Non-Equilibrium Dynamics of Dysons Model with an Infinite Number of Particles

Dyson's model is a one-dimensional system of Brownian motions with long-range repulsive forces acting between any pair of particles with strength proportional to the inverse of distances with proportionality constant $\beta/2$. We give sufficient con…

Authors: Makoto Katori, Hideki Tanemura

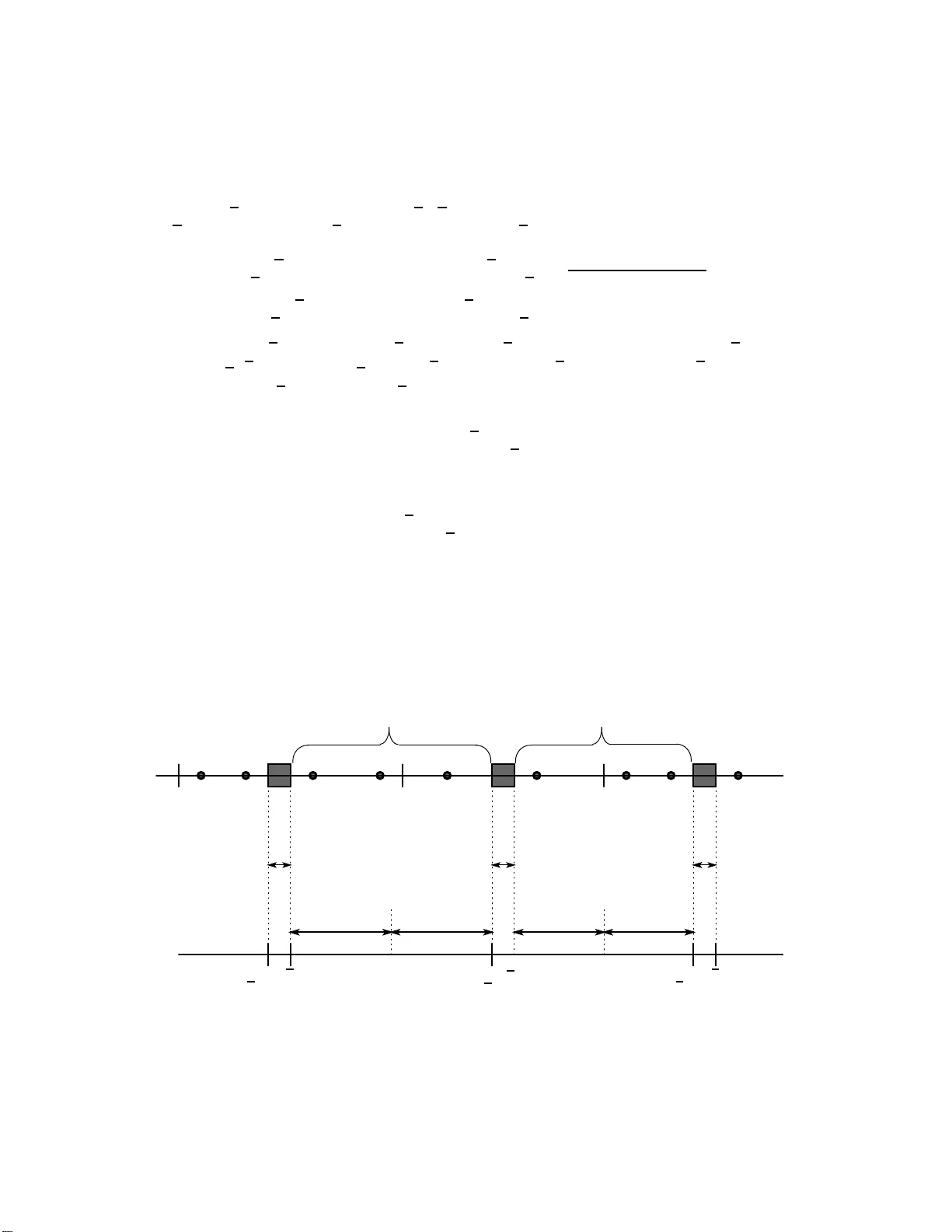

Non-Equilib rium Dynamics of Dyson ’s Mo del with an Infin ite Num b er of P article s Mak oto Katori 1 , Hideki T anem ura 2 1 Department of Physics, F aculty of Science and Engineering, Chuo Universit y , Kasuga , Bunkyo-ku, T oky o 112 -8551 , Japan. E-mail: k atori@phys.c huo-u.ac.jp 2 Department of Mathematics and Informatics, F aculty o f Science , Chiba Universit y , 1-33 Y ay oi-cho, Inage- ku, Chiba 263-85 22, Japa n. E-mail: tanemura@math.s.chiba-u.ac.jp (19 June 2009) Abstract: D yson’s mo del is a one-dimensional system of Brownian motions with long-range repulsiv e f o rces acting b etw een an y pair of part icles with strength pro- p ortional to t he in v erse of distances with prop ortionalit y constan t β / 2. W e give sufficien t conditions for initial configuratio ns so that Dyson’s model w ith β = 2 and an infinite n um b er of par t icles is w ell defined in the sense that an y multitime cor- relation function is giv en by a determinan t with a con tinuous k ernel. The class of infinite-dimensional configurations satisfying our conditions is larg e enough to study non-equilibrium dynamics. F or example, w e obtain the relaxation pro cess starting from a configuration, in whic h ev ery p oin t o f Z is o ccupied b y one particle, to the stationary state, whic h is the determinan tal p oin t pro ces s with the sine k ernel. 1 In tro duction In o rder to understand the statistics o f eigen v alues of random matrix ensem bles as equilibrium distributions of particle p o sitions in the one-dimensional Coulom b gas systems with log-p o ten tials, D yson in tro duced sto c hastic mo dels of particles in R , whic h ob ey the sto chastic differen tia l equations (SD Es), dX j ( t ) = dB j ( t ) + β 2 X 1 ≤ k ≤ N ,k 6 = j dt X j ( t ) − X k ( t ) , 1 ≤ j ≤ N , t ∈ [0 , ∞ ) , (1.1) where B j ( t )’s are indep enden t one-dimensional standard Bro wnian mot ions [3]. The Gaussian orthogonal ensem ble (GOE), the Gaussian unitary ense m ble (GUE), and the Gaussian symple ctic ens em ble (G SE) of random matrices cor r esp o nd to the SDEs (1.1) with β = 1 , 2 and 4 , res p ectiv ely [1 4 ]. Spohn [20] has considered an infinite particle system obtained by taking the N → ∞ limit of (1 .1) with β = 2 and called the system D yson ’s mo del . He studied the equilibrium dynamics with resp ect to the determinan tal (F ermion) p oint pro cess µ sin , in which an y spatial correlation function ρ m is giv en by a dete rminant with the sine kerne l [19, 18] K sin ( y − x ) = 1 2 π Z | k |≤ π dk e ik ( y − x ) = sin { π ( y − x ) } π ( y − x ) , x, y ∈ R , (1.2) 1 where i = √ − 1. By the Dirichlet f o rm approach Osada [16] constructed the infinite particle system represen ted by a diffusion pro cess , whic h has µ sin as a rev ersible measure. Recen tly he pro v ed that this system satisfies the SDEs (1.1) w ith N = ∞ [17]. On the other hand, it w as sho wn b y Eynard and Meh ta [4] that m ultitime correlation functions for the pro ces s (1.1) are generally g iv en b y determinan ts, if the pro cess starts from µ GUE N ,σ 2 , the eigen v alue distribution of GUE with v aria nce σ 2 . Nagao a nd F o rrester [15] ev alua t ed the bulk scaling limit σ 2 = 2 N/ π 2 → ∞ and deriv ed the so-called ex tend e d sine kernel with densit y 1, K sin ( t − s, y − x ) = 1 2 π Z | k |≤ π dk e k 2 ( t − s ) / 2+ ik ( y − x ) − 1 ( s > t ) p ( s − t, x | y ) = Z 1 0 du e π 2 u 2 ( t − s ) / 2 cos { π u ( y − x ) } if t > s K sin ( y − x ) if t = s − Z ∞ 1 du e π 2 u 2 ( t − s ) / 2 cos { π u ( y − x ) } if t < s, (1.3) s, t ≥ 0 , x, y ∈ R , where 1 ( ω ) is the indicator function of condition ω , and p ( t, y | x ) is the he at kernel p ( t, y | x ) = e − ( y − x ) 2 / 2 t √ 2 π t = 1 2 π Z R dk e − k 2 t/ 2+ ik ( y − x ) , t > 0 . (1.4) Since lim N →∞ µ GUE N , 2 N/π 2 = µ sin , the pro cess , wh ose m ultit ime correlation f unctions are giv en by determinan ts with the extended sine k ernel (1.3), is exp ected to b e iden tified with the infinite-dimensional equilibrium dynamics of Sp ohn and Osada. This equiv alence is, how ev er, not y et pro v ed. F ritz [5] established t he theory of non-equilibrium dynamics of infinite particle systems with a finite- r a nge smo oth p otential. Here w e study the non-equilibrium dynamics of infinite- pa r ticle Dyson’s mo del with a long- range log- p oten tial, in whic h the fo r ce acting eac h particle is singular b oth for short and lo ng distances (see (1.1)). W e denote b y M the space of nonnegative in teger-v alued Radon measures on R , whic h is a Polish space with the v ague top ology: we say ξ n , n ∈ N ≡ { 1 , 2 , . . . } con v erges to ξ v aguely , if lim n →∞ R R ϕ ( x ) ξ n ( dx ) = R R ϕ ( x ) ξ ( dx ) for any ϕ ∈ C 0 ( R ), where C 0 ( R ) is the set of all con tin uous real- v alued functions with compact supp orts. An y elemen t ξ of M can b e represen ted as ξ ( · ) = P j ∈ Λ δ x j ( · ) with a sequence of p oin ts in R , x = ( x j ) j ∈ Λ satisfying ξ ( K ) = ♯ { j ∈ Λ : x j ∈ K } < ∞ fo r any compact subset K ⊂ R . The index set Λ is N or a finite set. W e call an elemen t ξ of M an unlab eled configuration, and a sequenc e x a lab eled configuration. F or A ⊂ R , w e write the restriction of ξ o n A a s ( ξ ∩ A )( · ) = P j ∈ Λ: x j ∈ A δ x j ( · ). As an M -v alued pro cess ( P , Ξ( t ) , t ∈ [0 , ∞ ) ) , w e consider the system suc h that, for any in teger M ≥ 1, f m ∈ C 0 ( R ) , θ m ∈ R , 1 ≤ m ≤ M , 0 < t 1 < · · · < 2 t M < ∞ , the expectation of exp n P M m =1 θ m R R f m ( x )Ξ( t m , dx ) o can be expanded with χ m ( x ) = e θ m f m ( x ) − 1 , 1 ≤ m ≤ M as G ξ [ χ ] ≡ X N 1 ≥ 0 · · · X N M ≥ 0 M Y m =1 1 N m ! Z R N 1 N 1 Y j =1 dx (1) j · · · Z R N M N M Y j =1 dx ( M ) j × M Y m =1 N m Y j =1 χ m x ( m ) j ρ t 1 , x (1) N 1 ; . . . ; t M , x ( M ) N M , where x ( m ) N m denotes ( x ( m ) 1 , . . . , x ( m ) N m ) , 1 ≤ m ≤ M . Here ρ ’s are lo cally in tegrable functions, whic h are symmetric in the sense that ρ ( . . . ; t m , σ ( x ( m ) N m ); . . . ) = ρ ( . . . ; t m , x ( m ) N m ; . . . ) with σ ( x ( m ) N m ) ≡ ( x ( m ) σ (1) , . . . , x ( m ) σ ( N m ) ) for any p erm utation σ ∈ S N m , 1 ≤ ∀ m ≤ M . In suc h a system ρ ( t 1 , x (1) N 1 ; . . . ; t M , x ( M ) N M ) is called the ( N 1 , . . . , N M )-m ultitime correlation function a nd G ξ [ χ ] the generating function of multitime correlation functions. There are no m ultiple p o ints with prob- abilit y one for t > 0. Then w e assume that there is a function K ( s, x ; t, y ), whic h is con tin uous with respect to ( x, y ) ∈ R 2 for any fixed ( s, t ) ∈ [0 , ∞ ) 2 , suc h that ρ t 1 , x (1) N 1 ; . . . ; t M , x ( M ) N M = det 1 ≤ j ≤ N m , 1 ≤ k ≤ N n 1 ≤ m,n ≤ M " K ( t m , x ( m ) j ; t n , x ( n ) k ) # for an y in teger M ≥ 1, any sequence ( N m ) M m =1 of p ositiv e inte gers, and any time sequence 0 < t 1 < · · · < t M < ∞ . That is, the finite dimensional distributions of the pro cess are determined by the function K . Le t T = { t 1 , . . . , t M } . W e note that Ξ T = P t ∈ T δ t ⊗ Ξ( t ) is a determinan tal (F ermion) p oin t pro cess on T × R with an op erator K giv en by K f ( s, x ) = P t ∈ T R R dy K ( s, x ; t, y ) f ( t, y ) for f ( t, · ) ∈ C 0 ( R ) , t ∈ T . The pro cess is then said to be determinantal w ith the c orr elation kernel K . When K is s ymmetric, Soshniko v [19] and Shira i and T ak ahashi [18] ga v e sufficien t conditions for K to b e a correlation k ernel of a determinan t a l p oint pro cess. Though suc h conditions a r e not kno wn f o r asymme tric cases, a v ariety of pro cesses, whic h are determinan tal with asymmetric correlation k ernels, ha v e b een studied. As men tioned ab ov e the pro ces s Ξ( t ) = P N j =1 δ X j ( t ) with the SD Es (1.1) with β = 2 s tarting from its equilibrium measure µ GUE N ,σ 2 is a n e xample [4]. The infinite particle system of Naga o and F orrester [15] is also determinan tal with the extended sine k ernel, whic h is asymmetric as shown b y (1 .3 ). (F or other examples , see, for instance, [21, 10].) In the presen t pap er w e first sho w that, for any fixed configuration ξ N ∈ M with ξ N ( R ) = N , Dyson’s mo del starting from ξ N is determinan tal and its correlation k ernel K ξ N is g iven by using the multiple Hermite p olynomials [8, 2, 7 ] (Prop osition 2.1). 3 F or ξ ∈ M , when K ξ ∩ [ − L,L ] con v erges to a con tinuous function as L → ∞ , the limit is written a s K ξ . If P ξ ∩ [ − L,L ] con v erges to a probabilit y measure P ξ on M [0 , ∞ ) , whic h is determinan tal with the correlation k ernel K ξ , w eakly in the sense of finite dimensional distributions as L → ∞ in the v ague top ology , w e sa y that the pro cess ( P ξ , Ξ( t ) , t ∈ [0 , ∞ )) is we l l define d with the c orr elation kernel K ξ . (The regularity of the sample paths of Ξ( t ) will b e discussed elsewhere [11].) In the case ξ ( R ) = ∞ , the pro cess ( P ξ , Ξ( t ) , t ∈ [0 , ∞ )) is Dyson’s mo del with an infinite num b er of particles. F or ξ ∈ M with ξ ( { x } ) ≤ 1 , ∀ x ∈ R , w e giv e sufficien t conditions so that the pro cess ( P ξ , Ξ( t ) , t ∈ [0 , ∞ )) is w ell defined, in whic h the correlation k ernel is generally express ed using a double in tegral with the heat k ernels of an entir e function represen ted b y a n infinite pro duct (Theorem 2.2). The configuration in which ev ery p oin t of Z is o ccupied by one particle, ξ Z ( · ) ≡ P ℓ ∈ Z δ ℓ ( · ), satisfies the conditio ns and w e will sho w that Dyson’s mo del starting from ξ Z is determinan tal with the k ernel K ξ Z ( s, x ; t, y ) = K sin ( t − s, y − x ) + 1 2 π Z | k |≤ π dk e k 2 ( t − s ) / 2+ ik ( y − x ) n ϑ 3 ( x − ik s, 2 π is ) − 1 o (1.5) = K sin ( t − s, y − x ) + X ℓ ∈ Z \{ 0 } e 2 π ixℓ − 2 π 2 sℓ 2 Z 1 0 du e π 2 u 2 ( t − s ) / 2 cos h π u { ( y − x ) − 2 π isℓ } i , s, t ≥ 0 , x, y ∈ R , where ϑ 3 is a v ersion of the Jacobi theta function defined by ϑ 3 ( v , τ ) = X ℓ ∈ Z e 2 π ivℓ + π iτ ℓ 2 , ℑ τ > 0 . (1.6) The lattice structure K ξ Z ( s, x + n ; t, y + n ) = K ξ Z ( s, x ; t, y ) , ∀ n ∈ Z , s, t ≥ 0 is clear in (1.5) b y the p erio dicity of ϑ 3 , ϑ 3 ( v + n, τ ) = ϑ 3 ( v , τ ) , ∀ n ∈ Z . W e can prov e lim u →∞ K ξ Z ( u + s, x ; u + t, y ) = K sin ( t − s, y − x ) , (1.7) whic h implies that µ sin is an attractor of Dyson’s mo del and ξ Z is in its basin. W e are intereste d in the contin uity of the pro cess with resp ect to initial configura- tion. F or Dyson’s mo del with finite part icles, the w eak c onv ergence of the pro ces ses ( P ξ N n , Ξ( t ) , t ∈ [0 , ∞ )) → ( P ξ N , Ξ( t ) , t ∈ [0 , ∞ )) as n → ∞ is guarantee d b y the v ague con v ergence of the initial configura t io ns ξ N n → ξ N as n → ∞ , where ξ N n , ξ N ∈ M with ξ N n ( R ) = ξ N ( R ) = N < ∞ , n ∈ N . Based o n this contin uity , Dyson’s mo del can b e defined for any initial configurations with finite particles, whic h can hav e m ultiple p oin ts (see Prop osition 2.1). On the other hand, we ha v e found that, if ξ ( R ) = ∞ , the w eak con vergence of pro ces ses in t he sens e of finite dimensional distributions cannot b e c oncluded fro m the conv ergence of initial configurations in the v ague top ology . In the presen t pa p er w e consider a stronger top ology for infinite-particle 4 configurations (Definition 2.3). W e introduce the space s Y κ m , κ ∈ ( 1 / 2 , 1) , m ∈ N of initial configurations suc h that t he con v ergence of pr o cesse s is g uaran teed b y t ha t of the initial configurations in this new top ology (Theorem 2.4). Note that the union of the spaces Y = S κ ∈ (1 / 2 , 1) S m ∈ N Y κ m is large enough to carry the P oisson p oint pro cess es, Gibbs states with regula r conditions, µ sin , as w ell as infi nite-particle configurat io ns with multiple points. In particular, using the fact µ sin ( Y ) = 1 and the contin uity with resp ect to the initial configurations, w e can pro v e that the pro cess ( P sin , Ξ( t ) , t ∈ [0 , ∞ ) ) of Nagao and F orrester, whic h is determinan tal with the extended sine k ernel (1.3), is Mark ovian [11]. The pa p er is or g anized as follows. In Section 2 preliminaries a nd main results are giv en. In Section 3 the definitions of some sp ecial functions used in the presen t pap er a re giv en and their basic prop erties are summarized. Section 4 is dev oted to pro ofs of results. 2 Preliminaries and Main Results F or ξ ( · ) = P j ∈ Λ δ x j ( · ) ∈ M , w e introduce t he fo llo wing op erations; (shift) f or u ∈ R , τ u ξ ( · ) = X j ∈ Λ δ x j + u ( · ), (dilatation) for c > 0 , c ◦ ξ ( · ) = X j ∈ Λ δ cx j ( · ), (square) ξ h 2 i ( · ) = X j ∈ Λ δ x 2 j ( · ). W e use the con v en tion suc h that Y x ∈ ξ f ( x ) = exp Z R ξ ( dx ) log f ( x ) = Y x ∈ supp ξ f ( x ) ξ ( { x } ) for ξ ∈ M a nd a function f on R , where supp ξ = { x ∈ R : ξ ( { x } ) > 0 } . F or a m ultiv ariate symmetric function g w e write g (( x ) x ∈ ξ ) for g (( x j ) j ∈ Λ ). F or s, t ∈ [0 , ∞ ), x, y ∈ R and ξ N ∈ M with ξ N ( R ) = N ∈ N , w e set K ξ N ( s, x ; t, y ) = 1 2 π i I Γ( ξ N ) dz p ( s, x | z ) Z R dy ′ p ( t, − iy | y ′ ) × 1 iy ′ − z Y x ′ ∈ ξ N 1 − iy ′ − z x ′ − z − 1 ( s > t ) p ( s − t, x | y ) , (2.1) where Γ( ξ N ) is a closed contour on the complex plane C encircling the po ints in supp ξ N on the real line R once in the p ositiv e direction. 