On a Generalized Foster-Lyapunov Type Criterion for the Stability of Multidimensional Markov chains with Applications to the Slotted-Aloha Protocol with Finite Number of Queues

In this paper, we generalize a positive recurrence criterion for multidimensional discrete-time Markov chains over countable state spaces due to Rosberg (JAP, Vol. 17, No. 3, 1980). We revisit the stability analysis of well known slotted-Aloha protoc…

Authors: Sayee C. Kompalli, Ravi R. Mazumdar

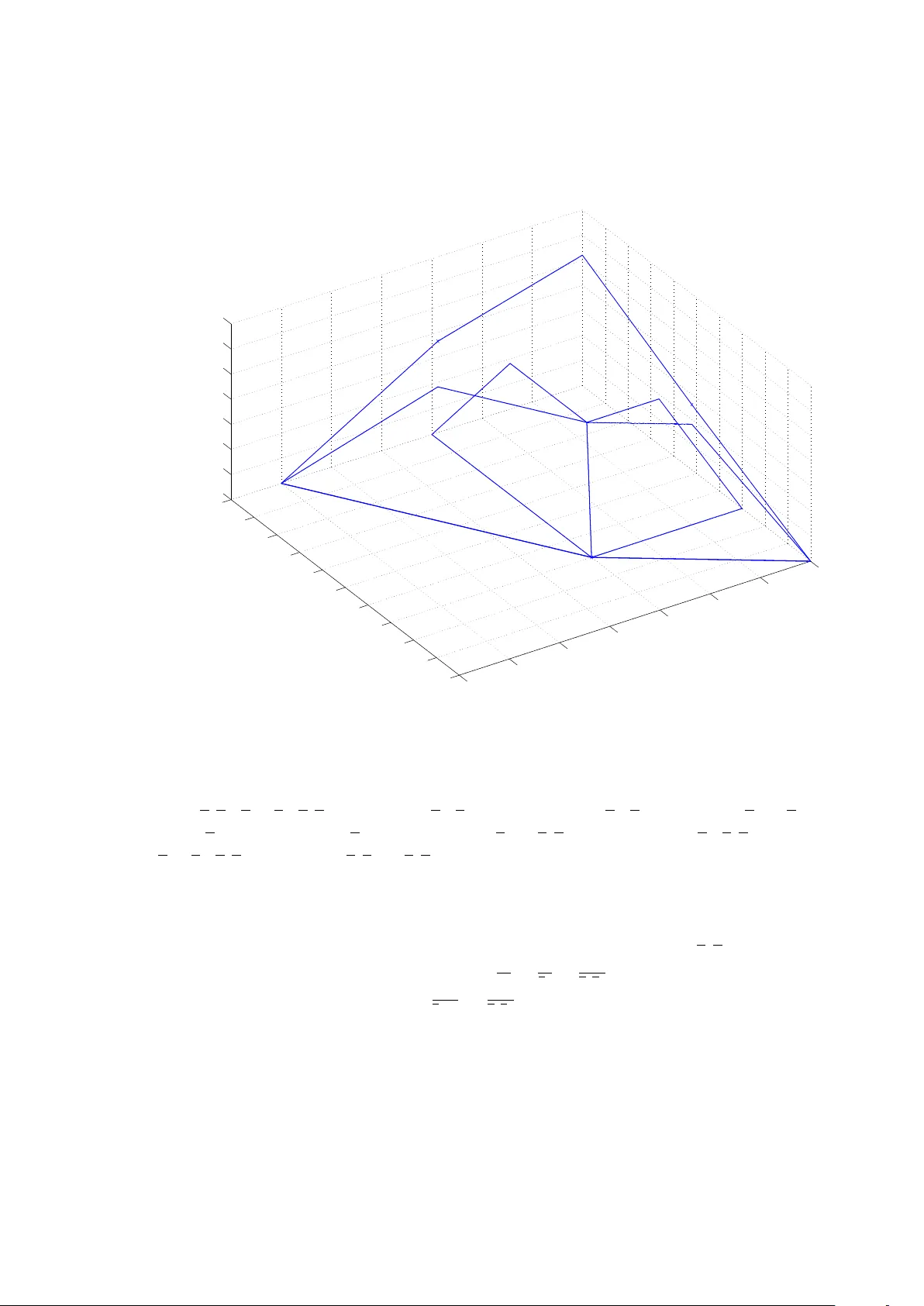

On a Generalized F oster-Ly apuno v T yp e Criterion for the Stabilit y of Multidimensional Mark o v c hains with Applications to the Slotted-Aloha Proto col with Finite Num b er of Queues ∗ Sa yee C. Kompalli and Ra vi R. Mazumdar Departmen t of Electrical and Computer Engineering Univ ersity of W aterlo o, Canada N2L 3G1. Email: sk ompall@uw aterlo o.ca, mazum@ece.u w aterlo o.ca June 5, 2018 Abstract In this pap er, w e generalize a p ositiv e recurrence criterion for multidimensional discrete-time Mark ov c hains ov er countable state spaces due to Rosb erg (JAP , V ol. 17, No. 3, 1980). W e revisit the stabilit y analysis of well kno wn slotted-Aloha proto col with finite num b er of queues. Under standard mo deling assumptions, we deriv e a sufficien t condition for the stability b y applying our positive recurrence criterion. Our sufficiency condition for stabilit y is linear in arriv al rates and do es not require knowledge of the stationary join t statistics of queue lengths. W e be- liev e that the technique rep orted here could b e useful in analyzing other stability problems in countable space Marko vian settings. T o w ard the end, we derive some sufficien t conditions for instability of the proto col. 1 In tro duction Recen tly there has been m uch activit y in trying to understand the stabilit y region of differen t m ultipleaccess schemes for wireless net works of whic h the Aloha proto col and its v ariation Slotted-Aloha protocol are archet yp es. The most common access sc heme for wireless netw orks is the conten tion mec hanism used in the IEEE 802.11 that uses a exp onen tial window type of back off where the window doubles if collisions o ccur. Due to the difficult y of analyzing the stability region muc h atten tion has been fo cussed on the so called saturation throughput. This is the av erage throughput seen by each queue or user assuming that they alw ays ha v e a pac ket to transmit. Th us the en tire question of stabilit y is sidestepp ed. It is well known and by now there are many text-b o ok accoun ts of it [1] that the slotted aloha scheme is unstable when the num b er of users (or queues) go es to infinit y and there is a fixed probabilit y of attempting to transmit. It is only the finite case that is really unkno wn. ∗ Preliminary v ersion of the results rep orted here are to appear in the Proceedings of 21st In ternational T eletraffic Congress (ITC 21), P aris. 1 The stabilit y analysis of slotted Aloha protocol with finite n um b er of queues has at- tracted lot of attention from researchers since its form ulation b y Tsybako v and Mikhailo v [2] in 1979. The contin ued interest in this proto col is c hiefly due to the fact that in spite of its extreme simplicit y the analytical difficulties presen ted by the interacting queues has yielded no general necessary and sufficient conditions for p ositive recurrence. The standard modeling assumptions made in the literature to analyze this proto col result in a discrete-time Mark o v c hain mo del of the queue lengths o ver a countable set. An imp ortan t p erformance measure of this protocol is stability , i.e., for what set of arriv al rates at different queues the av erage dela y experienced b y a pack et is finite. In this pap er, w e resurrect a p ositiv e recurrence criterion for countable space multidimensional Mark ov c hain prov ed b y Rosb erg [3] that has b een largely forgotten. W e show usefulness of this criterion b y first generalizing criterion [3] due to Rosb erg and then applying it to the stabilit y analysis of buffered slotted-Aloha proto col with finite num b er of queues. The discrete-time countable space Mark ov chain mo deling of the slotted-Aloha pro- to col with finite n umber of queues was first prop osed and analyzed b y Tsybak o v and Mikhailo v in [2]. In [2], they provided the exact stabilit y c haracterization when the n umber of queues J = 2. The next effort w as b y Rao and Ephremides [4] in 1988 who pro vided exact stability conditions for J = 2, and sufficien t conditions for stabilit y for J > 2 using sto chastic dominance arguments and assuming Bernoulli input pro cess at eac h queue. In 1994, Szpank o wski [5] obtained the exact stability region for J > 2. The stabilit y region c haracterization is giv en in terms of the stationary probabilities of joint statistics of the queues. Ho w ever, for systems with more than three queues, the neces- sary and sufficient condition cannot b e computed explicitly since it b ecomes v ery hard to compute the join t stationary statistics of the queues. In 1999, Luo and Ephremides [6] in tro duced the concept of “stability rank” to obtain tigh t inner and outer b ounds to the stabilit y region when J > 2. When queue i is kno wn to b e stable, then any queue j suc h that λ j (1 − p j ) p j ≤ λ i (1 − p i ) p i is also prov en to b e stable, where λ j and p j are, resp ectively , the av erage pac k et arriv al rate and the fixed transmission attempt probabilit y of the j th queue. Then it immediately follows that if queue k is unstable then λ k (1 − p k ) p k > λ i (1 − p i ) p i . With the help of stability ranks, they computed tigh t inner bounds to the stabilit y region. Unfortunately , here also it is required to determine some stationary joint probabilities but which are extremely difficult to compute. In all these pap ers, the goal w as to derive sufficiency conditions for a fixe d