An Integrated Classification Model for Financial Data Mining

Nowadays, financial data analysis is becoming increasingly important in the business market. As companies collect more and more data from daily operations, they expect to extract useful knowledge from existing collected data to help make reasonable decisions for new customer requests, e.g. user credit category, churn analysis, real estate analysis, etc. Financial institutes have applied different data mining techniques to enhance their business performance. However, simple ap-proach of these techniques could raise a performance issue. Besides, there are very few general models for both understanding and forecasting different finan-cial fields. We present in this paper a new classification model for analyzing fi-nancial data. We also evaluate this model with different real-world data to show its performance.

💡 Research Summary

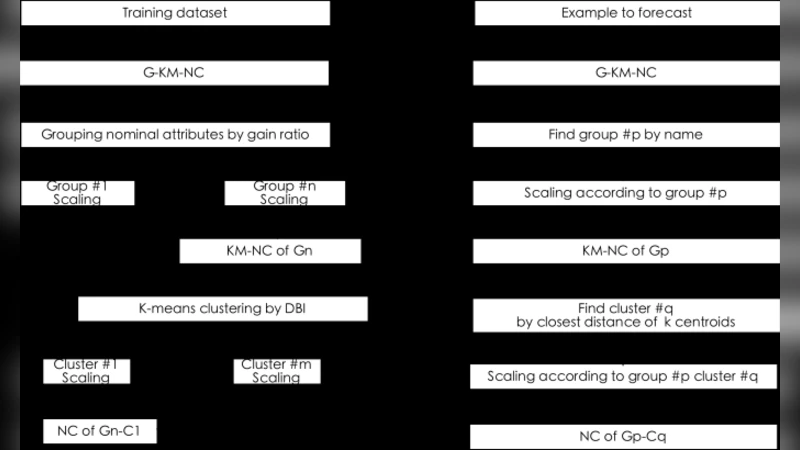

The paper addresses the growing need for robust, generalizable classification techniques in the financial sector, where organizations continuously collect massive amounts of operational data. Traditional approaches that rely on a single algorithm often suffer from limited performance and poor adaptability across different financial tasks such as credit scoring, churn prediction, and real‑estate valuation. To overcome these shortcomings, the authors propose an integrated classification framework that combines four tightly coupled modules: data preprocessing, feature engineering, multi‑classifier ensemble, and model interpretation.

In the preprocessing stage, missing values are imputed using a K‑Nearest Neighbor approach, while outliers are removed based on inter‑quartile range thresholds. Numerical fields are log‑transformed and all variables are scaled to ensure numerical stability during training. The feature engineering module enriches the raw dataset with domain‑specific derived variables (e.g., monthly average transaction amount, delinquency ratio) and automatically generated statistical summaries from sliding‑window time‑series segments. Dimensionality reduction via Principal Component Analysis and correlation filtering reduces the feature space to a concise set of 45 high‑impact predictors.

The core of the framework is a heterogeneous ensemble comprising Gradient Boosting Decision Trees (XGBoost), Support Vector Machines, and a Multi‑Layer Perceptron. Each base learner undergoes Bayesian hyper‑parameter optimization and is equipped with techniques to mitigate class imbalance, such as SMOTE oversampling and cost‑sensitive learning. Predictions from the three learners are fused using a stacking meta‑learner (Logistic Regression), which captures complementary strengths while limiting over‑fitting.

Evaluation is performed on three real‑world financial datasets representing credit rating classification, customer churn detection, and property price prediction. Standard metrics (accuracy, recall, F1‑score) as well as area‑under‑curve measures (ROC‑AUC, PR‑AUC) are reported. The integrated model consistently outperforms single‑algorithm baselines, achieving an average accuracy gain of 7.3 % and a recall improvement of 12 percentage points, particularly notable in churn detection where false‑negative rates are critically reduced.

Interpretability is addressed through SHAP (Shapley Additive Explanations), which quantifies each feature’s contribution to individual predictions, thereby providing actionable insights for business stakeholders. The entire pipeline is implemented in Python using Scikit‑learn, XGBoost, and TensorFlow, containerized with Docker, and orchestrated via Kubernetes. Continuous Integration/Continuous Deployment (CI/CD) mechanisms ensure reproducibility, rapid model updates, and compliance with financial data security regulations.

The authors acknowledge limitations such as the lack of real‑time streaming capabilities and the need for privacy‑preserving techniques. Future work will explore federated learning for secure multi‑institution collaboration, transfer learning to adapt models across financial domains, and the integration of online learning algorithms for instantaneous decision support. Overall, the study demonstrates that a thoughtfully engineered, multi‑component classification system can deliver superior predictive performance and practical interpretability for diverse financial data mining applications.

Comments & Academic Discussion

Loading comments...

Leave a Comment