5 Prop osition 2.1 Dyson ’s m o del ( P ξ N , Ξ( t ) , t ∈ [0 , ∞ )) , starting fr om any fixe d c o n - figur ation ξ N ∈ M with ξ N ( R ) = N < ∞ , is determinan tal with the c orr elation kernel K ξ N given by (2.1). W e put M 0 = n ξ ∈ M : ξ ( { x } ) ≤ 1 for an y x ∈ R o . Since any elemen t ξ of M 0 is determined uniquely b y it s supp o rt, it is iden tified with a coun table subse t { x j } j ∈ Λ of R . F or ξ N ∈ M 0 , a ∈ C , we in tro duce an entire function of z ∈ C Φ( ξ N , a, z ) = Y x ∈ ξ N ∩{ a } c 1 − z − a x − a , whose zero set is supp ( ξ N ∩ { a } c ) (see, for instance, [12]). Then, if ξ N ∈ M 0 , (2.1) is written as K ξ N ( s, x ; t, y ) = Z R ξ N ( dx ′ ) p ( s, x | x ′ ) Z R dy ′ p ( t, − iy | y ′ )Φ( ξ N , x ′ , iy ′ ) − 1 ( s > t ) p ( s − t, x | y ) . (2.2) F or L > 0 , α > 0 and ξ ∈ M w e put M ( ξ , L ) = Z [ − L,L ] \{ 0 } ξ ( dx ) x , M α ( ξ , L ) = Z [ − L,L ] \{ 0 } ξ ( dx ) | x | α 1 /α , and M ( ξ ) = lim L →∞ M ( ξ , L ) , M α ( ξ ) = lim L →∞ M α ( ξ , L ) , if the limits finitely exist. W e in tro duce the follo wing conditions: ( C.1 ) there exists C 0 > 0 suc h that | M ( ξ ) | < C 0 , ( C.2 ) (i) there exist α ∈ ( 1 , 2) and C 1 > 0 suc h that M α ( ξ ) ≤ C 1 , (ii) there exist β > 0 and C 2 > 0 suc h that M 1 ( τ − a 2 ξ h 2 i ) ≤ C 2 ( | a | ∨ 1) − β ∀ a ∈ supp ξ . W e denote b y X the set o f configurations ξ satisfying the conditions ( C.1 ) and ( C.2 ), and put X 0 = X ∩ M 0 . F or ξ ∈ X 0 , a ∈ R and z ∈ C w e define Φ( ξ , a, z ) = lim L →∞ Φ( ξ ∩ [ a − L, a + L ] , a, z ) . W e note that | Φ( ξ , a, z ) | < ∞ and Φ ( ξ , a, · ) 6≡ 0, if | M ( τ − a ξ ) | < ∞ and M 2 ( τ − a ξ ) < ∞ . 6 Theorem 2.2 If ξ ∈ X 0 , the pr o c ess ( P ξ , Ξ( t ) , t ∈ [0 , ∞ )) is wel l define d with the c orr elation kerne l given by K ξ ( s, x ; t, y ) = Z R ξ ( dx ′ ) p ( s, x | x ′ ) Z R dy ′ p ( t, − iy | y ′ )Φ( ξ , x ′ , iy ′ ) − 1 ( s > t ) p ( s − t, x | y ) . (2.3) In case ξ ( R ) = ∞ , Theorem 2.2 giv es Dyson’s mo del with an infinite num b er of particles starting from the configuration ξ ∈ X 0 . F rom (2.3) it is easy to c hec k that K ξ ( t, x ; t, y ) K ξ ( t, y ; t, x ) dxdy → ξ ( dx ) 1 ( x = y ) , t → 0 in the v ag ue to p ology . An in teresting and imp ortant example is obtained for the initial configuratio n, in whic h ev ery p oint in Z is o ccupied b y one particle, ξ Z ( · ) ≡ P ℓ ∈ Z δ ℓ ( · ). In this case ξ Z ( · ) ∈ X 0 and w e can show t ha t the correlation k ernel K ξ Z is giv en by (1.5). The pro cess ( P sin , Ξ( t ) , t ∈ [0 , ∞ )) is rev ersible with resp ect to µ sin . The result (1.7) implies that the pro cess ( P ξ Z , Ξ( u + t ) , t ∈ [0 , ∞ )) con v erges to ( P sin , Ξ( t ) , t ∈ [0 , ∞ )), as u → ∞ , w eakly in the sens e of finite dimensional distributions. In other w ords, ( P ξ Z , Ξ( t ) , t ∈ [0 , ∞ )) is the r elaxation pr o c ess fro m an initial configuration ξ Z to the in v ariant measure µ sin , whic h is determinan tal, and this non-equilibrium dynamics is completely determined via t he temp orally inhomogeneous correlation k ernel (1.5 ) . (See Remark in Section 4.3.) F or κ > 0, w e put g κ ( x ) = sgn( x ) | x | κ , x ∈ R , and η κ ( · ) = X ℓ ∈ Z δ g κ ( ℓ ) ( · ) . Since g κ is an o dd function, η κ satisfies ( C.1 ) for any κ > 0. F or an y κ > 1 / 2 w e can sho w b y simple calculation that η κ satisfies ( C.2 )(i) with an y α ∈ (1 /κ, 2) and some C 1 = C 1 ( α ) > 0 depending on α , and do es ( C.2 )(ii) with an y β ∈ (0 , 2 κ − 1) and some C 2 = C 2 ( β ) > 0 dep ending on β . This implies that η κ is an ele men t of X 0 in an y case κ > 1 / 2 . Note that η 1 = ξ Z . If there e xists β ′ < ( β − 1) ∧ ( β / 2) for ξ ∈ M 0 suc h that ♯ { x ∈ ξ : ξ ([ x − | x | β ′ , x + | x | β ′ ]) ≥ 2 } = ∞ , then ξ do es not satisfy the condition ( C.2 ) (ii). In o rder to include suc h initial configurat io ns as we ll as those with m ultiple p oin ts in our study of D yson’s mo del with an infinite num b er of particles, w e in tro duce another condition for configurations: ( C.3 ) there exists κ ∈ (1 / 2 , 1) and m ∈ N suc h that m ( ξ , κ ) ≡ max k ∈ Z ξ [ g κ ( k ) , g κ ( k + 1)] ≤ m. W e denote b y Y κ m the set of configurations ξ satisfying ( C.1 ) and ( C.3 ) with κ ∈ (1 / 2 , 1) and m ∈ N , and put Y = [ κ ∈ (1 / 2 , 1) [ m ∈ N Y κ m . 7 Noting tha t the set { ξ ∈ M : m ( ξ , κ ) ≤ m } is relativ ely compact for each κ ∈ ( 1 / 2 , 1) and m ∈ N , w e see t ha t Y is lo cally compact. W e in tro duce the follo wing top olog y on Y . Definition 2.3 Supp ose that ξ , ξ n ∈ Y , n ∈ N . We say that ξ n c onver ges Φ - mo der ately to ξ , if lim n →∞ Φ( ξ n , i, · ) = Φ( ξ , i, · ) uniformly on any c omp a ct s et o f C . (2.4) It is easy to see that (2.4) is satisfied, if ξ n con v erges to ξ v ag uely and the fo llo wing t w o conditions hold: lim L →∞ sup n> 0 Z [ − L,L ] c ξ n ( dx ) x = 0 , (2.5) lim L →∞ sup n> 0 Z [ − L,L ] c ξ h 2 i n ( dx ) x = 0 . (2.6) Note that for an y a ∈ R and z ∈ C lim n →∞ Φ( ξ n , a, z ) = Φ( ξ , a, z ) , (2.7) if ξ n con v erges Φ-mo derately to ξ and a / ∈ supp ξ . Then the second theorem of the presen t pap er is the f o llo wing. Theorem 2.4 (i) If ξ ∈ Y , ( P ξ , Ξ( t ) , t ∈ [0 , ∞ )) is w el l define d with a c orr elation kernel K ξ . In p articular, when ξ ∈ Y 0 ≡ Y ∩ M 0 , K ξ is given by (2.3). (ii) Supp os e that ξ , ξ n ∈ Y κ m , n ∈ N for some κ ∈ (1 / 2 , 1) and m ∈ N . If ξ n c onver ges Φ -mo der ately to ξ , then the pr o c ess ( P ξ n , Ξ( t ) , t ∈ [0 , ∞ )) c onver ges to the pr o c ess ( P ξ , Ξ( t ) , t ∈ [0 , ∞ )) we akly in the sense of finite dimensiona l distributions as n → ∞ in the va g ue top olo gy. In the pro of o f this theorem giv en in Section 4.4, w e will giv e an express ion ( 4 .26) to K ξ , whic h is v alid fo r a n y ξ ∈ Y . There we will use sp ecial functions suc h as the Hermite p olynomials, H k , k ∈ N 0 ≡ N ∪ { 0 } , the complete sym metric functions h k , k ∈ N 0 , and the Sc h ur functions s ( k | ℓ ) , k , ℓ ∈ N 0 . 3 Sp ecial F unction s 3.1 M ultiv ariate symmetric functions F or n ∈ N , let λ = ( λ 1 , λ 2 , . . . , λ n ) be a partition of length less than or equal to n , and δ = ( n − 1 , n − 2 , . . . , 1 , 0 ). F or x = ( x 1 , x 2 , . . . , x n ) consider t he sk ew-symmetric p olynomial a λ + δ ( x ) = det 1 ≤ j,k ≤ n x λ k + n − k j . 8 If λ = ∅ , it is the V andermonde determinan t, whic h is given b y the pro duct of difference of v ariables: a δ ( x ) = det 1 ≤ j,k ≤ n x n − k j = Y 1 ≤ j 0 suc h that ξ [ x 0 − ε, x 0 + ε ] = 0. W e see that for fixed z ∈ C Φ( ξ , x, z ) = Y u ∈ ξ − δ x 1 − z − x u − x = Y u ∈ ξ 1 − z − x 0 u − x 0 Y u ∈ ξ − δ x 1 1 − ( x − x 0 ) / ( u − x 0 ) = Φ( ξ , x 0 , z ) X r ∈ N 0 h r 1 u − x 0 u ∈ ξ ( x − x 0 ) r , where (3.3) ha s b een used. Then Φ( ξ , x, z ) is a smooth function of x on [ x 0 − ε, x 0 + ε ]. 