Extreme Value Inference for CoVaR and Systemic Risk

We develop an extreme value framework for CoVaR centered on $v(q \mid p ; C)$, the copula-adjusted probability level, or equivalently, the CoVaR on the uniform (0,1) scale. We characterize the possible tail regimes of $v(q \mid p ; C)$ through the li…

Authors: Xiaoting Li, Harry Joe

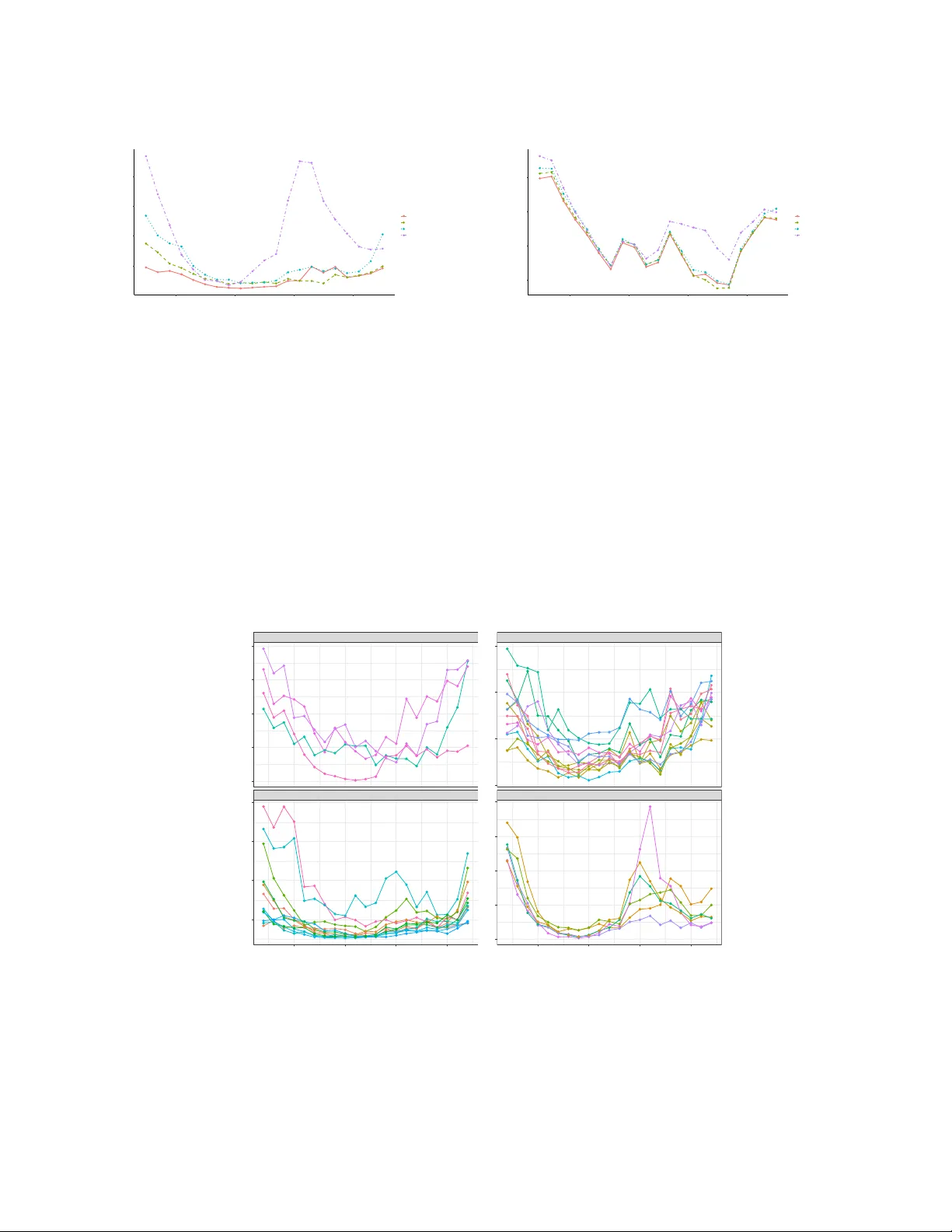

Extreme V alue Inference for CoV aR and Systemic Risk Xiaoting Li ∗ Departmen t of Statistics, Univ ersit y of Manitoba and Harry Jo e Departmen t of Statistics, Univ ersit y of British Colum bia Marc h 31, 2026 Abstract W e dev elop an extreme v alue framew ork for CoV aR cen tered on v ( q | p ; C ) , the copula-adjusted probabilit y level, or equiv alen tly , the CoV aR on the uniform (0,1) scale. W e c haracterize the p ossible tail regimes of v ( q | p ; C ) through the limit b ehavior of the copula conditional distribution and show that these regimes are determined b y the join t tail expansions of the copula. This leads to tractable conditions for iden tifying the tail regime and deriving the asymptotic b eha vior of v ( q | p ; C ) . Building on this characterization, we prop ose a minim um-distance estimation approach for CoV aR that accommo dates multiple tail regimes. The metho dology links CoV aR and ∆ CoV aR to the underlying joint tail b ehavior, thereby providing a clear in ter- pretation of these measures in systemic risk analysis. An empirical analysis across U.S. sectors demonstrates the practical v alue of the approach for assessing systemic risk contributions and exp osures with imp ortant implications for macroprudential surv eillance and risk management. K eywor ds: conditional quantiles, copulas, tail order, tail dep endence, extreme v alue theory ∗ The authors gratefully ackno wledge support from the Natural Sciences and Engineering Research Council of Canada. 1 1 In tro duction F rom a macroprudential view ( In ternational Monetary F und 2011 , Borio & Zh u 2012 ), systemic risk arises from the gradual buildup of financial imbalances, suc h as credit expansion, rising leverage, and concen trated asset exp osures. While these im balances do not immediately generate instability , they fundamentally alter how the system resp onds to severe sho c ks. In probabilistic terms, the buildup of systemic vulnerabilit y manifests as changes in the extremal dep endence structure of the system. The literature has dev elop ed a range of measures to quan tify systemic risk b y examining the system’s resp onse under stress ( Nolde & Zhou 2021 ). Among them, conditional V alue- at-Risk (CoV aR) ( A drian & Brunnermeier 2016 ) is defined as the system’s V alue-at-Risk conditional on the distress of a giv en institution. It has b een extensiv ely used in the literature to study systemic risk; see, e.g., F an et al. ( 2018 ), Ascorb eb eitia et al. ( 2022 ). By its probabilistic nature, CoV aR is an extreme conditional quan tile. The copula repre- sen tation of CoV aR has b een pro v en useful to study its theoretical prop erties; see, e.g., Bernard & Czado ( 2015 ), Li & Jo e ( 2026 ). It makes explicit how the extremal dep endence structure, captured b y the tail b eha vior of the joint copula, determines CoV aR through an adjusted probability lev el. This copula-adjusted lev el, denoted b y v ( q | p ; C ) , represents CoV aR on the uniform scale and lies at the core of our metho dology . Earlier works along this direction include Ja worski ( 2017 ) and Nolde et al. ( 2025 ), whic h deriv ed the limit of v ( q | p ; C ) as p ↓ 0 under asymptotic dep endence. Previous work in the copula literature, e.g., Hua & Joe ( 2011 ), Li & Jo e ( 2023 ), has dev elop ed a tail expansion framework to describe the extremal dep endence structure of m ultiv ariate random v ectors. Sp ecifically , a biv ariate copula C with a well b ehav ed join t low er tail is said to admit a lo wer tail expansion if there exist a tail order function 2 a ( w 1 , w 2 ) : (0 , ∞ ) 2 → (0 , ∞ ) , a tail order κ ≥ 1 , and a slo wly v arying function ℓ ( u ) such that, as u → 0 + , a ( w 1 , w 2 ) = lim u ↓ 0 C ( uw 1 , uw 2 ) u κ ℓ ( u ) . The tail b eha vior is further refined based on the tail order: C has strong tail dep endence if κ = 1 , intermediate tail dep endence if κ ∈ (1 , 2] , tail orthan t indep endence if κ = 2 , and sup er tail orthan t indep endence if κ > 2 . The recen t w ork Li & Jo e ( 2026 ) has established the v alue of tail expansions in analyzing the limiting behavior of v ( q | p ; C ) at the extreme quan tile lev el q = p for κ ∈ [1 , 2] . In this w ork, we prop ose an extreme v alue inference framew ork for CoV aR cen tered on this copula-adjusted probabilit y lev el. One main con tribution is to characterize the p ossible tail regimes, corresp onding to tail attraction, tail repulsion, and tail balance b et ween firm- lev el distress and system-wide loss, through the limiting b eha vior of the copula conditional distribution. W e then formally establish how these regimes are determined by tail expansions of the copula, thereb y pro viding tractable conditions for regime identification and for deriving the b eha vior of v ( q | p ; C ) . Building on this characterization, w e prop ose a minimum-distance estimation approac h for CoV aR ( q | p ) that accommo dates m ultiple tail regimes and establishes its asymptotic consistency . A similar approach w as used in Nolde et al. ( 2025 ) to estimate CoV aR ( q | p ) for the case q = p under the regime that we refer to as strong tail attraction. W e also in tro duce a ∆ CoV aR and derive its limiting b eha vior as p ↓ 0 . Unlike the ∆ CoV aR in earlier w orks such as Adrian & Brunnermeier ( 2016 ), Girardi & Ergün ( 2013 ), our copula-based form ulation isolates the effect of extremal dep endence from that of marginal v olatility . It aligns with the IMF’s macropruden tial view ( International Monetary F und 2011 ) of systemic risk and supp orts monitoring to ols that distinguish structural fragility from high-frequency mark et turbulence. 3 The rest of the pap er is organized as follows. Section 2 introduces the basic definitions and some prop erties of CoV aR and ∆ CoV aR . Section 3 and Section 4 presen t our main results on the b eha vior of CoV aR and ∆ CoV aR , resp ectively . Section 5 dev elops the estimation pro cedure and establishes its asymptotic prop erties. Section 6 demonstrates the empirical v alue of the prop osed metho dology through a comprehensiv e analysis of systemic risk in the U.S. mark et, highligh ting ho w extremal dep endence within the system shap es CoV aR and ∆ CoV aR and rev eals differences in the systemic roles of assets and institutions. Section 7 concludes with a brief discussion of the implications for macroprudential monitoring and risk managemen t. Proofs and technical details are provided in the supplementary material. 