transmission attempt probabilit y v ector p . Instead, if one considers the union of the stabilit y regions o ver all p ossible transmission probabilit y v ectors p , one obtains the closure of the stabilit y region. In 1991, Anantharam [7] obtained closure of the stability region for J > 2 alb eit for a correlated arriv al pro cesses. Recen tly , in [8], a simple appro ximate expression for the stabilit y region w as proposed b y using me an field analysis . Indeed they show a propagation of chaos takes place when the n umber of interacting queues is large. This expression is prov ed to b e exact when the n umber of queues gro ws large, and is also sho wn to b e accurate in the case of small-queue systems through n umerical experiments. The approximate stabilit y region is deriv ed assuming that queue lengths evolv e indep endently . The b oundary of the appro ximate stabilit y region is characterized by a parametric expression that is a function of the attempt probabilit y v ector p . Our sufficien t conditions for stability are in the form of simple linear inequalities and hence lead to m uch easier v erification. Our approac h leads to sufficien t conditions that do not depend on knowing the sta- tionary distributions, and are completely characterized by the arriv al parameters and 2 the attempt probabilities of the queues. In particular, w e show that for the case of t w o and three in teracting queues w e can reco ver the known results. Ho wev er, we ha ve found a few instances where certain arriv al rate v ectors λ satisfy the sufficiency condition for stabilit y deriv ed by Luo and Epphremides [6] but not ours. Ho w ev er w e do not need to establish the stability of an y higher rank queue as they require. A popular tec hnique to establish ergo dicit y of coun table space Mark o v c hains is through F oster-Lyapuno v approac h whic h consists of finding a function that satisfies F oster’s criterion [9]. Though this approach pro v ed to b e v ery successful for one dimen- sional Mark o v c hains, but finding such a function prov ed to b e v ery difficult in the case of multidimensional Mark ov chains. Rosb erg [3] extended F oster’s criterion [9] for J - dimensional Marko v chains b y requiring existence of J functions, one for each co ordinate of the pro cess. But the applicability of his criterion b ecame limited by the difficulties that arise in verifying his conditions. The main contribution of this pap er is in prop osing a generalization of the p ositiv e recurrence criterion due to Rosberg [3], thus expanding the scop e of its applicabilit y , and also distilling some of the assumptions made therein in to a form that immediately lead to easier v erification. T o illustrate the applicability of our criterion, we deriv e sufficient conditions for stability of the well kno wn slotted-Aloha proto col for multiaccess communication. The rest of the pap er is organized in to t wo ma jor parts: Section 2 and Section 3. In Section 2, we generalize the p ositive recurrence criterion for multidimensional coun table space Marko v c hains due to Rosb erg [3]. In Section 3, we apply the p ositive recurrence criterion dev elop ed in Section 2 to the stability analysis of the slotted-Aloha protocol with finite num b er of queues. W e provide some remarks on the instabilit y of the proto col in Section 3.4. W e end the pap er with conclusions in Section 4. 2 A Generalized F oster-Ly apuno v T yp e Criterion for P ositiv e Recurrence Let X b e a countable set of states ov er whic h the irreducible, aperio dic, and discrete-time Mark ov chain { X n , n ≥ 0 } tak es its v alues. F or any in teger k ≥ 1, define p k xy , x, y ∈ X to b e the k -step transition probability la w of the Marko v c hain { X n , n ≥ 0 } . F or an y subset B ⊆ X , we know that the lim k →∞ p k x B = lim k →∞ P y ∈B p k xy = π ( B ) ≥ 0 exists and is indep endent of the initial state x . F or an y nonnegative-v alued function V on X , let us define ∆ k V ( x ) , P y p k xy V ( y ) − V ( x ) to b e the k -step drift of the function V in state x . Let us now define the notion of “partial order” on the state space X . Let b e a binary relation on the set X suc h that (i) x x for all x ∈ X (reflexivity) (ii) x y and y z imply x z (transitivit y) (iii) x y and y x imply x = y (antisymmetry) Then is called a p artial or der on the set X . An elemen t x ∗ ∈ X is called the minimal elemen t of X with resp ect to the partial order if x ∗ y for all y ∈ X . Let us no w supp ose that defines a partial order on the set X , and the Marko v chain ev olution o ver the discrete-time n is mo deled by the sto chastic mapping f defined as 3 X n +1 = f ( X n , Λ n ) , n ≥ 0 (1) where X n ∈ X and Λ n is the input (driving function) to the system. W e will see tw o instances of this sto c hastic recursive relation in equations (6) and (7) in the con text of slotted-Aloha proto col. Let us sa y that the mapping f is or der-pr eserving when, for a fixe d input Λ n , we hav e X n Y n ⇒ X n +1 = f ( X n , Λ n ) f ( Y n , Λ n ) = Y n +1 (2) W e no w state our main con tribution, whic h is a generalization of the m ultidimensional p ositiv e recurrence criterion due to Rosb erg [3], as the follo wing theorem. In the rest of the pap er, we will b e using the same notation X to denote b oth the state space and its subsets. The distinction is made through the usage of subscripts, i.e., X j denotes a subset. Theorem 2.1 L et J ≥ 2 b e an inte ger. Assumption 2.1 Ther e exists a c ol le ction P = {P 1 , P 2 , . . . , P J } of p artitions of the set X wher e P j = X j , X c j , and nonne gative-value d functions { V j ( x ) , x ∈ X } for 1 ≤ j ≤ J such that the drift ∆ V j ( x ) of the function V j in the state x has the fol lowing form: ∆ V j ( x ) ≤ η j for x ∈ X − j for x ∈ X c j , (3) wher e j > 0 and η j ≥ 0 . Assumption 2.2 Ther e exist p artitions A j,k , A c j,k , k ≥ 1 and 1 ≤ j ≤ J , of the set X with the fol lowing two pr op erties: (i) p l xy = 0 , 0 ≤ l ≤ k − 1 , for x ∈ A c j,k and y ∈ X j (ii) ∩ j A j,k is a finite set Assumption 2.3 The sto chastic r e cursive r elation f (e quation (1))that mo dels the sys- tem is or der-pr eserving, and for 1 ≤ j ≤ J the drift function ∆ V j ( x ) in the ar gument x is a non-increasing function with r esp e ct to the p artial or der , i.e., x y ⇒ ∆ V j ( x ) ≥ ∆ V j ( y ) . Then the Markov chain { X n , n ≥ 1 } is p ositive r e curr ent. Before w e formally pro v e Theorem 2.1 and then p oin t out how Theorem 2.1 generalizes the p ositiv e recurrence criterion of Rosb erg, we briefly discuss a m ultiv ariate sto chastic order known as usual multivariate sto chastic or der [10] and also establish few supp orting Lemmas. 