Proxy-Reliance Control in Conformal Recalibration of One-Sided Value-at-Risk

We introduce a proxy-reliance-controlled conformal recalibration framework for one-sided Value-at-Risk (VaR), and study a question that existing state-aware methods do not usually isolate: how strongly should the recalibration adjustment depend on an…

Authors: Tenghan Zhong

Pr o xy -R eliance Control in Conf ormal R ecalibration of One-Sided V alue-at-Risk T enghan Zhong, U niv ersity of Souther n Calif or nia tenghanz@usc.edu Abstract W e introduce a pro xy-reliance-controlled conf ormal recalibration framew ork f or one- sided V alue-at-Risk (V aR), and study a ques tion that exis ting state-a ware methods do not usuall y isolate: ho w strongl y should the recalibration adjustment depend on an imperfect v olatility pro xy? W e formalize this through a proxy -reliance parameter that continuously inter polates between an appro ximatel y constant-shift cor rection and a full y proxy -scaled cor rection. This mak es pro xy reliance a distinct and practicall y interpretable design choice in one-sided V aR recalibration. W e sho w theoretically that larg er proxy reliance increases the responsiv eness of the tail adjustment to pro xy scale, but also increases stressed-state fragility when the proxy under reacts. Empir ically , in rolling out-of-sample tests on a six-ETF panel with VIX -link ed state v ar iables, and with suppor ting evidence from SPY , w e find that the empirical value of pro xy-reliance control lies in improv ed stressed-state robustness rather than unif orm o verall dominance. In particular, when the baseline f orecast remains e xposed to pro xy imperfection in s tressed states, lo w er or inter mediate pro xy reliance can outper f or m fully pro xy-scaled recalibration in stressed left-tail V aR control. Ke yw ords: V alue-at-Risk; Conf ormal recalibration; V olatility pro xy; Mark et stress; T ail r isk JEL Classification: C53, G17, G32 1 1 Intr oduction V alue-at-Risk (V aR) remains a standard tool f or market r isk measurement and capital assess- ment, ev en as the Basel market-risk frame work has shifted inter nal-model regulation to ward e xpected shortfall and more risk -sensitiv e capital standards [ Basel Committee on Banking Supervision , 2019 ]. Y et reliable one-sided V aR control is especially difficult in the market conditions where protection matters most. Financial retur n distributions are nonstationary , tail beha viour chang es across regimes, and f orecast perf or mance can deteriorate sharply in stressed episodes. As a result, methods that appear acceptable in pooled co v erage may still f ail where do wnside protection is mos t needed. A natural response is to incorporate v olatility inf or mation into recalibration, but v olatility signals are not g round tr uth. In practice the y are inf ormative y et imper f ect, and their misspecification can become most consequential precisely in adverse states. R ecent conf or mal and state-a ware recalibration methods address nonstationarity by allo wing calibration to depend on time, state, or obser vation w eights. This is an impor tant advance, but it lea ves open a distinct question that is central in financial r isk management: when the state v ar iable itself is an imper f ect v olatility pro xy , ho w strongl y should the recalibration cor rection depend on it? Existing approac hes allo w state inf or mation to enter the recalibration procedure, but the y typicall y do not isolate the degree of dependence of the cor rection itself on pro xy scale as a separate design object. T o address this, we de v elop a pro xy-reliance-controlled conf or mal recalibration frame w ork f or one-sided left-tail V aR under imperfect v olatility signals. Let b 𝑞 𝛼, 𝑡 denote a baseline f orecast of the lo w er 𝛼 -quantile of ne xt-per iod retur ns, and let 𝑣 𝑡 denote a positiv e v olatility pro xy . Our frame w ork introduces a proxy -reliance parameter 𝜌 ∈ [ 0 , 1 ] through the scaling rule 𝑣 𝜌 𝑡 , so that 𝜌 = 0 cor responds to an approximatel y constant cor rection, 𝜌 = 1 cor responds to a full y pro xy-scaled cor rection, and intermediate values provide a continuous compromise betw een state responsiveness and protection from proxy misspecification. In this wa y , the framew ork makes e xplicit a design margin that is usually left implicit in state-a w are V aR methods: pro xy r eliance , namely , ho w strongl y the recalibration cor rection inherits the scale of an imper fect v olatility signal. 2 The paper makes three contributions. First, it identifies proxy reliance as a distinct design object in one-sided V aR recalibration and gives it a clear r isk -management interpretation: larg er v alues of 𝜌 increase state responsiv eness, but also increase e xposure to proxy er ror . Second, it sho w s theoretically that 𝜌 go v er ns both the sensitivity of tail adjustment to proxy scale and stressed-s tate fragility under s tress-specific pro xy under reaction. Third, it e v aluates this design margin empir ically in a rolling out-of-sample study on a six-ETF panel with VIX -linked state inf or mation, with SPY retained as an illustrativ e benchmark. The evidence sho w s that pro xy- reliance control is most valuable f or stressed-state robustness rather than broad unconditional dominance. In par ticular , when residual s tress-per iod underco v erage remains after the baseline f orecast is formed and the v olatility pro xy under reacts in adverse states, lo w er or intermediate pro xy reliance can outperf orm full y pro xy -scaled recalibration in left-tail control. W e also study a regime-aw are e xtension with separate proxy -reliance lev els across low -, medium-, and high-stress states, although its gains ov er simpler global s tress-a ware rules are limited and non-unif or m. The rest of the paper is organized as f ollo ws. Section 2 re vie w s the related literature. Section 3 descr ibes the data and f eature construction. Section 4 introduces the proxy -reliance- controlled recalibration framew ork and the regime-aw are e xtension. Section 5 presents the empirical results, including s tress-per iod anal y sis and pro xy misspecification e xperiments. Sec- tion 6 discusses the implications f or financial r isk management and outlines directions f or future research. Section 7 concludes. 2 Literature R e vie w 2.1 V aR F orecasting, Dynamic Quantiles, and Bac ktesting The V aR f orecasting literature includes historical simulation, volatility -filtered methods, para- metric conditional heteroskedas tic models, and quantile-based predictiv e regressions. Standard approaches include his torical simulation and volatility -updated or filtered his torical simulation, as w ell as G AR CH-type models that map time-varying v olatility into conditional q uantiles [ Engle , 1982 , Bollerslev , 1986 , Hull and White , 1998 , Barone-A desi et al. , 1999 , Christof- 3 f ersen , 2012 ]. Quantile reg ression pro vides a direct semiparametr ic alter native f or modelling conditional tail behaviour from obser ved predictors [ Koenk er , 2005 ], while the C A ViaR fam- il y models conditional quantile dynamics directl y and remains an important benchmark for tail-risk f orecasting [ Engle and Mang anelli , 2004 ]. More recent w ork e xtends the forecas ting frontier to w ard high-freq uency deep v olatility models, adaptiv e mac hine-learning prediction of the VIX, option-sur face-driv en v olatility f orecasting, multiv ariate por tf olio V aR –ES f orecast- ing, and f or w ard-looking phy sical tail-risk models [ Moreno-Pino and Zohren , 2024 , Bai and Cai , 2024 , Michael et al. , 2025 , S tor ti and W ang , 2025 , Zhang et al. , 2026 ]. A central difficulty in this literature is that acceptable unconditional co v erage does not guarantee reliable local per f ormance. F inancial applications also require attention to violation clustering and conditional adequacy , motivating standard backtesting tools such as the Kupiec unconditional co verag e test, the Christoffersen conditional co v erag e test, and dynamic q uantile diagnostics [ Kupiec , 1995 , Chr istoffersen , 1998 , Engle and Manganelli , 2004 ]. Our paper is related to this literature, but shifts attention a wa y from proposing another raw tail-f orecasting engine and to w ard the design of a recalibration la y er applied after the baseline f orecast is f or med. Once the f ocus mov es from tail f orecasting itself to post-hoc recalibration under nonstationarity , conf or mal methods become especially rele v ant because the y provide a model- agnostic frame w ork f or uncer tainty calibration under distributional instability . 