On moment indeterminacy of the Benini income distribution

The Benini distribution is a lognormal-like distribution generalizing the Pareto distribution. Like the Pareto and the lognormal distributions it was originally proposed for modeling economic size distributions, notably the size distribution of perso…

Authors: Christian Kleiber

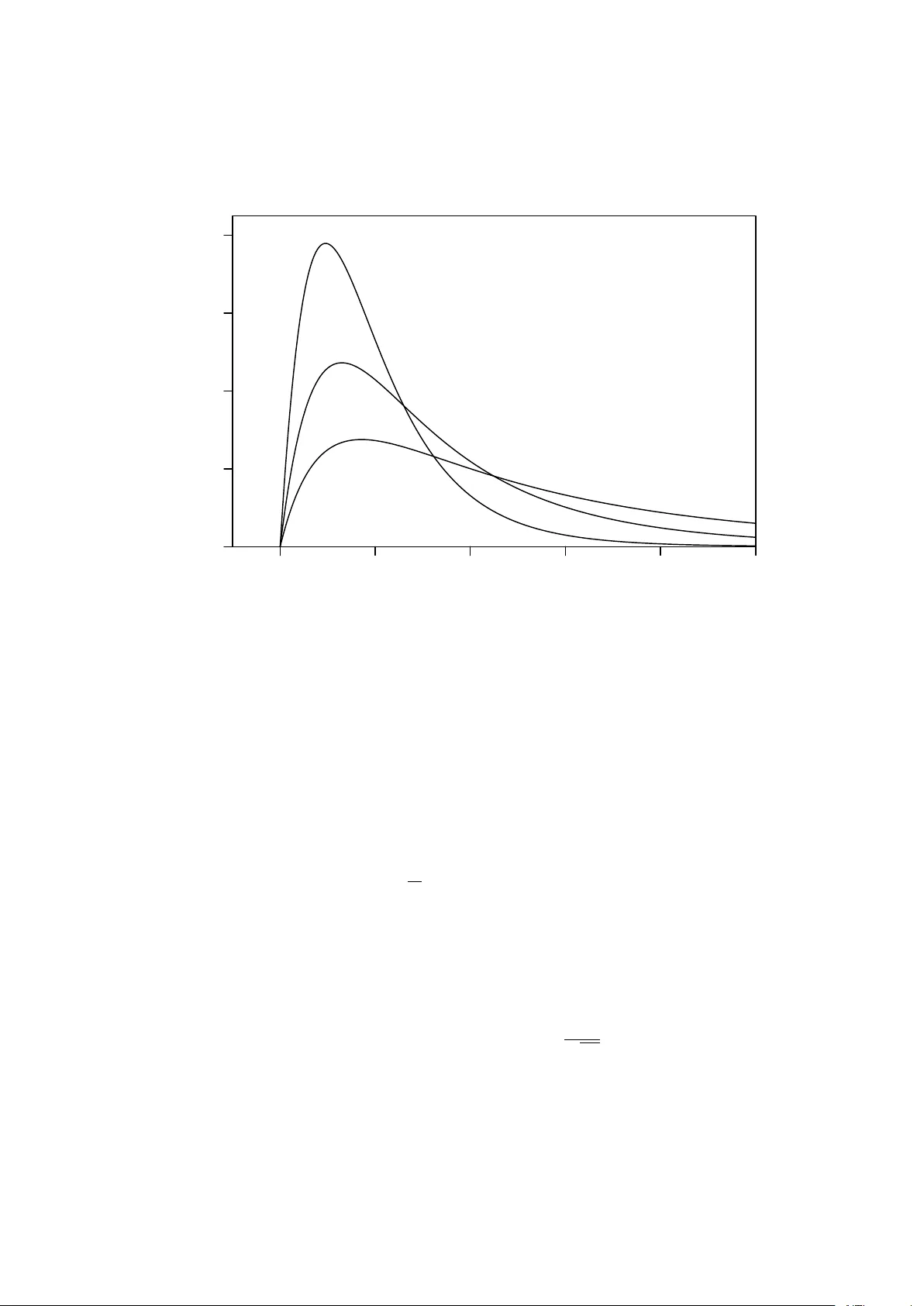

ON MOMENT INDETERMINA CY OF THE BENINI INCOME DISTRIBUTION Christian Kleiber The Benini distribution is a lognormal-lik e distribution generalizing the Pareto distribution. Lik e the P areto and the lognormal distributions it w as originally prop osed for mo deling economic size distributions, no- tably the size distribution of p ersonal income. This pap er explores a probabilistic prop ert y of the Benini distribution, sho wing that it is not determined b y the sequence of its momen ts although all the moments are finite. It also provides explicit examples of distributions p ossessing the same set of moment s. Related distributions are briefly explored. Keywords : Benini distribution, char acterization of distributions, in- come distribution, moment problem, statistical distributions, Stieltjes class. AMS 2010 Ma thema tics Subject Classifica tion: Primary 60E05, Secondary 62E10, 44A60. JEL Classifica tion: C46, C02. 1. INTR ODUCTION In the late 19th cent ury , the eminen t Italian economist Vilfredo P areto observ ed that empirical income distributions are well describ ed by a straight line on a doubly logarith- mic plot ( Paret o , 1895 , 1896 , 1897 ). Sp ecifically , with F = 1 − F denoting the surviv al function of an income distribution with c.d.f. F , Pareto observed that, to a go o d degree of appro ximation, ln F ( x ) = a 0 − a 1 ln x. (1.1) The distribution impl ied b y this equation is called the Pareto distribution. Not muc h later, the Italian statistician and demographer Ro dolfo Benini found that a second-order p olynomial ln F ( x ) = a 0 − a 1 ln x − a 2 (ln x ) 2 (1.2) sometimes pro vides a markedly better fit ( Benini , 1905 , 1906 ). The distribution implied by this equation is called the Benini distribution. The prese nt pap er is concerned with a probabilistic prop ert y of the Benini distribution, namely whether it is p ossible to charact erize this distribution in terms of its moments. The V ersion: April 29, 2013. Correspondence to: Christian Kleib er, F acult y of Business and Economics, Univ ersit ¨ at Basel, Peter Merian-W eg 6, 4002 Basel, Switzerland. christian.kleiber@unibas.ch 1 2 C. KLEIBER momen t probl em asks, for a giv en distri bution F with finite momen ts µ k ≡ E [ X k ] = R ∞ −∞ x k d F ( x ) of all orders k = 1 , 2 , . . . , whether or not F is uniquely determined by the sequence of its momen ts. See, for example, Shohat and T amarkin ( 1950 ) for analytical or Sto yan ov ( 2013 , Sec. 11) for probabilistic asp ects of the moment problem. If a distribution is uniquely determined b y the sequence of its momen