4 2.1 Multiv ariate Sto c hastic Order for Random V ariables Let b e a partial order on the set X . F or any tw o elemen ts x and y in X , w e sa y that a set B ⊆ X is (i) an Upp er Set if y ∈ B whenever x y and x ∈ B and (ii) a L ower Set if y ∈ B whenev er y x and x ∈ B . F or any tw o random v ariables X and Y that take v alues in the set X , w e sa y that the random v ariable X is sto chastic al ly lar ger than the random v ariable Y if p ( X ∈ B ) ≥ p ( Y ∈ B ) , ∀ Upp er sets B ⊆ X When X is stochastically larger than Y , w e write X ≥ st Y . W e sa y that X is sto c hastically smaller than Y , i.e., X ≤ st Y , if p ( X ∈ B ) ≥ p ( Y ∈ B ) , ∀ Low er sets B ⊆ X An imp ortant characterization of the usual sto chastic order is giv en in the following theorem due to Strassen [11]. Theorem 2.2 (Theorem 6.B.1. in [10]) The r andom ve ctors X and Y satisfy X ≤ st Y if, and only if, ther e exists two r andom ve ctors ˆ X and ˆ Y , define d on the same pr ob ability sp ac e, such that ˆ X = st X , ˆ Y = st Y , and P n ˆ X ≤ ˆ Y o = 1 . In Lemma 2.1, w e state an expression for ∆ k V ( x ) in terms of the one-step drifts { ∆ V ( x ) , x ∈ X } . Lemma 2.1 L et t 1 and t 2 b e p ositive inte gers. Then ∆ t 1 + t 2 V ( x ) = ∆ t 1 V ( x ) + X y ∈X p t 1 xy ∆ t 2 V ( y ) Pr o of: ∆ t 1 + t 2 V ( x ) = X y ∈X p t 1 + t 2 xy V ( y ) − V ( x ) = X y ∈X X z ∈X p t 1 xz p t 2 z y ! V ( y ) − V ( x ) = X z ∈X p t 1 xz X y ∈X p t 2 z y V ( y ) − V ( x ) = X z ∈X p t 1 xz ∆ t 2 V ( z ) + V ( z ) − V ( x ) = ∆ t 1 V ( x ) + X y ∈X p t 1 xy ∆ t 2 V ( y ) 5 Corollary 2.1 Define t 0 = 0 . F or some inte ger J ≥ 1 , let t 1 , t 2 , . . . , t J b e p ositive inte gers. Then for x ∈ X , ∆ P J j =1 t j V ( x ) = X y ∈X J − 1 X j =0 p ( P j k =0 t k ) xy ∆ t j +1 V ( y ) Pr o of: Rep eated application of Lemma 2.1 giv es the result. Next, we establish that lim k →∞ 1 k ∆ k V ( x ) = c ∗ ≥ 0 under the assumption that the Mark ov chain is irreducible and ap erio dic. T o see this, assume that the drift ∆ V ( x ) is upp er b ounded b y a p ositiv e constant η . Then it is easy to see the existence of lim k →∞ 1 k ∆ k V ( x ) b ecause lim k →∞ 1 k ∆ k V ( x ) = lim k →∞ 1 k P y ∈X ∆ V ( y ) P k − 1 l =0 p l xy ≤ η . More- o ver, since V ( x ) k k →∞ → 0 and V ( x ) ≥ 0, w e hav e lim k →∞ 1 k ∆ k V ( x ) = lim k →∞ 1 k X y ∈X p k xy V ( y ) − V ( x ) ! = c ∗ ≥ 0 . Lemma 2.2 F or any non-ne gative r andom variables Y 1 , Y 2 , . . . , Y m and a c onstant a > 0 , p max 1 ≤ i ≤ m Y i ≥ a ≤ 1 a m X i =1 E ( Y i ) Pr o of: p max 1 ≤ i ≤ m Y i ≥ a = p m [ i =1 { Y i ≥ a } ! ≤ m X i =1 p ( Y i ≥ a ) ( b ) ≤ 1 a m X i =1 E ( Y i ) , where ( b ) follows from Mark o v inequality . Lemma 2.3 L et k ≥ 1 . Then ∆ k V j ( x ) ≤ − k j , 1 ≤ j ≤ J , for x ∈ A c j,k . Pr o of: Let x ∈ A c j,k . Then ∆ k V j ( x ) = X y ∈X ∆ V j ( y ) k − 1 X l =0 p l xy = X y ∈X j ∆ V j ( y ) k − 1 X l =0 p l xy + X y ∈X c j ∆ V j ( y ) k − 1 X l =0 p l xy ( a ) ≤ − k j where ( a ) follows from Assumption 2.2. 6 Let us assume that ∆ V j ( x ) assumes L j differen t v alues d j, 1 > d j, 2 > · · · > d j,L j on the set X . F or 1 ≤ k ≤ L j , define A j,k = { x ∈ X : ∆ V j ( x ) = d j,k } . It is obvious to note that the collection of sets { A j,k , 1 ≤ k ≤ L j } defines a partition of the set X . W e now deduce that, for 1 ≤ l ≤ L j , the set S L j k = l A j,k is an Upp er Set. This simple fact follows from the Assumption 2.3 of Theorem 2.1 that ∆ V j ( x ) is a non-increasing function with resp ect to the partial order . Alternately , the set S l k =1 A j,k is a Low er Set. Next, for 1 ≤ j ≤ J , let us define the collection { B j,k , 1 ≤ k ≤ L j } of Low er sets of X as B j,k = { x ∈ X : ∆ V j ( x ) ≥ d j,k } = k [ l =1 A j,l No w, we express ∆ n V j ( x ) as a weighte d sum of pr ob abilities of L ower sets in X . Lemma 2.4 ∆ n V j ( x ) = d j,L j + L j − 1 X l =1 ( d j,l − d j,l +1 ) n − 1 X k =0 p k x,B j,l , 1 ≤ j ≤ J Pr o of: ∆ n V j ( x ) = X y ∈X ∆ V j ( y ) n − 1 X k =0 p k x,y = L j X l =1 X y ∈ A j,l ∆ V j ( y ) n − 1 X k =0 p k x,y = L j X l =1 d j,l n − 1 X k =0 p k x,A j,l = d j,L j + L j − 1 X l =1 d j,l − d j,L j n − 1 X k =0 p k x,A j,l = d j,L j + d j,L j − 1 − d j,L j n − 1 X k =0 p k x,B j,L j − 1 + L j − 2 X l =1 d j,l − d j,L j − 1 n − 1 X k =0 p k x,A j,l Con tinuing this w a y , finally , w e obtain the expression stated in Lemma 2.4. Lemma 2.5 The se quenc es 1 n ∆ n V j ( x ) , n ≥ 1 , indexe d by the elements x ∈ X , ar e uniformly upp er b ounded , i.e. for a given δ > 0 ther e exists a N ( δ ) such that 1 n ∆ n V j ( x ) ≤ c ∗ j + δ for al l x ∈ X and n ≥ N ( δ ) . Pr o of: Because the sto c hastic recursive relation f (equation (1)) is assumed to b e order-preserving, the Strassen’s Theorem 2.2 implies that for any tw o states x and y suc h that x y it is true that ( X n | X 0 = x ) ≤ st ( X n | X 0 = y ). In particular, w e hav e that p (( X n | X 0 = x ) ∈ B ) ≥ p (( X n | X 0 = y ) ∈ B ) for an y Lo wer set B ⊆ X . But this 7 observ ation in conjunction with Lemma 2.4 allows us to deduce that ∆ n V j ( x ) ≥ ∆ n V j ( y ) whenev er x y . In particular, ∆ n V j ( y ) ≤ ∆ n V j ( x ∗ ) where x ∗ is the minimal element of X . Now, for a δ > 0, we can find N ( δ ) suc h that 1 n ∆ n V j ( x ∗ ) ≤ c ∗ j + δ . This completes the pro of. Let us fix an arbitrary δ > 0. F rom Lemma 2.5, it follows that there exits a p ositiv e in teger K suc h that ∆ k V j ( x ) k ≤ c ∗ j + δ for k ≥ K and 1 ≤ j ≤ J . Let us pick one such K , and then introduce the set of functions g K j ( x ); x ∈ X suc h that the following holds: ∆ K V j ( x ) = − g K j ( x ) + K c ∗ j + δ (4) Tw o observ ations on the functions g K j are in order: the first and the ob vious obser- v ation is that g K j ( x ) ≥ 0 for x ∈ X . Also, since ∆ K V j ( x ) ≤ − K j for x ∈ A c j, K , we hav e that g K j ( x ) ≥ c ∗ j + δ + j for x ∈ A c j, K . Set = min j j and δ = min j δ j . As a result, w e hav e the obvious deduction that max j g K j ( x ) ≥ min j K c ∗ j + δ + j = ( c ∗ + δ + ) for x ∈ ∪ j A c j, K . Hence max j g K j ( x ) < min j K ( c ∗ + δ + ) implies that x ∈ ∩ j A j, K . W e should note that x ∈ ∩ j A j,k ne e d not imply that max j g K j ( x ) < K ( c ∗ + δ + ). 2.2 Pro of of Theorem 2.1 Pr o of: Denote by E x g K j ( X n ) the exp ectation of g K j ( X n ) given that X 0 = x and b y p x ( X n ∈ A ) the probability that X n ∈ A given that X 0 = x . No w ∆ n K V j ( x ) n = X y ∈X 1 n n − 1 X l =0 p l K xy ∆ K V j ( y ) ( a ) = X y ∈X 1 n n − 1 X l =0 p l K xy − g K j ( y ) + K ( c ∗ j + δ ) = − X y ∈X 1 n n − 1 X l =0 p l K xy g K j ( y ) + K ( c ∗ j + δ ) = − 1 n n − 1 X l =0 E x g K j X l K + K ( c ∗ j + δ ) where ( a ) follows from (4). Since lim n →∞ ∆ n K V j ( x ) n K = c ∗ j , we hav e that 1 n P n − 1 l =0 E x g K j X l K = K δ . Now 8 lim inf n →∞ 1 n p x max j g K j ( x ) < K ( c ∗ + δ + ) ( b ) ≥ 1 − lim sup n →∞ 1 n n − 1 X l =0 J X j =1 E x g K j X l K K ( c ∗ + δ + ) ≥ 1 − 1 K ( c ∗ + δ + ) × J X j =1 lim sup n →∞ 1 n n − 1 X l =0 E x g K j X l K = 1 − J K δ K ( c ∗ + δ + ) = 1 − J δ ( c ∗ + δ + ) , where ( b ) follows from Lemma 2.2. W e note that there exists a δ 0 > 0 such that 1 − J δ ( c ∗ + δ 0 + ) > 0. Define the set A 0 = x ∈ X : max j g K j ( x ) < K ( c ∗ + δ 0 + ) W e can observe that A 0 ⊆ ∩ j A j,k is a finite set. Hence it follows that for the finite set A 0 , lim inf n →∞ 1 n n − 1 X l =0 p x X l K ∈ A 0 > 0 Since the chain is assumed to b e irreducible and ap erio dic, it follows that the Marko v c hain is p ositive recurren t. Remarks: Rosb erg [3] assumed in his mo del that X = Z J + for some integer J ≥ 2, and then considered an equal num b er J of partitions X j , X c j , 1 ≤ j ≤ J , of the countable space X , and also the same num b er J of Lyapuno v functions { V j ( x ) , x ∈ X } , 1 ≤ j ≤ J . Ho wev er, in our generalization of his criterion, we do not require the countable space X to hav e a fixed predetermined dimension. This is reflexed in Assumption 2.1 of Theo- rem 2.1. Hence we are free to choose an appropriate num b er of Ly apuno v functions and the corresp onding suitable partitions of the state space X . W e b elieve this generalization will b e useful for the reason that in many situations of in terest one do es not obtain a state space of some fixed predetermined dimension. Moreo ver, ev en in the context of a Mark o v c hain with some fixed dimension it may not b e appropriate to consider an equal num b er J of Lyapuno v functions and hence an equal num b er J of partitions of the state space X . Finally , Assumption 2.3 of Theorem 2.1 is a refinement of the following definition 2.1 prop osed by Rosb erg. But to appreciate this, w e need to discuss mo del considered by Rosb erg in some more detail. Rosb erg considered a fixed dimensional non-negativ e in teger space Z J + and then for eac h dimension j , 1 ≤ j ≤ J , he assumed that there exist p ositive integers N j and the corresp onding partitions n X j,N j , X c j,N j o of the state space X where X c j,N j = { x ∈ X : x j ≥ N j } and X j,N j = { x ∈ X : x j < N j } . Then he assumed that 9 ∆ V j ( x ) ≤ η j for x ∈ X − j for x ∈ X c j,N j , (5) where j > 0 and η j ≥ 0. He also made another assumption that there exists a p ositive integer M suc h that p xy = 0 whenever ( x j − y j ) > M for some j , where x, y ∈ X . W e can note here that Assumption 2.2 of Theorem 2.1 is a generalization of the assumption made b y Rosb erg. Definition 2.1 (Rosb erg [3]) F or 1 ≤ j ≤ J , the se quenc e n ∆ k V j ( x ) k , k ≥ 1 o is said to b e uniformly upp er b ounde d (UUB) if, for any δ > 0 , ther e exists a p ositive inte ger K such that ∆ k V j ( x ) k < c ∗ j + δ for k ≥ K and x ∈ X j,N j +( k − 1) M . But no w it is straightforw ard to see that Lemma 2.5 implies UUB prop ert y of Rosb erg. 3 Stabilit y Analysis of Slotted-Aloha Proto col with Finite Num b er of Queues The rest of this section is organized as follows. In Section 3.1, we presen t mo deling details of the standard slotted-Aloha proto col. In Section 3.2, we describ e in detail a dominant queueing mo del of the proto col and then present its stabilit y analysis in Section 3.3. In Section 3.4, we make some remarks on the instability of the proto col. 3.1 Mo del Consider a system S 1 of J transmitting stations. A t each station, there is a queue with infinite buffer space to store incoming pac kets and the queue is connected to a transmitter. These J transmitters wish to send pack ets in their resp ective buffers to a common receiv er o ver a c ol lision channel . T ransmitter j is assumed to b e associated with a Bernoulli random process Y j = Y n j , n ≥ 1 where the random v ariable Y n j with the distribution p Y n j = 1 = p j = 1 − p Y n j = 0 mo dels the pack et transmission attempt of the transmitter j in the n th time slot. That is, the j th transmitter with non-empt y queue transmits in a slot with probability p j and do es not transmit with probability p j = 1 − p j , indep enden t of ev erything else. W e denote by Y n the random vector ( Y n 1 , Y n 2 , . . . , Y n J ). The communication channel b et ween the transmitters and the receiver