2.2 Conf ormal Calibration under Dependence and Recent Financial Ap- plications Conf or mal prediction pro vides a dis tr ibution-free frame w ork f or uncer tainty quantification and model-agnostic recalibration [ V o vk et al. , 2005 , Angelopoulos and Bates , 2023 ]. While its classical guarantees rely on e x chang eability , a gro wing literature studies conf ormal methods under dependence and nonstationarity through w eighted, localized, adaptiv e, and sequential procedures [ Cher nozhuk ov et al. , 2018 , Gibbs and Cand ` es , 2021 , Bastani et al. , 2022 , X u et al. , 2024 ]. These dev elopments are especiall y relev ant in financial applications, where nonstationarity , heteroskedasticity , and regime shifts are intr insic rather than ex ceptional. R ecent w ork has begun to apply adaptiv e conf or mal methods directly to financial risk f ore- 4 casting. F or e xample, adaptiv e conf or mal inf erence has been used to compute V aR across lar ge panels of cr ypto-assets, emphasizing robustness under market instability . More recent w ork studies sequential one-sided V aR control through regime-w eighted conf or mal r isk control f or nonstationary por tf olio losses, while other recent studies dev elop temporal conf or mal predic- tion framew orks tailored to adaptiv e r isk f orecasting in financial time ser ies [ Fantazzini , 2024 , Aich et al. , 2025 , Schmitt , 2026 ]. Related recent work also pushes conf or mal methods to ward finance-specific decisions and r isk functionals, including predictiv e por tf olio selection and con- f or malized real-time V aR es timation [ Kato , 2024 , W ang et al. , 2026 ]. These contr ibutions mo ve conf ormal calibration in finance tow ard e xplicitly time-varying, state-a w are, sequential, and decision-aw are designs. Our paper is closest to this emerging literature, but addresses a dif- f erent g ap. Existing adaptiv e and state-a ware conf or mal procedures mainl y ask ho w calibration er rors should be w eighted, localized, or updated o ver time. By contrast, w e study ho w s trongl y the cor rection itself should depend on the scale of the state v ar iable. 2.3 V olatility Pr o xies, Regime Dependence, and the Gap A ddressed Here In financial risk applications, the relev ant notion of state scale is often supplied by a volatility pro xy . Because volatility is latent, practical r isk measurement relies on proxies suc h as rolling v olatility , G AR CH-based f orecasts, rang e-based estimators, and implied-v olatility indices such as the VIX [ Parkinson , 1980 , Gar man and Klass , 1980 , Andersen and Bollerslev , 1998 , An- dersen et al. , 2003 , Poon and Granger , 2003 , Whaley , 2009 ]. These quantities are inf ormative but imper fect: some are backw ard-looking, some are model-dependent, and some embed risk premia or market fr ictions. In stressed markets, such imper f ections become especiall y impor - tant, making v olatility inputs themsel v es a source of model risk. Recent e vidence also sugg ests that VIX dynamics and option-implied inf or mation continue to contain incremental predictive content f or future v olatility and tail-sensitiv e f orecasting tasks [ Bai and Cai , 2024 , Mic hael et al. , 2025 ]. This issue is closely connected to the broader literature on regime dependence, stressed- market dynamics, and state-dependent r isk control [ Hamilton , 1989 , Ang and Bekaer t , 2002 , Glasserman et al. , 2015 , A drian and Br unner meier , 2016 , A char y a et al. , 2017 , Ardia et al. , 5 2018 ]. When recalibration is driv en b y an imperfect v olatility pro xy , regime dependence matters not onl y because mark et conditions chang e, but also because pro xy misspecification can become most consequential precisely in stressed states. This mak es the rele v ant question not merel y whether recalibration should respond to the environment, but ho w strongl y the cor rection should scale with the proxy itself. These considerations motiv ate introducing a pro xy-reliance parameter 𝜌 , which measures ho w strongl y the recalibration cor rection inher its the scale of an imper f ect volatility signal. Larg er values of 𝜌 increase state responsiv eness but also increase vulnerability to stressed-s tate proxy under reaction, whereas smaller values trade some responsiv eness f or robustness. 3 Data 3.1 Sample and Asse ts Our empir ical analy sis uses dail y data f or six widely traded ETFs—SPY , QQQ, IWM, EEM, GLD, and TL T —co v er ing broad U.S. equities, technology , small-cap equities, emerging-mark et equities, gold, and T reasur ies. The raw panel sample runs from Februar y 2, 2015 to December 29, 2025. ETF price and v olume data are collected from the T wel v e Data API at the 1-day frequency , and each ETF ser ies is merg ed b y trading date with the CBOE V olatility Inde x (VIX) f or state measurement and stress classification. The six-asset panel pro vides the main cross-asset evidence across equity , rates, commodity , and emerging-mark et e xposures, while SPY is retained as an illustrativ e single-asset benchmark within the same aligned sample. For each ETF , the f orecasting targ et is the one-da y-ahead log retur n. Let 𝑃 𝑖 ,𝑡 denote the dail y closing pr ice of asset 𝑖 on date 𝑡 . W e define 𝑟 𝑖 ,𝑡 = log 𝑃 𝑖 ,𝑡 𝑃 𝑖 ,𝑡 − 1 , 𝑌 𝑖 ,𝑡 = 𝑟 𝑖 ,𝑡 + 1 . Thus, at time 𝑡 , the f orecasting problem is to es timate the lo w er 𝛼 -quantile of 𝑌 𝑖 ,𝑡 , with 𝛼 = 0 . 05 in the baseline specification. Bef ore constr ucting the modeling panel, obser v ations are sor ted b y asset, date, and volume, duplicate ( 𝑖 , 𝑡 ) entries are remo v ed by retaining the final record f or 6 each asset-date pair , and the modeling sample is then f or med by dropping ro ws with missing v alues in the targ et and required v olatility-related predictors. After f eature construction and remo v al of observations with missing lagg ed inputs, the balanced panel retains 1,730 rolling one-step test f orecasts per asset. All bac ktests are conducted in a strictly chronological out-of-sample manner and are analyzed both asset b y asset and in pooled summaries. 3.2 V ariables and F eatures The predictor set combines recent retur n inf or mation, historical and range-based v olatility measures, implied-volatility inf or mation, drawdo wn, and trading activity . T able 1 summar izes the main variables used in the baseline f orecasting models and in the cons truction of s tate v ar iables. T able 1: Summar y of f orecasting v ar iables and state f eatures Category V ar iables R ole R etur ns 𝑟 𝑖 , 𝑡 , 𝑟 𝑖 , 𝑡 − 1 , 𝑟 𝑖 , 𝑡 − 2 , 𝑟 𝑖 , 𝑡 − 3 , 𝑟 𝑖 , 𝑡 − 5 R ecent price dynamics and shor t-run persistence Historical v olatility 20-da y rolling v olatility ; lagged volatility f ea- tures Time-v ar ying r isk inf or - mation EWMA v olatility EWMA v olatility (span 20) Smoothed v olatility scale Rang e-based prox- ies Parkinson and Garman–Klass estimators Intrada y range-based r isk inf or mation Implied v olatility VIX -implied daily v olatility; dail y VIX percent- ag e chang e Forw ard-looking s tress in- f or mation Dra wdo wn 60-da y rolling dra wdo wn A dv erse market-s tate indi- cator T rading activity Log v olume; rolling volume 𝑧 -score A ctivity and liquidity - related state inf ormation T w o v ariables pla y a central role in the market-s tate construction. Firs t, the VIX lev el is con v er ted into an approximate daily implied-v olatility pro xy . Let VIX 𝑡 denote the obser v ed VIX le v el on date 𝑡 . Then 𝑣 VIX 𝑡 = VIX 𝑡 100 √ 252 . (1) This transf or mation treats the VIX as a f or w ard-looking volatility gaug e rather than as ground truth, which is consistent with both classic inter pretations of the inde x and the broader v olatility- 7 f orecasting literature [ P oon and Grang er , 2003 , Whale y , 2009 , Bai and Cai , 2024 ]. Second, the rolling 60-da y dra wdown is defined as 𝐷 𝐷 ( 60 ) 𝑖 ,𝑡 = 𝑃 𝑖 ,𝑡 max 0 ≤ 𝑗 ≤ 59 𝑃 𝑖 ,𝑡 − 𝑗 − 1 . (2) In addition, w e include a trading-activity f eature based on v olume. Let V olume 𝑖 ,𝑡 denote the trading v olume of asset 𝑖 on date 𝑡 , and define 𝐿 v ol 𝑖 ,𝑡 = log ( V olume 𝑖 ,𝑡 ) , (3) which is s tandardized using a rolling 20-da y mean and standard de viation. These variables are not intended to form an exhaus tiv e alpha model. Rather , they pro- vide a compact and inter pretable s tate representation f or one-sided tail-risk f orecasting and recalibration. 3.3 V olatility Pr o xy and Stress-State Definition A central object in the paper is a positive v olatility pro xy 𝑣 𝑡 used to scale the recalibration ad- justment. W e constr uct a composite pro xy from three components: 20-da y rolling v olatility , a G AR CH-sty le v olatility pro xy , and the dail y v olatility transf or mation of the VIX. In implemen- tation, the G AR CH-sty le component is obtained from e xpanding-window conditional v olatility estimates; detailed estimation and fallbac k r ules are repor ted in Appendix C . T o preserve comparability across components while keeping the final pro xy in units comparable to rolling v olatility , we first nor malize each component by its in-sample median on the current training windo w and then re-anchor the a v erage to the rolling-v olatility component. Let C = { 𝑐 1 , 𝑐 2 , 𝑐 3 } denote the three components, and let T train denote the cur rent training-window inde x set. Define 𝑚 𝑗 = max median { 𝑐 𝑗 ,𝑠 : 𝑠 ∈ T train } , 10 − 8 , 𝑗 = 1 , 2 , 3 . (4) 8 Let 𝑆 denote the set of dates within the current rolling windo w on whic h the pro xy is e v aluated. Then, f or 𝑡 ∈ 𝑆 , 𝑣 𝑡 = © « 1 3 3 𝑗 = 1 𝑐 𝑗 ,𝑡 𝑚 𝑗 ª ® ¬ 𝑚 1 . (5) Thus, the composite proxy is e xpressed in units comparable to the rolling-v olatility component. A small floor is imposed to ensure positivity : 𝑣 𝑡 ← max ( 𝑣 𝑡 , 10 − 8 ) . (6) Market-s tate labels are g enerated without look -ahead bias. In each rolling training windo w , the distribution of 𝑣 VIX 𝑡 is used to define a three-bin regime par tition: • lo w-str ess regime : 𝑣 VIX 𝑡 belo w the training median; • mid-stress regime : 𝑣 VIX 𝑡 betw een the training median and the training 80th percentile; • high-stress regime : 𝑣 VIX 𝑡 abo ve the training 80th percentile. For subgroup ev aluation, w e also define a stricter stress flag. Let 𝑞 ( 𝑡 𝑟 𝑎𝑖 𝑛 ) 0 . 90 ( 𝑣 VIX ) denote the 90th percentile of the training-windo w VIX -based dail y v olatility proxy , and let 𝑞 ( 𝑡 𝑟 𝑎𝑖 𝑛 ) 0 . 30 ( 𝐷 𝐷 ( 60 ) 𝑖 ) denote the 30th percentile of the training-windo w 60-day dra wdo wn f or asset 𝑖 . Then 1 { stress 𝑡 = 1 } = 1 n 𝑣 VIX 𝑡 ≥ 𝑞 ( 𝑡 𝑟 𝑎𝑖 𝑛 ) 0 . 90 ( 𝑣 VIX ) o · 1 n 𝐷 𝐷 ( 60 ) 𝑖 ,𝑡 ≤ 𝑞 ( 𝑡 𝑟 𝑎𝑖 𝑛 ) 0 . 30 ( 𝐷 𝐷 ( 60 ) 𝑖 ) o . (7) This rolling cons tr uction a voids look -ahead bias and ensures that s tress is defined relative to the pre v ailing market en vironment rather than to the full sample. 