3.2 M ultiple Hermite p olynomials F or a n y ξ ∈ M with ξ ( R ) < ∞ , the multiple Hermite p olynomial of typ e II , P ξ is defined as the monic p olynomial of degree ξ ( R ) that satisfies for any x ∈ supp ξ Z R dy P ξ ( y ) y j e − ( y − x ) 2 / 2 = 0 , j = 0 , . . . , ξ ( { x } ) − 1 . (3.4) The multiple Hermi te p olynomials of typ e I consist of a set of p olynomials n A ξ ( · , x ) : x ∈ supp ξ , deg A ξ ( · , x ) = ξ ( { x } ) − 1 o (3.5) suc h that the function Q ξ ( y ) = X x ∈ supp ξ A ξ ( y , x ) e − ( y − x ) 2 / 2 (3.6) satisfies Z R dy Q ξ ( y ) y j = 0 , j = 0 , . . . , ξ ( R ) − 2 1 , j = ξ ( R ) − 1 . (3.7) The p olynomials { A ξ ( · , x ) } are uniquely determined by the degree requiremen ts (3.5) and the orthogonality relations (3.7) [8]. The m ultiple Hermite p olynomial of t yp e I I, P ξ and the function Q ξ defined b y (3.6 ) hav e the follow ing in tegration represen tat io ns [2 ], P ξ ( y ) = Z R dy ′ e − ( y ′ + iy ) 2 / 2 √ 2 π Y x ∈ ξ ( iy ′ − x ) , Q ξ ( y ) = 1 2 π i I Γ( ξ ) dz e − ( z − y ) 2 / 2 √ 2 π 1 Q x ∈ ξ ( z − x ) . (3.8) 10 No w we fix ξ N ∈ M with ξ N ( R ) = N ∈ N . W e write ξ N ( · ) = P N j =1 δ x j ( · ) with a lab eled configuration x = ( x j ) N j =1 suc h that x 1 ≤ x 2 ≤ · · · ≤ x N . Then w e define ξ N 0 ( · ) ≡ 0 and ξ N j ( · ) = j X k =1 δ x k ( · ) , 1 ≤ j ≤ N . By definition ξ N j ( R ) = j, 0 ≤ j ≤ N and ξ N j ( { x } ) ≤ ξ N j +1 ( { x } ) , ∀ x ∈ R , 0 ≤ j ≤ N − 1. W e define H ( − ) j ( y ; ξ N ) = P ξ N j ( y ) , H (+) j ( y ; ξ N ) = Q ξ N j +1 ( y ) , 0 ≤ j ≤ N − 1 . (3.9) By the orthogonality relations (3.4), (3.7) and the ab ov e definitions, w e can pro v e the biorthonormality [2] Z R dy H ( − ) j ( y ; ξ N ) H (+) k ( y ; ξ N ) = δ j k , 0 ≤ j, k ≤ N − 1 . (3.10) F or N ∈ N , let W N = { x ∈ R N : x 1 < x 2 < · · · < x N } , the W eyl c hamber o f type A N − 1 . Lemma 3.1 L et y = ( y j ) N j =1 ∈ W N . F or an y ξ N ( · ) = P N j =1 δ x j ( · ) ∈ M with a lab ele d c onfigur ation x = ( x j ) N j =1 such that x 1 ≤ x 2 ≤ · · · ≤ x N , 1 a δ ( x ) det 1 ≤ j,k ≤ N h e − ( y k − x j ) 2 / 2 i = ( − 1) N ( N − 1) / 2 (2 π ) N/ 2 det 1 ≤ j,k ≤ N h H (+) j − 1 ( y k ; ξ N ) i . (3.11) Her e when s o me of the x j ’s c oincide, we interpr et the LHS using l ’ Hˆ opital’s rule. Pr o o f. F ir st we assume ξ N ∈ M 0 . Since a δ ( x ) = ( − 1) N ( N − 1) / 2 Q N j =2 Q j − 1 m =1 ( x j − x m ), b y the multiline arity of determinan t 1 a δ ( x ) det 1 ≤ j,k ≤ N h e − ( y k − x j ) 2 / 2 i = ( − 1) N ( N − 1) / 2 (2 π ) N/ 2 det 1 ≤ j,k ≤ N " e − ( y k − x j ) 2 / 2 √ 2 π 1 Q j − 1 m =1 ( x j − x m ) # = ( − 1) N ( N − 1) / 2 (2 π ) N/ 2 det 1 ≤ j,k ≤ N " j X ℓ =1 e − ( y k − x ℓ ) 2 / 2 √ 2 π 1 Q 1 ≤ m ≤ j,m 6 = ℓ ( x ℓ − x m ) # . By definition (3.9) with (3.8), if ξ N ∈ M 0 , ξ N ( R ) = N , H (+) j − 1 ( y k ; ξ N ) = 1 2 π i I Γ( ξ N j ) dz e − ( y k − z ) 2 / 2 √ 2 π 1 Q x ∈ ξ N j ( z − x ) (3.12) = 1 2 π i I Γ( ξ N j ) dz e − ( y k − z ) 2 / 2 √ 2 π 1 Q j ℓ =1 ( z − x ℓ ) = j X ℓ =1 e − ( y k − x ℓ ) 2 / 2 √ 2 π 1 Q 1 ≤ m ≤ j,m 6 = ℓ ( x ℓ − x m ) , 1 ≤ j ≤ N . 11 Then (3.11) is prov ed for ξ N ∈ M 0 . When some of the x j ’s coincide, the LHS of (3.11) is in terpreted using l’Hˆ opital’s rule and in the R HS of (3.11) H (+) j − 1 ( y k ; ξ N ) should b e giv en by (3.12). Then (3.11) is v alid for an y ξ N ∈ M , ξ N ( R ) = N . Lemma 3.2 L et N ∈ N , ξ N ∈ M wi th ξ N ( R ) = N . F or 0 ≤ s ≤ t, x, y ∈ R , 0 ≤ j ≤ N − 1 , Z R dy H ( − ) j y √ t ; 1 √ t ◦ ξ N p ( t − s, y | x ) = s t j / 2 H ( − ) j x √ s ; 1 √ s ◦ ξ N , (3.13) Z R dx p ( t − s, y | x ) H (+) j x √ s ; 1 √ s ◦ ξ N = s t ( j +1) / 2 H (+) j y √ t ; 1 √ t ◦ ξ N , (3.14) wher e p i s the he at kernel (1.4). Pr o o f. Consider the in tegral Z R dy H ( − ) j y √ t ; 1 √ t ◦ ξ N p ( t − s, y | x ) = 1 p 2 π ( t − s ) 1 √ 2 π Z R dy ′ Y x ∈ ξ N j iy ′ − x √ t Z R dy e − ( y − x ) 2 / { 2( t − s ) }− ( y ′ + iy / √ t ) 2 / 2 = r t s 1 √ 2 π Z R dy ′ Y x ∈ ξ N j iy ′ − x √ t e − t ( y ′ + ix/ √ t ) 2 / (2 s ) . Change the integral v a r ia ble y ′ → y ′ p t/s to obta in the equalit y (3 .1 3). Similar calculation giv es (3.14 ). When ξ N ( · ) = N δ 0 ( · ), H ( − ) j ( y ; N δ 0 ) = 2 − j / 2 H j ( y / √ 2) , H (+) j ( y ; N δ 0 ) = 2 − j / 2 j ! √ 2 π H j ( y / √ 2) e − y 2 / 2 , 0 ≤ j ≤ N − 1 , where H j ( x ) is the Hermite p olynomial of degree j , H j ( x ) = j ! [ j / 2] X k =0 ( − 1) k (2 x ) j − 2 k k !( j − 2 k )! = 2 j / 2 Z R dy e − y 2 / 2 √ 2 π ( iy + √ 2 x ) j = j ! 2 π i I Γ( δ 0 ) dz e 2 z x − z 2 z j +1 . (3.15) 12 The last expression (3.15) implies tha t the generating f unction of the Hermite p oly- nomials is giv en by e 2 z x − z 2 = X j ∈ N 0 z j j ! H j ( x ) . (3.16) 4 Pro ofs of Results 4.1 Pr o of of Prop osition 2.1 F or x , y ∈ W N and t > 0, consider the Karlin - McGr e gor determinan t of the heat k ernel (1.4) [9] f N ( t, y | x ) = det 1 ≤ j,k ≤ N h p ( t, y j | x k ) i . If ξ N ∈ M 0 with ξ N ( R ) = N ∈ N , ξ N can be iden tified with a set x ∈ W N . F or an y M ≥ 1 and any time sequence 0 < t 1 < · · · < t M < ∞ , the multitime pr ob ability density of Dyson’s mo del is giv en by [6, 10] p ξ N t 1 , ξ (1) ; . . . ; t M , ξ ( M ) = a δ ( x ( M ) ) M − 1 Y m =1 f N ( t m +1 − t m , x ( m +1) | x ( m ) ) f N ( t 1 , x (1) | x ) 1 a δ ( x ) , where ξ ( m ) ( · ) = P N j =1 δ x ( m ) j ( · ), 1 ≤ m ≤ M . Define φ ( − ) j ( t, x ; ξ N ) ≡ t j / 2 H ( − ) j x √ t ; 1 √ t ◦ ξ N , φ (+) j ( t, x ; ξ N ) ≡ t − ( j + 1) / 2 H (+) j x √ t ; 1 √ t ◦ ξ N , 0 ≤ j ≤ N − 1 , t > 0 , x ∈ R . F rom the biorthonormalit y (3 .1 0) of the m ultiple Hermite p olynomials and Lemma 3.2 , the following relations are deriv ed. Lemma 4.1 F or ξ N ∈ M with ξ N ( R ) = N ∈ N , 0 ≤ t 1 ≤ t 2 , Z R dx 2 φ ( − ) j ( t 2 , x 2 ; ξ N ) p ( t 2 − t 1 , x 2 | x 1 ) = φ ( − ) j ( t 1 , x 1 ; ξ N ) , 0 ≤ j ≤ N − 1 , Z R dx 1 p ( t 2 − t 1 , x 2 | x 1 ) φ (+) j ( t 1 , x 1 ; ξ N ) = φ (+) j ( t 2 , x 2 ; ξ N ) , 0 ≤ j ≤ N − 1 , Z R dx 1 Z R dx 2 φ ( − ) j ( t 2 , x 2 ; ξ N ) p ( t 2 − t 1 , x 2 | x 1 ) φ (+) k ( t 1 , x 1 ; ξ N ) = δ j k , 0 ≤ j, k ≤ N − 1 . 13 Put µ ( ± ) ( t, x ; ξ N ) = det 1 ≤ j,k ≤ N h φ ( ± ) j − 1 ( t, x k ; ξ N ) i . Since H ( − ) j is a monic p olynomial of degree j , µ ( − ) ( t, x ; ξ N ) = ( − 1) N ( N − 1) / 2 a δ ( x ). By Lemma 3.1 , f N ( t 1 , x (1) | x ) /a δ ( x ) will b e replaced b y ( − 1) N ( N − 1) / 2 µ (+) ( t 1 , x (1) ; ξ N ) t o extend the expression to the case ξ N ∈ M . Then the m ultitime pro ba bilit y densit y of Dyson’s mo del is expressed as p ξ N t 1 , ξ (1) ; . . . ; t M , ξ ( M ) = µ ( − ) ( t M , x ( M ) ; ξ N ) M − 1 Y m =1 f N ( t m +1 − t m ; x ( m +1) | x ( m ) ) µ (+) ( t 1 , x (1) ; ξ N ) (4.1) for ξ N ∈ M with ξ N ( R ) = N ∈ N . F or x = ( x 1 , . . . , x N ) with ξ ( · ) = P N j =1 δ x j ( · ) and N ′ ∈ { 1 , 2 , . . . , N } , w e put x N ′ = ( x 1 , . . . , x N ′ ). F or a s equence ( N m ) M m =1 of p ositive in tegers less tha n or equal to N , w e obtain t he ( N 1 , . . . , N M )- multitime c orr elation function b y ρ ξ N N t 1 , x (1) N 1 ; . . . ; t M , x ( M ) N M = Z Q M m =1 R N − N m p ξ N t 1 , ξ (1) ; . . . ; t M , ξ ( M ) M Y m =1 1 ( N − N m )! N Y j = N m +1 dx ( m ) j . (4.2) F or f = ( f 1 , · · · , f M ) ∈ C 0 ( R ) M , and θ = ( θ 1 , · · · , θ M ) ∈ R M , the generating function for m ultitime correlation functions is giv en as G ξ N [ χ ] = E ξ N " exp ( M X m =1 θ m N X j m =1 f m ( X j m ( t m )) )# = N X N 1 =0 · · · N X N M =0 M Y m =1 1 N m ! Z R N 1 N 1 Y j =1 dx (1) j · · · Z R N M N M Y j =1 dx ( M ) j × M Y m =1 N m Y j =1 χ m x ( m ) j ρ ξ N t 1 , x (1) N 1 ; . . . ; t M , x ( M ) N M , where χ m ( x ) = e θ m f m ( x ) − 1 , 1 ≤ m ≤ M . By the argumen t giv en in Section 4.2 in [10], the expres sion (4 .1) with Lemma 4.1 leads to the F redholm determinan tal expres sion for the generating function, G ξ N [ χ ] = Det h δ mn δ ( x − y ) + e S m,n ( x, y ; ξ N ) χ n ( y ) i , where e S m,n ( x, y ; ξ N ) = S m,n ( x, y ; ξ N ) − 1 ( m > n ) p ( t m − t n , x | y ) 14 with S m,n ( x, y ; ξ N ) = N − 1 X j =0 φ (+) j ( t m , x ; ξ N ) φ ( − ) j ( t n , y ; ξ N ) = 1 √ t m N − 1 X j =0 t n t m j / 2 H (+) j x √ t m ; 1 √ t m ◦ ξ N H ( − ) j y √ t n ; 1 √ t n ◦ ξ N . Here the F redholm determinan t is expanded as Det h δ mn δ ( x − y ) + e S m,n ( x, y ; ξ N ) χ n ( y ) i = N X N 1 =0 · · · N X N M =0 M Y m =1 1 N m ! Z R N 1 N 1 Y j =1 dx (1) j · · · Z R N M N M Y j =1 dx ( M ) j × M Y m =1 N m Y j =1 χ m x ( m ) j det 1 ≤ j ≤ N m , 1 ≤ k ≤ N n 1 ≤ m,n ≤ M " e S m,n ( x ( m ) j , x ( n ) k ; ξ N ) # . Pr o o f o f Pr op osition 2.1. Inserting the in tegral form ulas f o r H ( ± ) j , the ke rnel S m,n is written as S m,n ( x, y ; ξ N ) = 1 √ t m 1 2 π i I Γ( t − 1 / 2 m ◦ ξ N ) dz e − ( z − x/ √ t m ) 2 / 2 √ 2 π Z R dy ′ e − ( y ′ + iy / √ t n ) 2 / 2 √ 2 π × N − 1 X k =0 t n t m k / 2 Q k ℓ =1 ( iy ′ − x ℓ / √ t n ) Q k +1 ℓ =1 ( z − x ℓ / √ t m ) = 1 2 π i I Γ( t − 1 / 2 m ◦ ξ N ) dz e − ( z − x/ √ t m ) 2 / 2 √ 2 π Z R dy ′ e − ( y ′ + iy / √ t n ) 2 / 2 √ 2 π × N − 1 X k =0 Q k ℓ =1 ( i √ t n y ′ − x ℓ ) Q k +1 ℓ =1 ( √ t m z − x ℓ ) . F or z 1 , z 2 ∈ C with z 1 / ∈ { x 1 , . . . , x N } , the follo wing iden tity holds, N − 1 X k =0 Q k ℓ =1 ( z 2 − x ℓ ) Q k +1 ℓ =1 ( z 1 − x ℓ ) = 1 z 1 − x 1 + z 2 − x 1 ( z 1 − x 1 )( z 1 − x 2 ) + · · · + ( z 2 − x 1 )( z 2 − x 2 ) · · · ( z 2 − x N − 1 ) ( z 1 − x 1 )( z 1 − x 2 ) · · · ( z 1 − x N ) = N Y ℓ =1 z 2 − x ℓ z 1 − x ℓ − 1 ! 1 z 2 − z 1 . 15 By this iden tit y , w e hav e S m,n ( x, y ; ξ N ) = 1 2 π i I Γ( t − 1 / 2 m ◦ ξ N ) dz e − ( z − x/ √ t m ) 2 / 2 √ 2 π Z R dy ′ e − ( y ′ + iy / √ t n ) 2 / 2 √ 2 π × N Y ℓ =1 i √ t n y ′ − x ℓ √ t m z − x ℓ − 1 ! 1 i √ t n y ′ − √ t m z . Note that 1 2 π i I Γ( t − 1 / 2 m ◦ ξ N ) dz e − ( z − x/ √ t m ) 2 / 2 √ 2 π Z R dy ′ e − ( y ′ + iy / √ t n ) 2 / 2 √ 2 π 1 i √ t n y ′ − √ t m z = 1 2 π i I Γ( t − 1 / 2 m ◦ ξ N ) dz e − ( z − x/ √ t m ) 2 / 2 √ 2 π Z R dy ′ e − ( y ′ + iy / √ t n ) 2 / 2 √ 2 π 1 i √ t n y ′ X j ∈ N 0 r t m t n z iy ′ j = 0 . By ch anging the in tegral v ariables appropriately , we find that e S m,n ( x, y ; ξ N ) is equal to (2.1) with s = t m , t = t n . This completes the pro of. 4.2 Pr o of of Theorem 2.2 In this subsection w e giv e a pro of of The orem 2.2. First w e prov e some lemmas. Lemma 4.2 If M α ( ξ ) < ∞ fo r some α ∈ (1 , 2) , then α X L ∈ N M 1 ( ξ , L ) α/ ( α − 1) L ( L + 1) α ≤ M α ( ξ ) α 2 / ( α − 1) . Pr o o f. By H¨ older’s inequalit y w e ha v e M 1 ( ξ , L ) = Z 0 < | x |≤ L ξ ( dx ) | x | ≤ M α ( ξ ) ξ [ − L, L ] \ { 0 } ( α − 1) /α . On the other hand M α ( ξ ) α = X L ∈ N Z L − 1 < | x |≤ L ξ ( dx ) | x | α ≥ X L ∈ N L − α ξ [ − L, L ] \ { 0 } − ξ [ − L + 1 , L − 1] \ { 0 } = X L ∈ N n L − α − ( L + 1) − α o ξ [ − L, L ] \ { 0 } ≥ α X L ∈ N ξ [ − L, L ] \ { 0 } L ( L + 1) α . 16 F rom the ab ov e inequalities we ha v e M α ( ξ ) α ≥ α X L ∈ N 1 L ( L + 1) α M 1 ( ξ , L ) M α ( ξ ) α/ ( α − 1) . Lemma 4.2 is deriv ed from this inequality , since α + α/ ( α − 1) = α 2 / ( α − 1). Lemma 4.3 L et α ∈ (1 , 2) an d δ > α − 1 . Supp ose that M α ( ξ ) < ∞ and put L 0 = L 0 ( α, δ, ξ ) = (2 M α ( ξ )) α/ ( δ − α +1) . Then M 1 ( ξ , L ) ≤ L δ , L ≥ L 0 . Pr o o f. Supp o se that L 1 ∈ N satisfies M 1 ( ξ , L 1 ) > L δ 1 . Then α X L ∈ N M 1 ( ξ , L ) α/ ( α − 1) L ( L + 1) α > α ∞ X L = L 1 L αδ/ ( α − 1) 1 L ( L + 1) α > α L αδ/ ( α − 1) 1 Z ∞ L 1 +1 dy y − ( α +1) = L αδ/ ( α − 1) 1 ( L 1 + 1) − α = L 1 L 1 + 1 α L α ( δ − α +1) / ( α − 1) 1 . F rom Lemma 4.2 w e hav e L 1 L 1 + 1 α L α ( δ − α +1) / ( α − 1) 1 ≤ M α ( ξ ) α 2 / ( α − 1) . Hence L 1 < L 1 + 1 L 1 ( α − 1) / ( δ − α +1) M α ( ξ ) α/ ( δ − α +1) < (2 M α ( ξ )) α/ ( δ − α +1) . This completes the pro of. The follow ing lemma will play an import an t role in the pro of of Theorem 2.2 . Lemma 4.4 F or any ξ ∈ X 0 , ther e exist C 3 = C 3 ( α, β , C 0 , C 1 , C 2 ) > 0 and θ ∈ ( α ∨ (2 − β ) , 2) such that | Φ( ξ , a, iy ) | ≤ exp h C 3 n ( | y | θ ∨ 1 ) + ( | a | θ ∨ 1 ) oi ∀ y ∈ R , ∀ a ∈ supp ξ . Pr o o f. F ir st w e estimate the entire function Φ( ξ , a, z ) , z ∈ C , in the case that a = 0 ∈ supp ξ . In case 2 | z | < | x | , b y using the expansion log 1 + z x = X k ∈ N ( − 1) k − 1 k z x k , 17 w e hav e Z 2 | z | < | x | ξ ( dx ) log 1 + z x = Z 2 | z | < | x | ξ ( dx ) X k ∈ N ( − 1) k − 1 k z x k = Z 2 | z | < | x | ξ ( dx ) z x + Z 2 | z | < | x | ξ ( dx ) z x 2 ∞ X k =2 ( − 1) k − 1 k z x k − 2 . Since Z 2 | z | < | x | ξ ( dx ) z x ≤ | M ( ξ ) || z | + M 1 ( ξ , 2 | z | ) | z | , and Z 2 | z | < | x | ξ ( dx ) z x 2 ∞ X k =2 ( − 1) k − 1 k z x k − 2 ≤ Z 2 | z | < | x | ξ ( dx ) | z | 2 | x | 2 1 2 ∞ X k =2 2 2 − k = Z 2 | z | < | x | ξ ( dx ) | z | 2 | x | 2 ≤ M α ( ξ ) α | z | α , w e hav e Y x ∈ ξ n 1 + 1 ( | x | > 2 | z | ) z x o ≤ exp n | M ( ξ ) || z | + M 1 ( ξ , 2 | z | ) | z | + M α ( ξ ) α | z | α o . (4.3 ) On the other hand w e hav e Y x ∈ ξ n 1 + 1 (0 < | x | ≤ 2 | z | ) z x o ≤ exp Z [ − 2 | z | , 2 | z | ] \{ 0 } ξ ( dx ) | x | | z | = exp n M 1 ( ξ , 2 | z | ) | z | o . (4.4) Com bining the ab o v e t w o inequalities (4 .3) and (4.4), w e obtain Y x ∈ ξ ∩{ 0 } c 1 + z x ≤ exp n | M ( ξ ) || z | + 2 M 1 ( ξ , 2 | z | ) | z | + M α ( ξ ) α | z | α o . By the conditions ( C.1 ), ( C.2 )(i) and Lemma 4.3 , we ha ve | M ( ξ ) || z | + 2 M 1 ( ξ , 2 | z | ) | z | + M α ( ξ ) α | z | α ≤ C 0 | z | + 4 | z | 1+ δ + C 1 | z | α for | z | ≤ L 0 ( α, δ, C 1 ) with δ > α − 1. Hence, if w e can ta k e θ > α , then | Φ( ξ , 0 , z ) | ≤ exp h C ( | z | θ ∨ 1 ) i (4.5) with a p ositiv e constan t C , whic h dep ends o n only α, β , C 0 and C 1 . 18 Next w e estimate the case that a 6 = 0 by using the follo wing equations: Φ( ξ , a, z ) = Φ( ξ , 0 , z )Φ( ξ ∩ { 0 } c , a, 0) z a ξ ( { 0 } ) a a − z and Φ( ξ ∩ { 0 } c , a, 0) = Φ( ξ ∩ {− a } c , 0 , − a )Φ( ξ h 2 i ∩ { 0 } c , a 2 , 0)2 1 − ξ ( {− a } ) , where a ∈ supp ξ . F rom the ab o v e estim ate (4.5) w e hav e | Φ( ξ ∩ {− a } c , 0 , − a ) | ≤ exp h C ( | a | θ ∨ 1 ) i . Since | ( iy /a ) ξ ( { 0 } ) a/ ( a − iy ) | ≤ 1 , it is enough to sho w the estimate Φ( ξ h 2 i ∩ { 0 } c , a 2 , 0) ≤ exp n 3 C 2 | a | 2 − β o for pro ving this lemma. W e hav e Z 2 a 2 < | x − a 2 | ξ h 2 i ( dx ) log 1 + a 2 x − a 2 = Z 2 a 2 < | x − a 2 | ξ h 2 i ( dx ) a 2 x − a 2 X k ∈ N ( − 1) k k a 2 x − a 2 k − 1 ≤ 2 Z 2 a 2 < | x − a 2 | ξ h 2 i ( dx ) a 2 x − a 2 ≤ 2 M 1 ( τ − a 2 ξ h 2 i ) a 2 . On the other hand w e see Y x ∈ ξ h 2 i 1 + 1 (0 < | x − a 2 | < 2 a 2 ) a 2 x − a 2 ≤ exp Z [ − 2 a 2 , 2 a 2 ] \{ 0 } ( τ − a 2 ξ h 2 i )( dx ) | x | a 2 = exp n M 1 ( τ − a 2 ξ h 2 i , 2 a 2 ) a 2 o . Then Φ( ξ h 2 i ∩ { 0 } c , a 2 , 0) = Y x ∈ ξ h 2 i ∩{ 0 ,a 2 } c 1 + a 2 x − a 2 ≤ exp n 3 M 1 ( τ − a 2 ξ h 2 i ) a 2 o = exp n 3 C 2 | a | 2 − β o . This completes the pro of. Pr o o f of The or e m 2.2. Note that ξ ∩ [ − L, L ], L > 0 and ξ satisfy ( C.1 ) and ( C.2 ) with the same cons tants C 0 , C 1 , C 2 and indices α, β . By virtue of Lemma 4.4 w e s ee that there exists C 3 > 0 suc h that | Φ( ξ ∩ [ − L, L ] , a, iy ) | ≤ exp h C 3 n | y | θ + ( | a | θ ∨ 1) oi , 19 ∀ L > 0 , ∀ a ∈ supp ξ , ∀ y ∈ R . Sin ce f o r an y y ∈ R Φ( ξ ∩ [ − L, L ] , a, iy ) → Φ( ξ , a, iy ) , L → ∞ , w e can apply Leb esgue’s conv ergence theorem to (2.2) and obtain lim L →∞ K ξ ∩ [ − L,L ] ( s, x ; t, y ) = K ξ ( s, x ; t, y ) . Since for an y ( s, t ) ∈ (0 , ∞ ) 2 and an y compact in terv a l I ⊂ R sup x,y ∈ I K ξ ∩ [ − L,L ] ( s, x ; t, y ) < ∞ , w e can obtain the con v ergence of generating functions for mu ltitime correlation functions; G ξ ∩ [ − L,L ] [ χ ] → G ξ [ χ ] as L → ∞ . It implies P ξ ∩ [ − L,L ] → P ξ as L → ∞ in the sense of finite dimensional distributions and t he pro of is completed. 