ts it is called momen t-determinate, otherwise it is called momen t-indeterminate. Cases where the support of the distribution is the p ositive half-axis R + = [0 , ∞ ) or an unbounded subset thereof are called Stieltjes-t yp e momen t problems. The Benini distribution th us p oses a Stieltjes-type moment problem. It is sho wn below that the Benini moment problem is indeterminate. Drawing on a classical example going bac k to Stieltjes ( 1894/1895 ) explicit examples of distributions p ossessing the same set of moments are const ructed. Certain generalizatio ns of the Benini distribution are briefly explored, all of whic h are momen t-indeterminate. 2. THE BENINI DISTRIBUTION P areto’s observ ation ( 1.1 ) leads to a distribution of the form F ( x ) = 1 − x σ − α , x ≥ σ > 0 , where α > 0. Benini’s observ ation ( 1.2 ) leads to a distribution of the form F ( x ) = 1 − exp − α ln x σ − β ln x σ 2 , x ≥ σ > 0 , (2.1) where α , β ≥ 0, with ( α, β ) 6 = (0 , 0). Setting β = 0 gives the Pareto distribution. F or parsimon y , Benini ( 1905 ) often w ork ed with the sp ecial case where α = 0, i.e. with F ( x ) = 1 − exp − β ln x σ 2 (2.2) = 1 − x σ − β (ln x − ln σ ) , x ≥ σ > 0 . Here σ > 0 is a scale and β > 0 is a shap e parameter. This distribution will b e denoted as Ben( β , σ ). F or the pu rp oses of the present pap er the scale parameter σ is immaterial. The ob ject under study is, therefore, the Ben( β , 1) ≡ Ben( β ) distr ibution with F ( x ) = 1 − exp {− β (ln x ) 2 } , x ≥ 1 . (2.3) It may b e worth noting that the Beni ni distri butions ar e stochastica lly ordered w.r.t. β . Sp ecifically , it follo ws directly from ( 2.3 ) that F ( x ; β 1 ) ≤ F ( x ; β 2 ) for all x ≥ 1 ⇐ ⇒ β 1 ≤ β 2 , (2.4) MOMENT INDETERMINACY OF THE BENINI DISTRIBUTION 3 hence F ( x ; β 1 ) is larger than F ( x ; β 2 ) under this condition in the sense of the usual stochas- tic order, often called first-order stochastic dominance in economics. Noting further that the c.d.f. of a W eibull distribution is F ( x ) = 1 − exp( − x a ), x > 0, a > 0, it follows that eq. ( 2.3 ) describ es a log-W eibull distribution with a = 2. The W eibull distribution with a = 2 is also known (up to scale) as th e Ra yleigh distribution, esp ecially in physics, and so the Benini distribut ion ma y b e seen as the log-Ra yleigh di stribution. It ma y also b e seen as a log-chi distribution with tw o degrees of freedom (again up to scale); i.e., the logarithm of a Benini random v ariable follows the distribution of the square root of a c hi-square random v ariable with t w o degrees of fre edom. The density implied by ( 2.3 ) is f ( x ) = 2 β ln x x exp − β (ln x ) 2 , x ≥ 1 , (2.5) and hence is similar to the densit y of the more familiar lognormal distribution. The log- normal distribution is p erhaps the most widely known example of a distribution that is not determined b y its momen ts, although all its momen ts are finite ( Heyde , 1963 ). The similarit y of the