A mixture model for unsupervised tail estimation

This paper proposes a new method to combine several densities such that each density dominates a separate part of a joint distribution. The method is fully unsupervised, i.e. the parameters in the densities and the thresholds are simultaneously estimated. The approach uses cdf functions in the mixing. This makes it easy to estimate parameters and the resulting density is smooth. Our method may be used both when the tails are heavier and lighter than the rest of the distribution. The presented model is compared with other published models and a very simple model using a univariate transformation.

💡 Research Summary

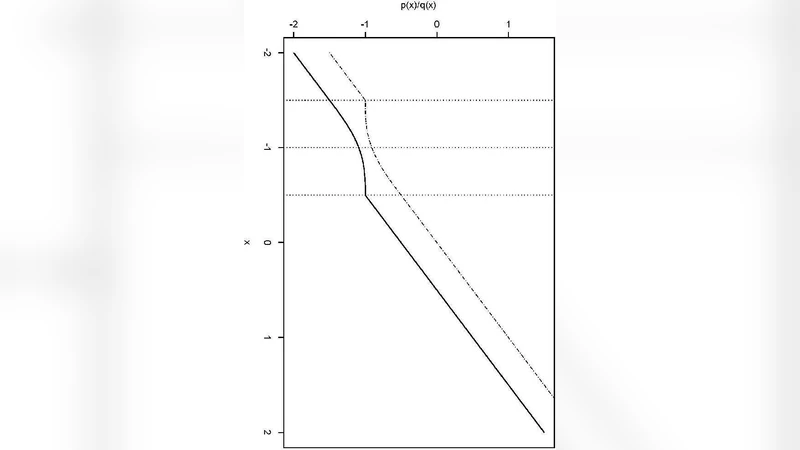

The paper addresses the long‑standing problem of accurately modeling the tails of a probability distribution, a task that is central to risk management, environmental statistics, and finance. Traditional tail‑estimation techniques typically separate the distribution into a “body” and a “tail” by imposing a pre‑specified threshold, then estimate the parameters of each part independently. This two‑step approach suffers from subjectivity in threshold selection, potential discontinuities at the boundary, and a lack of smoothness in the resulting overall density.

To overcome these drawbacks, the authors propose a novel mixture framework that blends several component densities using their cumulative distribution functions (CDFs). Let (f_k) and (F_k) denote the density and CDF of component (k) ((k=1,\dots,K)). The overall CDF is defined as

\

Comments & Academic Discussion

Loading comments...

Leave a Comment