2 Basic definitions and prop erties of CoV aR Let ( X i , X S ) denote, resp ectiv ely , the return of institution i and the system-wide return. Their biv ariate distribution is F X i ,X S ( x, s ) = Pr ( X i ≤ x, X S ≤ s ) , for ( x, s ) ∈ R 2 , with con tinuous marginals F X i and F S . Define the generalized inv erse g ← ( u ) : = inf { x ∈ R : g ( x ) ≥ u } , where g ← = g − 1 = { x : g ( x ) = u } if g is strictly monotone. Definition 2.1. Fix a smal l p ∈ (0 , 1) and V aR i ( p ) = F ← X i ( p ) b e the individual p -level V aR. Define the c onditional distribution of X S given the str ess event { X i ≤ V aR i ( p ) } by F X S | X i ≤ V aR i ( p ) ( s ) = Pr X S ≤ s | X i ≤ V aR i ( p ) . The c onditional V alue-at-Risk of the system at level q ∈ (0 , 1) is CoV aR S | i ( q | p ) : = F ← S | X i ≤ V aR i ( p ) ( q ) . The CoV aR S | i ( q | p ) admits an equiv alen t copula representation. Let U i = F i ( X i ) and U S = F S ( X S ) . The asso ciated copula C iS , such that ( U i , U S ) ∼ C iS , is uniquely sp ecified, 4 for ( u, v ) ∈ (0 , 1) 2 , C iS ( u, v ) = F X i ,X S F ← X i ( u ) , F ← S ( v ) . F or each p ∈ (0 , 1) , define C S | i ≤ ( v | p ) : = Pr( U S ≤ v | U i ≤ p ) = C iS ( p, v ) p , v ∈ [ 0 , 1] . Then CoV aR S | i ( q | p ) = ( F S ◦ C S | i ≤ ( · | p )) ← ( q ) = V aR S v S | i ( q | p ; C iS ) , (1) and the copula-adjusted probability level is v S | i ( q | p ; C iS ) : = C ← S | i ≤ ( q | p ) = inf n v ∈ [ 0 , 1] : C S | i ≤ ( v | p ) ≥ q o . (2) This representation makes explicit ho w the dep endence structure of ( X i , X S ) , enco ded b y their join t copula C iS , will affect CoV aR via the adjusted probabilit y lev el. In other w ords, the copula reflects how the system’s return quan tiles shift under the stress ev ent. As emphasized in Adrian & Brunnermeier ( 2016 ), Girardi & Ergün ( 2013 ), systemic impact is better reflected by the shift in CoV aR than by the CoV aR lev el itself. F or this end, w e in tro duce the risk measure ∆ CoV aR . Unlik e the existing literature, w e use the unconditional V aR as the b enchmark for normal market conditions. As shown in Section 4 , this c hoice giv es ∆ CoV aR a clear interpretation in terms of the joint tail b eha vior of the risk v ariables and its effect on systemic risk. Definition 2.2 ( ∆ CoV aR) . ∆ CoV aR S | i ( q | p ) : = CoV aR S | i ( q | p ) − V aR S ( q ) | V aR S ( q ) | = V aR S v S | i ( q | p ; C iS ) | V aR S ( q ) | − 1 . Belo w are some basic prop erties of the copula-adjusted probability level, or CoV aR in the uniform (0,1) scale. F or the remainder, w e omit the subscript when there is no am biguity . If ( X i , X S ) has copula C , then ( − X i , − X S ) has its reflected or surviv al copula C ∗ ( u, v ) = u + v − 1 + C (1 − u, 1 − v ) ; ( − X i , X S ) has 1 -reflected copula, C 1 ∗ ( u, v ) = v − C (1 − u, v ) = u − C ∗ ( u, 1 − v ) ; ( X i , − X S ) has its 2 -reflected copula, C 2 ∗ ( u, v ) = u − C ( u, 1 − v ) . 5 Prop osition 2.3. (a) Comonotonicity: v ( q | p ; C + ) = pq . (b) Indep endenc e: v ( q | p ; C ⊥ ) = q . (c) Countermonotonicity: v ( q | p ; C − ) = 1 − (1 − q ) p. (d) Coher enc e: if C 1 ⪯ c C 2 (i.e. C 1 ( u, v ) ≤ C 2 ( u, v ) for al l ( u, v ) ) then for al l p, q , v ( q | p ; C 2 ) ≤ v ( q | p ; C 1 ) . (e) R efle ction: v ( q | p ; C ) = 1 − v (1 − q | p ; C 2 ∗ ) , v ( q | p ; C ∗ ) = 1 − v (1 − q | p ; C 1 ∗ ) . (f ) R ange: pq ≤ v ( q | p ; C ) ≤ q if C ⊥ ≺ c C ≺ c C + and q ≤ v ( q | p ; C ) ≤ 1 − (1 − q ) p if C − ≺ c C ≺ c C ⊥ . 3 T ail regimes of the copula-adjusted lev el in CoV aR This section studies the limiting b eha vior of the copula-adjusted probability level v ( q | p ; C ) , whic h is central to the copula representation of CoV aR in Eq. ( 1 ). W e show that, as p ↓ 0 , the limit of v ( q | p ; C ) is determined by the limit la ws of the conditional cumulativ e distribution function (cdf ) C S | i ≤ ( · | p ) whic h in turn induces a classification of tail regimes. W e then link these regimes to the join t tail b eha vior of the v ariables through the tail expansion of the copula, whic h yields a criterion to identify the tail regime and refined c haracterization of v ( q | p ; C ) . Section 3.1 and Section 3.2 treat, resp ectiv ely , the fixed q case and the extreme quantile case q = p . 3.1 T ail regimes of v ( q | p ; C ) for fixed q Theorem 3.1. Supp ose ther e exists a function A : (0 , 1) → [0 , 1] such that, for v ∈ (0 , 1) , lim p ↓ 0 C S | i ≤ ( v | p ) = A ( v ) . (3) 6 A ssume that the c onver genc e is lo c al ly uniform on (0 , 1) , i.e., for every 0 < a < b < 1 , sup v ∈ [ a,b ] C S | i ≤ ( v | p ) − A ( v ) − − → p ↓ 0 0 . Then the fol lowing hold: (i) A is non-de cr e asing and c ontinuous on (0 , 1) . (ii) A ( v ) extends to a pr op er distribution function supp orte d on [0 , 1] with p ossible jumps at 0 and 1 of sizes p 0 : = A (0 + ) , p 1 : = 1 − A (1 − ) , 0 ≤ p 0 , p 1 ≤ 1 , p 0 + p 1 ≤ 1 . With v ( q | p ; C ) define d in Eq. ( 2 ) , for every q ∈ (0 , 1) , lim p ↓ 0 v ( q | p ; C ) = 0 , 0 < q < p 0 A ← ( q ) ∈ (0 , 1) , p 0 < q < 1 − p 1 , pr ovide d A ← is c ontinuous at q 1 , 1 − p 1 < q < 1 . Remark 3.2. The b oundary c df lim u → 0 Pr ( U S ≤ v | U i = u ) has b e en studie d in Hua & Jo e ( 2014 ); it assumes that the c opula has a c ontinuous first-or der derivative with r esp e ct to u . The b oundary of C S | i ≤ ( v | u ) has not, to our know le dge, b e en studie d b efor e. It do es not r e quir e that the c opula have c ontinuous derivatives. When the c opula is c ontinuously differ entiable in u , the two b oundary c dfs c oincide in the limit as u → 0 , fol lowing fr om l’Hopital’s rule. ◁ Theorem 3.1 characterizes the p ossible tail regimes of v ( q | p ; C ) based on the structure of the limiting conditional distribution A . (i) T ail attraction If p 0 = 1 and p 1 = 0 , then the extended distribution of A ( v ) is a pure atom at 0 . Consequen tly , v ( q | p ; C ) → 0 , q ∈ (0 , 1) . 7 W e refer to this regime as tail attraction, as the extremely small v alues of U i pull U S to w ards the lo wer endp oin t 0 . (ii) T ail repulsion If p 0 = 0 and p 1 = 1 , then the extended distribution of A ( v ) is a pure atom at 1 . Consequen tly , v ( q | p ; C ) → 1 , q ∈ (0 , 1) . W e refer to this regime as tail repulsion, as conditioning on extremely small v alues of U i pushes U S a w ay from 0 and to w ard the opp osite endp oin t 1 . (iii) T ail balance If p 0 = p 1 = 0 , then the extended distribution of A ( v ) has no b oundary atoms, so all mass lies en tirely in the interior. In this case, v ( q | p ; C ) → A ← ( q ) ∈ (0 , 1) . W e call this regime tail balance, as extreme v alues of U i do not force U S to the b oundary but balance it in the in terior. (iv) Mixed tail regimes W e refer to the case as mixed tail regimes when the extended limiting distribution has at least one b oundary atom and is not a single p oint mass. It places mass p 0 at 0 , mass p 1 at 1 and the remaining 1 − p 0 − p 1 on the interior. The b eha vior of v ( q | p ; C ) exhibits mixed regimes dep ending on how the total mass is distributed b et w een the t w o b oundary atoms and the interior comp onent. A central contribution of this pap er is to link the b eha vior of the limiting conditional distribution A ( v ) with the joint tail expansion of the copula so that w e can characterize the asymptotic regimes of the quan tiles based on tail prop erties of the copula, i.e., the tail order and the tail dep endence function. In Prop osition 3.3 , we show ed that when the copula 8 has strong lo w er tail dep endence with κ = 1 , the conditional limit A ( v ) will ha v e a strictly p ositiv e mass at 0 with size equal to the limit