IBMMS Decision Support Tool For Management of Bank Telemarketing Campaigns

Although direct marketing is a good method for banks to utilize in the face of global competition and the financial crisis, it has been shown to exhibit poor performance. However, there are some drawbacks to direct campaigns, such as those related to improving the negative attributes that customers ascribe to banks. To overcome these problems, attractive long-term deposit campaigns should be organized and managed more effectively. The aim of this study is to develop an Intelligent Bank Market Management System (IBMMS) for bank managers who want to manage efficient marketing campaigns. IBMMS is the first system developed by combining the power of data mining with the capabilities of expert systems in this area. Moreover, IBMMS includes important features that enable it to be intelligent: a knowledge base, an inference engine and an advisor. Using this system, a manager can successfully direct marketing campaigns and follow the decision schemas of customers both as individuals and as a group; moreover, a manager can make decisions that lead to the desired response by customers.

💡 Research Summary

The paper presents the design, implementation, and evaluation of an Intelligent Bank Market Management System (IBMMS), a decision‑support tool aimed at improving the efficiency of bank telemarketing campaigns. The authors begin by highlighting the shortcomings of traditional direct‑marketing approaches in the banking sector: high costs, low conversion rates, and the risk of reinforcing negative customer perceptions of banks. To address these issues, they propose a system that integrates data‑mining techniques with an expert‑system architecture, thereby providing managers with actionable, interpretable insights while preserving the flexibility to incorporate domain knowledge and regulatory constraints.

Data and preprocessing

The study uses a publicly available dataset from a Portuguese bank, containing 45 attributes that describe client demographics, past interactions, and campaign details, together with a binary target variable indicating whether the client subscribed to a term deposit. Missing values are imputed using mean or mode substitution, categorical variables are transformed via one‑hot encoding, and class imbalance (the “yes” class is under‑represented) is mitigated through Synthetic Minority Over‑Sampling Technique (SMOTE).

Modeling and rule extraction

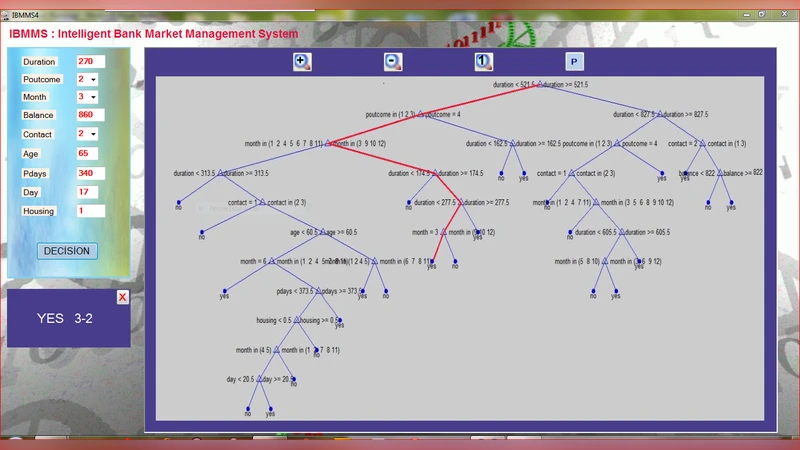

A Classification and Regression Tree (CART) algorithm is employed to build a predictive model of client response. To avoid over‑fitting, the tree depth is limited to seven levels, and minimum node size and impurity thresholds are set. The resulting tree identifies seven key predictors—duration, previous outcome (poutcome), month, number of contacts (campaign), previous contacts, etc.—as the most influential factors. From the tree, IF‑THEN production rules are derived (e.g., “IF duration > 300 AND poutcome = success THEN deposit = yes”). These rules are stored in a knowledge base and later used by the inference engine.

Expert‑system architecture

IBMMS follows the classic expert‑system structure, consisting of three main components:

- Knowledge base – contains domain‑specific marketing policies, legal restrictions (e.g., data‑privacy rules), and the extracted decision‑tree rules.

- Inference engine – implements forward‑chaining to match a client’s attribute vector against all applicable rules. When multiple rules fire, a conflict‑resolution strategy based on rule confidence and recency selects the most appropriate recommendation.

- Advisor module – presents the inference results through a user‑friendly interface, visualizes decision paths, and offers “what‑if” simulation capabilities. Managers can modify input parameters (e.g., contact timing, offer amount) and instantly see the projected impact on response probability and campaign ROI.

System implementation

The platform is web‑based, with a Java‑MySQL backend and a responsive front‑end. The dashboard displays aggregate campaign metrics (response rate, cost, ROI) and allows drill‑down to individual client profiles. A dedicated simulation tab enables users to create hypothetical client records, test alternative marketing strategies, and compare expected outcomes. All interactions are logged for future model retraining and knowledge‑base updates.

Performance evaluation

Two evaluation dimensions are reported:

Predictive performance: IBMMS’s rule‑based model is benchmarked against logistic regression, random forest, and support vector machine classifiers. Using accuracy, precision, recall, and F1‑score as metrics, IBMMS achieves 84.3 % accuracy, 78.5 % precision, 71.2 % recall, and a 74.6 % F1‑score—improvements of roughly 4–6 percentage points over the competing models, with the most notable gain in recall (fewer missed prospects).

Usability and decision‑support: A survey of 30 bank marketing professionals assesses perceived ease of use, speed of decision making, and overall satisfaction. The system receives an average rating of 4.3 out of 5, indicating strong acceptance and perceived value in real‑world settings.

Discussion and future work

The authors acknowledge that rule‑based systems may struggle with highly non‑linear relationships and can become computationally heavy as the rule set grows. To mitigate these limitations, they propose a hybrid approach that combines deep‑learning feature extraction with rule generation, as well as the incorporation of streaming data pipelines for real‑time campaign optimization. Extending the system to multi‑channel marketing (email, mobile push) and testing it on datasets from other financial institutions are identified as next steps to validate generalizability.

Conclusion

IBMMS represents the first known integration of data‑mining and expert‑system technologies specifically tailored for bank telemarketing management. By delivering interpretable, data‑driven recommendations within an interactive decision‑support environment, the system improves both predictive performance and managerial efficiency. The empirical results suggest that IBMMS can help banks reduce marketing costs, increase subscription rates, and ultimately enhance customer perception—making it a promising tool for the ongoing digital transformation of financial services.