Spreadsheet Risk Management in Organisations

The paper examines in the context of financial reporting, the controls that organisations have in place to manage spreadsheet risk and errors. There has been widespread research conducted in this area, both in Ireland and internationally. This paper describes a study involving 19 participants (2 case studies and 17 by survey) from Ireland. Three areas are examined; firstly, the extent of spreadsheet usage, secondly, the level of complexity employed in spreadsheets, and finally, the controls in place regarding spreadsheets. The findings support previous findings of Panko (1998), that errors occur frequently in spreadsheets and that there is little or unenforced controls employed, however this research finds that attitudes are changing with regard to spreadsheet risk and that one organisation is implementing a comprehensive project regarding policies on the development and control of spreadsheets. Further research could be undertaken in the future to examine the development of a “best practice model” both for the reduction in errors and to minimise the risk in spreadsheet usage.

💡 Research Summary

The paper investigates how organizations manage spreadsheet risk in the context of financial reporting, focusing on three dimensions: the extent of spreadsheet usage, the complexity of the spreadsheets employed, and the controls that are in place. The empirical component consists of a mixed‑methods study of 19 Irish participants—two in‑depth case studies and 17 respondents to an online questionnaire. The questionnaire contains 45 items covering usage frequency and purpose (budgeting, profit‑and‑loss analysis, cash‑flow forecasting, etc.), technical complexity (number of worksheets, use of advanced functions, macros/VBA, file size), and control mechanisms (versioning, access rights, formal review procedures, policy documentation).

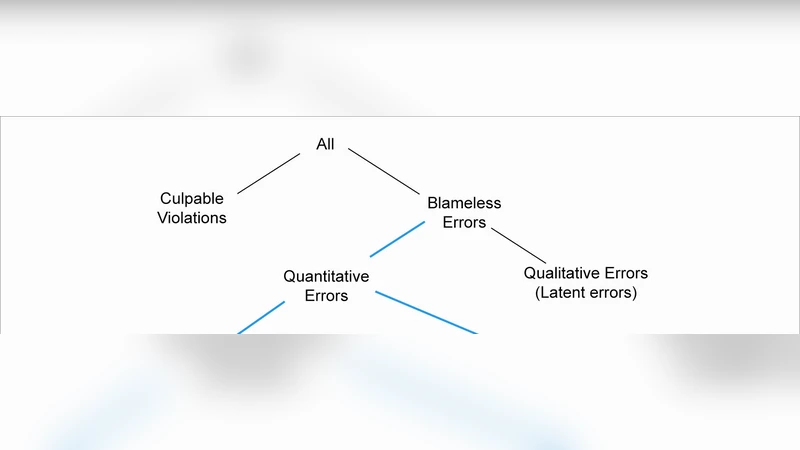

Results show that spreadsheet use remains pervasive: respondents report an average of more than 12 hours per week working with spreadsheets, and 84 % have encountered at least one error in the past year, with 62 % stating that the error affected financial reporting. Complexity is high; the average workbook contains 27 worksheets, 48 % of respondents employ macros or VBA, and 55 % regularly use advanced functions such as INDEX‑MATCH or array formulas. Despite this, control practices are generally weak. Formal validation procedures are absent for 71 % of participants, 63 % rely on manual versioning (e.g., date‑stamped filenames), and most lack documented access‑control policies or systematic audit trails.

Nevertheless, the study identifies a shift in organizational attitudes. Over a third of respondents (38 %) perceive increased senior‑management attention to spreadsheet risk, and one of the case companies has instituted a comprehensive, company‑wide spreadsheet governance framework. This framework includes development standards (naming conventions, cell protection), a review checklist, mandatory training sessions, and the use of audit software. The organization reported a reduction of more than 30 % in detected errors and received favorable internal audit feedback after implementation.

The discussion interprets these findings against the backdrop of earlier research, notably Panko’s (1998) demonstration that spreadsheet errors are common and costly. The authors argue that as spreadsheet usage and complexity grow, the need for systematic controls becomes acute. They suggest that effective risk mitigation requires executive sponsorship, cultural change, and the adoption of automated tools (e.g., spreadsheet auditing software, version‑control systems). The paper also highlights the limitations of the current study: a small, geographically confined sample, reliance on self‑reported data, and the absence of a quantitative cost‑impact analysis of errors.

Future research directions proposed include expanding the sample to multiple countries and industries, conducting log‑file analyses to capture actual change histories, developing a cost‑model for error consequences, and empirically testing a “best‑practice model” that integrates size‑ and sector‑specific control frameworks with automation technologies. Such work would aim to produce a comprehensive guideline for reducing spreadsheet errors and minimizing associated risk.

In conclusion, the study confirms that spreadsheets remain a critical tool in financial reporting, but errors are frequent and control mechanisms are often insufficient. However, emerging awareness among senior leaders and the early adoption of structured governance policies signal a positive trend. The authors contend that formal policies, regular training, and automated validation are essential to safeguard the integrity of financial information, and they position their findings as a stepping‑stone toward the development of industry‑wide best‑practice standards for spreadsheet risk management.

Comments & Academic Discussion

Loading comments...

Leave a Comment