Analytical Determination of Fractal Structure in Stochastic Time Series

Current methods for determining whether a time series exhibits fractal structure (FS) rely on subjective assessments on estimators of the Hurst exponent (H). Here, I introduce the Bayesian Assessment of Scaling, an analytical framework for drawing objective and accurate inferences on the FS of time series. The technique exploits the scaling property of the diffusion associated to a time series. The resulting criterion is simple to compute and represents an accurate characterization of the evidence supporting different hypotheses on the scaling regime of a time series. Additionally, a closed-form Maximum Likelihood estimator of H is derived from the criterion, and this estimator outperforms the best available estimators.

💡 Research Summary

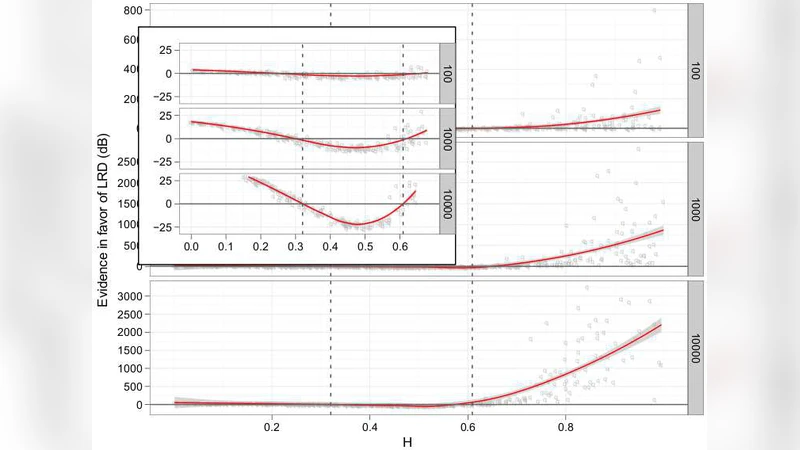

The paper introduces a Bayesian Assessment of Scaling (BAS) as a rigorous, analytical framework for determining whether a stochastic time series exhibits fractal structure (FS). Traditional approaches rely on estimating the Hurst exponent (H) through methods such as rescaled range analysis, detrended fluctuation analysis, wavelet techniques, or spectral estimators, and then subjectively deciding if the estimated H deviates sufficiently from 0.5. These methods suffer from three major drawbacks: (i) the choice of the scaling interval (τ_min, τ_max) is largely heuristic; (ii) they are sensitive to non‑stationarity, noise, and finite‑sample effects; and (iii) the statistical properties (bias, variance) of the estimators are rarely quantified in a unified way.

BAS reframes the problem by treating the time series as a diffusion process. For a given lag τ, the increment Δx(τ)=x_{t+τ}−x_t is assumed to follow a normal distribution with zero mean and variance σ²τ^{2H}. Under this model the log‑likelihood of observed increments {Δx_i(τ_i)} is

L(H,σ,τ_min,τ_max)=−½∑_{i}

Comments & Academic Discussion

Loading comments...

Leave a Comment