3.4 Out-of-Sample Design All results are produced under a strictly chronological rolling design. For each f orecast origin, the a v ailable data are divided into a training windo w of 504 obser v ations, a calibration-selection windo w of 252 obser v ations, a final calibration windo w of 126 observations, and a one-step test point. Thus, all baseline forecas ts, state thresholds, and recalibration quantities are f ormed using 9 onl y inf or mation a v ailable at the f orecast date. The selection logic is descr ibed in Section 4 , while additional implementation details are repor ted in Appendix C . This design yields 1,730 one-step test f orecasts per asset in the balanced panel and ensures that the repor ted results reflect genuine out-of-sample per f or mance under time-varying market conditions. 4 Methodology 4.1 Baseline F orecasts and Pro xy -Reliance-Contr olled R ecalibration For clar ity , we present the method f or a g ener ic asset; in the empirical anal y sis, the same rolling procedure is applied separatel y to each ETF in the panel. For notational simplicity , w e suppress the asset index 𝑖 in this section and write 𝑌 𝑡 = 𝑟 𝑡 + 1 f or the next-period retur n realized after forecas t or igin 𝑡 . Let b 𝑞 𝛼, 𝑡 denote a baseline f orecast of the lo w er 𝛼 -quantile of 𝑌 𝑡 , where 𝛼 = 0 . 05. Throughout the paper , V aR is e xpressed in retur n space, so more negativ e values cor respond to more conser vativ e left-tail f orecasts. Our goal is to construct a one-sided left-tail V aR f orecast d V aR 𝛼, 𝑡 = b 𝑞 𝑎 𝑑 𝑗 𝛼, 𝑡 , (8) such that the e x ceedance probability P 𝑌 𝑡 ≤ d V aR 𝛼, 𝑡 (9) is close to 𝛼 , both o v erall and in stressed market s tates. T able 2 summar izes the baseline V aR f orecasters considered in the empir ical anal y sis. These baselines range from simple nonparametric r ules to more structured parametr ic models, allo wing us to assess whether the proposed recalibration la yer adds value across different f orecasting f amilies. In the standalone SPY strong er -benchmark compar ison, w e also include AS-C A ViaR as an auxiliary conditional-quantile benchmark. In the main-text pooled tables, w e repor t GAR CH- 𝑡 as the representative parametr ic volatility famil y , while additional GJR - G AR CH- 𝑡 e vidence is repor ted in Appendix B . 10 T able 2: Baseline V aR f orecasters Baseline Definition Historical simulation (HS) Empirical 𝛼 -quantile of training-windo w retur ns Filtered his torical simulation (FHS) Empirical 𝛼 -quantile of standardized training-windo w retur ns, rescaled by current EWMA v olatility Quantile regression (QR) Linear quantile regression fitted on the full f eature v ector G AR CH-proxy q uantile (GPQ) Empirical standardized quantile based on a G AR CH-sty le v olatility pro xy G AR CH- 𝑡 Parametric G AR CH model with Student- 𝑡 inno vations GJR -GAR CH- 𝑡 Asymmetric GAR CH model with Student- 𝑡 inno vations Ag ainst this background, our methodological question is not ho w to replace the baseline f orecaster , but how strongl y the recalibration adjustment should depend on the v olatility proxy that scales it. The ke y tuning parameter is 𝜌 ∈ [ 0 , 1 ] , which controls ho w strongl y the recalibration adjustment depends on the v olatility pro xy . Giv en a baseline V aR f orecast b 𝑞 𝛼, 𝑠 and a positiv e v olatility proxy 𝑣 𝑠 , define the signed lo wer -tail residual at calibration date 𝑠 by 𝑢 ( 𝜌 ) 𝑠 = 𝑌 𝑠 − b 𝑞 𝛼, 𝑠 𝑣 𝜌 𝑠 . (10) For the calibration inde x set I 𝑡 associated with the cur rent f orecast origin 𝑡 , define 𝑐 𝜌 ,𝑡 = 𝑄 𝑙 𝑜 𝑤 𝑒 𝑟 𝛼 n 𝑢 ( 𝜌 ) 𝑠 : 𝑠 ∈ I 𝑡 o , (11) where 𝑄 𝑙 𝑜 𝑤 𝑒 𝑟 𝛼 denotes the low er empirical 𝛼 -quantile. The resulting one-step recalibrated f orecast is b 𝑞 𝑎 𝑑 𝑗 𝛼, 𝑡 = b 𝑞 𝛼, 𝑡 + 𝑐 𝜌 ,𝑡 𝑣 𝜌 𝑡 . (12) This f ormulation nests tw o limiting cases. When 𝜌 = 0, the recalibration behav es like an appro ximately constant shift. When 𝜌 = 1, the cor rection fully inher its the scale of the pro xy . Intermediate values inter polate continuously between these extremes. Thus, 𝜌 measures how strongl y the recalibration cor rection depends on pro xy scale. 11 4.2 F ormal Properties of Pr o xy Reliance T o f ormalize the role of 𝜌 , define the signed adjustment 𝐴 𝜌 ( 𝑣 ; 𝑐 ) = 𝑐 𝑣 𝜌 , (13) where 𝑐 < 0 is the lo wer -tail calibration constant and 𝑣 > 0 is the pro xy lev el. The f ollo w - ing results are mechanism-based str uctural proper ties under sty lized local assumptions, rather than finite-sample guarantees f or the full rolling procedure. The first two results characterize clean-pro xy scaling, while the third identifies stressed-state fragility under s tress-specific pro xy under reaction. Proposition 4.1 (Elasticity and in v ar iance under unif or m pro xy rescaling) . F ix 𝜌 ∈ [ 0 , 1 ] . F or any 𝜂 > 0 , 𝐴 𝜌 ( 𝜂 𝑣 ; 𝑐 ) = 𝜂 𝜌 𝐴 𝜌 ( 𝑣 ; 𝑐 ) . (14) Hence the sensitivity of the adjustment magnitude to proportional chan g es in pro xy scale is gov erned exactly by 𝜌 . Moreo ver , if the pr o xy is unif ormly rescaled by the same positiv e multiplicativ e fact or at all calibr ation points and at the f or ecast point, while the baseline f or ecast is held fixed, then the r esulting one-step r ecalibrat ed V aR f or ecast is unc hang ed. Proposition 4.2 (Cross-s tate contras t induced b y 𝜌 ) . F ix 𝑐 ≠ 0 and le t 𝑣 𝐻 > 𝑣 𝐿 > 0 denot e tw o pr o xy lev els corresponding t o a higher - and a low er -risk state. Then | 𝐴 𝜌 ( 𝑣 𝐻 ; 𝑐 ) | | 𝐴 𝜌 ( 𝑣 𝐿 ; 𝑐 ) | = 𝑣 𝐻 𝑣 𝐿 𝜌 . (15) Consequently , this contras t ratio is incr easing in 𝜌 , equals 1 at 𝜌 = 0 , and equals 𝑣 𝐻 / 𝑣 𝐿 at 𝜌 = 1 . Propositions 4.1 – 4.2 sho w that 𝜌 gov erns both the sensitivity of the adjustment to pro xy scale and the contras t of the adjustment across mark et states. These results sugg est f ocusing on heterog eneous, state-dependent dis tor tion rather than unif or m multiplicativ e rescaling. 12 Proposition 4.3 (S tress-state e x ceedance distortion under pro xy under reaction) . Fix a f orecas t date 𝑡 suc h that stress 𝑡 = 1 , and an exponent 𝜌 ∈ [ 0 , 1 ] . Let 𝑞 ∗ 𝜌 ,𝑡 = b 𝑞 𝛼, 𝑡 + 𝑐 𝜌 ,𝑡 𝑣 𝜌 𝑡 (16) denot e the clean-pro xy r ecalibr ated f or ecast, where 𝑐 𝜌 ,𝑡 < 0 is the clean-pro xy r ecalibr ation constant associat ed with f orecas t origin 𝑡 , and 𝑣 𝑡 > 0 . Define 𝐹 𝑡 ( 𝑦 ) : = P ( 𝑌 𝑡 ≤ 𝑦 | F 𝑡 ) , (17) wher e F 𝑡 denot es the inf ormation set available at the f orecas t date 𝑡 . Assume that under the clean pr o xy this f or ecast is conditionally exact at lev el 𝛼 , namely 𝐹 𝑡 ( 𝑞 ∗ 𝜌 ,𝑡 ) = 𝛼 . (18) N ow suppose t hat the pr oxy underr eacts multiplicatively at t he f orecas t point, e 𝑣 𝑡 = 𝜅 𝑣 𝑡 , 𝜅 ∈ ( 0 , 1 ) , (19) and define the misspecified f orecas t e 𝑞 𝜌 ,𝑡 = b 𝑞 𝛼, 𝑡 + 𝑐 𝜌 ,𝑡 e 𝑣 𝜌 𝑡 = b 𝑞 𝛼, 𝑡 + 𝑐 𝜌 ,𝑡 𝜅 𝜌 𝑣 𝜌 𝑡 . (20) Then the conditional exceedance dist ortion Δ 𝑡 ( 𝜌 ) : = P ( 𝑌 𝑡 ≤ e 𝑞 𝜌 ,𝑡 | F 𝑡 ) − 𝛼 (21) satisfies Δ 𝑡 ( 𝜌 ) = 𝐹 𝑡 ( e 𝑞 𝜌 ,𝑡 ) − 𝐹 𝑡 ( 𝑞 ∗ 𝜌 ,𝑡 ) ≥ 0 . (22) If, moreo ver , 𝜌 > 0 and 𝐹 𝑡 is continuous on [ 𝑞 ∗ 𝜌 ,𝑡 , e 𝑞 𝜌 ,𝑡 ] and differ entiable on ( 𝑞 ∗ 𝜌 ,𝑡 , e 𝑞 𝜌 ,𝑡 ) , 13 with deriv ative 𝑓 𝑡 ( 𝑦 ) : = 𝐹 ′ 𝑡 ( 𝑦 ) , then t her e exists some 𝜉 𝜌 ,𝑡 ∈ ( 𝑞 ∗ 𝜌 ,𝑡 , e 𝑞 𝜌 ,𝑡 ) (23) suc h that Δ 𝑡 ( 𝜌 ) = 𝑓 𝑡 ( 𝜉 𝜌 ,𝑡 ) | 𝑐 𝜌 ,𝑡 | 𝑣 𝜌 𝑡 ( 1 − 𝜅 𝜌 ) . (24) F or 𝜌 = 0 , one has e 𝑞 𝜌 ,𝑡 = 𝑞 ∗ 𝜌 ,𝑡 and hence Δ 𝑡 ( 0 ) = 0 . Consequently , for 𝜌 > 0 , if ther e exist constants 0 < 𝑓 𝑡 ≤ 𝑓 𝑡 < ∞ suc h that 𝑓 𝑡 ≤ 𝑓 𝑡 ( 𝑦 ) ≤ 𝑓 𝑡 f or all 𝑦 ∈ [ 𝑞 ∗ 𝜌 ,𝑡 , e 𝑞 𝜌 ,𝑡 ] , then 𝑓 𝑡 | 𝑐 𝜌 ,𝑡 | 𝑣 𝜌 𝑡 ( 1 − 𝜅 𝜌 ) ≤ Δ 𝑡 ( 𝜌 ) ≤ 𝑓 𝑡 | 𝑐 𝜌 ,𝑡 | 𝑣 𝜌 𝑡 ( 1 − 𝜅 𝜌 ) . (25) The same bounds hold trivially at 𝜌 = 0 , since Δ 𝑡 ( 0 ) = 0 . Corollary 4.4 (Ordering under matc hed clean-pro xy stress adjustment) . Under the assumptions of Pr oposition 4.3 , suppose in addition that the clean-pro xy signed adjustment magnitude is matc hed acr oss 𝜌 , i.e. there exis ts 𝑎 𝑡 > 0 such t hat | 𝑐 𝜌 ,𝑡 | 𝑣 𝜌 𝑡 = 𝑎 𝑡 f or all 𝜌 ∈ [ 0 , 1 ] . (26) Then, f or 𝜌 > 0 , Δ 𝑡 ( 𝜌 ) = 𝑓 𝑡 ( 𝜉 𝜌 ,𝑡 ) 𝑎 𝑡 ( 1 − 𝜅 𝜌 ) , (27) while Δ 𝑡 ( 0 ) = 0 . If, mor eo v er , ther e exist constants 0 < 𝑓 𝑡 ≤ 𝑓 𝑡 < ∞ suc h that 𝑓 𝑡 ≤ 𝑓 𝑡 ( 𝑦 ) ≤ 𝑓 𝑡 f or all 𝑦 ∈ [ 𝑞 ∗ 𝜌 ,𝑡 , e 𝑞 𝜌 ,𝑡 ] and all 𝜌 ∈ ( 0 , 1 ] , (28) 14 then f or 𝜌 > 0 , 𝑓 𝑡 𝑎 𝑡 ( 1 − 𝜅 𝜌 ) ≤ Δ 𝑡 ( 𝜌 ) ≤ 𝑓 𝑡 𝑎 𝑡 ( 1 − 𝜅 𝜌 ) . (29) The same bounds hold trivially at 𝜌 = 0 . Since 𝜅 ∈ ( 0 , 1 ) , the map 𝜌 ↦→ 1 − 𝜅 𝜌 is increasing on [ 0 , 1 ] . Hence the exceedance distortion is nondecr easing in 𝜌 up to the density f actor . In particular , if the map 𝜌 ↦→ 𝑓 𝑡 ( 𝜉 𝜌 ,𝑡 ) is nondecr easing and strictly positiv e on ( 0 , 1 ] , then Δ 𝑡 ( 𝜌 ) is increasing in 𝜌 on ( 0 , 1 ] . T aking conditional e xpectation ov er stressed f orecast dates yields ¯ Δ ( 𝜌 ) : = E [ Δ 𝑡 ( 𝜌 ) | stress 𝑡 = 1 ] . (30) Assuming the rele vant quantities are integ rable, the pointwise bounds abo v e impl y correspond- ing 𝜌 -dependent conditional-e xpectation bounds f or ¯ Δ ( 𝜌 ) . Nondecreasing dependence on 𝜌 f ollo w s under the additional condition that the map 𝜌 ↦→ 𝑓 𝑡 ( 𝜉 𝜌 ,𝑡 ) is constant or nondecreasing on ( 0 , 1 ] ; strong er monotonicity f ollo ws under the stricter positivity condition stated in Corol- lary 4.4 . Proofs, tog ether with a supplementar y screening result, are collected in Appendix A . 