is mo deled b y a collision c hannel mo del. Under the collision c hannel mo del, a pack et transmission is successful if and only if at most one transmitter with a non-empty queue transmits. When more than one transmitter transmits in a slot, all pack et transmissions inv olv ed in that time slot are considered to ha ve collided and hence are lost for all practical purp oses. The length of a time slot is taken to b e the duration of a pack et transmission. At the end of eac h time slot, all transmitting stations are provided with ternary feedback which tells whether the time slot was idle (no attempted transmissions), successful (exactly one transmitter transmitted), or a failure (at least t w o transmitters transmitted in that time slot). T o mo del pac k et arriv als in to v arious queues, w e assume that pack ets arriv e randomly in to v arious queues and the pac ket arriv al pro cess in to queue j is mo deled by an i.i.d. batc h arriv al pro cess Λ j = Λ n j , n ≥ 1 where the random v ariable Λ n j with finite first 10 momen t E Λ n j = λ j mo dels the n um b er of pack et arriv als in to queue j during the n th time slot. Define b y λ the v ector ( λ 1 , λ 2 , . . . , λ J ) of pack et arriv al rates. Let Q n j denote the n umber of pac kets present in the queue j at the beginning of the n th time slot. Denote by Q n = Q n 1 , Q n 2 , . . . , Q n J the queue-length vector at the b eginning of the n th time slot. F rom the assumptions made so far, w e can easily note that the queue-length pro cess Q n , n ≥ 0 is a discrete-time Marko v c hain ov er the countable space Z J + , where Z J + is the set of non-negative in teger vectors of dimension J . F or an even t A , let us define the indicator function I { A } as I { A } = 1 if the even t A is true, and I { A } = 0 otherwise. F rom the ab o v e discussion, it is clear that transmitter j transmits a pac k et if and only if the pro duct Y n j I Q n j > 0 = 1, and no pac ket transmission happ ens otherwise. If a pack et from the j th queue is inv olv ed in collision during the n th time slot it is then retransmitted in the ( n + 1)th time slot with the same probability p j . When there is only one transmission in a time slot w e sa y that the transmission is successful in that it is receiv ed error free at the receiver and the corresp onding queue length is decremented by 1. The queue length ev olution with time is given by Q n +1 j = Q n j + Λ n j − D n j D n j = Y n j I Q n j > 0 Y k 6 = j 1 − Y n k I Q n k > 0 (6) where the random v ariable D n j ∈ { 0 , 1 } denotes the num b er of departures from the j th queue in the n th time slot. 3.2 Dominan t System W e no w consider another system S 2 of J queues suc h that when S 1 and S 2 ha ve the follo wing identic al features F1 , F2 , and F3 , then S 2 will dominate the original system S 1 in the sense that queue lengths in S 2 will b e at least as large as the resp ective queue lengths in S 1 at all times. Let the random v ariables Q n j and D n j denote 1 the queue length of and the n umber of departures from the j th queue for the n th time slot. The following features are assumed to b e identical to b oth S 1 and S 2 . F1 initial state, i.e., Q 0 = Q 0 . F2 arriv al pro cesses, i.e., arriv als into the j th queue in S 2 o ccur exactly at the same time instants as in the original system S 1 . F3 transmission attempts, i.e., the Bernoulli random vector Y n that determines trans- mission attempts in the original system S 1 for the n th time slot also determines the transmission attempts for the n th time slot in the system S 2 . The distinguishing feature of S 2 from S 1 will come from the presence of dummy p acket tr ansmissions from S 2 , i.e., queue j of S 2 transmits a pack et, called dummy pac ket, with probabilit y p j up on b ecoming empty . The asp ect on which the tw o systems will differ is the interference as seen b y the individual queues in S 2 . By careful construction, we mak e in terference for the queue j in S 2 at least as large as the interference seen by the queue 1 Usage of an over line in the notation will distinguish queue length and departure random v ariables of S 1 from that of S 2 . An ov er line in the notation is used only for the original system S 1 . 11 j in the original system S 1 . As a consequence, a successful transmission from the queue j in S 2 implies a successful transmission from the queue j of S 1 pro vided Q j > 0. But the conv erse need not b e true. This fact b ecomes revealed when we compare the queue length ev olutions (6) and (7), resp ectively , of S 1 and S 2 . Henceforth, we will refer to S 2 as a dominant of the original S 1 . T o b e able to define the rules that will sp ecify the in terference to b e seen b y an y individual queue in S 2 , we define tw o sets U j and V j of queues for each queue j . U 1 = ∅ and U j = { 1 , 2 , . . . , j − 1 } for j ≥ 2 V j = { j + 1 , j + 2 , . . . , J } for j < J and V J = ∅ The sets U j and V j will b e designated as, resp ectively , the set of non-p ersistent and the set of p ersistent queues of the j th queue for the follo wing reason. A real pac ket transmission from queue j is effected by (i) only r e al pack et transmissions from the queues that b elong to the set of queues U j , and (ii) b oth r e al and dummy pac ket transmissions from the queues that b elong to the set of queues V j . In other words, eac h queue j in S 2 transmits a dummy pac k et with probability p j up on b ecoming empt y . But not ev ery real pack et transmission is effected by a dummy pac ket transmission from the j th queue. Dumm y transmissions are designed only to cause in terference but the successful transmission of a dumm y pack et from the queue j has no significance, i.e., queue length Q j is unaffected. An interesting p oint and the main asp ect in whic h our dominant system S 2 differs from the previous constructions is that different queues hav e differen t sets of p