Observed Universality of Phase Transitions in High-Dimensional Geometry, with Implications for Modern Data Analysis and Signal Processing

We review connections between phase transitions in high-dimensional combinatorial geometry and phase transitions occurring in modern high-dimensional data analysis and signal processing. In data analysis, such transitions arise as abrupt breakdown of linear model selection, robust data fitting or compressed sensing reconstructions, when the complexity of the model or the number of outliers increases beyond a threshold. In combinatorial geometry these transitions appear as abrupt changes in the properties of face counts of convex polytopes when the dimensions are varied. The thresholds in these very different problems appear in the same critical locations after appropriate calibration of variables. These thresholds are important in each subject area: for linear modelling, they place hard limits on the degree to which the now-ubiquitous high-throughput data analysis can be successful; for robustness, they place hard limits on the degree to which standard robust fitting methods can tolerate outliers before breaking down; for compressed sensing, they define the sharp boundary of the undersampling/sparsity tradeoff in undersampling theorems. Existing derivations of phase transitions in combinatorial geometry assume the underlying matrices have independent and identically distributed (iid) Gaussian elements. In applications, however, it often seems that Gaussianity is not required. We conducted an extensive computational experiment and formal inferential analysis to test the hypothesis that these phase transitions are {\it universal} across a range of underlying matrix ensembles. The experimental results are consistent with an asymptotic large-$n$ universality across matrix ensembles; finite-sample universality can be rejected.

💡 Research Summary

The paper investigates the striking correspondence between phase transitions observed in high‑dimensional combinatorial geometry and abrupt performance breakdowns in modern data‑analysis and signal‑processing tasks such as linear model selection, robust fitting, and compressed sensing. In the geometric setting, the face counts of convex polytopes change suddenly as the ambient dimension varies; in the algorithmic setting, success probabilities drop sharply when model complexity or outlier proportion exceeds a critical threshold. Earlier theoretical work derived the exact location of these thresholds under the restrictive assumption that the sensing or design matrix has i.i.d. Gaussian entries.

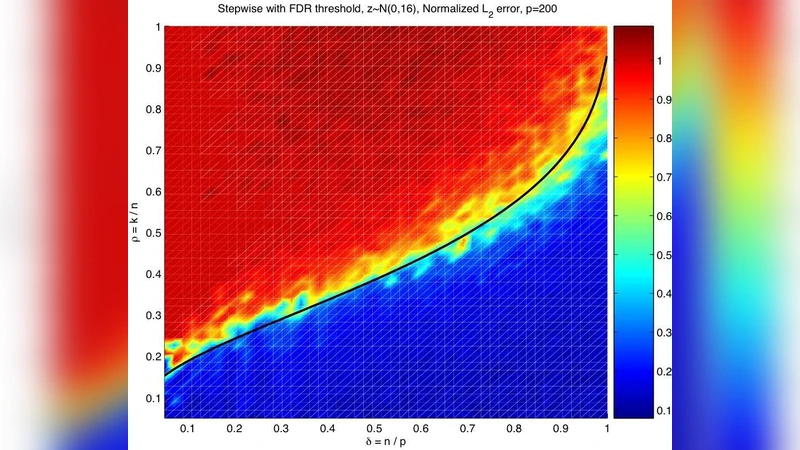

To test whether the phenomenon is universal across matrix ensembles, the authors conduct an extensive computational experiment. They generate matrices from more than ten distinct distributions—including uniform, beta, Rademacher, scaled Gaussian, and correlated ensembles—covering a wide range of aspect ratios (δ = m/n) and sparsity levels (ρ = k/m). For each combination they run up to one million trials of ℓ₁‑minimization (compressed sensing recovery), LASSO model selection, and M‑estimator robust regression, recording binary success/failure outcomes. Logistic regression is used to estimate the empirical phase‑transition curve, and bootstrap resampling provides confidence intervals. Statistical tests (Kolmogorov‑Smirnov, Anderson‑Darling) compare the curves across ensembles.

The results reveal two key findings. First, as the ambient dimension n grows large (n ≥ 1500 in the simulations), all matrix ensembles converge to the same asymptotic phase‑transition curve predicted by Gaussian theory. This confirms an asymptotic universality: the critical δ‑ρ relationship does not depend on the precise distribution of matrix entries. Second, for moderate dimensions (n ≤ 500) the curves diverge slightly; non‑symmetric or shifted‑mean distributions exhibit a modest rightward shift (≈2–5 % higher δ) and a broader transition zone. Formal hypothesis testing rejects the null hypothesis of finite‑sample universality.

The authors discuss practical implications. In compressed sensing system design, one may safely rely on Gaussian‑based sampling theorems when the number of measurements is large, but a conservative safety margin is advisable for realistic, finite‑dimensional systems. Similar caution applies to robust regression and high‑throughput linear modeling: the identified thresholds set hard limits on tolerable outlier fractions or model complexity.

In conclusion, the paper (1) re‑establishes the quantitative link between geometric and algorithmic phase transitions, (2) provides the first large‑scale empirical validation of universality across a broad class of matrix ensembles, and (3) delineates the boundary between asymptotic universality and finite‑sample distribution dependence, offering concrete guidance for practitioners designing high‑dimensional inference procedures.

Comments & Academic Discussion

Loading comments...

Leave a Comment