4.3 Pr o ofs of (1.5) and ( 1.7) Pr o o f of (1.5). Since ξ Z = η 1 ∈ X 0 , w e can start fro m the expression of the correla- tion k ernel (2.3) in Theorem 2 .2. F or ℓ ∈ Z , z ∈ C Φ( ξ Z , ℓ, z ) = Y j ∈ Z ,j 6 = ℓ 1 − z − ℓ j − ℓ = sin { π ( z − ℓ ) } π ( z − ℓ ) = 1 2 π Z | k |≤ π dk e ik ( z − ℓ ) , since Q n ∈ N (1 − x 2 /n 2 ) = sin( π x ) / ( π x ). Then K ξ Z ( s, x ; t, y ) + 1 ( s > t ) p ( s − t, x | y ) = X ℓ ∈ Z p ( s, x | ℓ ) I ( t, y , ℓ ) , (4.6) where I ( t, y , ℓ ) = Z R dy ′ p ( t, − iy | y ′ ) 1 2 π Z | k |≤ π dk e ik ( iy ′ − ℓ ) = 1 2 π Z | k |≤ π dk e k 2 t/ 2+ ik ( y − ℓ ) . By definition (1.6) of ϑ 3 , w e can rewrite (4.6) as 1 2 π Z | k |≤ π dk e k 2 ( t − s ) / 2+ ik ( y − x ) × ϑ 3 1 2 π is ( x − ik s ) , − 1 2 π is e − π i ( x − ik s ) 2 / (2 πis ) r i 2 π is . 20 Use the functional equation satisfied by ϑ 3 ( v , τ ) (see, for example, Section 10.12 in [1]), ϑ 3 ( v , τ ) = ϑ 3 v τ , − 1 τ e − π iv 2 /τ r i τ , and the in tegral represen tation of the heat k ernel (1.4). Then (1.5) is obtained. Pr o o f of (1.7). By the definition (1.6) of ϑ 3 , for s, t, u > 0 K ξ Z ( u + s, x ; u + t, y ) − K sin ( t − s, y − x ) = e − 2 π ix 2 π Z | k |≤ π dk e k 2 ( t − s ) / 2+ ik ( y − x ) − 2 π ( u + s )( π + k ) + e 2 π ix 2 π Z | k |≤ π dk e k 2 ( t − s ) / 2+ ik ( y − x ) − 2 π ( u + s )( π − k ) + X ℓ ∈ Z \{− 1 , 0 , 1 } e 2 π ixℓ 2 π Z | k |≤ π dk e k 2 ( t − s ) / 2+ ik ( y − x ) − 2 π ( u + s ) ℓ ( ℓπ − k ) . Then w e see for an y u > 0 K ξ Z ( u + s, x ; u + t, y ) − K sin ( t − s, y − x ) ≤ e π 2 ( t − s ) / 2 ∨ 1 ( 1 π Z | k |≤ π dk e − 2 π ( u + s )( π + k ) + 2 X ℓ ≥ 2 e − 2 π 2 ( u + s ) ℓ ) = e π 2 ( t − s ) / 2 ∨ 1 ( 1 − e − 4 π 2 ( u + s ) 2 π 2 ( u + s ) + 2 e − 4 π 2 ( u + s ) 1 − e − 2 π 2 ( u + s ) ) ≤ C u , where C > 0 dep ends on t a nd s , but do es not on u . This completes the pro of o f (1.7). Remark Since this relaxation pro ces s ( P ξ Z , Ξ( t ) , t ∈ [0 , ∞ )) is determinan tal with K ξ Z , at any in termediate time 0 < t < ∞ the particle distribution on R is the determinan tal p oint pro cess with the spatial corr elat io n k ernel K ξ Z ( x, t ; y , t ) , x, y ∈ R . It should b e noted that this spatial correlation k ernel is not symmetric, K ξ Z ( t, x ; t, y ) = X ℓ ∈ Z e 2 π ixℓ − 2 π 2 tℓ 2 sin h π { ( y − x ) − 2 π itℓ } i π { ( y − x ) − 2 π itℓ } , x, y ∈ R , 0 < t < ∞ . 21 4.4 Pr o of of Theorem 2.4 In this subsection w e pro v e Theorem 2.4. Supp ose ξ ∈ Y κ m ⊂ Y . F or k ∈ Z w e can tak e b k and b k suc h that b − k − 1 = − b k , b − k − 1 = − b k , b k , b k ⊂ ( g κ ( k ) , g κ ( k + 1)) , b k − b k ≥ g κ ( k + 1) − g κ ( k ) 2 m ( ξ , κ ) + 1 , ξ b k , b k = 0 and ξ ( b k − 1 + b k ) / 2 = 0 . W e put I k = b k , b k , ε k = | I k | = b k − b k , c k = ( b k − 1 + b k ) / 2, and ∆ k = ( b k − b k − 1 ) / 2. Note that [ b − k − 1 , b − k ] = − [ b k − 1 , b k ], I − k − 1 = − I k , ε − k − 1 = ε k , k ∈ N 0 . Then we define the k -th cluster in the configuratio n ξ b y C k = ξ ∩ [ b k − 1 , b k ] . It is easy to see that P k ∈ Z C k = ξ , and for eac h k ∈ Z | C k | ≡ C k ( R ) = ξ ([ b k − 1 , b k ]) ≤ 2 m ( ξ , κ ) , (4.7) | x − y | ≥ ε k − 1 ∧ ε k , x ∈ supp C k , y ∈ supp ( ξ − C k ) . (4.8) Let v k = ( v k ℓ ) | C k | ℓ =1 b e the increasing sequence with P | C k | ℓ =1 δ v kℓ = C k . See Figure 1. F or a ∈ supp ξ , w e denote b y C a the cluster containing a . Remark that, when ξ n con v erges t o ξ v aguely as n → ∞ , w e can tak e the k -th cluster C k ( ξ n ) of ξ n so that it con v erges to the k - th cluster C k ( ξ ) of ξ v aguely a s n → ∞ . g κ ( k − 1 ) g κ ( k ) g κ ( k + 1 ) I k − 1 I k I k +1 v k 1 v k 2 v k 3 v k +1 1 v k +1 2 v k +1 3 ∆ k ∆ k +1 ε k − 1 ε k +1 C k +1 C k b k − 1 b k +1 c k b k − 1 b k +1 ∆ k ∆ k ∆ k +1 b k b k c k +1 ε k Figure 1: The clusters W e in tro duce C -v alued functions Ψ k ( t, ξ , z , x ), k ∈ Z , t ≥ 0, ξ ∈ Y , z ∈ C , 22 x ∈ R , Ψ k ( t, ξ , z , x ) = Φ( ξ − C k , c k , z ) | C k | X ℓ =1 ( z − c k ) ℓ − 1 ( − 1) | C k |− ℓ − 1 × Θ k ,ℓ ( t, ξ , x ) + ∞ X q = | C k | Θ k ,q ( t, ξ , x ) s ( q − | C k ||| C k |− ℓ − 1) ( v k − c k ) , (4.9) if | C k | 6 = 0, and Ψ k ( t, ξ , z ) = 0, otherwise, where s ( k | ℓ ) is the Sc h ur function associated with the partition ( k | ℓ ) in F ro b enius’ notation, and Θ k ,q ( t, ξ , x ) = q X r =0 1 ( q − r )! − 1 √ 2 t q − r H q − r c k − x √ 2 t h r 1 u − c k u ∈ ξ − C k ! (4.10) with the Hermite p olynomials H k , k ∈ N 0 , and with the complete symm etric f unc- tions h k , k ∈ N 0 . Lemma 4.5 Supp ose that ξ ∈ Y 0 . Then for k ∈ Z , t ≥ 0 , x ∈ R , z ∈ C Z R C k ( dx ′ ) e − ( x ′ − x ) 2 / (2 t ) Φ( ξ , x ′ , z ) = e − ( c k − x ) 2 / (2 t ) Ψ k ( t, ξ , z , x ) . Pr o o f. F rom definitions of C k , k ∈ Z and Φ, w e hav e Z R C k ( dx ′ ) e − ( x ′ − x ) 2 / (2 t ) Φ( ξ , x ′ , z ) = Z R C k ( dx ′ ) e − ( x ′ − x ) 2 / (2 t ) Y u ∈ ξ − C k z − u x ′ − u Y v ∈ C k − δ x ′ z − v x ′ − v = e − ( c k − x ) 2 / (2 t ) Z R C k ( dx ′ ) e − ( x ′ − c k )( x ′ + c k − 2 x ) / (2 t ) × Y u ∈ ξ − C k ( z − c k ) − ( u − c k ) ( x ′ − c k ) − ( u − c k ) Y v ∈ C k − δ x ′ ( z − c k ) − ( v − c k ) ( x ′ − c k ) − ( v − c k ) = e − ( c k − x ) 2 / (2 t ) | C k | X j =1 ψ k ( t, ξ , v k j − c k , z , x ) a δ ( v k − c k ; j ; z − c k ) a δ ( v k − c k ) , where a δ ( x m ; j ; y ) = a δ ( x 1 , . . . , x j − 1 , y , x j +1 , . . . , x m ) , and ψ k ( t, ξ , x ′ , z , x ) = Φ( ξ − C k , x ′ + c k , z ) exp − 2( c k − x ) x ′ + x ′ 2 2 t . 23 No w w e introduce e Θ k ,q ’s as the co efficien ts of the expansion ψ k ( t, ξ , x ′ , z , x ) = X q ∈ N 0 e Θ k ,q ( t, ξ , z , x ) x ′ q . Then w e ha v e 1 a δ ( v k − c k ) | C k | X j =1 ψ k ( t, ξ , v k j − c k , z , x ) a δ ( v k − c k ; j ; z − c k ) = 1 a δ ( v k − c k ) | C k | X ℓ =1 ( z − c k ) ℓ − 1 ( − 1) | C k |− ℓ − 1 × det ψ k ( t, ξ , v k 1 − c k , z , x ) ψ k ( t, ξ , v k 2 − c k , z , x ) · · · ψ k ( t, ξ , v k | C k | − c k , z , x ) ( v k 1 − c k ) | C k |− 1 ( v k 2 − c k ) | C k |− 1 · · · ( v k | C k | − c k ) | C k |− 1 . . . . . . . . . . . . ( v k 1 − c k ) ℓ +1 ( v k 2 − c k ) ℓ +1 · · · ( v k | C k | − c k ) ℓ +1 ( v k 1 − c k ) ℓ − 1 ( v k 2 − c k ) ℓ − 1 · · · ( v k | C k | − c k ) ℓ − 1 . . . . . . . . . . . . v k 1 − c k v k 2 − c k · · · v k | C k | − c k 1 1 . . . 