of its tail dep endence function. Prop osition 3.3. A ssume the c opula C admits a lower tail exp ansion with a tail or der κ = 1 , as u ↓ 0 , C ( uw 1 , uw 2 ) u = b ( w 1 , w 2 ) + R ( u ; w 1 , w 2 ) , (4) in which R ( u ; w 1 , w 2 ) → 0 uniformly whenever uw 1 → 0 and uw 2 → 0 . The tail dep endenc e function b ( w 1 , w 2 ) is monotone and b ounde d with b ∞ : = lim r →∞ b (1 , r ) = sup r> 0 b (1 , r ) ∈ (0 , 1] . Then the function A define d in Eq. ( 3 ) satisfies A (0 + ) = b ∞ ∈ (0 , 1] . The results in the follo wing lemma aim to relate the b eha vior of v ( q | p ; C ) to the tail expansion of the copula and its 2-reflected copula. The pro of follows from the definition of C 2 ∗ . Lemma 3.4. L et C b e a bivariate c opula. Define its 2 -r efle ction C 2 ∗ ( u, v ) : = u − C ( u, 1 − v ) , ( u, v ) ∈ [ 0 , 1] 2 , which is the c opula asso ciate d with the r andom ve ctor ( X i , − X S ) . The c onditional distribution function C 2 ∗ S | i ≤ ( v | p ) : = Pr(1 − U S ≤ v | U i ≤ p ) = 1 − C S | i ≤ (1 − v | p ) . A ssume that for every v ∈ (0 , 1) , A ( v ) = lim p ↓ 0 C S | i ≤ ( v | p ) exists. Then A 2 ∗ ( v ) : = lim p ↓ 0 C 2 ∗ S | i ≤ ( v | p ) also exist and satisfy A 2 ∗ ( v ) = 1 − A (1 − v ) , v ∈ (0 , 1) . Theorem 3.5. A ssume the c opula C admits a lower tail exp ansion with tail or der κ ≥ 1 , C ( uw 1 , uw 2 ) u κ = a ( w 1 , w 2 ) ℓ ( u ) + R ( u ; w 1 , w 2 ) , u ↓ 0 , (5) 9 wher e ℓ is slow ly varying at 0 , R ( u ; w 1 , w 2 ) → 0 uniformly whenever uw 1 → 0 and uw 2 → 0 . When κ = 1 , the exp ansion r e duc es to Eq. ( 4 ) and the tail or der function a c oincides with the tail dep endenc e function b . A ssume in addition, the fol lowing b oundary c onditions on the tail or der function, (B1) A s r ↓ 0 , a (1 , r ) = a 1 r + o ( r ) for some c onstant a 1 > 0 . (B2) If κ = 1 , let H ( r ) = a (1 , r ) , which is c ontinuous and strictly incr e asing on (0 , ∞ ) , with lim r ↓ 0 H ( r ) = 0 , lim r →∞ H ( r ) = b ∞ ∈ (0 , 1] . If κ > 1 , then a (1 , r ) = O ( r ρ ) for some 0 < ρ ≤ κ − 1 as r → ∞ . Then the fol lowing hold. (i) The limiting c onditional c df A has a strictly p ositive mass at 0 , i.e. A (0 + ) > 0 , if and only if C has str ong lower tail dep endenc e, i.e., κ = κ ( C ) = 1 . Mor e over, when κ = 1 , A (0 + ) = b ∞ and for every q ∈ (0 , b ∞ ) , v ( q | p ; C ) ∼ H − 1 ( q ) p ↓ 0 . (ii) The limiting c onditional c df A has a strictly p ositive mass at 1 , i.e. 1 − A (1 − ) > 0 , if and only if the 2 -r efle cte d c opula C 2 ∗ has str ong lower tail dep endenc e, i.e., κ 2 ∗ = κ ( C 2 ∗ ) = 1 . In that c ase, 1 − A (1 − ) = b 2 ∗ ∞ , and for every q ∈ (1 − b 2 ∗ ∞ , 1) , v ( q | p ; C ) ∼ 1 − ( H 2 ∗ ) − 1 (1 − q ) p ↑ 1 . Remark 3.6. The c onclusion of the the or em r elies on two te chnic al c onditions, the uniform exp ansion of the c opula and gr owth r ate of the tail or der function. If the c onditions fail, the tail or der κ alone no longer determines the b oundary b ehavior of the limiting c onditional c df. It is p ossible to have κ > 1 while A (0 + ) > 0 and the c onditional quantiles c onver ge at non-p olynomial r ates that ar e not c aptur e d by the exp ansion use d in the the or em. The Gumb el c opula and the Gaussian c opula ar e two examples with tail or der κ > 1 and A in 10 Eq. ( 3 ) de gener ate at 0. F or these two families, the tail exp ansion in Eq. ( 5 ) is not uniform; the r emainder in the exp ansion inflates away fr om the diagonal. ◁ Copula κ A ( v ) v ( q | p ) v ( p ) Cla yton( θ > 0 ) 1 1 p ( q − θ − 1) − 1 /θ p 2 Gum b el ∗ ( δ > 1 ) 1 1 H − 1 ( q ; δ ) p p 2 IPS ∗ ( θ > 0 ) 1 + 1 θ 1 − e − F − 1 Γ ( v ; θ ) F Γ ( − ln(1 − q ); θ ) (Γ( θ + 1)) − 1 /θ p 2 − 1 /θ ( θ > 1) { Γ( θ + 1) } − 1 p θ (0 < θ < 1) F rank ( θ > 0 ) 2 (1 − e − θv )(1 − e − θ ) − 1 − 1 θ log(1 − q (1 − e − θ )) θ − 1 (1 − e − θ ) p Gum b el 2 ∗ ( δ > 1) 1 + δ 0 1 − exp n − ( δ q ) 1 /δ ( − log ( p )) 1 − 1 δ o ( δ p ) 1 /δ ( − log ( p )) 1 − 1 δ Cla yton 2 ∗ ( θ > 0) θ + 2 0 1 − ((1 − q ) − θ − 1) − 1 /θ p 1 − θ − 1 /θ p 1 − 1 /θ ( θ > 1) p 1 − θ (0 < θ < 1) T able 1: T ail order κ , limiting conditional cdf A ( v ) , copula-adjusted level v ( q | p ; C ) and v ( p ; C ) for common parametric copula families. A sup erscript ∗ denotes the reflected copula, 1 ∗ the 1 - reflected, and 2 ∗ the 2 - reflected copula. The IPS copula is an Arc himedean copula constructed from the integrated p ositive stable Laplace transform; see Section 4.11 of Jo e ( 2014 ) for details. Theorem 3.5 clarifies the link b et w een the b eha vior of A , v ( q | p ; C ) and the tail expansion of the copula. When the copula C has tail order 1 , the tail mass is asymptotically concentrated in the lo w er left corner. The limiting conditional cdf A has p ositiv e mass at 0 , and the conditional quan tiles con verge tow ard 0 at a linear rate in p . Con versely , if the 2-reflection of C has tail order 1 , then the tail mass is asymptotically concentrated in the upp er left corner. In that case, A assigns p ositive mass to 1 , and the conditional quantiles conv erge to w ard 1 at a linear rate in p . 11 Most common copula families fall into a single regime for v ( q | p ; C ) . T able 1 summarizes the tail order κ , the limiting conditional cdf A ( v ) , and the b ehavior of v ( q | p ; C ) for common copula families. The first tw o rows, corresp onding to the Clayton and reflected Gumbel copula families, b oth exhibit strong low er tail dep endence: A is degenerate at 0 , there is tail attraction for all q ∈ (0 , 1) , with v ( q | p ; C ) → 0 at a linear rate. The middle tw o rows, corresp onding to the reflected IPS and F rank copula families. In b oth cases κ > 1 , A ( v ) is strictly increasing, and v ( q | p ; C ) → A − 1 ( q ) for all q ∈ (0 , 1) , reac hing a tail balance. The last tw o rows corresp ond to 2 -reflected copula families, where the reflection op eration con v erts families with only p ositiv e dep endence to families with only negative dep endence. In these cases, A ( v ) is degenerate at 1 , and there is tail repulsion: v ( q | p ; C ) → 1 for all q ∈ (0 , 1) . The reflected I PS copula family has cdf C 2 ∗ ( u, v ; θ ) = u + v − F Γ ( x θ + y θ ) 1 /θ ; θ , x = F − 1 Γ ( u ; θ ) , y = F − 1 Γ ( v ; θ ) , θ > 0 , where F Γ ( · ; θ ) and F − 1 Γ ( · ; θ ) are the cdf and quantile functions for the Gamma ( θ , 1) distri- bution. It has negative dep endence for 0 < θ < 1 , indep endence for θ = 1 and p ositive dep endence for θ > 1 . The tail order is κ ( θ ) = 1 + θ − 1 > 1 . This family is useful for κ > 1 in (B2) of Theorem 3.5 . It can b e shown directly that its tail order function in Eq. ( 5 ) is a ( w 1 , w 2 ) = ( w 1 + w 2 ) κ − w κ 1 − w κ 2 with ℓ ( u ) = [ Γ( θ + 1)] 1 /θ /κ . Then a (1 , r ) ∼ κr κ − 1 as r → ∞ , so that the condition in (B2) is satisfied with ρ = κ − 1 . Mixed tail regimes arise when the tail mass is split b et w een the lo w er and upp er corners. This is less common among standard parametric copula families. The Studen t - t copula has tail order 1 in all four corners, which results in concen tration of tail mass in b oth the low er and upp er corners, and thus exhibits a mixed tail regime. Example 3.7. L et C ρ,ν b e the bivariate Student t ν c opula with c orr elation ρ ∈ ( − 1 , 1) and 12 de gr e es of fr e e dom