4.3 Pro xy -Reliance Selection and R egime-A w are Extension Empirically , w e use a nested rolling design. F or each f orecast origin 𝑡 , candidate pro xy -reliance rules are first selected on an intermediate selection bloc k, and the final recalibration cons tant is then re-estimated on a separate calibration bloc k bef ore one-s tep e valuation. The e xact windo w lengths and search grids are repor ted in Appendix C . W e consider tw o scalar selectors. Let R denote the candidate set of proxy -reliance values, and let S 𝑡 denote the inter mediate selection block associated with f orecast origin 𝑡 . The g lobal av er ag e selector chooses the pro xy-reliance v alue that minimizes a v erage capital on the selection block, b 𝜌 𝑔 𝑙 𝑜 𝑏 𝑎 𝑙 , 𝑎 𝑣 𝑔 𝑡 = arg min 𝜌 ∈ R 1 | S 𝑡 | 𝑠 ∈ S 𝑡 max − b 𝑞 𝑎 𝑑 𝑗 𝛼, 𝑠 ( 𝜌 ) , 0 , (31) where b 𝑞 𝑎 𝑑 𝑗 𝛼, 𝑠 ( 𝜌 ) denotes the candidate-specific recalibrated f orecast cons tr ucted on the selection block under pro xy-reliance v alue 𝜌 . This selector is intentionall y capital-or iented and does not 15 impose additional stress-specific f easibility screening. The g lobal str ess-aw ar e selector instead prior itizes adverse-s tate tail control: candidates are screened using stress-sensitiv e and ov erall e x ceedance cr iter ia, and among admissible can- didates the selector trades off stress-per iod pinball loss and capital usage. A dditional imple- mentation details, including search g r ids, f easibility thresholds, and f allbac k rules, are reported in Appendix C . After a scalar pro xy-reliance value b 𝜌 𝑡 is selected at f orecast or igin 𝑡 , the final recalibration constant is re-es timated on a separate calibration inde x set I 𝑡 , yielding the one-step f orecast b 𝑞 𝑎 𝑑 𝑗 𝛼, 𝑡 = b 𝑞 𝛼, 𝑡 + 𝑐 b 𝜌 𝑡 ,𝑡 𝑣 b 𝜌 𝑡 𝑡 , (32) where 𝑐 b 𝜌 𝑡 ,𝑡 = 𝑄 𝑙 𝑜 𝑤 𝑒 𝑟 𝛼 ( 𝑌 𝑠 − b 𝑞 𝛼, 𝑠 𝑣 b 𝜌 𝑡 𝑠 : 𝑠 ∈ I 𝑡 ) ! . (33) W e also consider a regime-dependent e xtension. Let 𝑔 𝑡 ∈ { lo w , mid , high } (34) denote the rolling regime label defined from the training-windo w VIX distr ibution, and let ρ = ( 𝜌 𝑙 𝑜 𝑤 , 𝜌 𝑚𝑖 𝑑 , 𝜌 ℎ𝑖 𝑔 ℎ ) (35) denote a regime-specific pro xy -reliance r ule. For a giv en candidate tuple ρ , define the regime- adjusted residual on the calibration sample b y 𝑢 ( ρ ) 𝑠 = 𝑌 𝑠 − b 𝑞 𝛼, 𝑠 𝑣 𝜌 𝑔 𝑠 𝑠 , 𝑠 ∈ I 𝑡 , (36) and the cor responding recalibration constant b y 𝑐 ρ ,𝑡 = 𝑄 𝑙 𝑜 𝑤 𝑒 𝑟 𝛼 n 𝑢 ( ρ ) 𝑠 : 𝑠 ∈ I 𝑡 o . (37) 16 The associated one-step recalibrated f orecast is b 𝑞 𝑎 𝑑 𝑗 𝛼, 𝑡 ( ρ ) = b 𝑞 𝛼, 𝑡 + 𝑐 ρ ,𝑡 𝑣 𝜌 𝑔 𝑡 𝑡 . (38) T o preser v e inter pretability and reduce o v er fitting, we res tr ict attention to monotone tuples satisfying 𝜌 𝑙 𝑜 𝑤 ≥ 𝜌 𝑚𝑖 𝑑 ≥ 𝜌 ℎ𝑖 𝑔 ℎ . (39) This restriction reflects the h ypothesis that pro xy reliance should w eaken in more stressed states. Let b ρ 𝑡 denote the selected monotone tuple at forecas t or igin 𝑡 ; the final regime-dependent f orecast is then b 𝑞 𝑎 𝑑 𝑗 𝛼, 𝑡 ( b ρ 𝑡 ) . 4.4 Empirical Im plement ation and Ev aluation W e s tudy tw o pro xy scenarios. U nder the clean pr o xy , the composite v olatility pro xy is used as constructed. U nder the underreacting str ess pr o xy , the pro xy is shr unk only in stressed states according to 𝑣 𝑚𝑖 𝑠 𝑡 = 𝜅 𝑣 𝑡 , if stress 𝑡 = 1 , 𝑣 𝑡 , otherwise , 𝜅 ∈ ( 0 , 1 ) , (40) so that the pro xy underreacts precisel y where s tressed-state tail control matters mos t. The repor ted implementation uses 𝜅 = 0 . 4; fur ther implementation details are giv en in Appendix C . Each method is e v aluated in a one-step rolling backtes t. For each forecas t date, we record the realized return 𝑌 𝑡 , the recalibrated f orecast b 𝑞 𝑎 𝑑 𝑗 𝛼, 𝑡 , and the e xceedance indicator 𝐼 𝑡 = 1 { 𝑌 𝑡 ≤ b 𝑞 𝑎 𝑑 𝑗 𝛼, 𝑡 } . (41) W e repor t the unconditional e x ceedance frequency b 𝑝 = 1 𝑇 𝑇 𝑡 = 1 𝐼 𝑡 , (42) 17 the strict-stress e x ceedance frequency b 𝑝 𝑠𝑡 𝑟 𝑖 𝑐 𝑡 = Í 𝑇 𝑡 = 1 𝐼 𝑡 1 { stress 𝑠𝑡 𝑟 𝑖 𝑐 𝑡 𝑡 = 1 } Í 𝑇 𝑡 = 1 1 { stress 𝑠𝑡 𝑟 𝑖 𝑐 𝑡 𝑡 = 1 } , (43) where stress 𝑠𝑡 𝑟 𝑖 𝑐 𝑡 𝑡 denotes the rolling strict-stress flag defined in Section 3 . In the empirical anal y sis, stress 𝑡 denotes the broader rolling stress indicator used in proxy misspecification and stress-a ware selection, whereas stress 𝑠𝑡 𝑟 𝑖 𝑐 𝑡 𝑡 is used onl y f or final stressed-state repor ting. W e also repor t the a v erage capital 1 𝑇 𝑇 𝑡 = 1 max − b 𝑞 𝑎 𝑑 𝑗 𝛼, 𝑡 , 0 . (44) W e also repor t quantile tick loss and s tandard V aR bac ktests, including the Kupiec unconditional co verag e test, the Chr istoffersen conditional cov erag e test, and the Engle–Manganelli dynamic quantile (DQ) tes t. 5 R esults W e organise the empir ical results around the cross-asset panel and use SPY onl y as an illustrativ e benchmark. The six-ETF panel provides the main evidence across heterogeneous assets and baseline f orecasters, while the aligned SPY slice visualises the same mechanisms in a familiar single-market setting. Each method is e v aluated o v er 1,730 rolling one-s tep test dates per asset, f or a pooled total of 10,380 out-of-sample f orecasts. 5.1 Cross-asse t panel e vidence W e begin with pooled panel compar isons across the six ETFs. T able 3 show s that pro xy-reliance- controlled recalibration does not deliv er unif orm impro vements across pooled ov erall metr ics. As sho wn below , its empir ical gains are more concentrated in stressed-s tate tail per f ormance. T able 3 reports the pooled o v erall results. FHS and GPQ already per f or m s trongl y under the clean pro xy . By contrast, histor ical simulation underco v ers the tail, with e x ceedance 0 . 0598, and quantile regression is more distorted, with e xceedance 0 . 0925. Recalibration mo v es both much closer to the nominal 5% targ et, although at a capital cos t. F or G ARCH- 𝑡 , the ra w model is 18 o ver ly conser vativ e, and recalibration releases much of this conser vatism while lo wering a v erage capital to ward 0 . 023, although conditional-cov erag e and DQ diagnostics remain w eak. This indicates that recalibration repairs unconditional and s tress-sensitiv e cov erag e more reliably than it remo ves all dynamic dependence misspecification in tail violations. Additional GJR - G AR CH- 𝑡 results lead to the same qualitativ e conclusion; see Appendix B . T able 3: Pooled ov erall out-of-sample results across the six-asset panel under the clean proxy specification. Exceedance denotes pooled unconditional breach frequency . A v g cap. denotes a v erage capital pro xy . UC, CC, and DQ indicate whether the pooled Kupiec, Chr istoffersen, and Engle–Manganelli dynamic q uantile (DQ) tests are passed at the 5% le v el. Baseline Method Ex ceed. A vg cap. Tick loss UC CC DQ FHS Base 0.0497 0.0205 0.001415 Y Y N FHS 𝜌 = 0 0.0487 0.0216 0.001461 Y Y N FHS 𝜌 = 1 0.0468 0.0223 0.001464 Y Y N FHS Global-stress 0.0481 0.0219 0.001461 Y Y N FHS Regime-s tress 0.0476 0.0225 0.001499 Y Y N GPQ Base 0.0516 0.0201 0.001384 Y Y N GPQ 𝜌 = 0 0.0487 0.0211 0.001411 Y Y N GPQ 𝜌 = 1 0.0472 0.0215 0.001415 Y Y N GPQ Global-stress 0.0485 0.0213 0.001414 Y Y N GPQ Regime-s tress 0.0477 0.0217 0.001432 Y Y N HS Base 0.0598 0.0188 0.001598 N N N HS 𝜌 = 0 0.0501 0.0211 0.001525 Y N N HS 𝜌 = 1 0.0499 0.0208 0.001469 Y N N HS Global-stress 0.0501 0.0211 0.001489 Y N N HS Regime-s tress 0.0495 0.0218 0.001558 Y N N QR Base 0.0925 0.0180 0.001791 N N N QR 𝜌 = 0 0.0466 0.0229 0.001566 Y N N QR 𝜌 = 1 0.0463 0.0228 0.001526 Y N N QR Global-stress 0.0469 0.0227 0.001535 Y N N QR Regime-s tress 0.0468 0.0246 0.001620 Y N N GAR CH- 𝑡 Base 0.0472 0.0323 0.002137 Y N N GAR CH- 𝑡 𝜌 = 0 0.0434 0.0228 0.001553 N N N GAR CH- 𝑡 𝜌 = 1 0.0472 0.0236 0.001650 Y N N GAR CH- 𝑡 Global-stress 0.0453 0.0232 0.001563 N N N GAR CH- 𝑡 Regime-s tress 0.0447 0.0245 0.001665 N N N Figure 1 visualises the pooled o verall e x ceedance compar isons. The main message is that recalibration repairs w eak baselines, but does not unif or mly dominate the strong est raw pro xy-a ware benc hmarks in tick loss or capital usag e. The panel results also sho w substantial cross-asset heterogeneity . Figure 2 show s that the v alue of recalibration depends on both the baseline famil y and the asset. The lar g est ra w distortions ar ise f or historical simulation and quantile reg ression, whereas FHS and GPQ are already more s table across assets. The clearest repair cases are QQQ and SPY . F or e xample, the ra w GPQ baseline f or QQQ has o verall ex ceedance 0 . 0566 and strict-stress e x ceedance 0 . 0718; using 𝜌 = 0 lo wers these to 0 . 0497 and 0 . 0462, respectiv ely , at higher capital. F or SPY , the raw 19 (a) Historical simulation (b) Quantile regression (c) G AR CH-proxy q uantile (d) GAR CH- 𝑡 V aR Figure 1: P ooled o v erall e x ceedance across the six-asset panel under the clean pro xy specifica- tion. The dashed hor izontal line marks the nominal 5% targ et. (a) Historical simulation (b) Quantile regression (c) Filtered his torical simulation (d) G AR CH-proxy q uantile Figure 2: Cross-asset e xceedance heatmaps under the clean pro xy specification. GPQ baseline mo ves from 0 . 0578 ov erall and 0 . 0894 under strict stress to 0 . 0514 o v erall and 0 . 0447 under the regime-stress rule. By contrast, IWM, GLD, and TL T already ha v e raw GPQ performance close to targ et, lea ving less room for impro v ement. Figure 3 summar izes these e xceedance–capital trade-offs. 20 (a) QR: clean pro xy (b) QR: underreacting stress pro xy (c) GPQ: clean pro xy (d) GPQ: under reacting stress pro xy Figure 3: Cross-asset e xceedance–capital trade-offs f or tw o representativ e baseline f amilies. A second panel-lev el result concer ns robustness under pro xy under reaction. T able 4 sho ws that the main deterioration appears in stressed states rather than in pooled o v erall perf ormance. This deter ioration is concentrated in high- 𝜌 r ules. F or e xample, f or HS the stressed ex ceedance of 𝜌 = 1 w orsens from 0 . 0622 under the clean pro xy to 0 . 0873 under pro xy underreaction, and f or QR it worsens from 0 . 0512 to 0 . 0693. By contrast, GPQ with 𝜌 = 0 remains essentiall y unchang ed at 0 . 