1 = | C k | X ℓ =1 ( z − c k ) ℓ − 1 ( − 1) | C k |− ℓ − 1 × e Θ k ,ℓ ( t, ξ , z , x ) + ∞ X q = | C k | e Θ k ,q ( t, ξ , z , x ) s ( q − | C k ||| C k |− ℓ − 1) ( v k − c k ) . Then, to pro v e the lemma, it is enough to sho w the equ ality e Θ k ,q ( t, ξ , z , x ) = Φ( ξ − C k , c k , z )Θ k ,q ( t, ξ , x ) , t ≥ 0 , ξ ∈ Y 0 , z ∈ C , x ∈ R , (4.11) for | C k | 6 = 0. F rom the form ula (3.3), w e hav e Φ( ξ − C k , x ′ + c k , z ) = Y u ∈ ξ − C k z − u x ′ − ( u − c k ) = Y u ∈ ξ − C k u − z u − c k Y u ∈ ξ − C k 1 1 − x ′ / ( u − c k ) = Y u ∈ ξ − C k u − z u − c k X r ∈ N 0 h r 1 u − c k u ∈ ξ − C k ! x ′ r = Φ( ξ − C k , c k , z ) X r ∈ N 0 h r 1 u − c k u ∈ ξ − C k ! x ′ r . (4.12) 24 By the form ula (3.16 ), w e hav e exp − 2( c k − x ) x ′ + x ′ 2 2 t = X k ∈ N 0 1 k ! − x ′ √ 2 t k H k c k − x √ 2 t . (4.13) Com bining (4.1 2 ) and (4.13), w e ha v e ψ k ( t, ξ , x ′ , z , x ) = Φ( ξ − C k , c k , z ) X r ∈ N 0 h r 1 u − c k u ∈ ξ − C k ! x ′ r × X k ∈ N 0 1 k ! − x ′ √ 2 t k H k c k − x √ 2 t = Φ( ξ − C k , c k , z ) X q ∈ N 0 x ′ q q X r =0 1 ( q − r )! − 1 √ 2 t q − r × H q − r c k − x √ 2 t h r 1 u − c k u ∈ ξ − C k ! . Then, b y definition (4.1 0), (4.11) is pro v ed. Lemma 4.6 Assume that ( C.3 ) holds with som e κ ∈ (1 / 2 , 1 ) and m ∈ N . (i) Supp ose that α ∈ (1 /κ, 2) . Then ther e ex ists C 4 ( κ, m, α ) > 0 such that M α ( τ − a ( ξ − C a )) ≤ C 4 ( κ, m )( | a | ∨ 1) (1 − κ ) /κ ∀ a ∈ supp ξ , (4.14) and ( C .2 ) (i) hold s, that is, ther e exists C 1 = C 1 ( α, ξ ) such that M α ( ξ ) ≤ C 1 . (4.15) (ii) Supp ose that β ∈ (0 , 2 κ − 1) . Then ξ − C a − c C a satisfies ( C.2 ) (ii) ∀ a ∈ supp ξ , wher e c C a = C − k in c ase C a = C k . That is, ther e exists C 2 ( κ, m ) > 0 such that M 1 τ − a 2 ( ξ − C a − c C a ) h 2 i ≤ C 2 ( κ, m )( | a | ∨ 1) − β ∀ a ∈ supp ξ . (4.16) Pr o o f. By simp le calcu lations w e see that there ex ists a p ositiv e constan t C ( κ ) suc h that M α ( τ − a η κ ) ≤ C ( κ )( | a | ∨ 1) (1 − κ ) /κ ∀ a ∈ supp η κ . (4.17) Supp ose that C a = C k , k ∈ Z . Then ξ − C a = ξ ∩ [ b k − 1 , b k ] c . W e divide t he set [ b k − 1 , b k ] c in to the following four sets : A 1 = − ∞ , g κ ( k − 2) i , A 2 = g κ ( k − 2) , b k − 1 , A 3 = b k , g κ ( k + 2) , A 4 = h g κ ( k + 2) , −∞ . 25 Then w e ha v e Z R ( ξ − C a )( dx ) | x − a | α 1 /α ≤ 4 X j =1 Z A j ξ ( dx ) | x − a | α ! 1 /α . F rom (4.7) and (4.8), w e hav e Z A 1 ξ ( dx ) | x − a | α ≤ m X −∞ <ℓ ≤ k − 2 1 | g κ ( ℓ ) − g κ ( k − 1) | α , Z A 2 ξ ( dx ) | x − a | α ≤ 2 m 1 ε k − 1 α , Z A 3 ξ ( dx ) | x − a | α ≤ 2 m 1 ε k α , Z A 4 ξ ( dx ) | x − a | α ≤ m X k +2 ≤ ℓ< ∞ 1 | g κ ( ℓ ) − g κ ( k + 1) | α . Com bining these estimates with (4.1 7), w e ha ve Z R ( ξ − C a )( dx ) | x − a | α 1 /α ≤ O ( | g κ ( k − 1) | ∨ | g κ ( k + 1) | ∨ 1) (1 − κ ) /κ , | k | → ∞ . Since max k − 1 ≤ j ≤ k +1 | g κ ( j ) | ≤ 2( | a | ∨ 1), w e o btain (4.14). The estimate (4.15 ) is deriv ed from (4 .14) with a = 0 and C a = C 0 , and the fact that M α ( C 0 ) < ∞ . Noting that ( ξ − C a − c C a ) h 2 i satisfies ( C.3 ) with 2 κ and 2 m , w e obtain (4.16 ) b y a similar argumen t giv en a b ov e to show (4 .14). This completes the pro of. Lemma 4.7 L et α ∈ (1 , 2) and | a | ≥ 1 . Assume that ( C .1 ) and the c ondition M α ( τ − a ξ ) ≤ C 5 | a | γ (4.18) with som e γ > 0 and C 5 > 0 ar e satisfie d . Then ther e exists C 6 = C 6 ( α, β , C 1 , C 5 ) > 0 such that | M ( τ − a ξ ) − M ( ξ ) | ≤ C 6 | a | δ 1 , wher e δ 1 = α ( 1 + γ ) − 1 . Pr o o f. F rom Lemma 4.3 and the fa ct that M 1 ( τ − a ξ , L ) is increasing in L , w e see that max 0 ≤ L ≤ L 0 M 1 ( τ − a ξ , L ) = M 1 ( τ − a ξ , L 0 ) ≤ (2 M α ( τ − a ξ )) αδ 1 / ( δ 1 − α +1) ≤ C | a | δ 1 from (4.18) with a constan t C > 0. Comb ining this estimate with Lemma 4.3, we ha v e M 1 ( τ − a ξ , L ) ≤ C | a | δ 1 ∨ L δ 1 . (4.19) 26 W e assume a 6 = 0. By the definitions of M ( ξ ) a nd M ( τ − a ξ ), | M ( τ − a ξ ) − M ( ξ ) | ≤ 1 + ξ ( { 0 } ) | a | + | a | Z { a, 0 } c ξ ( dx ) | x ( x − a ) | . W e divide the set { a, 0 } c in to the three disjoint subsets { x : 0 < | x | < 2 | a | , 2 | a − x | > | a |} , { x : | x | ≥ 2 | a |} and { x : 0 < | x | < 2 | a | , 0 < 2 | a − x | ≤ | a |} . By simple calculation, w e see Z 0 < | x | < 2 | a | , 2 | a − x | > | a | ξ ( dx ) | x ( x − a ) | ≤ 2 | a | Z 0 < | x | < 2 | a | ξ ( dx ) | x | = 2 | a | M 1 ( ξ , 2 | a | ) . Since | x − a | ≥ | x | − | a | ≥ | x | / 2, if | x | ≥ 2 | a | , Z | x |≥ 2 | a | ξ ( dx ) | x ( x − a ) | ≤ 2 Z | x |≥ 2 | a | ξ ( dx ) | x | 2 ≤ 2 α − 1 M α ( ξ ) α | a | α − 2 . Since | x | ≥ | a | − | a − x | ≥ | a | / 2, if 2 | a − x | ≤ | a | , Z 0 < | x | < 2 | a | , 0 < 2 | a − x |≤ | a | ξ ( dx ) | x ( x − a ) | ≤ 2 | a | Z 0 < 2 | a − x |≤| a | ξ ( dx ) | x − a | = 2 | a | M 1 τ − a ξ , | a | 2 . Com bining the ab o v e estimates with the fact | a | − 1 ≤ 1, w e hav e | M ( τ − a ξ ) − M ( ξ ) | ≤ 2 α − 1 M α ( ξ ) α | a | α − 1 + 2 M 1 ( ξ , 2 | a | ) + 2 M 1 τ − a ξ , | a | 2 + 2 . Then the lemma is deriv ed fro m (4.18) and (4.19). The follow ing is a k ey lemma to pro v e Theorem 2.4. Lemma 4.8 L et t ≥ 0 , x ∈ R , ξ ∈ Y κ m ⊂ Y with κ ∈ (1 / 2 , 1) and m ∈ N . Then for any θ ∈ (3 − 2 κ, 2) ther e exist p ositive c onstants C 7 = C 7 ( t, κ, C 0 , x ) and b C 7 = b C 7 ( t, κ, m, θ , C 0 , x ) such that | Ψ k ( t, ξ , iy , x ) | ≤ b C 7 exp h C 7 n | y | θ + | c k | θ oi , ∀ y ∈ R , ∀ k ∈ Z . Pr o o f. W e not e the equality Φ( ξ − C k , c k , iy ) = Φ( ξ − C k − C − k , c k , iy )Φ( C − k , c k , iy ) . Let β ∈ (0 , 2 κ − 1 ) a nd α = (1 /κ, 2) . By virtue of Lemma 4.6 , w e can apply Lemma 4.4 for ξ − C k − C − k and see that there e xist p ositiv e cons tant C 3 and θ ∈ (3 − 2 κ, 2) suc h that | Φ( ξ − C k − C − k , c k , iy ) | ≤ exp h C 3 n | y | θ + | c k | θ oi , y ∈ R , k ∈ Z . 27 Here w e used the fact that 3 − 2 κ > 1 /κ for κ ∈ (1 / 2 , 1). Since Φ( C − k , c k , iy ) is a p olynomial function of y , w e ha v e | Φ( ξ − C k , c k , iy ) | ≤ b C 3 exp h C 3 n | y | θ + | c k | θ oi , y ∈ R , k ∈ Z , for some b C 3 > 0. Hence, from the definition (4.9) of Ψ k ( t, ξ , z , x ), to prov e the lemma it is enough to sho w the following estimates : for an y ℓ = 1 , 2 , . . . , | C k | , | ( z − c k ) ℓ − 1 | = O ( | z | | C k | ∨ | c k | | C k | ) , | k | → ∞ , | z | → ∞ , (4.20) | Θ k ,ℓ ( t, ξ , x ) | = O ( | c k | ℓ ) , | k | → ∞ , (4.21) ∞ X q = | C k | Θ k ,q ( t, ξ , x ) s ( q − | C k ||| C k |− ℓ − 1) ( v k − c k ) ≤ exp h C ( | c k | θ ′ ∨ 1) i , k ∈ Z , (4.22) with some C = C ( t, x ) > 0 and θ ′ < θ . Since (4.20 ) and (4.21) can b e confirmed easily , here w e show o nly the pro of of (4.22). Since | v k ,ℓ − c k | ≤ ∆ k , 1 ≤ ℓ ≤ | C k | , from the fact (3.1) s ( q − | C k ||| C k |− ℓ − 1) ( v k − c k ) ≤ q − ℓ − 1 | C k | − ℓ − 1 q ℓ ∆ q k ≤ q | C k | ∆ q k , q ∈ N . Put ∆ k = ∆ k + ( ε k − 1 ∧ ε k ) / 2, and remind that ∆ k = O ( c ( κ − 1) /κ k ), | k | → ∞ . Then w e hav e s ( q − | C k ||| C k |− ℓ − 1) ( v k − c k ) ≤ C ′ ∆ k q , k ∈ Z , q ∈ N , with some p ositiv e constan t C ′ > 0 . Then Θ k ,q ( t, ξ , x ) s ( q − | C k ||| C k |− ℓ − 1) ( v k − c k ) ≤ C ′ q X r =0 1 ( q − r )! ∆ k √ 2 t q − r H q − r c k − x √ 2 t ∆ k r h r 1 u − c k u ∈ ξ − C k ! , and th