Applications of band-limited extrapolation to forecasting of weather and financial time series

This paper describes the practical application of causal extrapolation of sequences for the purpose of forecasting. The methods and proofs have been applied to simulations to measure the range which data can be accurately extrapolated. Real world data from the Australian Stock exchange and the Australian Bureau of Meteorology have been tested and compared with simple linear extrapolation of the same data. In a majority of the tested scenarios casual extrapolation has been proved to be the more effective forecaster.

💡 Research Summary

This paper investigates the practical use of causal band‑limited extrapolation for forecasting both financial and meteorological time series. Building on the theoretical framework introduced by Dokuchaev (2012), the authors define a left‑band‑limited sequence and construct linear operators Q (a sinc‑kernel based convolution) and its regularized inverse R⁺ using Tikhonov regularization. The process maps raw observations z(t) into a band‑limited space Bₙ, applies a causal smoothing filter, and then reconstructs a forecasted sequence x̂(t) that depends only on past data.

A Monte‑Carlo simulation is first conducted to assess the method’s intrinsic extrapolation horizon. Using N = 45 (91 historical points) and 10 000 repetitions, the authors extrapolate up to 20 steps ahead. Mean residuals remain between 0.95 and 1.0, indicating reasonable short‑term accuracy, but a systematic amplitude drop appears after the first few points due to the phase properties of the sinc kernel. To mitigate this, the authors employ an “overlap” strategy—re‑using the latter half of each forecast as the seed for the next—and rescale using the most recent moving‑average value.

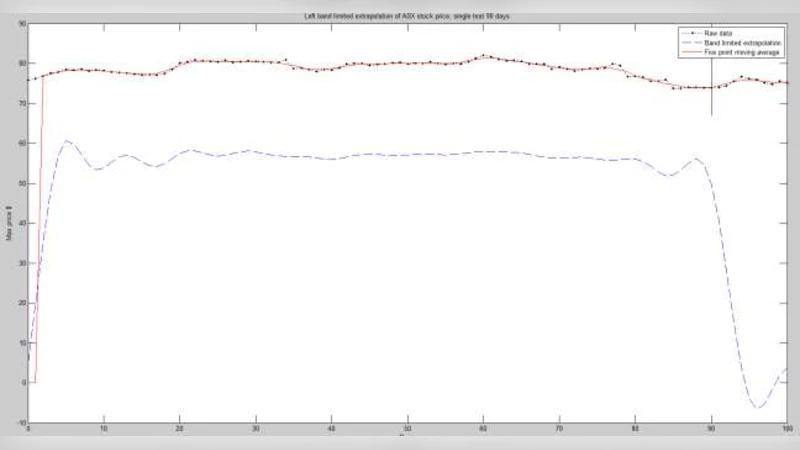

The technique is then applied to two real‑world domains.

-

Australian Stock Exchange (ASX200) and Commonwealth Bank (CBA) data – Daily open, high, low, and close prices from 11 Oct 2017 to 10 Oct 2018 are used. Three experiments are performed: a single 20‑day forecast, a 5‑day forecast repeated 32 times, and a 2‑day forecast repeated 79 times. Causal extrapolation is compared against a simple linear extrapolation that fits a two‑point line over the same historical window (90 points for the 5‑day case, 5 points for the 2‑day case). Results show that for the 5‑day horizon the causal method reduces the average absolute error by roughly 0.16 cents per day, while for the 2‑day horizon the improvement is about 0.04 cents. The 20‑day single forecast suffers from the early amplitude drop, but after applying the overlap‑and‑scale correction the error becomes comparable to the shorter horizons.

-

Bureau of Meteorology – Perth Metro maximum temperature – Daily maximum temperature records from Jan 1994 to Oct 2018 are examined, with 2016 serving as a control set and 2017 as the test set. Forecasts of 14‑day, 7‑day (repeated 38 times), and 2‑day (repeated 133 times) horizons are generated using the same N = 45 window and the overlap‑scale technique. In all cases, causal band‑limited extrapolation outperforms linear extrapolation by at least 1 °C, reflecting the strong low‑frequency content of temperature series that aligns well with the band‑limited assumption.

The authors discuss several methodological insights. The causal extrapolation yields a unique solution when the underlying process satisfies the left‑band‑limited condition; the choice of regularization parameter λ and window size N critically influences performance; and pre‑processing (e.g., moving averages) is essential for non‑stationary series. The amplitude attenuation inherent to sinc‑based kernels can be partially corrected by overlapping forecasts and scaling, but a more principled solution (e.g., adaptive kernel shaping) remains an open problem.

Limitations include sensitivity to parameter selection, the need for additional handling of trends and seasonality, and computational cost for large N. Future work is suggested in three directions: (a) automatic tuning of λ and N via cross‑validation or Bayesian optimization, (b) extension to multivariate series (e.g., joint forecasting of several stocks), and (c) real‑time implementation using FFT‑accelerated convolution and GPU processing.

In conclusion, the study demonstrates that causal band‑limited extrapolation provides a theoretically sound and empirically effective alternative to simple linear forecasts. It achieves lower mean absolute errors for short‑term horizons (≤ 7 days) in both financial and meteorological contexts, and shows particular strength for slowly varying, low‑frequency signals such as temperature. The work paves the way for more sophisticated, data‑driven forecasting systems that exploit band‑limited properties of time‑series.

Comments & Academic Discussion

Loading comments...

Leave a Comment