ν > 0 . Its lower tail dep endenc e function is b ( w 1 , w 2 ; ρ, ν ) = w 1 T ν +1 n K h ρ − ( w 2 w 1 ) − 1 /ν io + w 2 T ν +1 n K h ρ − ( w 1 w 2 ) − 1 /ν io , wher e T ν +1 is the univariate t CDF with ν +1 de gr e es of fr e e dom and K = q ( ν + 1) / (1 − ρ 2 ) . L et H ( r ) = b (1 , r ; ρ, ν ) and H 2 ∗ ( r ) = b (1 , r ; − ρ, ν ) . F or v ∈ (0 , 1) , A ( v ) = sup r> 0 H ( r ) = T ν +1 ( ρK ) = q ∗ , and has a jump of size p 1 = 1 − q ∗ at 1 . It thus exhibits a mixe d tail r e gime dep ending on q . F or q < q ∗ , it has tail attr action v ( q | p ; C ) ∼ H − 1 ( q ) p → 0 . F or q > q ∗ , it has tail r epulsion, v ( q | p ; C ) ∼ 1 − ( H 2 ∗ ) − 1 (1 − q ) p → 1 . F or q = q ∗ , v ( q ∗ | p ; C ) → 1 2 . ◁ 3.2 T ail regimes of v ( q | p ; C ) for extreme-lev el q In systemic risk measurement, we are particularly in terested in extreme quantile levels, t ypically with the same tail probability used for b oth the institution and the system, i.e., q = p . Under this setting, Definition 2.1 simplifies to: CoV aR S | i ( p ) = V aR S ( v ( p ; C iS )) , and the adjusted lev el v ( p ; C iS ) = C ← S | i ≤ ( p | p ) . A k ey difference is that, under q = p , the right-hand-side target probabilit y b ecomes smaller order than p . Driving v ( p ) to the lo w er endp oin t, as a result, do es not require the same strength of tail concentration as in Section 3.1 . Theorem 3.8 derives the limit of v ( p ) based on the limiting conditional cdf, sho wing that v ( p ) → 0 holds broadly except in the degenerate case where mass concentrates in the upp er left corner, in whic h case higher-order terms determine the limit. Theorem 3.8. With A ( v ) define d in Eq. ( 3 ) , (i) If A (0 + ) = p 0 > 0 , as p ↓ 0 , v ( p ; C ) → 0 . 13 (ii) If A (0 + ) = p 0 = 0 and A (1 − ) = 1 − p 1 ∈ (0 , 1] , and v − = inf { v ∈ [0 , 1] : A ( v ) > 0 } = 0 , then as p ↓ 0 , v ( p ; C ) → 0 . (iii) If p 0 = 0 , p 1 = 1 , then A ( v ) = 0 for al l v ∈ (0 , 1) , it would dep end on the higher-or der terms. A ssume ther e exists δ > 0 , a non-de cr e asing function B : (0 , 1) → (0 , ∞ ) , and ℓ is slow ly varying with ℓ 0 : = lim p ↓ 0 ℓ ( p ) ∈ (0 , ∞ ) such that uniformly for v ∈ (0 , 1) C ( p, v ) = B ( v ) p 1+ δ ℓ ( p ) + o ( p 1+ δ ) . (a) 0 < δ < 1 : v ( p ; C ) → 0 . (b) δ = 1 : v ( p ; C ) → B ← ( ℓ − 1 0 ) if B ← is c ontinuous at ℓ − 1 0 . (c) δ > 1 : v ( p ; C ) → 1 . The next theorem c haracterizes the b eha vior of v ( p ; C ) using the lo w er tail expansion of the copula. It pro vides a criterion in terms of the tail order and yields explicit con vergence rates for v ( p ; C ) . The case of κ ∈ [ 1 , 2] has b een studied in Li & Jo e ( 2026 ). Theorem 3.9. A ssume the c opula C admits the lower-tail exp ansion as describ e d in The or em 3.5 . Then v ( p ; C ) → 0 ⇐ ⇒ 1 ≤ κ < 2 + ρ. Mor e over as p ↓ 0 , v ( p ; C ) = O ( p 3 − κ ) , 1 ≤ κ ≤ 2 , O ( p 1 − κ − 2 ρ ) , 2 < κ < 2 + ρ. The last column of T able 1 sho ws v ( p ; C ) for common copula families. Cla yton and reflected Gum b el copulas ha v e κ = 1 , so v ( p ) = O ( p 2 ) . The reflected IPS copula has tail order κ = 1 + 1 /θ and ρ = κ − 1 for (B2) of Theorem 3.5 ; then v ( p ) = O ( p 2 − 1 /θ ) when θ > 1 ( 1 < κ ≤ 2 ) and v ( p ) = O ( p 1 / ( κ − 1) ) = O ( p θ ) when 0 < θ < 1 ( 2 < κ < 2 + ( κ − 1) ). The F rank 14 copula has tail orthan t independence with κ = 2 for all −∞ < θ < ∞ , and hence v ( p ) = O ( p ) . The 2-reflected Gumbel and Cla yton copulas exhibit negativ e quadran t dep endence with κ > 2 . F or the former, it has 2 < κ < 2 + ρ for all δ > 1 , and v ( p ) = O ( p 1 /δ ( − log p ) 1 − 1 /δ ) ↓ 0 . F or the latter, 2 < κ < 2 + ρ when 0 < θ < 1 , so v ( p ) = O ( p 1 − θ ) when 0 < θ < 1 . Ho wev er, when θ > 1 , w e instead ha v e v ( p ) ∼ 1 − θ − 1 /θ p ( θ − 1) /θ ↑ 1 . 4 T ail limits of ∆ CoV aR and systemic risk implications In quan tifying systemic risk impact, the primary concern is its effect on extreme system losses. Therefore, ∆ CoV aR S | i ( q | p ) is most informative when ev aluated at small q . When q = p , Definition 2.2 reduces to ∆CoV aR S | i ( p ) = V aR S ( v ( p ; C )) − V aR S ( p ) | V aR S ( p ) | , whic h measures the p ercentage c hange in the system’s V aR under distress c onditions relativ e to normal conditions. Its b ehavior will dep end on the the limiting b eha vior of v ( p ) , determined b y the tail dep endence structure of the copula, and V aR , determined b y the marginal distribution of X S , as detailed in the following theorem. Theorem 4.1. L et ( X i , X S ) b e the r eturns of institution i and the system, with joint c df F X i ,S ( x, s ) = Pr( X i ≤ x, X S ≤ s ) = C iS ( F X i ( x ) , F X S ( s )) . A ssume that (A1) F S lies in the minimum-domain of attr action of a univariate gener alize d extr eme value (GEV) distribution with lower–tail index ξ = ξ S ≥ 0 . Henc e, as p ↓ 0 V aR S ( p ) ∼ − p − ξ L ∗ (1 /p ) , ξ > 0 , − H − 1 ( − log p ) , ξ = 0 . wher e L ∗ is slow ly varying at ∞ and H − 1 has extende d r e gular variation at ∞ with index γ ∈ (0 , ∞ ] . 15 (A2) The c opula C iS admits a lower exp ansion of Eq. ( 5 ) , with tail or der κ = κ iS ∈ [1 , 2 + ρ ) so that v ( p ; C ) b ehaves as describ e d in The or em 3.9 . Then, as p ↓ 0 , the fol lowing hold: (i) He avy mar ginal tail ( ξ > 0) ∆ CoV aR S | i ( p ) ∼ − p − (2 − κ ) ξ → −∞ , 1 ≤ κ < 2 , 1 − a − ξ 0 ∈ ( −∞ , 1) , κ = 2 , with a (1 , a 0 ) = 1 . 1 − p ( κ − 2) ξ ρ → 1 , 2 < κ < 2 + ρ. (ii) Light mar ginal tail ( ξ = 0) ∆ CoV aR S | i ( p ) → 1 − (3 − κ ) γ < 0 , 1 ≤ κ < 2 , 0 , κ = 2 , 1 − (1 − κ − 2 ρ ) γ ∈ (0 , 1] , 2 < κ < 2 + ρ. This result provides a clear in terpretation of ∆ CoV aR based on the joint tail b eha vior of the distribution, through the copula tail and the marginal tail. When the copula exhibits strong to in termediate tail dep endence (i.e., κ ∈ [1 , 2) ), ∆ CoV aR S | i ( p ) is ev entually negativ e. This reflects a risk amplification effect: under the distress of institution i , the system is pushed deep er in to the tail. The amplification factor is determined b y the marginal tail distribution. If F S lies in the F réchet domain ( ξ > 0) , the amplification scales as − p − (2 − κ ) ξ and diverges as p ↓ 0 . If F S lies in the Gumbel domain ( ξ = 0) , the amplification con v erges to the finite limit 1 − (3 − κ ) γ , with larger γ (faster gro wth of H − 1 ) pro ducing a stronger effect. When 2 < κ < 2 + ρ , which can occur with negativ e dependence, ∆ CoV aR S | i ( p ) is asymptotically p ositive. This reflects a risk atten uation effect: under the distress of institution i , the system’s tail losses b ecome less extreme. The atten uation factor is b et ween 16 0 and 1 , and tends to 1 when ξ > 0 . Note, when v ( p ) → 1 , the factor can exceed 1 or ev en div erges to ∞ . In the middle case with tail-orthant indep endence ( κ = 2) , if ξ = 0 then ∆ CoV aR S | i ( p ) → 0 , indicating that the system’s tail risk is asymptotically unc hanged. If ξ > 0 , the sign depends on the v alue of a 0 = lim p → 0 r ( p ; C ) . ∆ CoV aR S | i ( p ) is asymptotically negativ e when a 0 < 1 and p ositiv e when a 0 > 1 . 