Real time estimation in local polynomial regression, with application to trend-cycle analysis

The paper focuses on the adaptation of local polynomial filters at the end of the sample period. We show that for real time estimation of signals (i.e., exactly at the boundary of the time support) we cannot rely on the automatic adaptation of the local polynomial smoothers, since the direct real time filter turns out to be strongly localized, and thereby yields extremely volatile estimates. As an alternative, we evaluate a general family of asymmetric filters that minimizes the mean square revision error subject to polynomial reproduction constraints; in the case of the Henderson filter it nests the well-known Musgrave’s surrogate filters. The class of filters depends on unknown features of the series such as the slope and the curvature of the underlying signal, which can be estimated from the data. Several empirical examples illustrate the effectiveness of our proposal.

💡 Research Summary

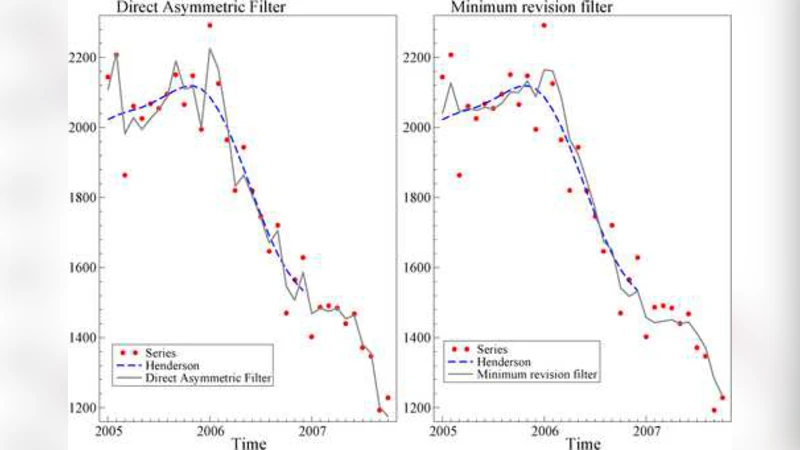

The paper addresses a fundamental problem in time‑series analysis: how to obtain reliable real‑time estimates of an underlying signal when only past observations are available. Local polynomial regression (LPR) – the workhorse behind many popular smoothers such as the Henderson filter – works well in the interior of a sample because it can use a symmetric kernel that balances information from both sides of the target point. At the end of the sample, however, symmetry is impossible; the filter must become asymmetric and rely solely on historical data.

The authors first demonstrate that the naïve “automatic adaptation” commonly employed – simply re‑computing the symmetric LPR coefficients using the available past observations – leads to a filter that is excessively localized. In practice this means that the real‑time estimate reacts too strongly to the most recent observation, producing a highly volatile series that is dominated by noise rather than by the true trend.

To overcome this, the paper proposes a general class of asymmetric filters that are derived by minimizing the mean‑square revision error (the expected squared difference between the real‑time estimate and the final two‑sided estimate) subject to two sets of constraints:

-

Polynomial reproduction constraints – the filter must exactly reproduce polynomials up to a chosen degree p (typically p = 3 for trend‑cycle analysis). This guarantees that low‑order trend components are preserved.

-

Signal‑feature constraints – the filter’s moments are forced to match the (unknown) first‑ and second‑order derivatives of the underlying signal, i.e., its slope and curvature. These quantities, denoted θ₁ and θ₂, are not known a priori but can be estimated from the data either once (pre‑estimation) or continuously (real‑time updating).

Formally, the filter weights w = (w₀,…,w_m) are obtained by solving

\

Comments & Academic Discussion

Loading comments...

Leave a Comment