0462, and the GPQ global-stress selector is like wise stable. This patter n is consistent with Proposition 4.3 and Corollar y 4.4 : strong er pro xy dependence increases fragility when the pro xy under reacts precisely in stressed states. Figure 4 show s the same robustness pattern across assets. T aken tog ether , the panel evidence sugges ts that pro xy-reliance-controlled recalibration is best vie w ed as a model-agnostic repair mechanism whose empir ical value is concentrated in stressed-s tate robustness under proxy imper f ection rather than in unif or m ov erall dominance. 21 T able 4: Pooled strict-stress robustness under clean and under reacting-stress pro xy specifica- tions. Stress e xceed. denotes pooled strict-stress e x ceedance; stressed cap. denotes pooled strict-stress a v erag e capital. Baseline Method Clean s tress e x ceed. Underreact stress ex ceed. Clean stressed cap. Underreact stressed cap. HS Base 0.1717 0.1717 0.0141 0.0141 HS 𝜌 = 0 0.0783 0.0783 0.0294 0.0294 HS 𝜌 = 1 0.0622 0.0873 0.0304 0.0265 HS Global-stress 0.0703 0.0894 0.0306 0.0271 QR Base 0.2209 0.2209 0.0218 0.0218 QR 𝜌 = 0 0.0592 0.0592 0.0368 0.0368 QR 𝜌 = 1 0.0512 0.0693 0.0379 0.0327 QR Global-stress 0.0552 0.0703 0.0368 0.0323 GPQ Base 0.0612 0.0612 0.0325 0.0325 GPQ 𝜌 = 0 0.0462 0.0462 0.0363 0.0363 GPQ 𝜌 = 1 0.0402 0.0472 0.0398 0.0366 GPQ Global-stress 0.0462 0.0462 0.0374 0.0363 GAR CH- 𝑡 Base 0.1446 0.1446 0.0261 0.0261 GAR CH- 𝑡 𝜌 = 0 0.0723 0.0723 0.0307 0.0307 GAR CH- 𝑡 𝜌 = 1 0.0763 0.0813 0.0308 0.0308 GAR CH- 𝑡 Global-stress 0.0683 0.0803 0.0311 0.0299 (a) QR: clean pro xy (b) QR: underreacting stress pro xy (c) GPQ: clean pro xy (d) GPQ: under reacting stress pro xy Figure 4: Cross-asset e x ceedance heatmaps under clean and under reacting-stress proxy speci- fications. Its v alue is g reatest when the ra w baseline undercov ers the left tail, especiall y in s tressed states, whereas already strong proxy -a w are baselines lea ve less room f or impro v ement. The robustness e xper iments fur ther suppor t inter preting 𝜌 as a trust parameter on the v olatility proxy . 22 T able 5: Main SPY o v erall out-of-sample results under the clean pro xy specification. Ex- ceedance denotes the unconditional breach frequency . A v g cap. denotes the av erage capital pro xy . UC, CC, and DQ indicate whether the K upiec, Chr istoffersen, and Engle–Manganelli dynamic quantile (DQ) tes ts are passed at the 5% le v el. Baseline Method Ex ceed. A v g cap. Tick loss UC CC DQ HS Base 0.054 0.018 0.001689 Y N N HS 𝜌 = 0 0.050 0.021 0.001571 Y Y N HS 𝜌 = 1 0.052 0.020 0.001472 Y Y N HS Global-stress 0.050 0.021 0.001507 Y Y N HS Regime-stress 0.049 0.021 0.001524 Y Y N FHS Base 0.051 0.019 0.001387 Y Y N FHS 𝜌 = 0 0.053 0.021 0.001469 Y Y N FHS 𝜌 = 1 0.048 0.021 0.001445 Y Y N FHS Global-stress 0.052 0.021 0.001451 Y Y N FHS Regime-s tress 0.050 0.022 0.001478 Y Y N QR Base 0.070 0.018 0.001429 N N N QR 𝜌 = 0 0.055 0.021 0.001470 Y Y N QR 𝜌 = 1 0.052 0.021 0.001433 Y Y N QR Global-stress 0.054 0.021 0.001463 Y Y N QR Regime-s tress 0.053 0.022 0.001521 Y Y N GPQ Base 0.058 0.018 0.001339 Y Y Y GPQ 𝜌 = 0 0.054 0.020 0.001357 Y Y N GPQ 𝜌 = 1 0.049 0.020 0.001364 Y Y N GPQ Global-stress 0.053 0.020 0.001368 Y Y N GPQ R egime-stress 0.051 0.020 0.001362 Y Y Y GAR CH- 𝑡 Base 0.035 0.033 0.002274 N N N GAR CH- 𝑡 𝜌 = 0 0.046 0.023 0.001606 Y Y N GAR CH- 𝑡 𝜌 = 1 0.049 0.023 0.001649 Y N N GAR CH- 𝑡 Global-stress 0.046 0.023 0.001587 Y N N GAR CH- 𝑡 R egime-stress 0.045 0.024 0.001642 Y N N 5.2 SPY as an illustrativ e benchmar k The aligned SPY slice is included onl y to illustrate the panel mechanisms in a familiar single- market benchmark. T able 5 deliv ers the same qualitativ e ranking. QR remains the clearest repair case, with recalibration mo ving ex ceedance mater ially closer to targ et. FHS and GPQ are already relativel y well calibrated on the aligned SPY sample, so recalibration mainly reshapes the co v erag e–capital and stress-control trade-off rather than generating larg e unconditional gains. For G AR CH- 𝑡 , recalibration releases e xcess conser vatism while bringing e xceedance closer to targ et. Additional aligned-SPY results for GJR -G AR CH- 𝑡 are repor ted in Appendix B . 5.3 Detailed SPY case study : comparison with strong er ra w tail baselines T o assess whether the proposed recalibration lay er adds v alue bey ond weak er benchmark fam- ilies, we also compare it ag ainst AS-CA V iaR in an auxiliary standalone-SPY benchmark r un. This auxiliar y standalone-SPY r un is based on a separate SPY -only rolling sample with 1,822 23 one-step f orecasts, whereas the aligned SPY slice in the balanced six-asset panel contains 1,730 f orecasts; the tw o e xercises are theref ore not numerically identical. AS-C A ViaR is included because it is specificall y designed f or conditional quantile dynamics and, in this auxiliary bench- mark ex ercise, delivers one of the strong est ra w o v erall per f or mances among the benc hmark models. W e also repor t GPQ as the strong est pro xy-a ware comparator . T able 6 sho w s the role of the proposed method against strong er raw tail benchmarks. For both AS-C A ViaR and GPQ, the ra w baselines already perf orm strongl y in unconditional ter ms, with acceptable e xceedance, low tick loss, and successful UC/CC/DQ diagnostics. In this benchmark e xercise, differences across recalibrated variants appear mainly in stress-period per f or mance rather than in o verall ranking. T able 6: A uxiliar y standalone-SPY compar ison agains t strong er ra w tail baselines under the clean proxy specification. These results are reported on a standalone SPY sample and are theref ore not numer icall y identical to the aligned SPY slice in T ables 5 and 7 . Stress e x ceed. denotes ex ceedance on the strict-stress subset. Backtests repor t UC/CC/DQ pass indicators at the 5% le v el. Baseline Method Ex ceed. Stress ex ceed. A vg cap. Tic k loss Backtests AS-CA ViaR Base 5.87% 7.32% 0.0177 0.001324 Y/Y/Y AS-CA ViaR 𝜌 = 1 5.49% 5.37% 0.0195 0.001365 Y/Y/Y AS-CA ViaR Global-stress 5.43% 5.85% 0.0192 0.001360 Y/Y/Y AS-CA ViaR Regime-s tress 5.54% 5.37% 0.0201 0.001404 Y/Y/N GPQ Base 5.98% 8.78% 0.0183 0.001350 Y/Y/Y GPQ 𝜌 = 1 4.88% 5.37% 0.0202 0.001374 Y/Y/N GPQ Global-stress 5.54% 5.85% 0.0198 0.001372 Y/Y/N GPQ Regime-s tress 5.38% 4.88% 0.0201 0.001382 Y/Y/N 5.3.1 Stress-period illustration The stressed SPY results in T able 7 are consistent with the panel-lev el message that s tressed performance is the main margin of interest. The historical-simulation baseline deteriorates shar pl y under strict stress, with stressed e x ceedance 0 . 240, and recalibration reduces this sub- stantiall y , although not fully to targ et. GPQ again provides the strong est stressed case among the representativ e models: the regime-stress r ule low ers strict-stress ex ceedance from 0 . 089 to 0 . 045. QR also mo v es close to targ et under stress after recalibration. These SPY results theref ore reinf orce the panel conclusion that the method is most useful as a robus tness la y er f or stressed-tail control. 24 T able 7: SPY strict stress-per iod results under the clean pro xy specification. S tress e x ceed. denotes the breach frequency conditional on the rolling s tr ict s tress flag. Stress gap is measured relativ e to the nominal 5% targ et. A v g cap. is the full-sample av erage capital proxy sho wn f or ref erence. Baseline Method Stress e xceed. Stress gap A v g cap. HS Base 0.240 0.190 0.018 HS 𝜌 = 0 0.095 0.045 0.021 HS 𝜌 = 1 0.067 0.017 0.020 HS Global-stress 0.078 0.028 0.021 HS Regime-s tress 0.078 0.028 0.021 FHS Base 0.078 0.028 0.019 FHS 𝜌 = 0 0.073 0.023 0.021 FHS 𝜌 = 1 0.061 0.011 0.021 FHS Global-stress 0.067 0.017 0.021 FHS Regime-s tress 0.061 0.011 0.022 QR Base 0.089 0.039 0.018 QR 𝜌 = 0 0.056 0.006 0.021 QR 𝜌 = 1 0.045 -0.005 0.021 QR Global-stress 0.050 0.000 0.021 QR Regime-s tress 0.050 0.000 0.022 GPQ Base 0.089 0.039 0.018 GPQ 𝜌 = 0 0.061 0.011 0.020 GPQ 𝜌 = 1 0.050 0.000 0.020 GPQ Global-stress 0.061 0.011 0.020 GPQ Regime-s tress 0.045 -0.005 0.020 GAR CH- 𝑡 Base 0.184 0.134 0.033 GAR CH- 𝑡 𝜌 = 0 0.095 0.045 0.023 GAR CH- 𝑡 𝜌 = 1 0.078 0.028 0.023 GAR CH- 𝑡 Global-stress 0.078 0.028 0.023 GAR CH- 𝑡 Regime-s tress 0.078 0.028 0.024 The SPY robus tness and regime-selection diagnostics are also aligned with the panel ev - idence. Under stress-specific pro xy underreaction, deter ioration is concentrated in higher - 𝜌 v ar iants, while GPQ remains comparativ ely stable. Let ¯ 𝜌 𝑙 𝑜 𝑤 , ¯ 𝜌 𝑚𝑖 𝑑 , and ¯ 𝜌 ℎ𝑖 𝑔 ℎ denote the sample a v erages of the selected regime-specific pro xy -reliance lev els o ver the rolling f orecast or igins. These a v erage regime-dependent selections satisfy ¯ 𝜌 𝑙 𝑜 𝑤 > ¯ 𝜌 𝑚𝑖 𝑑 > ¯ 𝜌 ℎ𝑖 𝑔 ℎ , indicating w eaker pro xy dependence in more stressed states. This patter n is structurally mean- ingful, although it does not translate into unif or m predictiv e dominance o v er simpler scalar r ules. Ov erall, the SPY e vidence suppor ts the same conclusion as the panel: pro xy -reliance-controlled recalibration is most useful where stressed tail underco v erage remains after the baseline f orecast is f or med, and 𝜌 go v erns ho w strongl y the recalibration cor rection depends on the volatility pro xy . 