ersisten t and non-p ersistent queues in the same time slot . F rom the discussion made ab ov e, the queue length ev olution in the dominan t system S 2 can now b e represented as Q n +1 j = Q n j + Λ n j − D n j D n j = Y k ∈U j (1 − Y n k I { Q n k > 0 } ) Y n j I Q n j > 0 Y k ∈V j (1 − Y n k ) (7) F or the queue-length vector Q , we define u j ( Q ) as the probabilit y that no real pac ket is transmitted from the queues of the set U j . That is u 1 ( Q ) = 1 u j ( Q ) = j − 1 Y k =1 (1 − p k I { Q k > 0 } ) for j ≥ 2 Similarly , v j ( Q ) will b e defined as the probabilit y that neither a real pac ket trans- mission nor a dumm y pac ket transmission will o ccur from the queues of the set V j , i.e., v j ( Q ) = J Y k = j +1 p k for 1 ≤ j ≤ J − 1 v J ( Q ) = 1 12 W e note here that v j ( Q ) is queue-length indep endent and u j ( Q ) is queue-length de- p endent . Likewise, we define the suc c ess pr ob ability r j ( Q ) of the j th queue as r j ( Q ) = u j ( Q ) p j v j ( Q ) I { Q i > 0 } Define the success probability ve ctor r ( Q ) = ( r 1 ( Q ) , r 2 ( Q ) , . . . , r J ( Q )). F or the sake of notational conv enience, henceforth, w e denote the more expressive notation u j ( Q ), v j ( Q ), r j ( Q ), and r ( Q ), resp ectively , as simply u j , v j , r j , and r , as long as no am biguit y is caused. Some times we ma y also write u j ( r ) in place of u j ( Q ) or u j . F rom the knowledge of r , we can immediately tell whic h queues are empt y and which queues are non-empt y and hence indices of the non-empty queues in the U j . Then it b ecomes straigh tforw ard to write down the v alue of u j ( r ). Also, in the rest of this pap er, w e will prefer the more con venien t notation Q j in place of Q n j unless explicit emphasis on the time slot is needed, and w e extend this rule to other v ariables to o. With the help of the notation introduced so far, we now state our central result on stability of the slotted-Aloha proto col. Prop osition 3.1 L et η = ( η 1 , η 2 , . . . , η J ) denote a p ermutation of the set { 1 , 2 , . . . , J } . Define C ( η ) ⊂ R J + to b e the set of λ that satisfies λ η j p η j v η j + I { j ≥ 2 } j − 1 X k =1 λ η k v η k < 1 , for 1 ≤ j ≤ J Define C = ∪ η C ( η ) . Then the dominant system S 2 is stable for λ ∈ C . Since stabilit y of S 2 implies stabilit y of S 1 b ecause of queue length dominance, w e conclude that the original system S 1 is also stable for λ that satisfies the conditions of Prop osition 3.1. In Figure 1, w e show a p ortion of the stabilit y region C when J = 3. W e will now sp ecialize Prop osition 3.1 for J = 2 , 3, and J → ∞ . F or J = 2, we ha ve C ( { 1 , 2 } ) = λ : λ 1 p 1 p 2 < 1 and λ 1 p 2 + λ 2 p 2 < 1 C ( { 2 , 1 } ) = λ : λ 2 p 1 p 2 < 1 and λ 1 p 1 + λ 2 p 1 < 1 Then C = C ( { 1 , 2 } ) ∪ C ( { 2 , 1 } ) reduces to the exact stability condition derived by Tsy- bak ov and Mikhailo v [2]. Let us now consider J = 3. W e hav e a total of six p erm utations of the set of queues { 1 , 2 , 3 } and the corresp onding sufficient conditions for stability are as follo ws: C ( { 1 , 2 , 3 } ) = λ : λ 1 p 1 p 2 p 3 < 1 λ 2 p 2 p 3 + λ 1 p 2 p 3 < 1 λ 3 p 3 + λ 2 p 3 + λ 1 p 2 p 3 < 1 13 C ( { 1 , 3 , 2 } ) = λ : λ 1 p 1 p 2 p 3 < 1 λ 3 p 2 p 3 + λ 1 p 2 p 3 < 1 λ 2 p 2 + λ 3 p 2 + λ 1 p 2 p 3 < 1 C ( { 2 , 3 , 1 } ) = λ : λ 2 p 2 p 1 p 3 < 1 λ 3 p 3 p 1 + λ 2 p 1 p 3 < 1 λ 1 p 1 + λ 3 p 1 + λ 2 p 1 p 3 < 1 C ( { 2 , 1 , 3 } ) = λ : λ 2 p 2 p 1 p 3 < 1 λ 1 p 1 p 3 + λ 2 p 1 p 3 < 1 λ 3 p 3 + λ 1 p 3 + λ 2 p 1 p 3 < 1 C ( { 3 , 2 , 1 } ) = λ : λ 3 p 3 p 1 p 2 < 1 λ 2 p 2 p 1 + λ 3 p 1 p 2 < 1 λ 1 p 1 + λ 2 p 1 + λ 3 p 1 p 2 < 1 C ( { 3 , 1 , 2 } ) = λ : λ 3 p 3 p 1 p 2 < 1 λ 1 p 1 p 2 + λ 3 p 1 p 2 < 1 λ 2 p 2 + λ 1 p 2 + λ 3 p 1 p 2 < 1 Eac h of these six sufficien t conditions for J = 3 strictly include the resp ectiv e sufficien t conditions derived in Rao and Ephremides [4]. F or the asymptotic case of J → ∞ and symmetric arriv al rates and transmission probabilities (i.e., λ j = λ and p j = p ), our result recov ers the w ell known result [12] that the system is unstable. 3.3 P ositiv e Recurrence of the Queue Length Pro cess { Q n , n ≥ 1 } W e no w prov e Prop osition 3.1 for the particular permutation η = (1 , 2 , . . . , J ). The pro of consists of v erifying v alidit y of the Assumptions 2.1, 2.2, and 2.3 of Theorem 2.1 for the Marko v c hain { Q n , n ≥ 1 } . Then Theorem 2.1 implies the sufficiency condition of Prop osition 3.1. But to facilitate the presentation, w e need to introduce some more notation. W e sa y that Q and Q 0 are “comp onen t-wise” partially ordered and write Q Q 0 if Q j ≤ Q 0 j for 1 ≤ j ≤ J . 14 0 0.05 0.1 0.15 0.2 0.25 0.3 0.35 0 0.05 0.1 0.15 0.2 0.25 0.3 0.35 0.4 0.45 0.5 0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 B Q β Y E λ 1 α O C F X γ P λ 2 A λ 3 Figure 1: Figure sho ws the sufficiency conditions for stabilit y for the permutations { 3 , 2 , 1 } and { 3 , 1 , 2 } . In the figure, A = ( p 1 , 0 , 0), B = (0 , p 2 , 0), C = (0 , 0 , p 3 ), O = ( p 1 p 2 p 3 , p 1 p 2 p 3 , p 1 p 2 p 3 ), α = ( p 1 p 2 , p 1 p 2 , 0), β = (0 , p 2 p 3 , p 2 p 3 ), γ = ( p 1 p 3 , 0 , p 1 p 3 ), P = ( p 1 p 2 , 0 , 0), Q = (0 , p 1 p 2 , 0), X = ( p 1 p 3 , 0 , p 1 p 2 p 3 ), Y = (0 , p 2 p 3 , p 1 p 2 p 3 ), E = (0 , p 1 p 2 p 3 , p 1 p 2 p 3 ), F = ( p 1 p 2 p 3 , 0 , p 1 p 2 p 3 ). When λ 3 = 0, the stabilit y region is confined to λ 1 λ 2 -plane and the corresponding stabilit y region boundary is described b y the line segmen ts Aα and B α . Similarly , the line segments Aγ and C γ together represen t the b oundary of the stabilit y region when λ 2 = 0, and the line segments B β and C β together represen t the b oundary of the stability region when λ 1 = 0. F or λ 3 < p 1 p 2 p 3 , the plane segmen t AαO X , bearing the plane equation λ 1 p 1 + λ 2 p 1 + λ 3 p 1 p 2 = 1 and the plane segment QαO E , b earing the plane equation λ 2 p 1 p 2 + λ 3 p 1 p 2 = 1, together describ e the sufficiency condition for stability . 