lognormal and the Benini densities now suggests that the Benini distribu- tion might also p ossess this somewhat pathological prop ert y . The remainder of the present pap er explores thi s issue. Figure 1 depicts some t wo-parameter Benini densities, sho wing that distributions with smaller v alues of β are associated with hea vier tails, as in dicated b y ( 2.4 ). F rom a mo deling p oin t of view, the significance of the Benini distribution lies in the fact that it generalizes the Pareto distribution while itself b eing ‘lognormal-lik e’. It thus enables to discriminate b et w een these t wo widely used distribution s, at least appro ximately . F urther details on the Benini distribution, including an indep enden t rediscov ery in actuarial science motiv ated by failure rate considerat ions ( Shpilb erg , 1977 ), ma y b e found in Kleib er and Kotz ( 2003 , Ch. 7.1). The app endix of Kleiber and Kotz ( 2003 ) also provides a brief biograph y of Ro dolfo Benini. 3. THE BENINI DISTRIBUTION AND THE MOMENT PROBLEM The follo wing prop osition provides t wo basic prop erties of the Benini distribution that are relev an t in the context of the momen t problem. Pr oposition 1 (a) The moments µ k , k ∈ N , of the Benini distribution Ben( β ) ar e given by µ k ≡ E [ X k ] = 1 + k (2 β ) − (1 / 2) e k 2 / (8 β ) D − 1 − k √ 2 β (3.1) = 1 + k √ π 2 √ β e k 2 / (4 β ) 1 + erf k 2 √ β . (3.2) 4 C. KLEIBER 1 2 3 4 5 6 0.0 0.2 0.4 0.6 0.8 f(x) Figure 1 .— Some Benini densities; β = 2 , 1 , 0 . 5 (from left to right). Her e, D − 1 is a p ar ab olic cylinder function and erf denotes the err or function. (b) The moment gener ating function (m.g.f.) of the Benini distribution do es not exist. Pr o of. (a) W e ha v e µ k ≡ E [ X k ] = k Z ∞ 0 x k − 1 F ( x ) d x = 1 + k Z ∞ 1 x k − 1 exp {− β (ln x ) 2 } d x = 1 + k Z ∞ 0 e kx − β x 2 d x = 1 + k (2 β ) − (1 / 2) e k 2 / (8 β ) D − 1 − k √ 2 β , using Gradsht eyn and Ryzhik ( 2007 ), no. 3.462, eq. 1. This pro v es ( 3.1 ). The alternativ e represen tation ( 3.2 ) is established via the relation ( Olv er et al. , 2010 , § 12.7. 5) MOMENT INDETERMINACY OF THE BENINI DISTRIBUTION 5 D − 1 ( x ) = r π 2 e x 2 / 4 erfc x √ 2 , where erfc( · ) is the complemen tary error function, togeth er with erfc( x ) = 1 − erf( x ) and erf( − x ) = − erf( x ). (b) The defining in tegral is E [ e tX ] = Z ∞ 1 e tx 2 β ln x x exp − β (ln x ) 2 d x =: Z ∞ 1 h ( x ) d x. No w the leading term in ln h ( x ) = tx + ln(2 β ln x ) − ln x − β (ln x ) 2 is the linear term, hence E [ e tX ] = ∞ for all t > 0. The represen tation ( 3.2 ) can also b e obtained using Mathematica ( W olfram Research, Inc. , 2013 ), v ersion 9.0.1.0. As an i llustration, T able I pr ovides the first four momen ts of selected Benini di stributions, namely those from Figure 1 . These momen ts are rather large, esp ecially for small v alues of β . T ABLE I Lower-o rder moments of Benini distributions. E [ X ] E [ X 2 ] E [ X 3 ] E [ X 4 ] β = 2 1.98 4.48 11.81 37.20 β = 1 2.73 9.88 50.59 387.19 β = 0 . 