25 6 Discussion The results identify pr o xy r eliance as a distinct design choice in one-sided V aR recalibration. Rather than treating pro xy scaling as an implicit f eature of state-a ware adjustment, the framew ork makes that dependence e xplicit and allo w s its stressed-state implications to be studied directl y . V olatility signals are informativ e but not ground tr uth: the same pro xy that impro v es state sensitivity in nor mal times can become a source of stressed-s tate fragility when it under reacts precisel y where do wnside protection matters most. The empirical and theoretical results point to the same takea wa y: the decisive margin is stressed-s tate fragility rather than av erag e per f or mance. Se v eral baselines that appear acceptable in pooled co verag e deter iorate mater ially on the rolling str ict-stress subset, and the gains from recalibration are more consistent on that margin than in aggregate unconditional metr ics. The pro xy-misspecification e xper iments shar pen the inter pretation of 𝜌 : when the pro xy under reacts in adverse states, deter ioration appears mainly in stressed e x ceedance and is more pronounced f or higher - 𝜌 r ules. Empirically , 𝜌 behav es like a tr ust parameter on the volatility pro xy: larg er v alues deliver greater state responsiv eness, while smaller values pro vide more protection agains t pro xy er ror . The regime-dependent e xtension is most useful as a structural diagnostic rather than as a unif or mly super ior f orecasting r ule. The selected tuples are often economically sensible, with w eak er pro xy reliance in more stressed states, although the y do not deliv er unif or m gains o v er simpler scalar r ules. The same pattern appears in the auxiliary AS-C A V iaR comparison: when the ra w tail model is already strong, pro xy -reliance-controlled recalibration is best vie wed as a complementary robustness de vice. Its role is to strengthen stressed-state control rather than to substitute f or the baseline f orecasting model. The proposed method is a recalibration frame work rather than a full dynamic tail model. It often restores unconditional co v erag e and can improv e conditional co verag e, although dynamic quantile diagnostics remain challenging in man y specifications. These DQ rejections indicate that residual ser ial str ucture in tail violations can persist after one-sided recalibration, because dynamic misspecification and proxy reliance are related but distinct problems. The paper theref ore contributes a f ocused answ er to a nar ro w er but impor tant q uestion: ho w strongl y 26 a one-sided recalibration adjustment should depend on an imperfect v olatility pro xy when stress-period protection is the pr ior ity . On this dimension, both the theoretical results and the stress-period evidence are economicall y inf or mative. Se v eral limitations remain. The empir ical study is restricted to six liquid daily U .S.-traded ETFs and a common VIX -linked state pro xy ; the anal y sis is confined to one-da y-ahead left-tail V aR at the 5% le v el; and the regime-a w are specification uses a deliberately coarse three-bin par tition with a monotone restriction on ( 𝜌 𝑙 𝑜 𝑤 , 𝜌 𝑚𝑖 𝑑 , 𝜌 ℎ𝑖 𝑔 ℎ ) . In addition, the stress-a ware selector uses a looser stressed subset dur ing selection than during final repor ting, reflecting stressed- sample scarcity . N atural e xtensions include r icher state v ariables and alter nativ e pro xies, smoother state-dependent pro xy-reliance maps, tighter integration with strong er dynamic tail models, and applications to other one-sided risk functionals such as e xpected shor tf all. 7 Conclusion This paper studies one-sided V aR recalibration through the lens of pr o xy r eliance , which we f or malize by a parameter 𝜌 ∈ [ 0 , 1 ] that go verns ho w strongl y the left-tail adjustment scales with a v olatility proxy . The main finding is that pro xy reliance matters most when stressed-state undercov erag e interacts with proxy imper f ection. The theoretical results sho w that larger 𝜌 increases respon- siv eness to pro xy scale but also raises fragility under proxy underreaction, while the empir ical results sho w that lo wer or inter mediate pro xy reliance can outperf orm full y pro xy -scaled recali- bration in such settings. The regime-dependent e xtension pro vides str uctural insight but limited incremental predictiv e benefit ov er simpler global rules. Ov erall, the paper sho ws that, when v olatility proxies are inf or mativ e yet imper f ect, pro xy reliance should itself be treated as a separate and e xplicit design choice in one-sided V aR recalibration. 27 A Pr oofs and supplementary theoretical r esults This appendix collects the proofs of the main theoretical results and records two supplementar y propositions that are omitted from the main te xt f or e xpositional focus. A.1 Supplementary propositions Proposition A.1 (Heterog eneous pro xy distortion and directional f orecast shift) . F ix an expo- nent 𝜌 ∈ [ 0 , 1 ] and a f or ecast dat e 𝑡 . Let 𝑢 ( 𝜌 ) 𝑠 = 𝑌 𝑠 − b 𝑞 𝛼, 𝑠 𝑣 𝜌 𝑠 , 𝑠 ∈ I , denot e the clean-pr oxy calibr ation residuals on a calibr ation sample I , and let 𝑐 𝜌 = 𝑄 𝑙 𝑜 𝑤 𝑒 𝑟 𝛼 { 𝑢 ( 𝜌 ) 𝑠 : 𝑠 ∈ I } be the corr esponding clean-pr o xy low er -tail recalibr ation constant. Suppose the pro xy is distort ed multiplicativ ely accor ding to e 𝑣 𝑠 = 𝑑 𝑠 𝑣 𝑠 , 𝑠 ∈ I , and e 𝑣 𝑡 = 𝑑 𝑡 𝑣 𝑡 , wher e all dist ortion fact ors ar e strictly positiv e. Define the distort ed calibr ation constant e 𝑐 𝜌 = 𝑄 𝑙 𝑜 𝑤 𝑒 𝑟 𝛼 { 𝑑 − 𝜌 𝑠 𝑢 ( 𝜌 ) 𝑠 : 𝑠 ∈ I } , and the dist orted f orecas t e 𝑞 𝜌 ,𝑡 = b 𝑞 𝛼, 𝑡 + e 𝑐 𝜌 e 𝑣 𝜌 𝑡 . Assume that the clean-pr o xy r ecalibr ation constant satisfies 𝑐 𝜌 < 0 . If 𝑑 𝑡 ≤ 𝑑 𝑠 f or all 𝑠 ∈ I , 28 then e 𝑞 𝜌 ,𝑡 ≥ b 𝑞 𝛼, 𝑡 + 𝑐 𝜌 𝑣 𝜌 𝑡 . If inst ead 𝑑 𝑡 ≥ 𝑑 𝑠 f or all 𝑠 ∈ I , then e 𝑞 𝜌 ,𝑡 ≤ b 𝑞 𝛼, 𝑡 + 𝑐 𝜌 𝑣 𝜌 𝑡 . Consequently , if the clean-pro xy f or ecast is conditionally exact at lev el 𝛼 , where 𝐹 𝑡 ( 𝑦 ) : = P ( 𝑌 𝑡 ≤ 𝑦 | F 𝑡 − 1 , stress 𝑡 = 1 ) , and 𝐹 𝑡 b 𝑞 𝛼, 𝑡 + 𝑐 𝜌 𝑣 𝜌 𝑡 = 𝛼 , then for ecast-point underreaction that is at least as sever e as calibration-sample underreac- tion yields nonneg ativ e conditional exceedance distortion, while the r ev erse or dering yields nonpositiv e conditional exceedance dist ortion. Proposition A.2 (Selection implication under stress screening) . Suppose that under str ess- specific pr o xy underr eaction the av erag e str essed-stat e exceedance distortion ¯ Δ ( 𝜌 ) : = E [ Δ 𝑡 ( 𝜌 ) | stress 𝑡 = 1 ] is continuous and nondecreasing on [ 0 , 1 ] . Assume mor eov er that under the matched clean- pr o xy adjustment condition ther e exists a nonneg ative pr ocess 𝑎 𝑡 suc h that the dist orted str essed- stat e f or ecast can be written as e 𝑞 𝜌 ,𝑡 = b 𝑞 𝛼, 𝑡 − 𝑎 𝑡 𝜅 𝜌 , 𝜅 ∈ ( 0 , 1 ) , 29 f or str essed f or ecast dat es. Define the str essed-state av erag e capital pr o xy ¯ 𝐾 ( 𝜌 ) : = E max ( − e 𝑞 𝜌 ,𝑡 , 0 ) | stress 𝑡 = 1 . Then ¯ 𝐾 ( 𝜌 ) is nonincr easing in 𝜌 . F or a str ess toler ance 𝜏 ≥ 0 , consider the scr eened selector b 𝜌 ( 𝜏 ) ∈ arg min 𝜌 ∈ R ¯ 𝐾 ( 𝜌 ) subject to ¯ Δ ( 𝜌 ) ≤ 𝜏 , wher e R ⊂ [ 0 , 1 ] is the candidate g rid. Then the f easible set is of the f or m F ( 𝜏 ) = R ∩ [ 0 , 𝜌 max ( 𝜏 ) ] f or some 𝜌 max ( 𝜏 ) ∈ [ 0 , 1 ] (possibly wit h emp ty f easible set), and any minimizer can be taken to be the lar g est f easible candidate. In par ticular , if 0 ≤ 𝜏 1 ≤ 𝜏 2 , then b 𝜌 ( 𝜏 1 ) ≤ b 𝜌 ( 𝜏 2 ) . Hence tightening the str essed-stat e exceedance toler ance w eakly low ers the selected pro xy r eliance. A.2 Proofs Pr oof of Pr oposition 4.1 . For an y 𝜂 > 0, 𝐴 𝜌 ( 𝜂 𝑣 ; 𝑐 ) = 𝑐 ( 𝜂 𝑣 ) 𝜌 = 𝜂 𝜌 𝑐 𝑣 𝜌 = 𝜂 𝜌 𝐴 𝜌 ( 𝑣 ; 𝑐 ) , 30 which pro v es the homogeneity s tatement. T aking logs yields log | 𝐴 𝜌 ( 𝜂 𝑣 ; 𝑐 ) | = log | 𝑐 | + 𝜌 log 𝜂 + 𝜌 log 𝑣 , so 𝜕 log | 𝐴 𝜌 ( 𝜂 𝑣 ; 𝑐 ) | 𝜕 log 𝜂 = 𝜌 . No w suppose ˜ 𝑣 𝑡 = 𝜂 𝑣 𝑡 f or all calibration and test points. The signed residual becomes ˜ 𝑢 ( 𝜌 ) 𝑡 = 𝑌 𝑡 − b 𝑞 𝛼, 𝑡 ( 𝜂 𝑣 𝑡 ) 𝜌 = 𝜂 − 𝜌 𝑢 ( 𝜌 ) 𝑡 . Since 𝜂 − 𝜌 > 0 and the lo w er empirical conformal quantile is positiv ely homog eneous, ˜ 𝑐 𝜌 = 𝑄 𝑙 𝑜 𝑤 𝑒 𝑟 𝛼 { ˜ 𝑢 ( 𝜌 ) 𝑡 } = 𝑄 𝑙 𝑜 𝑤 𝑒 𝑟 𝛼 { 𝜂 − 𝜌 𝑢 ( 𝜌 ) 𝑡 } = 𝜂 − 𝜌 𝑄 𝑙 𝑜 𝑤 𝑒 𝑟 𝛼 { 𝑢 ( 𝜌 ) 𝑡 } = 𝜂 − 𝜌 𝑐 𝜌 . Theref ore the final signed adjustment at the f orecast point satisfies ˜ 𝑐 𝜌 ( ˜ 𝑣 𝑡 ) 𝜌 = 𝜂 − 𝜌 𝑐 𝜌 ( 𝜂 𝑣 𝑡 ) 𝜌 = 𝑐 𝜌 𝑣 𝜌 𝑡 , and hence the recalibrated f orecast is unchang ed. □ Pr oof of Pr oposition 4.2 . Since 𝐴 𝜌 ( 𝑣 ; 𝑐 ) = 𝑐 𝑣 𝜌 , | 𝐴 𝜌 ( 𝑣 𝐻 ; 𝑐 ) | | 𝐴 𝜌 ( 𝑣 𝐿 ; 𝑐 ) | = | 𝑐 | 𝑣 𝜌 𝐻 | 𝑐 | 𝑣 𝜌 𝐿 = 𝑣 𝐻 𝑣 𝐿 𝜌 . Because 𝑣 𝐻 / 𝑣 𝐿 > 1, this ratio is increasing in 𝜌 . At 𝜌 = 0 it equals 1, and at 𝜌 = 1 it equals 𝑣 𝐻 / 𝑣 𝐿 . □ Pr oof of Pr oposition A.1 . W r ite 𝑎 𝑠 : = 𝑑 𝑡 𝑑 𝑠 𝜌 , 𝑠 ∈ I . 31 Using positiv e homogeneity of the lo w er empir ical quantile, w e hav e e 𝑐 𝜌 = 𝑄 𝑙 𝑜 𝑤 𝑒 𝑟 𝛼 { 𝑑 − 𝜌 𝑠 𝑢 ( 𝜌 ) 𝑠 : 𝑠 ∈ I } , and hence e 𝑞 𝜌 ,𝑡 = b 𝑞 𝛼, 𝑡 + 𝑑 𝜌 𝑡 𝑣 𝜌 𝑡 𝑄 𝑙 𝑜 𝑤 𝑒 𝑟 𝛼 { 𝑑 − 𝜌 𝑠 𝑢 ( 𝜌 ) 𝑠 : 𝑠 ∈ I } = b 𝑞 𝛼, 𝑡 + 𝑣 𝜌 𝑡 𝑄 𝑙 𝑜 𝑤 𝑒 𝑟 𝛼 { 𝑎 𝑠 𝑢 ( 𝜌 ) 𝑠 : 𝑠 ∈ I } . Define 𝑥 𝑠 : = 𝑎 𝑠 𝑢 ( 𝜌 ) 𝑠 , 𝑠 ∈ I . Firs t suppose that 𝑑 𝑡 ≤ 𝑑 𝑠 f or all 𝑠 ∈ I . Then 𝑎 𝑠 ≤ 1 f or all 𝑠 ∈ I . W e claim that f or ev ery 𝑧 < 0, { 𝑥 𝑠 ≤ 𝑧 } ⊆ { 𝑢 ( 𝜌 ) 𝑠 ≤ 𝑧 } . Indeed, if 𝑥 𝑠 ≤ 𝑧 < 0, then necessarily 𝑢 ( 𝜌 ) 𝑠 ≤ 0, because 𝑎 𝑠 > 0. Since 𝑎 𝑠 ≤ 1 and 𝑢 ( 𝜌 ) 𝑠 ≤ 0, the inequality 𝑎 𝑠 𝑢 ( 𝜌 ) 𝑠 ≤ 𝑧 implies 𝑢 ( 𝜌 ) 𝑠 ≤ 𝑧 𝑎 𝑠 ≤ 𝑧 . Theref ore { 𝑥 𝑠 ≤ 𝑧 } ⊆ { 𝑢 ( 𝜌 ) 𝑠 ≤ 𝑧 } . It f ollow s that the empir ical distribution function of { 𝑥 𝑠 } is pointwise no larg er than that of { 𝑢 ( 𝜌 ) 𝑠 } on the neg ativ e half-line. Since 𝑐 𝜌 < 0 is the lo wer 𝛼 -quantile of the clean residuals, w e obtain 𝑄 𝑙 𝑜 𝑤 𝑒 𝑟 𝛼 ( { 𝑥 𝑠 : 𝑠 ∈ I } ) ≥ 𝑄 𝑙 𝑜 𝑤 𝑒 𝑟 𝛼 { 𝑢 ( 𝜌 ) 𝑠 : 𝑠 ∈ I } = 𝑐 𝜌 . Hence e 𝑞 𝜌 ,𝑡 = b 𝑞 𝛼, 𝑡 + 𝑣 𝜌 𝑡 𝑄 𝑙 𝑜 𝑤 𝑒 𝑟 𝛼 ( { 𝑥 𝑠 : 𝑠 ∈ I } ) ≥ b 𝑞 𝛼, 𝑡 + 𝑐 𝜌 𝑣 𝜌 𝑡 . No w suppose instead that 𝑑 𝑡 ≥ 𝑑 𝑠 f or all 𝑠 ∈ I . Then 𝑎 𝑠 ≥ 1 f or all 𝑠 ∈ I . For e very 𝑧 < 0, 32 if 𝑢 ( 𝜌 ) 𝑠 ≤ 𝑧 , then necessar ily 𝑢 ( 𝜌 ) 𝑠 ≤ 0, and so 𝑥 𝑠 = 𝑎 𝑠 𝑢 ( 𝜌 ) 𝑠 ≤ 𝑢 ( 𝜌 ) 𝑠 ≤ 𝑧 . Thus { 𝑢 ( 𝜌 ) 𝑠 ≤ 𝑧 } ⊆ { 𝑥 𝑠 ≤ 𝑧 } . Theref ore the empirical dis tr ibution function of { 𝑥 𝑠 } is pointwise no smaller than that of { 𝑢 ( 𝜌 ) 𝑠 } on the negativ e half-line, which implies 𝑄 𝑙 𝑜 𝑤 𝑒 𝑟 𝛼 ( { 𝑥 𝑠 : 𝑠 ∈ I } ) ≤ 𝑐 𝜌 . Consequentl y , e 𝑞 𝜌 ,𝑡 ≤ b 𝑞 𝛼, 𝑡 + 𝑐 𝜌 𝑣 𝜌 𝑡 . For the final claim, if 𝐹 𝑡 b 𝑞 𝛼, 𝑡 + 𝑐 𝜌 𝑣 𝜌 𝑡 = 𝛼 , then monotonicity of 𝐹 𝑡 implies that an upward shift in the f orecast threshold yields nonneg ativ e e xceedance distortion, whereas a do wnw ard shift yields nonpositiv e e xceedance distortion. □ Pr oof of Pr oposition 4.3 . If 𝜌 > 0, then 𝜅 𝜌 < 1. Since 𝑐 𝜌 ,𝑡 < 0, we ha v e e 𝑞 𝜌 ,𝑡 = b 𝑞 𝛼, 𝑡 + 𝑐 𝜌 ,𝑡 𝜅 𝜌 𝑣 𝜌 𝑡 > b 𝑞 𝛼, 𝑡 + 𝑐 𝜌 ,𝑡 𝑣 𝜌 𝑡 = 𝑞 ∗ 𝜌 ,𝑡 . If 𝜌 = 0, then 𝜅 𝜌 = 1, so e 𝑞 𝜌 ,𝑡 = 𝑞 ∗ 𝜌 ,𝑡 . Theref ore, f or all 𝜌 ∈ [ 0 , 1 ] , 𝐹 𝑡 ( e 𝑞 𝜌 ,𝑡 ) − 𝐹 𝑡 ( 𝑞 ∗ 𝜌 ,𝑡 ) ≥ 0 . Using the conditional e xactness assumption 𝐹 𝑡 ( 𝑞 ∗ 𝜌 ,𝑡 ) = 𝛼 , it f ollow s that Δ 𝑡 ( 𝜌 ) = 𝐹 𝑡 ( e 𝑞 𝜌 ,𝑡 ) − 𝐹 𝑡 ( 𝑞 ∗ 𝜌 ,𝑡 ) ≥ 0 . 