15 W e note that the distribution of the departure random v ariable D j is p ( D j = 1) = r j = 1 − p ( D j = 0). Hence follows that E ( D j ) = r j (8) Define R to b e the set of all success probability v ectors, i.e. R = r ( Q ) : Q ∈ Z J + . F or 1 ≤ j ≤ J , we define a partition {R j , R c j } of the set R as R j = { r ∈ R : r j = 0 } and R c j = { r ∈ R : r j > 0 } Define the mapping g : Z J + → R by g ( Q ) = ( r 1 ( Q ) , r 2 ( Q ) , . . . , r J ( Q )), where g ( Q ) is the v ector of success probabilities when the queue length vector is Q . Since the kno wledge of whic h queues are empt y and whic h queues are non-empt y alone is sufficien t to determine the success probability vector r , we can group all queue length vectors Q that result in the same r . This is done by defining the set-value d map g − 1 : R → Z J + as g − 1 ( r ) , Q ∈ Z J + : g ( Q ) = r W e note that the collection { g − 1 ( r ) , r ∈ R} of sets defines a partition of the space queue length vectors, Z J + . Next, w e prov e that there exist positive w eights suc h that the sum of weighte d exp e cte d numb er of dep artur es fr om the queues that b elong to the set { 1 , 2 , . . . , j } conditioned on the ev ent { Q j ≥ 1 } equals one, and when conditioned on the even t { Q j = 0 } , equals the probabilit y (1 − u j ) that there is at least one transmission from the set of queues U j . W e establish this fact for every j . F or brevity , let us define the random v ariable ˆ D j = D j p j v j + I { j ≥ 2 } j − 1 X k =1 D k v k , 1 ≤ j ≤ J Lemma 3.1 E ˆ D j A = 1 − u j if A = { Q j = 0 } 1 if A = { Q j ≥ 1 } Pr o of: Suppose that for some k 1 and k 2 suc h that 1 ≤ k 1 < k 2 ≤ j ≤ J , let it b e true that (i) Q k 1 > 0 and Q k 2 > 0, and (ii) every other queue l , k 1 < l < k 2 , is such that Q l = 0. Then it is easy to note that u k 2 = p k 1 u k 1 . As a consequence, we can immediately note that u k 2 + p k 1 u k 1 = u k 1 . Then E ˆ D j Q j ≥ 1 ( a ) = u j + I { j ≥ 2 } j − 1 X k =1 p k u k I { Q k > 0 } ( b ) = 1 where ( a ) follows from (8) and ( b ) follo ws b y rep eatedly applying the observ ation made ab o ve. Almost on the similar lines, w e can also note that 16 E ˆ D j Q j = 0 = j − 1 X k =1 p k u k I { Q k > 0 } = 1 − u j No w, we are at a stage to verify the Assumption 2.1. T o verify the Assumption 2.1, consider the Lyapuno v functions V j , 1 ≤ j ≤ J , defined as V j ( Q ) = Q j v j p j + I { j ≥ 2 } j − 1 X k =1 Q k v k (9) Ov er the state space { Q j ≥ 1 } , the drift ∆ V j ( Q ) can b e written as ∆ V j ( Q ) = λ j v j p j + I { j ≥ 2 } j − 1 X k =1 λ k v k − E ˆ D j Q j ≥ 1 = λ j v j p j + I { j ≥ 2 } j − 1 X k =1 λ k v k − 1 (10) Lik ewise, the drift ∆ V j ( Q ) ov er the state space { Q j = 0 } can b e written as ∆ V j ( Q ) = λ j v j p j + I { j ≥ 2 } j − 1 X k =1 λ k v k − (1 − u j ) (11) where (10) and (11) follow from Lemma 3.1. W e now verify Assumption 2.2. Define A c j,k = { Q ∈ Z J + : Q j ≥ k } and A j,k = { Q ∈ Z J + : Q j < k } . W e can easily see that ∩ J j =1 A j,k is a finite set. W e can no w make an imp ortan t observ ation that with resp ect to the comp onen t-wise partial order the drift ∆ V j ( Q ) is a non-increasing function of the argumen t Q . T o see this, w e note that E ˆ D j is at most one and this v alue is attained when Q j ≥ 1 irresp ective of the size of other queues. When Q j = 0, E ˆ D j equals the probabilit y 1 − u j that there is at least one transmission from the set U j of queues. But for t wo states Q and Q 0 suc h that Q j = Q 0 j = 0 and Q ≤ Q 0 , the set of non-empty queues asso ciated with the queue length v ector Q is a subset of the set of non-empt y queues asso ciated with the queue length vector Q 0 . Hence the the probability that there is at least one transmission from the set U j of queues asso ciated with the state Q 0 is at le ast as lar ge as the corresp onding probabilit y associated with the state Q . In other words, for 1 ≤ j ≤ J , E ˆ D j is a non-decreasing function of the state Q , and hence the drift ∆ V j ( Q ) is a non-increasing function of the argumen t Q . These argumen ts essentially v erify the second part the Assumption 2.3. W e now pro v e that the stochastic recursiv e relation (7) that mo dels the queue lengths ev olution of the dominan t system S 2 is order preserving. Consider t w o queue length v ectors Q and Q 0 suc h that Q ≤ Q 0 . Then let us imagine tw o dominant systems of which the first one is started in state Q and the second one is started in state Q 0 but b oth are fed b y the iden tical input pro cesses { Y n , n ≥ 1 } and { Λ n , n ≥ 1 } . An ob vious inference is 17 that the set of non-empt y queues of U j ( Q ) is contained in the set of non-empty queues of U j ( Q 0 ). Hence a successful transmission from queue j corresp onding to the state Q need not imply a successful transmission from queue j of the state Q 0 . In other words, the queue lengths in the dominan t system corresp onding to the initial state Q 0 dominate the corresp onding queue lengths in the dominan t system corresp onding to the initial state Q , and hence the queue length ev olution (7) is order preserving. 