5 4.48 37. 20 677.00 29888.67 Prop osition 1 show ed that the Benini distribution has momen ts of all orders, but no m.g.f. Distributions p ossessing these properties are candidates for momen t indeterminacy , although these facts alone are not conclusive. Unfortunately , no tractable necessary and sufficien t condi tion for momen t indeterminacy is currently kno wn. F or exploring determinacy , the Carleman criterion (e.g. Sto yano v , 2013 , Sec. 11) some- times provides an answer. In a Stieltjes-t yp e problem, the condition C S := ∞ X k =1 µ − 1 2 k k = ∞ 6 C. KLEIBER implies that the underlying distribution is c haracterized by its mo ments. Ho wev er, Prop osition 1 indicates that the m oments of the Benini distribution gro w rather rapidly . In view of erf( x ) ≥ 0, for x ≥ 0, it follo ws from ( 3.2 ) that E [ X k ] ≥ k √ π 2 √ β e k 2 / (4 β ) . Using the ratio test this further implies that C S = ∞ X k =1 µ − 1 2 k k ≤ ∞ X k =1 2 √ β k √ π 2 k e − k/ (8 β ) < ∞ . (3.3) So the Carleman condition cannot establish determinacy here. This suggests to explore indeterminacy instead. Indeed, Theorem 2 shows that all Benini distributions are momen t-indeterminate. Two pro ofs are given, one utilizing a conv erse to the Carleman criterion due to P akes ( 2001 ) and the other utilizing the Krein criterion ( Sto ya nov , 2000 , 2013 ). Theorem 2 The Benini distribution Ben ( β ) is moment-indeterminate for any β > 0 . Pr o of 1. P ak es ( 2001 , Th. 3) show ed that if ther e exists x 0 ≥ 0 suc h that 0 < f ( x ) < ∞ for x > x 0 , the condition C S < ∞ together with the con v exity of the function ψ ( x ) := − ln f ( e x ) on the interv al (ln x 0 , ∞ ) implies momen t indeterminacy . C S < ∞ was sho wn in ( 3.3 ). F or t he Benini distribution, the function ψ ( x ) = − ln f ( e x ) = − ln(2 β x ) + x + β x 2 is easily seen to be con v ex on the interv al (0 , ∞ ) in view of β > 0. Pr o of 2. In the case of a Stieltjes-t yp e moment problem, the Krein criterion requires, for a strictly positive densit y f and some c > 0, that the logarithmic integral K S [ f ] = Z ∞ c − ln f ( x 2 ) 1 + x 2 d x (3.4) is finite. F or the Benini distribution this in tegral is, c hoosing c = e , K S [ f ] = − Z ∞ e ln(2 β ln x 2 ) − ln x 2 − β (ln x 2 ) 2 1 + x 2 d x. This quantit y is finite for all β > 0. MOMENT INDETERMINACY OF THE BENINI DISTRIBUTION 7 4. A STIEL TJES CLASS F OR THE BENINI DISTRIBUTION The metho ds used in the proof of Theorem 2 only establish existence of further distri- butions p ossessing the same set of momen ts as the Benini distribution. It is known from Berg and Christensen ( 1981 ) that if a distribution is moment-indetermina te, then there exist infinitely many contin uous and also infinitely man y discrete dist ributions p ossessing the same momen ts. It is, therefore, of in terest to find explicit examples of such ob jects. A Stieltjes class ( Stoy ano v , 2004 ) corresp onding to a moment-i ndeterminate distribution with density f is a set S ( f , p ) = { f ε ( x ) | f ε ( x ) := f ( x )[1 + ε p ( x )] , x ∈ supp( f ) } , where p is a p erturbation function satisfying E [ X k p ( X )] = 0 for all k = 0 , 1 , 2 , . . . . If − 1 ≤ p ( x ) ≤ 1 and ε ∈ [ − 1 , 1], then S ( f , p ) is called a tw o-sided Stieltjes class. Counterexampl es to momen t det erminacy in the literature are t ypically of this t yp e. It is also possible to hav e one-sided Stieltjes classes, for which p only needs to b e b ounded from b elo w, and ε ≥ 0. The following Theorem provides a one-sided Stieltjes class for the Benini di stribution. Theorem 3 The distributions with densities f ε , 0 ≤ ε ≤ 1 , f ε ( x ) = f ( x ) 1 + ε x exp {− ( x − 1) 1 / 4 + β (ln x ) 2 } sin { ( x − 1) 1 / 4 } 2 C β ln x , x ≥ 1 , al l have the same moments as the Benini distribution Ben ( β ) with density f . Her e C > 0 is a normalizing c onstant define d in the pr o of. Pr o of. Consider the (unscaled) p erturbation ˜ p ( x ) = x exp {− ( x − 1) 1 / 4 + β (ln x ) 2 } sin { ( x − 1) 1 / 4 } 2 β ln x , x ≥ 1 . This p erturbation has the follow ing properties: (P1). lim x → 1 + ˜ p ( x ) = ∞ . (P2). Basic properties of the sine function imply that ˜ p ( x ) ≥ 0 on the interv al (1 , 2]. (P3). On the in terv al [2 , ∞ ), the function ˜ p is contin uous, with ˜ p (2) < ∞ and lim x →∞ ˜ p ( x ) = 0. Hence ˜ p ( x ) is bounded there. Let C = sup x ∈ [2 , ∞ ) | ˜ p ( x ) | and set p ( x ) = ˜ p ( x ) /C . It follows from (P1)–(P3) that p is un b ounded from ab o v e and b ounded from below, specifically − 1 ≤ p ≤ ∞ . By construction, 8 C. KLEIBER f ε ≥ 0. The momen ts of the corresp onding random v ariable X ε with density f ε , 0 ≤ ε ≤ 1, are further giv en by E [ X k ε ] = Z ∞ 1 x k f ε ( x ) d x = Z ∞ 1 x k f ( x ) { 1 + ε p ( x ) } d x = Z ∞ 1 x k f ( x ) d x + ε C Z ∞ 1 x k exp {− ( x − 1) 1 / 4 } sin { ( x − 1) 1 / 4 } d x =: E [ X k ] + J. It remains to sho w that J = 0. No w Z ∞ 1 x k exp {− ( x − 1) 1 / 4 } sin { ( x − 1) 1 / 4 } d x = Z ∞ 0 ( x + 1) k exp {− x 1 / 4 } sin { x 1 / 4 } d x = k X j =0 k j Z ∞ 0 x k − j exp {− x 1 / 4 } sin { x 1 / 4 } d x = 0 in view of Z ∞ 0 x n exp {− x 1 / 4 } sin { x 1 / 4 } d x = 0 (4.1) for all n ∈ N 0 . In particular, R ∞ 0 f ε ( x ) d x = 1. Note that Theorem 3 pro vides a fu rther pro of of the momen t indeterminacy of the Benini distribution. Apart from the shifted argumen t, the p erturbation emplo y ed here draws on the pioneering w ork of Stieltjes ( 1894/1895 ). In mo dern terminology , Stieltjes sho wed that the relation ( 4.1 ) leads to a family of distributions whose momen ts coincide with those of a certain generalized gamma distri bution, implying that the latter is moment-indetermin ate. Stieltjes ( 1894/1895 ) has a further, and more widely known, example of a distribution that is not determined by its momen ts, the lognormal distribution. The counterexam ple he pro vides for that