5 Estimation of CoV aR and its asymptotic prop erties Estimation of CoV aR, based on the copula representation in Eq. ( 1 ), inv olves estimating the marginal V alue-at-Risk (V aR) and the copula-adjusted level v ( q | p ; C ) . In this work, we prop ose a minimum-distance estimation approach for v ( q | p ; C ) , whic h represen ts CoV aR on the uniform scale, and can then be com bined with the marginal distribution to estimate CoV aR on the original scale. 5.1 Empirical estimators of tail dep endence Let { ( X i , Y i ) , i ∈ { 1 , 2 , . . . , }} b e an infinite sequence of indep enden t random vectors with common biv ariate distribution function F and univ ariate con tinuous margins F X , F Y . Denote b y X i : n b e the i -th smallest among the first n random v ariables { X 1 , . . . , X n } . Define the transformed v ariables U i = F X ( X i ) , and V i = F Y ( Y i ) and their empirical distribution function is C n ( u, v ) = 1 n n X i =1 1 { U i ≤ u, V i ≤ v } , u, v ∈ (0 , 1) . In practice, U i and V i are unobserved, w e replace them with pseudo-observ ations from ranks, U i,n = n − 1 n X j =1 1 ( X j ≤ X i ) , V i,n = n − 1 n X j =1 1 ( Y j ≤ Y i ) . 17 Using these pseudo-observ ations, the empirical copula function is b C n ( u, v ) = 1 n n X i =1 1 { U i,n ≤ u, V i,n ≤ v } , u, v ∈ (0 , 1) . Prop osition 5.1. L et C X Y b e the bivariate c opula of ( U i , V i ) = ( F X ( X i ) , F Y ( Y i )) . The c onditional c df is C Y | X ≤ ( v | p ) = C X Y ( p, v ) /p , for v ∈ (0 , 1) . L et p n = k n /n , and define the se quenc e of empiric al estimators, b A k n ,n ( v ) : = b C n ( p n , v ) p n = 1 k n n X i =1 1 U i,n ≤ k n n , V i,n ≤ v , v ∈ (0 , 1) . Supp ose ther e exists a function A : (0 , 1) → (0 , 1) such that as p ↓ 0 , sup v ∈ (0 , 1) C Y | X ≤ ( v | p ) − A ( v ) − → 0 . Then as n → ∞ , with k n → ∞ , k n /n → 0 , k n / √ n − → ∞ , sup v ∈ (0 , 1) b A k n ,n ( v ) − A ( v ) P − → 0 . Prop osition 5.2. Supp ose the c opula C X Y admits a lower tail exp ansion in Eq. ( 5 ) with tail or der κ = 1 and tail dep endenc e function b ( w 1 , w 2 ; C ) . With p n = k n /n , for fixe d ( w 1 , w 2 ) ∈ S 1 : = { ( w 1 , w 2 ) : w 1 > 0 , w 2 > 0 , w 1 + w 2 = 2 } , let b b k n ,n ( w 1 , w 2 ) : = b C n ( p n w 1 , p n w 2 ) p n = n k n n X i =1 1 U i,n ≤ k n n w 1 , V i,n ≤ k n n w 2 . Then as n → ∞ , k n /n → 0 , k n → ∞ , sup ( w 1 ,w 2 ) ∈S 1 b b k n ,n ( w 1 , w 2 ) − b ( w 1 , w 2 ; C ) P − → 0 . 5.2 Minim um distance estimation of CoV aR The prop osed estimation pro cedure is based on the classical principle of minimum distance estimation ( Parr & Sc hucan y 1982 ), where one fits a parametric mo del b y aligning it as 18 closely as p ossible to an empirical counterpart. A similiar idea has b een used in Einmahl et al. ( 2012 ) and Nolde et al. ( 2025 ) for extreme v alue estimation. F ollowing this general principle, we define a criterion function Q n ( θ ) as the integrated distance b et w een an empirical tail functional and its mo del-based counterpart, and estimate the parameter θ b y minimizing Q n ( θ ) . The choice of the tail functional is guided by the theoretical results established in Section 3 , whic h provides a basis to determine the regimes of v ( q | p ; C ) based on the tail order in the low er and upp er left corner, κ and κ 2 ∗ . With the assumptions in Theorem 3.5 , we consider the follo wing cases. (i) T ail attraction If κ = 1 and κ 2 ∗ > 1 , the tail mass is concen trated in the lo w er left corner. W e assume a parametric mo del for the tail dep endence function in the low er left corner b ( w 1 , w 2 ; θ ) with H ( r ) = b (1 , r ; θ ) → 1 as r → ∞ , and construct the criterion function Q k n ,n ( θ ) = Z S 1 b b k n ,n ( w 1 , w 2 ) − b ( w 1 , w 2 ; θ ) d w 1 d w 2 , (6) where b b k n ,n ( w 1 , w 2 ) is the empirical tail dep endence function defined in Proposition 5.2 . By Theorem 3.5 , the conditional quantiles can b e estimated as, for q ∈ (0 , 1) , ˆ v n ( q | p n ) = H − 1 ( q ; ˆ θ n ) · p n , (7) whic h con verges to 0 as p n → 0 . (ii) T ail repulsion If κ > 1 and κ 2 ∗ = 1 , the tail mass is concen trated in the upp er left corner, and w e will assume a parametric mo del for b ( w 1 , w 2 ; C 2 ∗ ) . The criterion function will b e constructed based on b b k n ,n ( w 1 , w 2 ) of the 2 -reflected data. By Theorem 3.5 , the conditional quan tiles can b e estimated by ˆ v n ( q | p n ) = 1 − ( H 2 ∗ ) − 1 (1 − q ; ˆ θ n ) · p n , 19 whic h con verges to 1 as p n → 0 . (iii) T ail balance If κ > 1 and κ 2 ∗ > 1 , then b y Theorem 3.5 , A ( v ) do es not ha ve any b oundary atoms. W e therefore assume a prop er parametric distribution A ( v ; θ ) and define the criterion function as Q k n ,n ( θ ) = Z 1 0 b A k n ,n ( v ) − A ( v ; θ ) d v , (8) where b A k n ,n is the empirical estimator for the conditional cdf defined in Prop osition 5.1 . The conditional quan tile at level q is then estimated b y in verting the fitted mo del: ˆ v n ( q | p n ) = A ← ( q ; ˆ θ n ) . (9) The three cases ab o v e fall in to a single tail regime, which co v ers the b eha vior of most parametric copula families. As discussed in Section 3 , ho wev er, mixed tail regimes ma y o ccur; for example, a tail order of 1 in b oth corners indicates a mixed regime. In this case, one could mo del using the first-order expansion of Student- t copula, as in Example 3.7 , and construct a criterion function that targets b oth corners, Q k n ,n ( ρ, ν ) = Z S 1 b b k n ,n ( w 1 , w 2 ) − b ( w 1 , w 2 ; ρ, ν ) + b b 2 ∗ k n ,n ( w 1 , w 2 ) − b ( w 1 , w 2 ; − ρ, ν ) d w 1 d w 2 . The next tw o theorems establish the consistency of ˆ v n ( q | p n ) , the estimator of CoV aR on the uniform scale. T o recov er CoV aR on the original scale, we can plug it in to a marginal quan tile estimator, suc h as \ CoV aR ( q | p n ) = b F − 1 S,n ˆ v n ( q | p n ) , whose consistency follows from the contin uous-mapping theorem, once the marginal quan tile estimator is uniformly consistent on a neighbourho o d of v ( q | p ; C ) . Theorem 5.3. A ssume the mo del A ( · ; θ ) for the b oundary c df is c orr e ctly sp e cifie d. 20 (A1) The p ar ameter set Θ ⊂ R p is non-empty, close d, and b ounde d (henc e c omp act). (A2) Ther e exists a true p ar ameter value θ 0 ∈ Θ such that lim p ↓ 0 C ( p, v ) p = A ( v ; θ 0 ) , uniformly in v ∈ (0 , 1) . (A3) F or every θ ∈ Θ , the function v 7→ A ( v ; θ ) is a pr op er distribution function on [0 , 1] , c ontinuous and strictly incr e asing on (0 , 1) . Mor e over, the mapping ( v , θ ) 7→ A ( v ; θ ) is jointly c ontinuous on [0 , 1] × Θ . (A4) F or every ε > 0 , inf ∥ θ − θ 0 ∥≥ ε Z 1 0 A ( v ; θ ) − A ( v ; θ 0 ) dv > 0 . L et ˆ θ n b e the minimizer of the criterion function in Eq. ( 8 ) , and the plug-in estimator of the extr eme c onditional quantile in Eq. ( 9 ) . Under A ssumptions (A1) to (A4) , as n → ∞ , k n → ∞ , p n = k n /n → 0 , and k n / √ n → ∞ , ˆ θ n P − → θ 0 , and for every fixe d q ∈ (0 , 1) , ˆ v n ( q | p n ) − v ( q | p n ; C ) P − → 0 . Theorem 5.4 treats the regime where v ( q | p ; C ) conv erges to zero. In this case, we establish consistency by showing the ratio conv erges to one in probabilit y . Theorem 3.1 in Nolde et al. ( 2025 ) presents a similar result for the adjustmen t factor in the case q = p . Theorem 5.4. A ssume the mo del for tail dep endenc e function b ( · ; θ ) is c orr e ctly sp e cifie d and assume d κ = 1 . (A1) The p ar ameter sp ac e Θ ⊂ R p is a c omp act subset. 