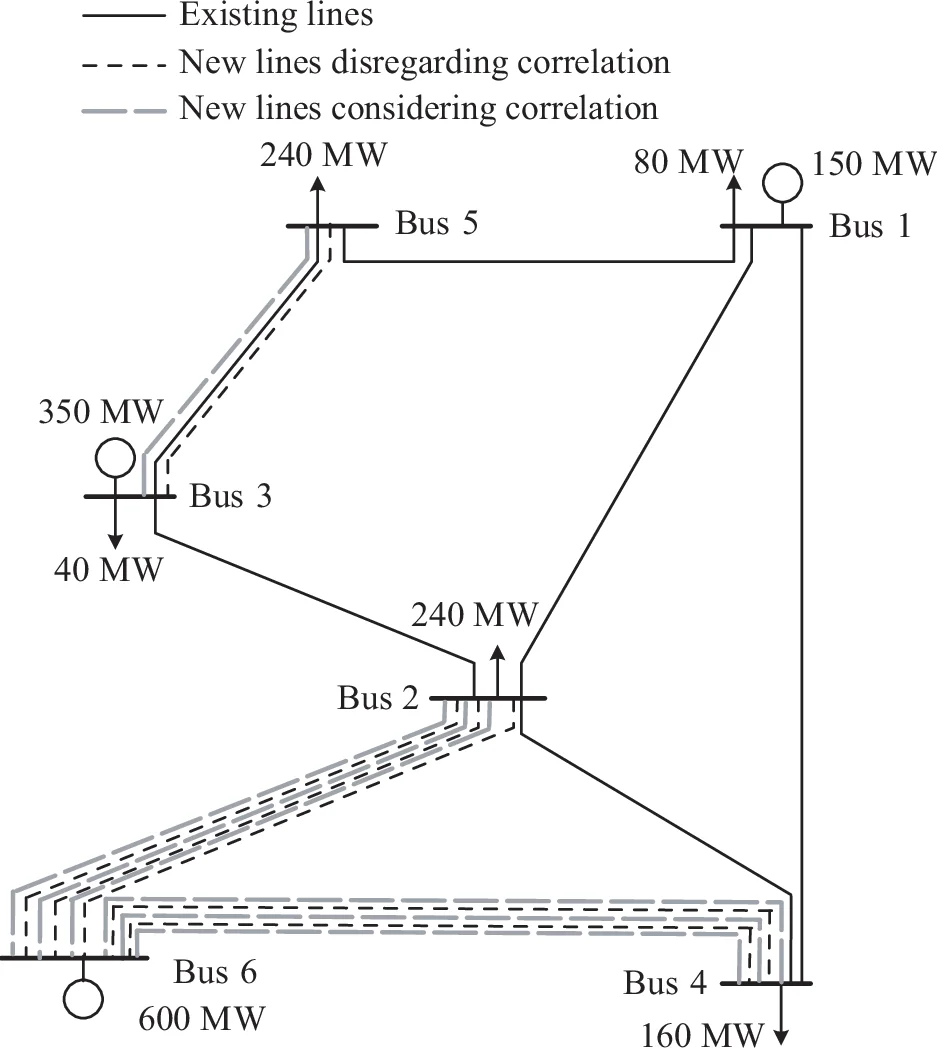

Numerical experiments are conducted on IEEE 14‑bus, IEEE 30‑bus, and a realistic Polish 2,383‑bus system. Results demonstrate that ignoring correlation can lead to sub‑optimal investment decisions, with cost overruns ranging from 5 % to 12 % compared to the correlated‑aware model. The impact of correlation is especially pronounced in scenarios with high penetration of renewable generation, where spatial and temporal dependencies are strong. Sensitivity analysis on the conservativeness parameter β shows that planners can smoothly trade off robustness against cost, providing a practical tool for risk‑averse decision making.

The paper’s contributions are fourfold: (1) introduction of an ellipsoidal uncertainty set that captures correlation with a single tunable parameter; (2) formulation of a two‑stage adaptive robust TNEP model that integrates this set; (3) establishment of a rigorous analogy with structural reliability problems, enabling quantitative assessment of solution quality; and (4) development of a novel nested decomposition algorithm that combines C&CG with reliability‑based decomposition, achieving scalable performance on large‑scale networks.

Limitations include the lack of a theoretical guarantee of global optimality— the algorithm relies on multi‑start heuristics—and the dependence on an accurately estimated covariance matrix, which may be challenging in data‑scarce environments. Future research directions suggested by the authors involve Bayesian or machine‑learning approaches for covariance estimation, incorporation of distributionally robust techniques, and exploration of stronger global optimization methods to further close the optimality gap.

Comments & Academic Discussion

Loading comments...

Leave a Comment