3.4 Remarks on the Sufficien t Conditions for instabilit y of S 1 W e use the indistinguishability argument of [5] and [4] to derive sufficien t conditions for transience of the Marko v c hain. W e shall use a coupling argument to show that with p ositiv e probabilit y the dominan t system S 2 and the original system S 1 are indistinguish- able under the stated sufficient condition for transience of S 2 in Prop osition 3.2. Hence instabilit y of the dominant system S 2 also implies instabilit y of the original system S 1 . But b efore w e pro ceed further in this section, we state a sufficien t condition for transience in the context of Mark o v chains o v er a countable state space. Theorem 3.1 (Theorem 8.0.2 (i) of [13]) A n irr e ducible Markov chain over a c ount- able sp ac e X is tr ansient iff ther e exists a b ounde d non-ne gative function, V , and a non-empty set C ⊂ X such that for al l x ∈ C c , ∆ V ( x ) ≥ 0 , and ∃ x ∈ C c such that V ( x ) > sup y ∈ C V ( y ) . Prop osition 3.2 L et η = ( η 1 , η 2 , . . . , η J ) denote a p ermutation of the set { 1 , 2 , . . . , J } . Define D ( η ) ⊂ R J + to b e the set of λ that satisfies λ η 1 p η 1 v η 1 < 1 λ η j p η j v η j + j − 1 X k =1 λ η k v η k > 1 , for 2 ≤ j ≤ J Define D = ∪ η D ( η ) . Then the dominant system S 2 is unstable for λ ∈ D . Pr o of: Let 0 < θ < 1. F or each j , 2 ≤ j ≤ J , consider the Ly apunov function Z j ( Q, θ ) , 1 − θ V j ( Q ) , where V j ( Q ) is as defined in equation (9). First, we note that the Ly apunov function Z j ( Q, θ ) is b ounded. Define the drift ∆ Z j ( Q, θ ) as ∆ Z j ( Q, θ ) = X Q 0 ∈ Z J + h 1 − θ V j ( Q 0 ) − 1 − θ V j ( Q ) i p QQ 0 = X Q 0 ∈ Z J + θ V j ( Q ) − θ V j ( Q 0 ) p QQ 0 Differen tiating ∆ Z j ( Q, θ ) with resp ect to θ , we obtain d ∆ Z j ( Q, θ ) dθ = X Q 0 ∈ Z J + V j ( Q ) θ V j ( Q ) − 1 − V j ( Q 0 ) θ V j ( Q 0 ) − 1 p QQ 0 18 The following tw o observ ations are immediate: (i) ∆ Z j ( Q, 1) = 0 and (ii) d ∆ Z j ( Q, 1) dθ = P Q 0 ∈ Z J + ( V j ( Q ) − V j ( Q 0 )) p QQ 0 = − ∆ V j ( Q ) where ∆ V j ( Q ) is as defined in equations (10) and (11). Let us now supp ose that ∆ V j ( Q ) ≥ 0 o v er the entir e state space Z J + . Because ∆ Z j ( Q, θ ) is a differen tiable function of θ and also b ecause of the observ ation (i) and (ii) made ab ov e, there exists a 0 < θ ∗ < 1 suc h that ∆ Z j ( Q, θ ∗ ) > 0 ov er the state space Z J + . Hence the sufficiency condition stated in Theorem 3.1 for transience of the Mark ov c hain { Q n , n ≥ 1 } is satisfied. Finally , w e note that λ η j p η j v η j + P j − 1 k =1 λ η k v η k > 1 for 2 ≤ j ≤ J imply ∆ V j ( Q ) > 0 for 2 ≤ j ≤ J . Remarks: 1. The indistinguishability argumen t is based on the fact that the dominan t and the original are identical as long as the their queues do not empt y . 2. If our aim is to deriv e sufficient conditions for instabilit y of the dominant system S 2 , then the conditions stated in the Prop osition 3.2 are to o str ong . The requiremen t that λ j v j p j + I { j ≥ 2 } P j − 1 k =1 λ k v k > 1 for at le ast one j , 1 ≤ j ≤ J , is sufficient for instabilit y of S 2 . But w e require the conditions under which the dominant system S 2 is indistinguishable from the original system S 1 and hence the need for the requiremen t that λ j v j p j + I { j ≥ 2 } P j − 1 k =1 λ k v k > 1 for 2 ≤ j ≤ J . 4 Conclusion In this pap er, w e ha ve revisited the stability analysis of slotted-Aloha proto col with finite n umber of queues by applying Theorem 2.1 whic h is a generalization of the p ositive recurrence criterion due to Rosb erg [3]. An aim in this pap er has b een to illustrate ho w sto c hastic monotonicit y arguments in conjunction with Ly apunov-drift properties can b e used in establishing p ositiv e recurrence of a Marko v chain in a countable space setting. W e ha v e seen that t wo steps are inv olv ed in v erifying Theorem 2.1. The first step inv olv es verifying Assumptions 2.1 and 2.2. The second step is ab out verifying Assumption 2.3 and is also the stage where we in vok e sto chastic monotonicit y arguments of the underlying Marko v c hain. Our exp erience so far has b een that one of these tw o steps is hard to verify , if not b oth, dep ending on the problem. A simplifying feature of this p ositive recurrence criterion we b elieve is that it allows one to think of Lyapuno v- drift prop erties confined to certain pr op er subsets of the state space, which is relatively simpler, rather than the entire state space, whic h is harder. An interesting topic for further researc h on this problem w ould b e to pro vide tigh ter sufficiency conditions for transience of the proto col. References [1] P . Br ´ emaud. Markov chains: Gibbs fields, Monte Carlo simulation, and queues , v olume 31 of T exts in Applie d Mathematics . Springer-V erlag, New Y ork, 1999. [2] B. Tsybako v and W. Mikhailov. “Ergo dicity of Slotted ALOHA System”. Pr ob. In- form. T r ansm , 15(4):73–87, 1979. 19 [3] Z. Rosb erg. “A Positiv e Recurrence Criterion Asso ciated with Multidimensional Queueing Pro cesses”. Journal of Applie d Pr ob ability , 17(3):790–801, 1980. [4] R. Rao and A. Ephremides. “On the Stability of In teracting Queues in a Multi-access System”. IEEE T r ansactions on Information The ory , 34:918–930, Sept. 1988. [5] W. Szpanko wski. “Stabilit y Conditions for Some Multiqueue Distributed Systems: Buffered Random Access Systems”. A dvanc es in Applie d Pr ob ability , 26(2):498–515, Jun 1994. [6] W. Luo and A. Ephremides. “Stabilit y of N Interacting Queues in Random-access Systems”. IEEE T r ansactions on Information The ory , 45(5):1579–1587, 1999. [7] V. Anan tharam. “Stabilit y Region of the Finite-User Slotted ALOHA Proto col”. IEEE T r ansactions on Information The ory , 37(3):535–540, Ma y 1991. [8] C. Bordena ve, D. McDonald, and A. Proutiere. “Performance of Random Medium Access Control - An Asymptotic Approac h”. ACM Sigmetrics , 2008. [9] F. G. F oster. “On the stochastic matrices asso ciated with certain queueing pro- cesses”. A nn. Math. Statist , 24:355–360, 1953. [10] M. Shaked and J. G. Shantikumar. Stho chastic Or ders . Springer Series in Statistics. Springer. [11] V. Strassen. “The Existence of Probability Measures with Giv en Marginals”. A nn. Math. Statist. , 36:423–439, 1965. [12] G. F a yolle, E. Gelenbe, and J. Lab etolle. “Stability and optimal con trol of the pack et switc hing broadcast channel”. Journal of the ACM , 24(3):375–386, 1977. [13] S.P . Meyn and R.L. Tw eedie. Markov Chains and Sto chastic Stability . Springer V erlag, 1993. 20

Original Paper

Loading high-quality paper...

Comments & Academic Discussion

Loading comments...

Leave a Comment