21 (A2) Ther e exists a true p ar ameter θ 0 ∈ Θ ⊂ R p such that, for every ( w 1 , w 2 ) ∈ S 1 : = { ( w 1 , w 2 ) : w 1 > 0 , w 2 > 0 , w 1 + w 2 = 2 } , C ( uw 1 , uw 2 ) u = b ( w 1 , w 2 ; θ 0 ) + R ( u ; w 1 , w 2 ) , sup ( w 1 ,w 2 ) ∈S 1 | R ( u ; w 1 , w 2 ) | − − → u ↓ 0 0 . (A3) The map ( w 1 , w 2 , θ ) 7→ b ( w 1 , w 2 ; θ ) is c ontinuous on S 1 × Θ . (A4) F or every θ ∈ Θ the function H ( r ; θ ) : = b (1 , r ; θ ) , r > 0 , is a pr op er, absolutely c ontinuous distribution function on (0 , ∞ ) . (A5) F or every ε > 0 , inf { θ : ∥ θ − θ 0 ∥≥ ε } Z S 1 | b ( w 1 , w 2 ; θ ) − b ( w 1 , w 2 ; θ 0 ) | d w 1 d w 2 > 0 . L et ˆ θ n minimize the sample obje ctive Q k n ,n ( θ ) define d in Eq. ( 6 ) , and let ˆ v n ( q | p n ) b e the c onditional quantile estimator in Eq. ( 7 ) , Then, as n → ∞ , k n → ∞ , k n /n → 0 , ˆ θ n P − → θ 0 ; F or every fixe d q ∈ (0 , 1) , as p n → 0 , ˆ v n ( q | p n ) v ( q | p n ) P − → 1 . The finite-sample performance of the prop osed estimation approac h is assessed through an extensiv e sim ulation study . The parametric extreme v alue mo dels, along with detailed estimation pro cedures and results, are rep orted in Section B of the supplemen tary material. 22 6 Empirical systemic risk analysis This section applies the prop osed framework to empirical data from the U.S. financial mark et. The goal is to assess systemic risk contributions and exp osures using CoV aR and ∆ CoV aR, with an emphasis on how joint tail b eha vior and tail dep endence with the system shap e these measures and reveal differences in the systemic roles of assets and institutions. 6.1 CoV aR and ∆ CoV aR in the Copula-AR-GAR CH mo del Let R t = ( R ti , R tS ) denote the biv ariate return vector at time t , consisting of returns for institution i and the system S , for t = 1 , 2 , . . . , T . The return pro cess is adapted to the filtration {F t } T t =0 , generated by the observ ed history: F t : = σ ( R s : s ≤ t ) . Under the Copula-AR-GAR CH mo del ( Jondeau & Ro ckinger 2006 ): R tj = µ tj + σ tj Z tj , Z tj ∼ F Z j , j ∈ { i, S } , where: µ tj = E ( R tj | F t − 1 ) , σ 2 tj = V ar ( R tj | F t − 1 ) , and Z tj are standardized innov ations with marginal distribution F Z j . The AR and GARCH dynamics are giv en b y: µ tj = µ j + p j X k =1 ϕ j k R t − k,j , σ 2 tj = β 0 j + β 1 j Z 2 t − 1 ,j + β 2 j σ 2 t − 1 ,j . The join t conditional distribution of returns ( R ti , R tS ) is determined by the copula C iS linking the inno v ations: F R t ( r ti , r tS | F t − 1 ) = C iS F Z i r ti − µ ti σ ti , F Z S r tS − µ tS σ tS . Let the distress even t of institution i , giv en the past information, b e D i,t ( p ) : = n R ti ≤ V aR i | t ( p ) o and the enlarged information set b e the smallest σ -field that includes b oth the past market information and the even t that institution i is in distress: H i,t ( p ) : = F t − 1 ∨ σ ( D i,t ( p )) = σ ( F t − 1 ∪ { D i,t ( p ) } ) . 23 Then, the system CoV aR conditional on the information set H i,t ( p ) is CoV aR S | i,t ( p ) = µ tS + σ tS F − 1 Z S r S | i ( p ) · p (10) with the adjustmen t factor r S | i ( p ) = C ← S | i ≤ ( p | p ) /p. The time-v arying ∆ CoV aR is giv en b y ∆ CoV aR S | i,t ( p ) = CoV aR S | i,t ( p ) − V aR S | t ( p ) | V aR S | t ( p ) | = σ tS F − 1 Z S ( r S | i ( p ) · p ) − σ tS F − 1 Z S ( p ) | µ tS + σ tS F − 1 Z S ( p ) | . F or financial returns, the conditional mean µ tS is typically negligible relativ e to the tail quan tiles, so w e obtain, ∆ CoV aR S | i ( p ) ≈ F − 1 Z S r S | i ( p ) · p − F − 1 Z S ( p ) | F − 1 Z S ( p ) | , (11) and Theorem 4.1 would apply . The explicit form ulas clarify the main driv ers of the t w o risk measures and ho w they should b e in terpreted. CoV aR S | i,t ( p ) in Eq. ( 10 ) measures the absolute lev el of system loss conditional on institution i b eing in distress. As a high-frequency risk metric, it is largely driv en by changes in mark et volatilit y . ∆ CoV aR S | i ( p ) in Eq. ( 11 ), on the other hand, is determined more b y the dep endence and market regime, captured by the adjustmen t factor r S | i ( p ) and the tail index of F Z S . A smaller adjustment factor and a larger tail index b oth con tribute to a more negativ e ∆ CoV aR S | i , indicating a greater con tribution of firm-lev el distress to systemic risk. 6.2 Systemic risk impact of the financial sector A large literature, e.g., Bernal et al. ( 2014 ), do cuments the buildup of systemic risk in the financial sector b efore the 2008 crisis, and the sector remains cen tral to macroprudential regulation. Ho wev er, structural c hanges in the economy and the rapid expansion of the tec hnology sector raise the question of whether the systemic role of financial institutions has 24 0.06 0.07 0.08 0.09 2005 2010 2015 2020 Y ear Mean adjustment factor Sector broker−dealer depository insurance real−estate −1.4 −1.2 −1.0 −0.8 2005 2010 2015 2020 Y ear Mean Delta CoVaR Sector broker−dealer depository insurance real−estate Figure 1: Mean estimates of r S | i ( p ) (left) and ∆ CoV aR S | i ( p ) (righ t) for large U.S. financial institutions with p = 0 . 05 , segmented by dep ository , broker-dealers, insurance companies, and real estate firms. The estimates for r S | i ( p ) and ∆ CoV aR S | i ( p ) are calculated based on the daily log return data from June 2000 to June 2025 using five-y ear rolling window. insurance real−estate broker−dealer depository 2005 2010 2015 2020 2005 2010 2015 2020 0.050 0.055 0.060 0.065 0.05 0.07 0.09 0.11 0.13 0.0500 0.0525 0.0550 0.0575 0.0600 0.06 0.08 0.10 0.12 year adjustment factor Figure 2: P ath of the estimated adjustment factor r S | i ( p ) at p = 0 . 05 for 35 institutions that are consisten tly among the top 100 firms by market capitalization throughout 2000-2025. 25 shifted ov er time. W e address this question by estimating ∆ CoV aR S | i for large U.S. financial institutions, using the S&P 500 index as a proxy for the system. F or eac h rolling five-y ear windo w o v er 2000–2025, we iden tify the 100 largest firms b y market capitalization and mo del their daily returns using marginal AR-GARCH sp ecifications with sk ew- t inno v ations. Based on the resulting filtered innov ations, w e then estimate the adjustmen t factor r S | i ( p ) follo wing the pro cedure prop osed in Section 5 . Candidate mo dels are deriv ed from the tail expansions of parametric copulas listed in T able 1 , with further details provided in Section B.1 of the Supplemen tary Material. As discussed in Section 5.2 , the mo del c hoices are determined b y the tail regime. In practice, w e tell the regime based on the pair of empirical tail dep endence co efficients in the lo wer-left and upp er-left corners, ( ˆ λ, ˆ λ 2 ∗ ). A p ositiv e ˆ λ with ˆ λ 2 ∗ close to zero indicates tail attraction, in whic h case b ( w 1 , w 2 ) is mo deled using the low er tail dep endence function of the reflected Gum b el or Student- t copula. A p ositiv e ˆ λ 2 ∗ with ˆ λ close to zero indicates tail repulsion, and b ∗ 2 ( w 1 , w 2 ) is mo deled using the lo w er tail dep endence function of the Clayton copula. If b oth co efficients are close to zero, the regime is classified as tail balance, and A ( v ) is mo deled using the b oundary cdf of the reflected IPS copula. F ollowing the sim ulation exp erimen ts in the Supplementary Material, k n = 100 is used in the analysis. Fig. 1 rep orts the mean estimates of r S | i ( p ) and ∆ CoV aR S | i ( p ) at p = 0 . 