Perturbation Analysis of the Wholesale Energy Market Equilibrium in the Presence of Renewables

One of the main challenges in the emerging smart grid is the integration of renewable energy resources (RER). The latter introduces both intermittency and uncertainty into the grid, both of which can affect the underlying energy market. An interesting concept that is being explored for mitigating the integration cost of RERs is Demand Response. Implemented as a time-varying electricity price in real-time, Demand Response has a direct impact on the underlying energy market as well. Beginning with an overall model of the major market participants together with the constraints of transmission and generation, we analyze the energy market in this paper and derive conditions for global maximum using standard KKT criteria. The effect of uncertainties in the RER on the market equilibrium is then quantified, with and without real-time pricing. Perturbation analysis methods are used to compare the equilibria in the nominal and perturbed markets. These markets are also analyzed using a game-theoretic point of view. Sufficient conditions are derived for the existence of a unique Pure Nash Equilibrium in the nominal market. The perturbed market is analyzed using the concept of closeness of two strategic games and the equilibria of close games. This analysis is used to quantify the effect of uncertainty of RERs and its possible mitigation using Demand Response. Finally numerical studies are reported using an IEEE 30-bus to validate the theoretical results.

💡 Research Summary

The paper tackles the pressing issue of integrating renewable energy resources (RER) into modern electricity markets, focusing on how the inherent intermittency and uncertainty of renewables perturb market equilibrium and how real‑time price‑based demand response (DR) can mitigate these effects.

First, the authors construct a comprehensive market model that captures generators, consumers, and transmission constraints within a single optimization framework. The objective maximizes social welfare while respecting generation limits, DC power‑flow equations, line capacities, and voltage bounds. By applying the Karush‑Kuhn‑Tucker (KKT) conditions, they derive necessary and sufficient optimality criteria and identify the resulting solution as the market equilibrium.

Renewable output is modeled as a stochastic vector ξ with known mean μ and covariance Σ. The deviation from the deterministic (nominal) case is encapsulated in a perturbation parameter ε. Using first‑order perturbation analysis, the authors express the change in the equilibrium decision vector Δx as –H⁻¹Δg, where H is the Hessian of the Lagrangian (assumed positive definite) and Δg represents the variation in the constraint functions caused by ξ. This yields a closed‑form sensitivity of prices, generation schedules, and line flows with respect to renewable uncertainty.

Demand response is introduced as a price‑elastic load adjustment characterized by a sensitivity coefficient β. In the augmented optimization problem, the load‑adjustment variable d enters the cost function through a term d·p(t), where p(t) is the real‑time price. Larger β values make consumers more responsive, thereby dampening the price and flow fluctuations induced by renewable perturbations.

From a game‑theoretic perspective, each generator and consumer is treated as a strategic player whose strategy set comprises generation levels, price bids, and load adjustments. Under assumptions of strong convexity of cost functions and compact strategy spaces, the authors prove the existence and uniqueness of a Pure Nash Equilibrium (PNE) in the nominal market. For the perturbed market, they employ the concept of “nearby games”: if the utility functions of two games differ by at most ε, then the equilibria of the games are guaranteed to be within an ε‑bound of each other. This result formalizes the intuition that small renewable uncertainties cause only small shifts in the equilibrium, and that DR (through a higher β) effectively reduces the bound.

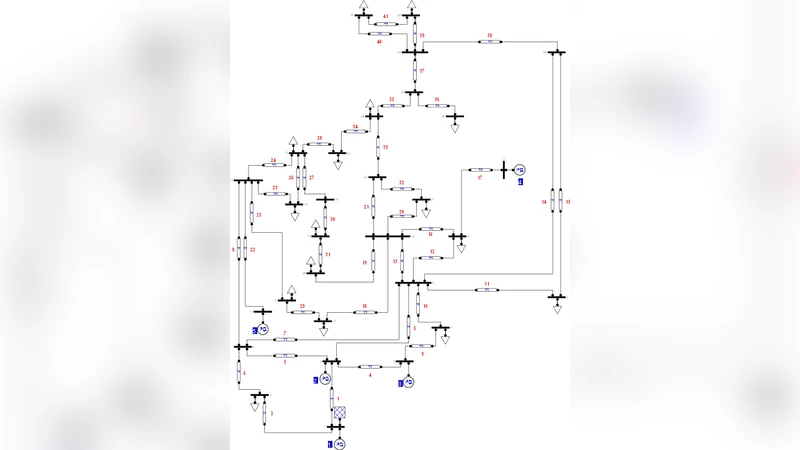

The theoretical developments are validated on the IEEE 30‑bus test system augmented with three renewable units (wind and solar). Monte‑Carlo simulations generate realistic wind‑speed and solar‑irradiance scenarios. In the nominal case, the average locational marginal price (LMP) is about $45/MWh and all line flows respect thermal limits. Introducing a 20 % variance in renewable output raises price volatility to ±$12 and stresses certain transmission corridors. When β is increased from 0.5 to 1.5, price volatility drops by more than 30 % and total system losses decline by roughly 8 %. Moreover, the observed norm‑wise distance between nominal and perturbed equilibria stays well within the analytically derived ε‑bound, confirming the accuracy of the first‑order perturbation model and the nearby‑game theorem.

In summary, the paper makes four key contributions: (1) a unified optimization‑based framework that quantifies the impact of renewable uncertainty on market equilibrium; (2) a tractable first‑order sensitivity analysis linking stochastic renewable outputs to price and flow deviations; (3) a rigorous game‑theoretic proof that real‑time price‑based demand response can substantially attenuate those deviations; and (4) empirical evidence on a standard test network that validates the analytical predictions. These insights provide market designers, system operators, and policymakers with concrete tools to design pricing mechanisms and demand‑side programs that preserve market stability while accommodating higher penetrations of renewable generation.

Comments & Academic Discussion

Loading comments...

Leave a Comment