33 If moreo v er 𝐹 𝑡 is differentiable on ( 𝑞 ∗ 𝜌 ,𝑡 , e 𝑞 𝜌 ,𝑡 ) , then f or 𝜌 > 0 the mean-v alue theorem yields some 𝜉 𝜌 ,𝑡 ∈ ( 𝑞 ∗ 𝜌 ,𝑡 , e 𝑞 𝜌 ,𝑡 ) such that 𝐹 𝑡 ( e 𝑞 𝜌 ,𝑡 ) − 𝐹 𝑡 ( 𝑞 ∗ 𝜌 ,𝑡 ) = 𝑓 𝑡 ( 𝜉 𝜌 ,𝑡 ) e 𝑞 𝜌 ,𝑡 − 𝑞 ∗ 𝜌 ,𝑡 . Since e 𝑞 𝜌 ,𝑡 − 𝑞 ∗ 𝜌 ,𝑡 = 𝑐 𝜌 ,𝑡 𝜅 𝜌 𝑣 𝜌 𝑡 − 𝑐 𝜌 ,𝑡 𝑣 𝜌 𝑡 = | 𝑐 𝜌 ,𝑡 | 𝑣 𝜌 𝑡 ( 1 − 𝜅 𝜌 ) , this prov es ( 24 ) f or 𝜌 > 0. For 𝜌 = 0, both sides of ( 24 ) eq ual 0. The bounds in ( 25 ) then f ollo w immediatel y from 𝑓 𝑡 ≤ 𝑓 𝑡 ( 𝜉 𝜌 ,𝑡 ) ≤ 𝑓 𝑡 . □ Pr oof of Cor ollar y 4.4 . Substituting the matc hed-adjustment condition | 𝑐 𝜌 | 𝑣 𝜌 𝑡 = 𝑎 𝑡 into Proposition 4.3 giv es Δ 𝑡 ( 𝜌 ) = 𝑓 𝑡 ( 𝜉 𝜌 ,𝑡 ) 𝑎 𝑡 ( 1 − 𝜅 𝜌 ) , and like wise 𝑓 𝑡 𝑎 𝑡 ( 1 − 𝜅 𝜌 ) ≤ Δ 𝑡 ( 𝜌 ) ≤ 𝑓 𝑡 𝑎 𝑡 ( 1 − 𝜅 𝜌 ) . Since 𝜅 ∈ ( 0 , 1 ) , 𝑑 𝑑 𝜌 ( 1 − 𝜅 𝜌 ) = − 𝜅 𝜌 log 𝜅 > 0 , so the factor 1 − 𝜅 𝜌 is increasing in 𝜌 . Therefore Δ 𝑡 ( 𝜌 ) is increasing in 𝜌 up to the density f actor . In par ticular , if 𝑓 𝑡 ( 𝜉 𝜌 ,𝑡 ) is constant in 𝜌 , or more g enerally nondecreasing, then Δ 𝑡 ( 𝜌 ) is increasing in 𝜌 . □ Pr oof of Pr oposition A.2 . Since 𝜅 ∈ ( 0 , 1 ) , the map 𝜌 ↦→ 𝜅 𝜌 is decreasing on [ 0 , 1 ] . Theref ore 34 f or each stressed f orecast date 𝑡 , e 𝑞 𝜌 ,𝑡 = b 𝑞 𝛼, 𝑡 − 𝑎 𝑡 𝜅 𝜌 is nondecreasing in 𝜌 , because 𝑎 𝑡 ≥ 0. Since the function 𝑥 ↦→ max ( − 𝑥 , 0 ) is nonincreasing in 𝑥 , it f ollo w s that max ( − e 𝑞 𝜌 ,𝑡 , 0 ) is nonincreasing in 𝜌 f or each stressed date 𝑡 . T aking conditional e xpectation giv es that ¯ 𝐾 ( 𝜌 ) is nonincreasing in 𝜌 . Ne xt, since ¯ Δ ( 𝜌 ) is continuous and nondecreasing on [ 0 , 1 ] , the sublev el set { 𝜌 ∈ [ 0 , 1 ] : ¯ Δ ( 𝜌 ) ≤ 𝜏 } is an interv al of the f or m [ 0 , 𝜌 max ( 𝜏 ) ] or is empty . Intersecting with the finite candidate grid R yields F ( 𝜏 ) = R ∩ [ 0 , 𝜌 max ( 𝜏 ) ] . Because ¯ 𝐾 ( 𝜌 ) is nonincreasing in 𝜌 , minimizing ¯ 𝐾 ( 𝜌 ) ov er the f easible set is eq uiv alent to choosing the lar g est f easible candidate. Theref ore an y minimizer can be tak en as b 𝜌 ( 𝜏 ) = max F ( 𝜏 ) , whene v er the feasible set is nonempty . Finall y , if 0 ≤ 𝜏 1 ≤ 𝜏 2 , then { 𝜌 : ¯ Δ ( 𝜌 ) ≤ 𝜏 1 } ⊆ { 𝜌 : ¯ Δ ( 𝜌 ) ≤ 𝜏 2 } , 35 so F ( 𝜏 1 ) ⊆ F ( 𝜏 2 ) . Hence max F ( 𝜏 1 ) ≤ max F ( 𝜏 2 ) , which implies b 𝜌 ( 𝜏 1 ) ≤ b 𝜌 ( 𝜏 2 ) . This pro ves that tighter s tressed-state tolerance w eakl y lo wers the selected pro xy reliance. □ B A dditional GJR -GAR CH- 𝑡 results T able 8: Additional SPY clean-pro xy results f or the GJR -GAR CH- 𝑡 baseline. Ex ceed. and A v g cap. are computed on the full aligned SPY test sample. Stress ex ceed. and Stress cap. are computed on the rolling strict-stress subset. Tic k loss denotes full-sample quantile tick loss. Method Ex ceed. Stress ex ceed. A vg cap. Stress cap. Tic k loss UC CC DQ Base 0.0503 0.2402 0.0197 0.0119 0.001700 Y N N 𝜌 = 0 0.0503 0.0950 0.0210 0.0335 0.001600 Y Y N 𝜌 = 1 0.0514 0.0838 0.0202 0.0335 0.001500 Y N N Global-av erage 0.0491 0.0782 0.0208 0.0344 0.001500 Y Y N Global-stress 0.0497 0.0894 0.0205 0.0340 0.001500 Y Y N Regime-a verag e 0.0549 0.0838 0.0215 0.0392 0.001600 Y N N Regime-s tress 0.0462 0.0726 0.0216 0.0381 0.001500 Y Y N C A dditional Implementation Details C.1 R olling design All empir ical results are produced in a strictly chronological rolling design. F or each forecas t origin, the sample is divided into a training windo w of 504 observ ations, a calibration-selection windo w of 252 obser v ations, a final calibration windo w of 126 obser v ations, and a one-step test point. The calibration-selection windo w is split into a 𝜌 -fit block of 84 obser vations and a 𝜌 -ev aluation block of 168 observations. 36 At each forecas t origin, the baseline V aR model is fitted on the training block only . Candidate pro xy-reliance r ules are compared on the calibration-selection block. After a rule has been selected, the recalibration constant is re-estimated on the final calibration block and applied to the one-step test f orecast. All regime thresholds, stress flags, pro xy nor malizations, and recalibration quantities are recomputed within each rolling windo w using onl y inf or mation a v ailable at the f orecast date. C.2 Composite v olatility pro xy The v olatility pro xy used in the recalibration la y er combines 20-da y rolling v olatility , a GAR CH- sty le v olatility pro xy , and the VIX -based dail y volatility transf or mation. Let C = { 𝑐 1 , 𝑐 2 , 𝑐 3 } denote these components. Within each rolling training windo w , each component is normalized b y its in-sample median, 𝑚 𝑗 = max median ( 𝑐 𝑗 ) , 10 − 8 , 𝑗 = 1 , 2 , 3 , and the pro xy on subset 𝑆 is defined by 𝑣 𝑡 = © « 1 3 3 𝑗 = 1 𝑐 𝑗 ,𝑡 𝑚 𝑗 ª ® ¬ 𝑚 1 , 𝑡 ∈ 𝑆 . A small floor is imposed to ensure positivity , 𝑣 𝑡 ← max ( 𝑣 𝑡 , 10 − 8 ) . In implementation, the G AR CH-sty le component is obtained from e xpanding-windo w one- step-ahead conditional volatility estimates whene v er the arch packag e is av ailable; other wise, or when a local fit f ails, the cor responding pro xy value is replaced by the EWMA volatility estimate. 37 C.3 Baseline f orecasters T able 9 summar izes the baseline V aR f orecasters used in the empirical anal y sis. T able 9: Baseline V aR f orecasters used in the implementation. Baseline Implementation summary Historical simulation (HS) Empirical 𝛼 -quantile of training-window returns. Filtered historical simulation (FHS) Let 𝜎 EWMA 𝑡 denote ewma v ol 20. W e compute the empir ical low er -tail quantile of ( 𝑌 𝑡 − ¯ 𝑌 ) / 𝜎 EWMA 𝑡 on the training block and rescale b y the cur rent EWMA volatility le v el. Quantile regression (QR) Linear quantile regression fitted on the full predictor v ector after f eature standardization, implemented as a StandardScaler follo wed b y QuantileRegressor with quantile lev el 𝛼 , 𝐿 1 -penalty parameter 10 − 4 , and highs solv er. The predictor v ector includes retur n lags, historical and EWMA volatility measures, the GAR CH-sty le v olatility pro xy , Parkinson and Garman–Klass rang e proxies, VIX -based variables, drawdo wn, and rolling v olume f eatures. GAR CH-proxy quantile (GPQ) Let 𝜎 GPQ 𝑡 denote garch vol pro xy. W e compute the empir ical low er -tail quantile of ( 𝑌 𝑡 − ¯ 𝑌 ) / 𝜎 GPQ 𝑡 on the training block and rescale b y the cur rent proxy le vel. When the GAR CH- sty le pro xy is una vailable at a giv en point, it is replaced by e wma vol 20. GAR CH- 𝑡 V aR P arametric constant-mean GAR CH(1,1) model with Student- 𝑡 innov ations, fitted on training returns and used to generate the implied low er-tail quantile path o ver the e valuation hor izon. GJR -GAR CH- 𝑡 V aR Parametric constant-mean GJR -GAR CH(1,1) model with Student- 𝑡 innov ations, fitted on training returns and used to generate the implied lo wer -tail q uantile path ov er the e valuation horizon. For the GAR CH-sty le pro xy used in GPQ and in the composite recalibration pro xy , w e compute e xpanding-window one-step-ahead conditional volatility estimates with a lookbac k length of 252 obser vations whene v er the arch packag e is a v ailable. The pro xy fit uses a constant- mean G AR CH(1,1) specification with nor mal innov ations. If the packag e is unav ailable or a local fit f ails, the cor responding pro xy value is replaced b y ewma v ol 20. For the GAR CH- 𝑡 and GJR -GAR CH- 𝑡 baselines, the fitted model g enerates a multi-step path of conditional lo wer -tail quantiles o v er the rele v ant ev aluation block. If a parametr ic volatility fit fails, the implementation falls bac k to historical simulation f or that rolling windo w . In the auxiliary standalone SPY benchmark compar ison, AS-C A V iaR is also included as a strong er ra w tail benchmark and is estimated b y bounded multi-start optimization of the asymmetric C A ViaR q uantile-loss objectiv e. C.4 Pro xy -reliance selection For the scalar specification, candidate v alues are searched o v er R = { 0 , 0 . 1 , 0 . 2 , . . . , 1 . 0 } . 38 For each 𝜌 ∈ R , the recalibration constant is estimated on the 𝜌 -fit block and the resulting f orecast is e v aluated on the 𝜌 -e v aluation block. T w o scalar selectors are used. The g lobal av erag e select or chooses the candidate with the smallest av erag e capital pro xy on the ev aluation block. The g lobal str ess-awar e selector instead emphasizes adv erse-state control using a looser stress subset. The initial selection-s tag e stress threshold is based on the 70th percentile of the rolling training-windo w VIX -based daily v olatility measure and is relaxed, if necessar y , until a minimum stressed count is reached. A candidate is treated as f easible if its stress-per iod ex ceedance and ov erall ex ceedance remain within prespecified tolerances; among f easible candidates, the selector trades off stress-period pinball loss and a v erage capital, while inf easible cases are handled b y a penalized objectiv e. For the regime-dependent specification, the rolling training-windo w VIX distribution de- fines lo w -, medium-, and high-stress regimes through the median and 80th percentile cutoffs. Candidate rules are searched o v er monotone tuples ( 𝜌 𝑙 𝑜 𝑤 , 𝜌 𝑚𝑖 𝑑 , 𝜌 ℎ𝑖 𝑔 ℎ ) , 𝜌 𝑙 𝑜 𝑤 ≥ 𝜌 𝑚𝑖 𝑑 ≥ 𝜌 ℎ𝑖 𝑔 ℎ , with each component dra wn from { 0 , 0 . 