05 , group ed b y Standard Industrial Classification (SIC) into depository institutions, brok er-dealers, insurance firms, and real estate firms. Fig. 2 as complemen tary to the aggregate view, sho ws the time path of r S | i ( p ) for institutions that remained in the top 100 b y market capitalization throughout 2000–2025. Ov erall, it suggests that the financial sector remains the ma jor contributor to systemic risk with the adjustment factors close to the lo w er b ound p = 0 . 05 (compare the comonotonicit y b ound in Prop osition 2.3 when q = p ) and large negativ e v alues of ∆ CoV aR S | i . Over time, 26 XL Y XLI QQQ VUG ARKW ARKQ SSO TQQQ UPRO C BAC WFC MS JPM GS AIG MET PNC SCHW BK AAPL MSFT AMZN GOOGL MET A ORCL NVDA AMD INTC AV GO QCOM −1.4 −1.2 −1.0 0.05 0.06 0.07 0.08 0.09 0.10 ETF Financial Tech XL Y XLI QQQ VUG ARKW ARKQ SSO TQQQ UPRO C BAC WFC MS JPM GS AIG MET PNC SCHW BK AAPL MSFT AMZN GOOGL MET A ORCL NVDA AMD INTC AV GO QCOM −1.4 −1.2 −1.0 0.05 0.06 0.07 0.08 0.09 0.10 ETF Financial Tech Figure 3: CoV aR S | i ( p ) v ersus the adjustment factor r S | i ( p ) at p = 0 . 05 for ma jor U.S. financial institutions, large technology firms, and equit y ETF s, based on daily returns for t w o sample p erio ds: 2012–2018 (left panel) and 2018–2025 (righ t panel). as sho wn in Fig. 2 , b oth banks and insurance firms exhibit a mild U-shap ed pattern: their systemic imp ortance rises from the early 2000s, p eaks around the financial crisis and its aftermath, and then declines gradually in recen t y ears. Real-estate firms, how ever, show a differen t pattern. Their systemic impact increases sharply in the y ears leading up to the crisis, declines mark edly afterward, and then remains relativ ely stable in recen t y ears. 6.3 Cross-sectional con tributions to systemic risk This section reveals cross-sectional differences in systemic risk con tributions among large- capitalization U.S. firms across ma jor sectors. Fig. 3 and Fig. 4 plot the estimated ∆ CoV aR S | i ( p ) against the adjustment factor r S | i ( p ) at p = 0 . 05 for firms spanning fi- nancials, tec hnology , consumer, energy , health care, real estate, and utilities ov er t wo sample p erio ds, 2012–2018 and 2018–2025. As in Fig. 3 , financial institutions and technology firms exhibit the strongest tail dep endence with the system, and this translates to strong tail attraction b et ween firm-level distress and system losses. It signals that these firms are likely systemically central: stress originating in them tends to transmit rapidly and in tensify system-wide tail losses, making them p otential originators and amplifiers of systemic risk. 27 KO GIS PM WMT PG PEP CL KMB MO PFE JNJ LL Y UNH MRK ABBV NEE DUK SO D AEP EXC XEL SRE DLR AMT EQIX VTR O PSA XOM CVX COP SLB OXY EOG −1.5 −1.0 −0.5 0.0 0.2 0.4 0.6 Consumer Energy Health care Real estate Utilities KO GIS PM WMT PG PEP CL KMB MO PFE JNJ LL Y UNH MRK ABBV NEE DUK SO D AEP EXC XEL SRE DLR AMT EQIX VTR O PSA XOM CVX COP SLB OXY EOG −1.5 −1.0 −0.5 0.0 0.2 0.4 0.6 Consumer Energy Health care Real estate Utilities Figure 4: ∆ CoV aR S | i ( p ) versus the adjustmen t factor r S | i ( p ) at p = 0 . 05 for firms across consumer, energy , health care, real estate, and utilities sectors, based on daily returns for t w o sample p erio ds: 2012–2018 (left panel) and 2018–2025 (righ t panel). Firms from the other sectors, as sho wn in Fig. 4 , also exhibit negative ∆ CoV aR S | i , indicating a p ositive contribution to systemic risk. But their tail behaviors are more heterogeneous, com bining b oth tail attraction and tail balance, and their adjustment factors and ∆ CoV aR S | i span a wider range. In Fig. 3 , w e notice that the entities with the most negative ∆ CoV aR S | i are large equit y exc hange-traded funds (ETF s) and m utual funds. As discussed in financial literature ( Ramasw am y 2011 ), these in vestmen t vehicles t ypically do not originate distress, but they act as imp ortan t channels that amplify systemic losses. Comparing the tw o p erio ds, ∆ CoV aR S | i exhibits an ov erall upw ard shift. This c hange is b ecause the innov ation distribution has a less hea vier tail in 2018-2025 compared to 2012- 2018. The b ehavior of r S | i ( p ) rev eals changes in the dep endence structure. In particular we observ e a clear reordering of systemic imp ortance. In 2012–2018, systemic risk contributions are dominated b y financial institutions, while most tec hnology firms, aside from a few exceptionally large firms suc h as Microsoft and Go ogle, ha v e relatively mo dest impacts. This pattern changes markedly in 2018–2025, with systemic imp ortance shifting to ward the tec hnology sector and a w ay from financial firms. As sho wn in Fig. 4 , this trend is particularly evident for companies such as NVIDIA, AMD, and Broadcom, which hav e 28 IEF TL T SHY VGIT VGL T AGG BND TIP SCHP UUP UDN FXY FXF FXE FXB GLD SL V PPL T USO UNG DBC DBA −1.5 −1.0 −0.5 0.0 0.5 1.0 0 2 4 6 8 Commodities Fixed income Fx currency IEF TL T SHY VGIT VGL T AGG BND TIP SCHP UUP UDN FXY FXF FXE FXB BTC−USD SOL−USD XMR−USD L TC−USD ADA−USD GLD SL V PPL T USO UNG DBC DBA −1.5 −1.0 −0.5 0.0 0.5 1.0 0 2 4 6 8 Commodities Crypto Fixed income Fx currency Figure 5: ∆ CoV aR i | S ( p ) v ersus the adjustment factor r i | S ( p ) at p = 0 . 05 for fixed income securities, crypto currency , commo dities, computed based the daily returns from 2012–2018 (left panel) and 2018–2025 (right panel). expanded rapidly with surging demand for AI infrastructure. This shift is consisten t with the findings in Section 6.2 , which indicate a declining systemic impact of the financial sector. At the same time, it p oin ts to an emerging source of systemic risk in the technology sector, particularly among firms closely tied to the AI b o om. 6.4 Systemic risk exp osures and hedging assets The ∆ CoV aR in Eq. ( 11 ), when conditioning on system-wide distress, measures an asset’s exp osure to systemic risk. A v alue near zero indicates that the asset’s low er-tail distribution is largely unaffected b y systemic stress while a large p ositive ∆ CoV aR i | S implies that the asset tends to gain v alue when the system is under distress. This information is useful for p ortfolio risk management as CoV aR i | S can help in vestors and risk managers iden tify assets that improv e p ortfolio resilience during episodes of system-wide stress. Fig. 5 and Fig. 6 plot the estimated ∆ CoV aR i | S ( p ) against r i | S ( p ) at p = 0 . 05 , for a wide range of assets including fixed income securities, commo dities, and crypto currencies based on daily returns ov er 2012–2018 and 2018–2025. F or structured hedging instrumen ts sho wn in Fig. 6 , w e observ e strong tail repulsion and large p ositiv e ∆ CoV aR i | S . Some of these instrumen ts are explicitly designed to mov e against 29 VIXY VIXM DOG PSQ RWM TZA HDGE SJB BT AL 0.0 0.5 1.0 1.5 2.0 0 5 10 15 20 Hedge Instrument VIXY VIXM DOG PSQ RWM TZA HDGE SJB BT AL 0.0 0.5 1.0 1.5 2.0 0 5 10 15 20 Hedge Instrument Figure 6: ∆ CoV aR i | S ( p ) versus the adjustment factor r i | S ( p ) at p = 0 . 