Transient fluctuation of the prosperity of firms in a network economy

The transient fluctuation of the prosperity of firms in a network economy is investigated with an abstract stochastic model. The model describes the profit which firms make when they sell materials to a firm which produces a product and the fixed cost expense to the firms to produce those materials and product. The formulae for this model are parallel to those for population dynamics. The swinging changes in the fluctuation in the transient state from the initial growth to the final steady state are the consequence of a topology-dependent time trial competition between the profitable interactions and expense. The firm in a sparse random network economy is more likely to go bankrupt than expected from the value of the limit of the fluctuation in the steady state, and there is a risk of failing to reach by far the less fluctuating steady state.

💡 Research Summary

The paper presents a stochastic framework for analyzing the transient fluctuations of firm prosperity within a networked economy. Each firm is represented by a continuous variable y_i(t) denoting its net worth or cumulative profit. Inter‑firm transactions are encoded as directed arcs v_j → v_i on a fixed digraph, with profitability parameters c_{ij} governing the income a firm receives from its suppliers and expense parameters d_i representing production costs. This formulation mirrors predator–prey dynamics in population biology, allowing the authors to derive a set of Langevin equations (1) and the associated Fokker‑Planck equation (2) for the joint probability density P(y,t).

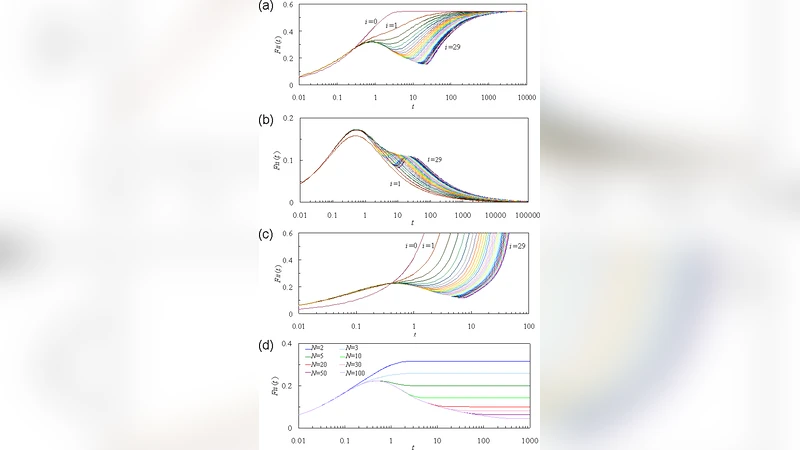

The authors first obtain closed‑form analytic solutions for two elementary topologies: a linear chain (representing a supply chain with unidirectional flow) and a directed ring (representing a business cluster with reciprocal interactions). Assuming homogeneous parameters (c for self‑profitability, c′ for nearest‑neighbor profit transfer, and d for fixed cost), they compute the first‑order moments μ_i(t) and the second‑order moments (covariances) σ_{ij}(t) explicitly via matrix exponentials and integral expressions (5)–(7). From these they define a dimensionless fluctuation measure F_{ij}(t)=σ_{ij}²/(μ_i μ_j).

Key analytic findings include:

- In the chain, the mean prosperity grows exponentially when c≥d, and the fluctuation initially scales as √t, reaching a local maximum around the “ignition time” t_p≈1/c′ when profit from the nearest neighbor becomes significant. Upstream firms experience lower fluctuations than downstream firms, reflecting the directional nature of the supply chain.

- In the ring, the feedback loop suppresses divergence; if c′>0 the fluctuation remains bounded. The long‑term limit of F_{ij} depends only on the combination of c, c′, and d (eq. 10). When c−d>0 the limit is finite; otherwise it diverges, indicating systemic instability.

- When self‑sustaining profitability (c) is absent, the system can still converge provided d<c′, but convergence is slower and the limiting fluctuation scales as N^{−½} with the number of firms N.

To explore more realistic settings, the authors perform numerical integration of the covariance integral (6) on heterogeneous random digraphs. Parameters c_{ij} and d_i are drawn from distributions centered on median values \hat{c} and \hat{d} with heterogeneity factor h. Simulations reveal that:

- Most firms exhibit a local peak in F_{ii}(t) near t≈t_p, followed by additional extrema whose number depends on node degree and position in the network.

- Downstream nodes in a chain display larger fluctuations than upstream nodes, confirming the analytic prediction.

- Sparse random networks with low average degree show a pronounced discrepancy between the theoretical steady‑state fluctuation limit (derived from chain or ring analysis) and the observed risk of bankruptcy; many firms experience fluctuations far exceeding the steady‑state bound, implying a higher probability of hitting the zero‑prosperity (bankruptcy) threshold during the transient phase.

The paper argues that traditional risk assessments based solely on steady‑state averages underestimate systemic vulnerability, especially in economies where the interaction graph is sparse and lacks reciprocal loops. The presence of cycles (rings) acts as a stabilizing mechanism, reducing the amplitude of fluctuations and thereby lowering the chance of cascading failures.

Policy implications are drawn: monitoring firms that occupy central positions or have high c′ values can provide early warning of systemic stress; encouraging reciprocal trade relationships (i.e., fostering ring‑like substructures) may enhance overall resilience. The authors suggest extensions such as incorporating nonlinear cost functions, adaptive network rewiring, and empirical validation with real supply‑chain data.

In conclusion, the study bridges stochastic population dynamics and corporate finance, offering a mathematically rigorous tool to quantify how network topology shapes the transient risk profile of firms. It highlights that the path to a stable, low‑fluctuation steady state can be fraught with heightened bankruptcy risk, especially for firms embedded in sparse, unidirectional trade networks.

Comments & Academic Discussion

Loading comments...

Leave a Comment