Classification of interest rate curves using Self-Organising Maps

The present study deals with the analysis and classification of interest rate curves. Interest rate curves (IRC) are the basic financial curves in many different fields of economics and finance. They are extremely important tools in banking and financial risk management problems. Interest rates depend on time and maturity which defines term structure of the interest rate curves. IRC are composed of interest rates at different maturities (usually fixed number) which move coherently in time. In the present study machine learning algorithms, namely Self-Organising maps - SOM (Kohonen maps), are used to find clusters and to classify Swiss franc (CHF) interest rate curves.

💡 Research Summary

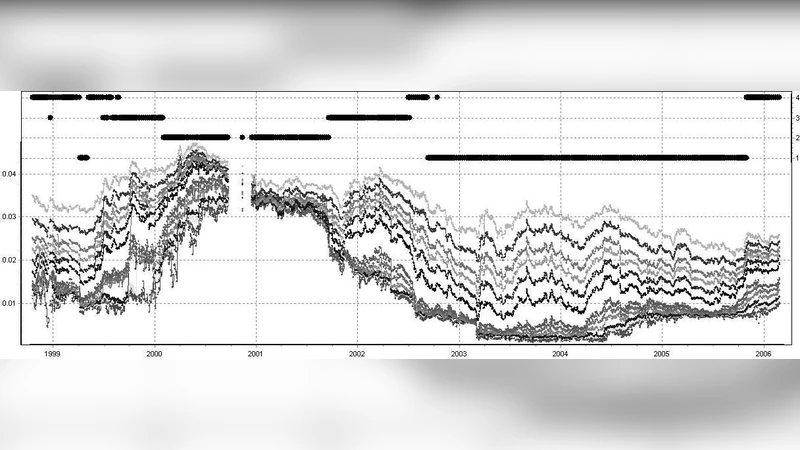

The paper investigates the classification of Swiss‑franc (CHF) interest‑rate curves (IRCs) by applying the Self‑Organising Map (SOM), a type of unsupervised neural network introduced by Kohonen. Interest‑rate curves, which consist of rates at a set of maturities (e.g., 1 month, 3 months, 6 months, 1 year, 2 years, 5 years, 10 years, 30 years), evolve together over time and encode the term structure of the market. Because the shape of an IRC reflects macro‑economic conditions, central‑bank policy, and market expectations, a reliable way to group similar curves can be valuable for risk management, portfolio construction, and economic forecasting.

Data and preprocessing

The authors use daily (or weekly) CHF IRC observations published by the Swiss National Bank. Each observation is transformed into an 8‑dimensional vector (one dimension per maturity). Missing values are linearly interpolated, and the entire dataset is standardized using a z‑score transformation to eliminate scale differences across maturities. No dimensionality reduction (e.g., PCA) is applied before feeding the vectors into the SOM, preserving the original shape information.

SOM architecture and training

A two‑dimensional rectangular lattice of 10 × 10 neurons (100 units) is chosen as the map. Initial weight vectors are drawn randomly. The training proceeds for 1,000 epochs, each epoch presenting the whole dataset in a shuffled order. For each input vector the best‑matching unit (BMU) is identified by Euclidean distance; the BMU and its neighbourhood (initial radius ≈ 3, decreasing exponentially) have their weight vectors moved toward the input according to a learning rate that also decays exponentially. This classic SOM schedule ensures that early iterations capture the global topology of the data, while later iterations fine‑tune local relationships.

Visualization and cluster extraction

After training, the authors compute the U‑matrix (distance matrix) to visualise inter‑neuron distances. The U‑matrix reveals clear valleys and ridges, indicating natural cluster boundaries. By overlaying the distribution of data points on the map, three to four major clusters become apparent. The clusters are characterised by their average curve shapes:

- Flat cluster – rates across maturities are roughly equal, typical of a stable macro‑environment.

- Steep (normal) cluster – short‑term rates are higher than long‑term rates, reflecting expectations of rising inflation or tighter monetary policy.

- Inverted cluster – long‑term rates fall below short‑term rates, a classic predictor of an upcoming recession.

- Mixed/transition cluster – occasional curves that display a pronounced hump or kink, often appearing during policy shifts.

For each cluster the authors compute the mean curve and the standard deviation across maturities, providing a quantitative picture of intra‑cluster volatility. The flat cluster shows low dispersion, while the steep and inverted clusters exhibit higher short‑term variability, suggesting different risk‑management implications.

Interpretation and implications

The SOM not only groups similar IRCs but also preserves the topological ordering of the clusters, allowing the authors to trace temporal transitions (e.g., a sequence of flat → steep → inverted) on the map. This visual trace can be interpreted as a market‑wide “state‑change” indicator, potentially useful for early warning systems. Moreover, because each cluster is associated with a distinct shape and volatility profile, portfolio managers can align asset‑allocation strategies (duration, convexity, hedging) with the prevailing cluster. For instance, during an inverted‑cluster regime, long‑duration bonds may be less risky due to lower long‑term volatility, whereas a steep‑cluster regime calls for heightened attention to short‑term funding costs.

Limitations

The study acknowledges several constraints. First, the choice of SOM hyper‑parameters (grid size, learning rate schedule, neighbourhood function) influences the granularity of the clusters; a systematic hyper‑parameter optimisation was not performed. Second, the dataset covers a limited historical window, which may not capture all possible market regimes (e.g., extreme crises). Third, SOM is inherently unsupervised, so the number of clusters emerges from the data rather than being predetermined, introducing a degree of subjectivity in interpreting the map. Finally, only pure IRCs are used; incorporating related instruments such as swaps, futures, or option‑implied volatilities could enrich the feature space.

Future research directions

The authors propose several extensions: (i) benchmarking SOM against other clustering techniques such as DBSCAN, HDBSCAN, or Gaussian mixture models to assess robustness; (ii) augmenting the input vectors with additional term‑structure instruments (swap spreads, forward rates, volatility surfaces) to capture a more comprehensive market picture; (iii) developing an online or incremental SOM that can update the map in real time as new data arrive; and (iv) coupling the SOM‑derived clusters with supervised forecasting models (e.g., LSTM networks) to predict future curve shapes or macro‑economic indicators.

Conclusion

Overall, the paper demonstrates that Self‑Organising Maps provide a powerful, intuitive framework for classifying interest‑rate curves without imposing strong parametric assumptions. By revealing coherent clusters that correspond to economically meaningful regimes, SOM can support risk‑management decisions, enhance market‑monitoring tools, and serve as a foundation for more sophisticated predictive models in fixed‑income analytics.

Comments & Academic Discussion

Loading comments...

Leave a Comment