distribution employs the perturbation p ( x ) = sin(2 π ln x ) , x > 0 , (4.2) whic h was further dev elop ed b y Heyde ( 1963 ). It can also lead to a Stieltjes class for the Benini distribution. Ho w ever, note that in view of the exp onen tial term common to b oth MOMENT INDETERMINACY OF THE BENINI DISTRIBUTION 9 the lognormal and the Benini densities, the p erturbation based on ( 4.2 ) only w orks for small v alues of β , otherwise the resulting ratio div erges for x → ∞ . Methods outlined b y Sto yan ov and T olmatz ( 2005 ) may help to construct Stieltjes classes based on ( 4.2 ) and the lognormal densit y that cov er the en tire range of the shap e parameter β , at the price of somewhat greater analytical complexit y . 5. RELA TED DISTRIBUTIONS It is natural to augmen t Pareto’s equation ( 1.1 ) by higher-order terms going b ey ond the second-order term proposed b y Benini ( 1905 ) . Not surprisingly , curv es of the form ln F ( x ) = a 0 − a 1 ln x − a 2 (ln x ) 2 − . . . − a k (ln x ) k (5.1) so on b egan to app ear in the subsequ ent Italian-language literature on economic statistics; see, e.g., Bresciani T urroni ( 1914 ) and Mortara ( 1917 ) for some early contribu tions. Some- what later, the Austrian statistician Winkler ( 1950 ) independently also exp erimen ted with p olynomials in ln x . Sp ecifically , he fitted a quadratic—i.e., the three-parameter Benini distribution ( 2.1 )—to the U.S. income distr ibution of 1919. Dropping a scale parameter, i.e. setting a 0 = 0, eq. ( 5.1 ) gives the c.d.f. F ( x ) = 1 − exp ( − k X j =1 a j (ln x ) j ) , x ≥ 1 , (5.2) where a 1 , . . . , a k ≥ 0, with corresp onding density f ( x ) = exp ( − k X j =1 a j (ln x ) j ) ( k X j =1 j a j (ln x ) j − 1 ) 1 x , x ≥ 1 . (5.3) Using the Krein criterion it is not difficult to see that these generalized Benini distri- butions are momen t-indeterminate, pro vided ( a 2 , . . . , a k ) 6 = (0 , . . . , 0) as otherwise not all momen ts exist. A further generalization of the Benini distribution pro ceeds along differen t lines. In sec- tion 2 it w as noted that the Benini distribution ma y be seen as the log-Rayleig h distribution, up to scale. It is then natural to consider the log-W eibull family , with c.d.f. F ( x ) = 1 − exp {− (ln x ) a } , x ≥ 1 , where a > 0, and corresp onding densit y f ( x ) = a (ln x ) a − 1 x exp {− (ln x ) a } , x ≥ 1 . 10 C. KLEIBER Indeed, Benini ( 1905 , p. 231) briefly discusses this mo del and reports that, for his data, when a = 2 . 15 the fit is sup erior to the one using mo del ( 2.3 ). Again, the Krein criterion ma y b e used to show that the log-W eibull distributions are moment-indetermin ate for an y a > 0. REFERENCES Benini, R. (1905): “I diagrammi a scala logaritmica (a prop osito della graduazione p er v alore delle suc- cessioni ereditarie in Italia, F rancia e Inghilterra),” Giornale de gli Ec onomisti, Serie II , 16, 222–231. ——— (1906): Principii di Statistic a Meto dolo gic a , T orino: Unione Tipografica–Editrice T orinese. Berg, C. and J. P. R. Christensen (1981): “Density Questions in the Classical Theory of Momen ts,” An nales de l’Institut F ourier , 31, 99–114. Bresciani Turroni, C. (1914): “Osserv azioni critic he sul “Meto do di Wolf ” p er lo studio della dis- tribuzione dei redditi,” Giornale de gli Ec onomisti e Ri vista di Statistic a, Serie IV , 25, 382–394. Gradshteyn, I. S. and I. M. R yzhik (2007): T ables of Inte gr als, Series and Pr o ducts , Amsterdam: Academic Press, 7th ed. Heyde, C. C. (1963): “On a Prop ert y of the Lognormal Distribution,” Journal of the R oyal Statistic al So ciety, Series B , 25, 392–393. Kleiber, C. and S. K otz (2003): Statistic al Size Distributions in Ec onomics and A ctuarial Scienc es , Hob ok en, NJ: John Wiley & Sons. Mor t ara, G. (1917): Elementi di Statistic a , Rome: A thenaeum. Ol ver, F. W. J., D. W. Lozier, R. F. Boisver t, and C. W. Clark , eds. (2010): NIST Handb o ok of Mathematic al F unctions , Cambridge: Cambridge Universit y Press. P akes, A. G. (2001): “Remarks on Conv erse Carleman and Krein Criteria for the Classical Moment Problem,” Journal of the Austr alian Mathematic al So ciety , 71, 81–104. P areto, V. (1895): “La legge della domanda,” Giornale de gli Ec onomisti , 10, 59–68, English translation in Rivista di Politic a Ec onomic a , 87 (1997), 691–700. ——— (1896): “La courb e de la r´ epartition de la richesse,” in R e cueil publi´ e p ar la F acult´ e de Dr oit ` a l’o c c asion de l’Exp osition Nationale Suisse, Gen` eve 1896 , Lausanne: Ch. Viret-G enton, 373–387, English translation in Rivista di Politic a Ec onomic a , 87 (1997), 645–660. ——— (1897): Cours d’´ ec onomie p olitique , Lausanne: Ed. Rouge. Shoha t, J. A. and J. D. T amarkin (1950): The Pr oblem of Moments , Providence, RI: American Math- ematical So ciety , revised ed. Shpilber g, D. C. (1977): “The Probabilit y Distribution of Fire Loss Amount,” Journal of R isk and Insur anc e , 44, 103–115. Stiel tjes, T. J. (1894/1895): “Recherc hes sur les fractions con tinues,” A nnales de la F acult ´ e des Scienc es de T oulouse , 8/9, 1–122, 1–47. Stoy anov, J. (2000): “Krein Condition in Probabilistic Momen t Problems,” Bernoul li , 6, 939–949. ——— (2004): “Stieltjes Classes for Moment-Indeterminate Probability Distributions,” Journal of Applie d Pr ob ability , 41A, 281–294. ——— (2013): Counter examples in Pr ob ability , New Y ork: Dov er Publications, 3rd ed. Stoy anov, J. and L. Tolma tz (2005): “Methods for Constructing Stieltjes Classes for M-Indeterminate Probabilit y Distributions,” Applie d Mathematics and Computation , 165, 669–685. Winkler, W. (1950): “The Corrected Pareto Law and its Economic Meaning,” Bul letin of the International Statistic al Institute , 32, 441–449. W olfram Research, Inc. (2013): Mathematica , V ersion 9.0.1.0 , Champaign, IL.

Original Paper

Loading high-quality paper...

Comments & Academic Discussion

Loading comments...

Leave a Comment