05 for hedging instrumen ts based on daily returns from 2012–2018 and 2018–2025. the system, such as inv erse equity ETF s and VIX - link ed pro ducts. Others provide protection through exp osure to sp ecific stress c hannels; for example, SJB, which holds short p ositions in high - yield corp orate b onds, gains from the deterioration of credit markets during systemic crises. Fig. 5 iden tifies sev eral natural hedging assets, including long-duration U.S. T reasury b ond ETF s (e.g., TL T, VGL T, and IEF) and currency ETF s (e.g., FXY, FXF). These assets exhibit w eak tail repulsion, or negativ e tail balance, indicating that they tend to appreciate or remain stable under systemic distress. The righ t panel of Fig. 5 rep orts the estimates for crypto currencies. Although these assets are often viewed as isolated from the traditional financial assets ( Corb et et al. 2018 ), our results show that they still display w eak tail attraction, or p ositiv e tail balance. In addition, their marginal tail indices are noticeably larger than those of other asset classes, p oin ting to greater exp osure to idiosyncratic extreme sho c ks. The sign reversal in the b ond-sto ck correlation has b een widely do cumented in the economics literature, see e.g., Campb ell et al. ( 2025 ), and is often link ed to shifts in the macro economic regime. Comparing the tw o panels of Fig. 5 suggest a similar change in tail dep endence. The r i | S ( p ) of fixed-income b onds and safe-ha ven currencies decreases and ∆ CoV aR i | S b ecomes less p ositive, and in some cases, turns negative. This indicates that their hedging 30 effectiv eness against systemic risk declines ov er time, with these assets increasingly comoving with system losses instead of offsetting them. 7 Discussion In this work, we dev elop a theoretical and inferential framew ork for conditional V alue-at-Risk (CoV aR) based on copula and extreme v alue theory . It clarifies how the tail dep endence structure determines the limiting b eha vior of CoV aR and ∆ CoV aR, thereb y providing a principled basis for interpreting these measures in systemic risk analysis. The pap er also con tributes an empirical analysis based on the prop osed framework, highlight- ing sev eral imp ortan t findings. Our results show that, although the financial sector remains the ma jor contributor to systemic risk, its impact has weak ened in recent years, coinciding with the rising systemic imp ortance of ma jor technology firms. F rom the p ersp ectiv e of macropruden tial regulation, this shift suggests an emerging source of systemic risk from the tec hnology sector. The 2007–2009 financial crisis illustrates how the repricing of housing assets b ecame systemic when comp ounded with the structure of the financial system. Our findings p oin t to a related but distinct concern: ev en though the sho c ks originate outside the traditional financial sector, they may generate system-wide effects as ma jor technology firms hav e b ecome deeply embedded in the system’s downside dep endence structure. An imp ortan t direction for future research is therefore to develop systemic risk monitoring and stress-testing frameworks that accoun t for the p oten tial repricing of AI-linked assets and their impacts for system-wide stability . Data a v ailabilit y statemen t The data used in this study were obtained through Wharton Researc h Data Services (WRDS) and Y aho o Finance. The replication pac kage, including the co de and instructions 31 for accessing the data, is av ailable in a GitHub rep ository . Disclosure statemen t The authors rep ort there are no comp eting in terests to declare. References A drian, T. & Brunnermeier, M. K. (2016), ‘CoV aR’, A meric an Ec onomic R eview 106 (7), 1705–1741. Ascorb eb eitia, J., F erreira, E. & Orb e, S. (2022), ‘The effect of dep endence on Europ ean mark et risk. a nonparametric time v arying approac h’, Journal of Business & Ec onomic Statistics 40 (2), 913–923. Bernal, O., Gnab o, J.-Y. & Guilmin, G. (2014), ‘Assessing the contribution of banks, insurance and other financial services to systemic risk’, Journal of Banking & Financ e 47 , 270–287. Bernard, C. & Czado, C. (2015), ‘Conditional quan tiles and tail dep endence’, Journal of Multivariate A nalysis 138 , 104–126. Borio, C. & Zhu, H. (2012), ‘Capital regulation, risk-taking and monetary p olicy: a missing link in the transmission mechanism?’, Journal of Financial Stability 8 (4), 236–251. Campb ell, J. Y., Pflueger, C. & Viceira, L. M. (2025), Bond-sto ck comov ements, T ec hnical rep ort, National Bureau of Economic Researc h. Corb et, S., Meegan, A., Larkin, C., Lucey , B. & Y aro v ay a, L. (2018), ‘Exploring the dynamic relationships b etw een cryptocurrencies and other financial assets’, Ec onomics L etters 165 , 28–34. 32 Einmahl, J. H. J., Kra jina, A. & Segers, J. (2012), ‘An M-estimator for tail dep endence in arbitrary dimensions’, The A nnals of Statistics 40 (3), 1764–1793. F an, Y., Härdle, W. K., W ang, W. & Zhu, L. (2018), ‘Single-index-based CoV aR with very high-dimensional co v ariates’, Journal of Business & Ec onomic Statistics 36 (2), 212–226. Girardi, G. & Ergün, A. T. (2013), ‘Systemic risk measuremen t: multiv ariate GAR CH estimation of CoV aR’, Journal of Banking & Financ e 37 (8), 3169–3180. Hua, L. & Jo e, H. (2011), ‘T ail order and in termediate tail dep endence of multiv ariate copulas’, Journal of Multivariate A nalysis 102 (10), 1454–1471. Hua, L. & Jo e, H. (2014), ‘Strength of tail dep endence based on conditional tail exp ectation’, Journal of Multivariate A nalysis 123 , 143–159. In ternational Monetary F und (2011), Global financial stabilit y rep ort: Grappling with crisis legacies, T echnical rep ort, In ternational Monetary F und, W ashington, DC. Ja w orski, P . (2017), ‘On conditional v alue at risk for tail-dep endent copulas’, Dep endenc e Mo deling 5 (1), 1–19. Jo e, H. (2014), Dep endenc e Mo deling with Copulas , CRC Press, Bo ca Raton, FL. Jondeau, E. & Ro ckinger, M. (2006), ‘The copula-GAR CH mo del of conditional dep endencies: An in ternational sto c k market application’, Journal of International Money and Financ e 25 (5), 827–853. Li, X. & Jo e, H. (2023), ‘Estimation of m ultiv ariate tail quantities’, Computational Statistics & Data A nalysis 185 , 107761. Li, X. & Jo e, H. (2026), ‘Prop erties of CoV aR based on tail expansions of copulas’, Journal of Multivariate A nalysis 211 , 105510. 33 Nolde, N. & Zhou, C. (2021), ‘Extreme v alue analysis for financial risk managemen t’, A nnual R eview of Statistics and Its A pplic ation 8 (1), 217–240. Nolde, N., Zhou, C. & Zhou, M. (2025), ‘T ail risk in the tail: Estimating high quan tiles when a related v ariable is extreme’, Journal of the A meric an Statistic al A sso ciation . P arr, W. C. & Sch ucany , W. R. (1982), ‘Minimum distance estimation and comp onents of go o dness-of-fit statistics’, Journal of the R oyal Statistic al So ciety Series B: Statistic al Metho dolo gy 44 (2), 178–189. Ramasw amy , S. (2011), Market structures and systemic risks of exc hange-traded funds, T echnical rep ort, Bank for In ternational Settlemen ts. 34

Original Paper

Loading high-quality paper...

Comments & Academic Discussion

Loading comments...

Leave a Comment