us ∞ X q = | C k | Θ k ,q ( t, ξ , x ) s ( q − | C k ||| C k |− ℓ − 1) ( v k − c k ) ≤ C ′ X q ∈ N 0 1 q ! ∆ k √ 2 t q H q c k − x √ 2 t X r ∈ N 0 ∆ k r h r 1 u − c k u ∈ ξ − C k ! . Since d k dz k e 2 z y − z 2 z =0 ≤ d k dz k e 2 z | y | + z 2 z =0 , k ∈ N , y ∈ R , 28 w e obtain from (4.1 3) X q ∈ N 0 1 q ! ∆ k √ 2 t q H q c k − x √ 2 t ≤ exp 2 ∆ k ( c k − x ) + ∆ 2 k 2 t ! = O exp e C c k 1+( κ − 1) /κ ! , (4.23) | k | → ∞ , with a constan t e C = e C ( t, x ). And if ( ξ − C k )( u ) ≥ 1, then | u − c k | ≥ ∆ k + ε k − 1 ∧ ε k and 1 1 − ∆ k / | u − c k | ≤ C m with a p ositiv e constan t C . Hence from (3.2) X r ∈ N 0 ∆ k r h r 1 u − c k u ∈ ξ − C k ! ≤ exp ( M τ − c k ( ξ − C k ) ∆ k + C m ∆ k 2 M 2 τ − c k ( ξ − C k ) 2 ) . (4.24) Using Lemmas 4.6 and 4.7, w e see that M τ − c k ( ξ − C k ) ∆ k = O | c k | δ 1 +( κ − 1) /κ , | k | → ∞ , with an y δ 1 > { 1 + (1 − κ ) /κ } /κ − 1 = 1 /κ 2 − 1 , and ∆ k 2 M 2 τ − c k ( ξ − C k ) 2 = O | c k | α (1 − κ ) /κ ∆ α k = O (1) , | k | → ∞ . Since 1 /κ 2 − 1 + ( κ − 1) /κ + 1 + ( κ − 1 ) / κ = 1 /κ 2 + 2( κ − 1 ) /κ < 3 − 2 κ , for κ ∈ (1 / 2 , 1), (4.22) is deriv ed from (4.23 ) and (4.24). This completes the pro of. Pr o o f of The or em 2.4. (i) By Lemmas 4.5 and 4.8, if ξ ∈ Y 0 , Z R ξ ( dx ′ ) p ( s, x | x ′ ) Z R dy ′ p ( t, − iy | y ′ )Φ( ξ , x ′ , iy ) = X k ∈ Z p ( s, x | c k ) Z R dy ′ p ( t, − iy | y ′ )Ψ k ( t, ξ , iy ′ , x ) . (4.25) Since this equalit y holds ev en if we replace ξ b y ξ ∩ [ − L, L ] for any L > 0, lim L →∞ K ξ ∩ [ − L,L ] ( s, x ; t, y ) + 1 ( s > t ) p ( s − t, x | y ) = lim L →∞ Z R ξ ∩ [ − L, L ]( dx ′ ) p ( s, x | x ′ ) Z R dy ′ p ( t, − iy | y ′ )Φ( ξ ∩ [ − L, L ] , x ′ , iy ) = lim L →∞ X k ∈ Z p ( s, x | c k ) Z R dy ′ p ( t, − iy | y ′ )Ψ k ( t, ξ ∩ [ − L, L ] , iy ′ , x ) . 29 By Lemma 4.8, w e can apply Leb esgue’s conv ergence theorem t o sho w that the limit is X k ∈ Z p ( s, x | c k ) Z R dy ′ p ( t, − iy | y ′ )Ψ k ( t, ξ , iy ′ , x ) . W e can rep eat the arg ument in the pro of of Theorem 2 .2 given at the end o f Section 4.2. Then if ξ ∈ Y 0 , ( P ξ , Ξ( t ) , t ∈ [0 , ∞ )) is w ell-defined with the correlation kerne l K ξ ( s, x ; t, y ) = X k ∈ Z p ( s, x | c k ) Z R dy ′ p ( t, − iy | y ′ )Ψ k ( t, ξ , iy ′ , x ) − 1 ( s > t ) p ( s − t, x | y ) . (4.26) It is equal to (2.3) of Theorem 2.2 by the equality (4.25). When ξ ∈ Y \ Y 0 , (4.25) is not v alid. F or any L > 0, ho w ev er, the equalit y K ξ ∩ [ − L,L ] ( s, x ; t, y ) + 1 ( s > t ) p ( s − t, x | y ) = X k ∈ Z p ( s, x | c k ) Z R dy ′ p ( t, − iy | y ′ )Ψ k ( t, ξ ∩ [ − L, L ] , iy ′ , x ) holds b y the con tin uity with respect to the initial configuration for Dyson’s mo del with finite particles. Then, again b y Lemma 4.8 with Leb esgue’s con v ergence theo- rem, w e will obtain the result (4.26 ). (ii) By the fact (2.7) and the defin ition of Ψ k , w e see that for an y k ∈ N , t ≥ 0 , and x, y ′ ∈ R lim n →∞ Ψ k ( t, ξ n , iy ′ , x ) = Ψ k ( t, ξ , iy ′ , x ) . By using Lemma 4.8 we see t ha t, for fixed t ≥ 0 , x ∈ R , there exist θ ∈ (1 , 2) , C 7 = C 7 ( t, x ) > 0, a nd b C 7 = b C 7 ( t, x ) > 0 such that | Ψ k ( t, ξ n , iy ′ , x ) | ≤ b C 7 exp h C 7 n | y ′ | θ + | c k | θ oi , k ∈ Z , y ′ ∈ R , n ∈ N . Therefore, b y applying Leb esgue’s con ve rgence theorem, w e obtain the theorem. A cknow le dgments. The presen t authors w ould lik e to thank T. Shirai and H. S p ohn for useful commen ts on the manuscript. A part of the present work wa s d one durin g the participation of M.K. in the ESI program “Com binatorics and Statistical Ph ysics” (Marc h and Ma y in 2008). M. K. expr esses his g ratitude for hospitalit y of the Erwin Sc hr¨ odinger Institute (ESI) in Vienna and for w ell-organization of the pr ogram b y M. Drm ota and C. Kratten thaler. M.K. is supp orted in part by the Gran t-in-Aid for Scien tific Researc h (C) (No.215 40397) of Japan So cie ty for the Promotion of Science. H.T. is supp orted in part b y the Gran t-in-Aid for Scient ific R esearch (KIBAN-C, No.19540 114) of Japan So ciet y for the Promoti on of Science. 30 References [1] Andrews, G. E., Ask ey , R., Ro y , R.: Sp ecial functions. Cambridge: Cam bridge Uni- v ersit y Press, 1999 [2] Bleher, P . M., Ku ijlaars, A. B.: Integral representa tions for multiple Hermite and m ultiple Laguerre p olynomials. Ann. In s t. F our ier. 55 , 2001 -2014 (2005) [3] Dyson, F. J. : A Bro wnian-motion mo del for the eige nv alues of a r andom m atrix. J. Math. Ph ys. 3 , 119 1-1198 (1962 ) [4] Eynard, B., Meh ta, M. L. : Matrices coupled in a c hain: I. Eigen v alue correlations. J. Ph ys. A 3 1 , 444 9-4456 (1998) [5] F ritz, J.: Gr ad ient dyn amics of in finite p oin t systems. An n. Probab. 15 , 478-514 (1987 ) [6] Grabiner, D. J.: Bro wnian motion in a W eyl c hamber, n on -colliding particles, and random mat rices. Ann. Inst. Henri Poinca r´ e, Probab. Stat. 35 , 177-204 (1999) [7] Imam ur a, T., Sasamoto, T.: Polyn uclear gro wth mo del with external source and random matrix mo d el w ith deterministic source. Phys. Rev. E 71 , 041606/1 -12 (2005) [8] Ismail, M. E. H.: Classical and Quan tum O rthogonal P olynomials in One V ariable. Cam bridge: Cambridge Univ ersity Pr ess, 2005 [9] Karlin, S., McGregor, J. : Coinciden ce probabilities. Pa cific J. Math. 9 , 1141-1164 (1959 ) [10] Katori, M., T anem ura, H.: Noncolliding Brownian m otion and determinantal pr o- cesses. J. Stat. Phys. 129 , 123 3-1277 (2007 ) [11] Katori, M., T anemura, H.: in preparation [12] Levin, B. Y a.: Lectures on Enti re F unctions. T ranslations of Mathematical Mono- graphs, 150 , Pro vidence R. I.: Amer. Math. So c., 1996 [13] Macdonald, I. G. : S ymmetric F un ctions and Hall P olynomials. 2nd ed ition, Oxford: Oxford Univ. Press, 1995 [14] Meht a, M. L. : Rand om Matrices. 3rd edition, Amsterdam: Elsevier, 2004 [15] Nagao, T., F orr ester, P . J. : Multilev el dynamical correlat ion fun ctions for Dyson’s Bro wnian motion mo del of random mat rices. Ph ys. Lett . A247 , 42-46 (1998 ) [16] Osada, H. : Dirichlet form appr oac h to infinite-dimensional Wiener pro cesses with singular interact ions. Commun. Math. Ph ys. 176 , 11 7-131 (1996) [17] Osada, H. : Int eracting Bro wnian motions in in finite dimensions with logarithmic in teraction p oten tials. a rXiv:math.PR/0902.356 1 31 [18] Sh ir ai, T., T ak ah ash i, Y.: Random p oin t fields asso ciated with certain F redh olm determinan ts I: ferm ion, P oisson and b oson p oint pro cess. J. F unct. Anal. 20 5 , 414- 463 (2003) [19] Soshn ik o v, A. : Determinan tal random p oin t fields. Russian Math. S urveys 55 , 923- 975 (2000) [20] Sp ohn, H. : In teracting Brownian p articles: a study of Dyson’s mo d el. In: Hy- dro dyn amic Beha vior and In teracting Particle Systems, G. Papanicol aou (ed), IMA V olumes in Mathematics and its Applications, 9 , Berlin: Spr inger-V erlag, 1987, pp . 151-1 79 [21] T racy , C. A., Widom, H.: Differen tial equations for Dyson p ro cesses. Comm un. Math. Ph ys. 252 , 7-41 (2 004) 32

Original Paper

Loading high-quality paper...

Comments & Academic Discussion

Loading comments...

Leave a Comment