25 , 0 . 50 , 0 . 75 , 1 . 0 } . For each candidate tuple, a single recalibration constant is estimated after scaling residuals b y the regime-specific exponent. The regime-av erag e selector trades off av erage capital and a smoothness penalty , while the regime-stress selector replaces the scalar stress subset with the high-stress regime and applies an analogous f easibility -and-penalty logic. C.5 Pro xy misspecification and e valuation T w o pro xy scenarios are studied. Under the clean pro xy , the composite volatility pro xy is used as constructed. Under the underreacting str ess pr o xy , the proxy is shr unk on stress dates according to 𝑣 𝑚𝑖 𝑠 𝑡 = 𝜅 𝑣 𝑡 , 𝜅 = 0 . 4 . 39 In the repor ted implementation, the stress dates used in this misspecification e xper iment are defined b y the rolling strict-stress rule in the main te xt. For each f orecast date, the implementation records the realized retur n, the baseline V aR f orecast, the recalibrated V aR f orecast, the signed recalibration shift, the e x ceedance indica- tor , the selected pro xy -reliance lev el, and the associated regime and stress labels. R epor ted performance metr ics include unconditional e x ceedance, strict-stress e x ceedance, av erag e cap- ital, quantile tick loss, the Kupiec unconditional co v erage test, the Chr istoffersen conditional co verag e test, and a DQ-s ty le dynamic quantile diagnos tic. Disclosure statement The authors repor t no potential conflict of interest. Funding No e xternal funding was receiv ed f or this research. Data a v ailability statement The data used in this study w ere obtained from public sources cited in the te xt, including the T w el ve Data API ( https://api.twelvedata.com ) and publicly av ailable VIX data. Processed data and replication mater ials are av ailable to the editor and re vie w ers upon reasonable reques t dur ing the re vie w process. Code a vailability Code used to g enerate the empir ical results is av ailable to the editor and re view ers upon reasonable request during the revie w process. A public replication repositor y will be provided after the re vie w process. 40 R ef erences Viral V . A chary a, Lasse H. P edersen, Thomas Philippon, and Matthe w Ric hardson. Measur ing sy stemic risk. Rev . F inanc. Stud. , 30(1):2–47, 2017. doi: 10.1093/ r fs/hhw088. T obias Adrian and Mark us K. Br unner meier . CoV aR. Am. Econ. Rev . , 106(7):1705–1741, 2016. doi: 10.1257/aer .20120555. Agnideep Aich, Ashit Baran Aich, and Dipak C. Jain. T emporal conf or mal prediction (TCP): A distribution-free statistical and machine lear ning framew ork f or adaptiv e risk f orecasting, 2025. URL . arXiv prepr int. T orben G. Andersen and Tim Bollerslev . Answ er ing the skeptics: y es, standard v olatility models do pro vide accurate f orecasts. Int. Econ. Rev . , 39(4):885–905, 1998. doi: 10.2307/2527343. T orben G. Andersen, T im Bollerslev , Francis X. Diebold, and Paul Lab ys. Modeling and f orecasting realized v olatility . Econome trica , 71(2):579–625, 2003. doi: 10.1111/1468- 0262. 00418. Andre w Ang and Geert Bekaert. Inter national asset allocation with regime shifts. Rev . F inanc. Stud. , 15(4):1137–1187, 2002. doi: 10.1093/ r fs/15.4.1137. Anastasios N . Angelopoulos and Stephen Bates. Conf ormal prediction: A g entle introduction. F ound. T rends Mac h. Lear n. , 16(4):494–591, 2023. doi: 10.1561/2200000101. Da vid Ardia, K ev en Bluteau, Kris Boudt, and Leopoldo Catania. Forecas ting risk with marko v - switching G AR CH models: A larg e-scale per f or mance study . Int. J. F orecas t. , 34(4):733– 747, 2018. doi: 10.1016/j.ijf orecast.2018.05.004. Y unf ei Bai and Charlie X. Cai. Predicting VIX with adaptive machine lear ning. Quant. F inance , 24(12):1857–1873, 2024. doi: 10.1080/14697688.2024.2439458. Gio vanni Barone- A desi, K ostas Giannopoulos, and Les V osper . V aR without correlations f or por tf olios of derivativ e secur ities. J. F utur es Mark. , 19(5):583–602, 1999. doi: 10.1002/ (SICI)1096- 9934(199908)19:5 ⟨ 583::AID- FUT5 ⟩ 3.0.CO;2- S. 41 Basel Committee on Banking Supervision. Minimum capital requirements f or market risk. T echnical repor t, Bank f or Inter national Settlements, 2019. URL https://www.bis.org/ bcbs/publ/d457.htm . Corrected version published 25 F ebr uar y 2019. Osber t Bastani, V ar un Gupta, Christopher Jung, Geor gy Noaro v , Ram ya Rama- lingam, and Aaron Roth. Practical adv ersar ial multiv alid conf or mal prediction. In Adv ances in Neur al Inf or mation Pr ocessing Sy st ems 35 , pages 29362–29373, 2022. URL https://proceedings.neurips.cc/paper_files/paper/2022/hash/ bcdaaa1aec3ae2aa39542acefdec4e4b- Abstract- Conference.html . Tim Bollersle v . Generalized autoregressiv e conditional heteroskedasticity . J. Econom. , 31(3): 307–327, 1986. doi: 10.1016/0304- 4076(86)90063- 1. Victor Chernozhuko v , Kaspar W ¨ uthrich, and Yinchu Zhu. Exact and robust conf ormal in- f erence methods f or predictive machine lear ning with dependent data. In Pr oceedings of the 31st Confer ence on Lear ning Theor y , v olume 75 of Proceedings of Machine Lear ning Resear ch , pages 732–749. PMLR, 2018. URL https://proceedings.mlr.press/v75/ chernozhukov18a.html . P eter F . Chr istoffersen. Ev aluating inter val f orecasts. Int. Econ. Rev . , 39(4):841–862, 1998. doi: 10.2307/ 2527341. P eter F . Chr istoffersen. Elements of financial risk manag ement . Academic Press, W altham, MA, 2nd edition, 2012. R ober t F . Engle. Autoregressiv e conditional heteroscedasticity with estimates of the variance of united kingdom inflation. Econometrica , 50(4):987–1007, 1982. doi: 10.2307/1912773. R ober t F . Engle and Simone Mang anelli. CA V iaR: Conditional autoregressive value at risk by regression quantiles. J. Bus. Econ. Stat. , 22(4):367–381, 2004. doi: 10.1198/ 073500104000000370. Dean Fantazzini. A daptiv e conf or mal inf erence f or computing mark et r isk measures: An anal y sis with f our thousand cr ypto-assets. J. Risk F inancial Manag. , 17(6):248, 2024. doi: 10.3390/jr fm17060248. 42 Mark B. Garman and Michael J. Klass. On the estimation of security price v olatilities from historical data. J. Bus. , 53(1):67–78, 1980. doi: 10.1086/296072. Isaac Gibbs and Emmanuel J. Cand ` es. Adaptiv e conf or mal inf erence under distribution shift. In Advances in Neur al Inf ormation Processing Sys tems 34 , pages 1660–1672, 2021. URL https://proceedings.neurips.cc/paper_files/paper/2021/hash/ 0d441de75945e5acbc865406fc9a2559- Abstract.html . Paul Glasser man, Chulmin Kang, and W anmo Kang. Stress scenar io selection b y empirical likelihood. Quant. F inance , 15(1):25–41, 2015. doi: 10.1080/ 14697688.2014.926019. James D. Hamilton. A ne w approach to the economic anal ysis of nons tationary time series and the business cy cle. Econometrica , 57(2):357–384, 1989. doi: 10.2307/1912559. John Hull and Alan White. Incor porating v olatility updating into the historical simulation method f or value-at-risk. J. Risk , 1(1):5–19, 1998. doi: 10.21314/JOR.1998.001. Masahiro Kato. Conf or mal predictive por tf olio selection, 2024. URL abs/2410.16333 . arXiv prepr int. R oger Koenk er . Quantile reg r ession , v olume 38 of Econometric Society Monog raphs . Cam- bridge U niversity Press, Cambridg e, 2005. doi: 10.1017/CBO9780511754098. Paul H. Kupiec. T echniques f or v er ifying the accuracy of risk measurement models. J. Deriv a- tiv es , 3(2):73–84, 1995. doi: 10.3905/jod.1995.407942. Nik olas Michael, Mihai Cucur ingu, and Sam Ho wison. Options-dr iven volatility f orecasting. Quant. F inance , 25(3):443–470, 2025. doi: 10.1080/14697688.2025.2454623. Fernando Moreno-Pino and Stef an Zohren. DeepV ol: v olatility f orecasting from high-frequency data with dilated causal conv olutions. Quant. F inance , 24(8):1105–1127, 2024. doi: 10. 1080/14697688.2024.2387222. Michael P arkinson. The e xtreme v alue method f or estimating the v ar iance of the rate of return. J. Bus. , 53(1):61–65, 1980. doi: 10.1086/296071. 43 Ser -Huang P oon and Cliv e W . J. Grang er . F orecasting v olatility in financial mark ets: A re vie w . J. Econ. Lit. , 41(2):478–539, 2003. doi: 10.1257/002205103765762743. Marc Schmitt. T aming tail r isk in financial markets: conf ormal r isk control f or nonstationar y por tf olio V aR, 2026. URL . arXiv prepr int. Giuseppe Storti and Chao W ang. A semi-parametr ic dynamic conditional cor relation frame w ork f or risk f orecasting. Quant. F inance , 25(1):31–49, 2025. doi: 10.1080/14697688.2024. 2446740. Vladimir V o vk, Ale xander Gammerman, and Glenn Shafer . Algorit hmic lear ning in a random w or ld . Spr inger , Ne w Y ork, NY , 2005. doi: 10.1007/ b106715. Du- Yi W ang, Guo Liang, Kun Zhang, and Qianw en Zhu. R eliable real-time value at risk estimation via quantile regression f orest with conf ormal calibration, 2026. URL https: //arxiv.org/abs/2602.01912 . arXiv prepr int. R ober t E. Whale y . Unders tanding the VIX. J. P ortf. Manag. , 35(3):98–105, 2009. doi: 10.3905/JPM.2009.35.3.098. Chen X u, Hany ang Jiang, and Y ao Xie. Conf or mal prediction f or multi-dimensional time series b y ellipsoidal sets. In Pr oceedings of the 41st International Confer ence on Mac hine Learning , v olume 235 of Proceedings of Machine Lear ning Resear ch , pages 55076–55099. PMLR, 2024. URL https://proceedings.mlr.press/v235/xu24m.html . Jingy an Zhang, Cong Ma, and Wim Schoutens. Forward-looking phy sical tail r isk: a deep learning approach. Quant. Finance , 2026. doi: 10.1080/14697688.2026.2623897. Published online 25 February 2026. 44

Original Paper

Loading high-quality paper...

Comments & Academic Discussion

Loading comments...

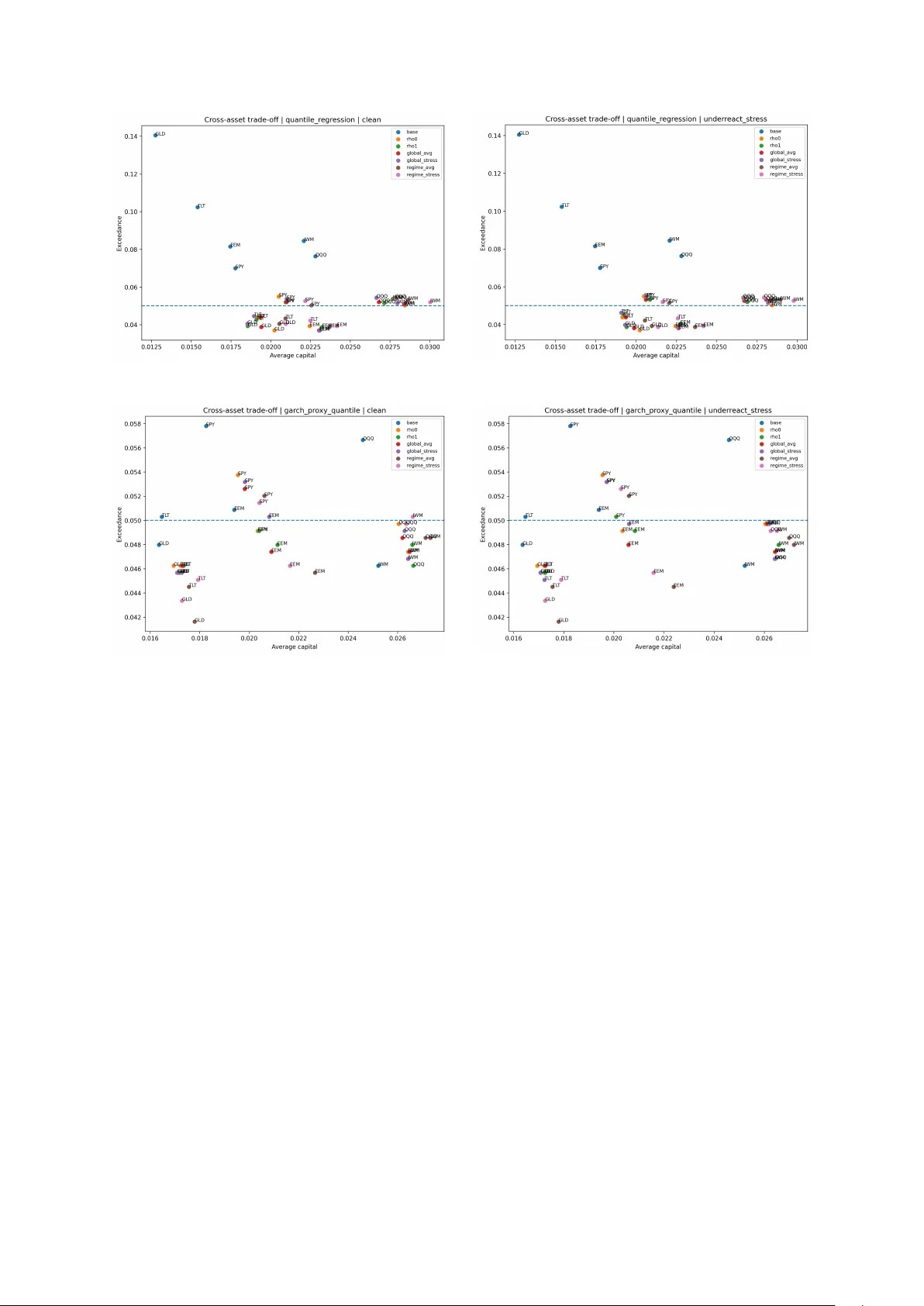

Leave a Comment