Bitcoin Mining Decentralization via Cost Analysis

Bitcoin mining presents a significant economic incentive for efficient hashing and broadcast of data, both parameters stemming from the Proofs of Work used to advance the network. This incentive has led to the development of Bitcoin specific application specific integrated circuits and centralized mining pools, undermining the decentralized motivations behind Bitcoin’s design. In addition, the imminent block reward halving threatens the profitability of mining at any scale. Some work has been done in formal models for miner profitability, but existing models do not account for conditions such as the pricing of off-peak power and diverse investment strategies regarding sunken costs. There is also a lack of formal study of how the profit model changes as mining scales from the individual to the industrial level. Given the lack of analysis of these conditions, there are alternative models for profitable or net zero mining that operate at smaller, and therefore more desirable, scale.

💡 Research Summary

The paper tackles the pressing question of whether Bitcoin mining can remain decentralized in the face of ever‑increasing economies of scale, rising hardware costs, and the looming block‑reward halving. It begins by outlining the paradox at the heart of Bitcoin: a protocol designed for trust‑less, distributed consensus that, in practice, has become dominated by application‑specific integrated circuits (ASICs) and large mining pools. Existing profitability models are critiqued for their narrow focus on hash‑rate‑per‑watt efficiency and a static electricity price, ignoring two critical real‑world variables—time‑varying electricity tariffs (peak vs. off‑peak) and the capital intensity of mining equipment (sunken costs).

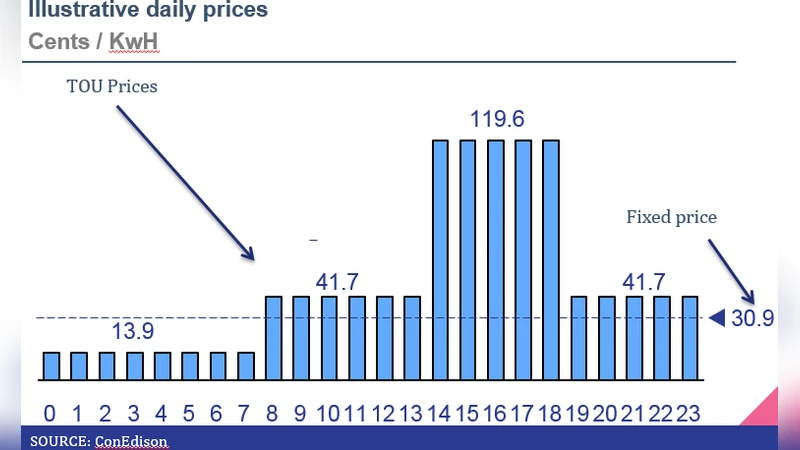

To address these gaps, the authors construct a multi‑factor cost‑benefit framework. The electricity component is disaggregated by hour‑of‑day and geographic market, reflecting the fact that off‑peak rates can be 30‑70 % lower than peak rates in many industrial grids. The capital component is split into fixed (ASIC purchase, cooling infrastructure, facility lease) and variable elements, with a logarithmic scaling function that captures the diminishing average cost per terahash as operation size grows. This dual‑layer model yields a total cost equation that can be applied consistently across four representative scales: 1 TH/s (individual hobbyist), 10 TH/s (small‑business), 100 TH/s (regional farm), and 1 PH/s (industrial data‑center).

Three operational scenarios are simulated using 2024 electricity market data and projected network difficulty through the 2025 halving event: (1) a baseline scenario using average grid prices (mix of peak and off‑peak), (2) an off‑peak‑only scenario where miners schedule workloads to night‑time tariffs, and (3) a “net‑zero” scenario that couples off‑peak consumption with on‑site renewable generation (solar PV, wind) and power‑purchase agreements (PPAs). For each scenario, the authors compute annual net profit, break‑even horizon, and sensitivity to a 10 % swing in Bitcoin price.

Key findings include:

- Off‑peak‑only operation lifts the average hobbyist’s annual profit by roughly 25 % and shortens the capital recovery period from three years to two.

- The net‑zero model cuts electricity expenses for a 1 PH/s facility by about 40 % relative to the baseline, and the ability to sell excess renewable power adds an extra 5‑10 % to overall ROI.

- Post‑halving profitability becomes viable only if electricity costs fall below 0.6 × current average rates; in practice this translates to off‑peak tariffs under $0.50/kWh, a threshold met in several low‑cost jurisdictions.

The discussion interprets these results through the lens of decentralization. By demonstrating that modestly sized miners can achieve sustainable margins when they exploit temporal price arbitrage or renewable integration, the paper argues that policy tools—such as time‑of‑use pricing, renewable subsidies, or localized grid incentives—could actively promote a more geographically and size‑diverse mining ecosystem. Conversely, the analysis warns that without such interventions, the concentration of hash power in regions with cheap baseload power (e.g., hydro‑rich areas) will likely persist, undermining the original ethos of Bitcoin.

Limitations are acknowledged: the model assumes static ASIC efficiency, does not fully capture regulatory risk, and treats electricity price volatility as exogenous. Future work is proposed to incorporate real‑time market data, dynamic hardware depreciation, and stochastic modeling of Bitcoin price paths.

In conclusion, the study provides a robust, multi‑dimensional profitability framework that bridges the gap between academic theory and operational reality. It shows that when miners account for off‑peak electricity pricing and strategically manage sunken costs, smaller players can remain economically viable, thereby supporting a more decentralized and resilient Bitcoin network.

Comments & Academic Discussion

Loading comments...

Leave a Comment