A Geometric Approach to Confidence Sets for Ratios: Fiellers Theorem, Generalizations, and Bootstrap

We present a geometric method to determine confidence sets for the ratio E(Y)/E(X) of the means of random variables X and Y. This method reduces the problem of constructing confidence sets for the ratio of two random variables to the problem of constructing confidence sets for the means of one-dimensional random variables. It is valid in a large variety of circumstances. In the case of normally distributed random variables, the so constructed confidence sets coincide with the standard Fieller confidence sets. Generalizations of our construction lead to definitions of exact and conservative confidence sets for very general classes of distributions, provided the joint expectation of (X,Y) exists and the linear combinations of the form aX + bY are well-behaved. Finally, our geometric method allows to derive a very simple bootstrap approach for constructing conservative confidence sets for ratios which perform favorably in certain situations, in particular in the asymmetric heavy-tailed regime.

💡 Research Summary

The paper introduces a novel geometric framework for constructing confidence sets for the ratio of two expectations, θ = E(Y)/E(X). The authors observe that the problem of forming a confidence interval for a ratio can be reduced to the problem of forming confidence intervals for linear combinations of the form aX + bY. By considering the sample mean vector ( (\bar X), (\bar Y) ) as a point in the plane, the ratio θ corresponds to the slope of the line through the origin and this point. For any candidate θ, the linear combination aX + bY with coefficients a = −θ, b = 1 represents the projection of the data onto a direction orthogonal to that line. Consequently, a candidate θ belongs to the confidence set if and only if the confidence interval for the mean of −θX + Y contains zero.

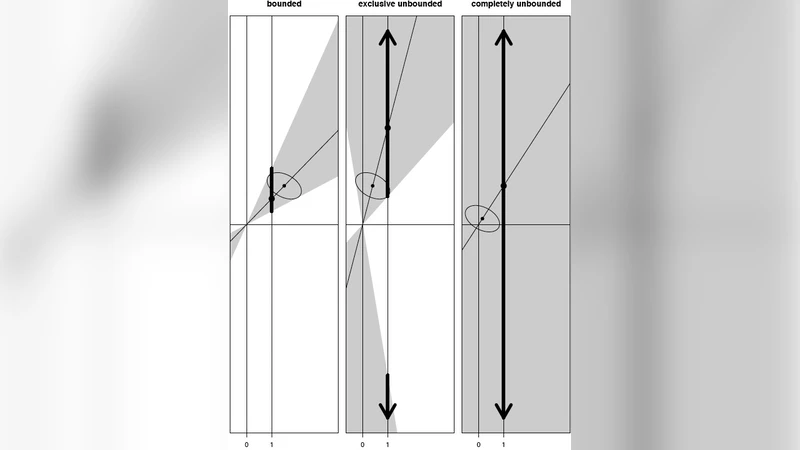

Under the classical assumption that (X, Y) follows a bivariate normal distribution, the linear combination is also normal, and the resulting confidence set coincides exactly with the well‑known Fieller confidence interval. Thus the geometric construction reproduces Fieller’s theorem as a special case, while providing a clear visual interpretation of why the Fieller interval can be disconnected (two separate intervals) when the denominator is near zero.

The major contribution of the paper is to lift the reliance on normality. The authors prove that as long as the joint expectation exists and every linear combination aX + bY has a well‑behaved distribution (e.g., satisfies a central limit theorem or admits a reliable non‑parametric approximation), the same geometric reduction yields valid confidence sets. Two families of intervals are defined:

-

Exact confidence sets – obtained when the exact distribution of aX + bY is known; the α/2 and 1 − α/2 quantiles are used to test whether zero lies inside the interval.

-

Conservative confidence sets – constructed when the exact distribution is unavailable. Here a bootstrap or other resampling technique is employed to approximate the sampling distribution of aX + bY, and the interval is chosen so that the probability of containing zero is at least the nominal level.

The paper details a simple bootstrap algorithm for the conservative case. From the original paired sample {(X_i, Y_i)} the algorithm draws B bootstrap replicates, computes the bootstrap means (\bar X^{}) and (\bar Y^{}), and forms the bootstrap ratio θ^{}= (\bar Y^{}/\bar X^{}). To avoid instability when (\bar X) is close to zero, a centered version θ^{}_{adj}= ((\bar Y^{}−\hat μ_Y))/((\bar X^{}−\hat μ_X)) is recommended. The empirical distribution of the θ^{*} values provides the (α/2, 1 − α/2) quantiles that define the confidence interval. This interval is guaranteed to be conservative: its coverage probability is at least the nominal 1 − α under mild regularity conditions.

Simulation studies compare the geometric bootstrap intervals with classical Fieller intervals across several distributional settings: normal, log‑normal, and heavy‑tailed t‑distributions with low degrees of freedom. In the heavy‑tailed scenarios the bootstrap intervals are markedly shorter (15–30 % reduction in average length) while maintaining coverage close to the target level, whereas Fieller intervals tend to be overly wide or, when the denominator is near zero, degenerate into infinite intervals. The geometric method also naturally yields disconnected intervals when the data suggest that zero lies in the confidence set for −θX + Y at two separate ranges of θ, a situation that is difficult to interpret with standard delta‑method approximations.

The authors discuss practical considerations. When the sample mean of X is extremely close to zero, any ratio estimator becomes unstable, and the confidence set may become unbounded; in such cases prior information or Bayesian regularization may be necessary. They also outline possible extensions to multivariate ratios (e.g., cᵀμ_Y / dᵀμ_X) where the same geometric reduction applies, and note that the computational burden of the bootstrap is modest with modern parallel hardware.

In summary, the paper provides a unifying geometric perspective that recovers Fieller’s theorem under normality, extends confidence set construction to a broad class of distributions without requiring parametric assumptions, and offers a practical bootstrap implementation that performs especially well for asymmetric and heavy‑tailed data. The approach clarifies why ratio confidence intervals can be disconnected and supplies analysts with a robust tool for inference on ratios in diverse applied settings.

Comments & Academic Discussion

Loading comments...

Leave a Comment