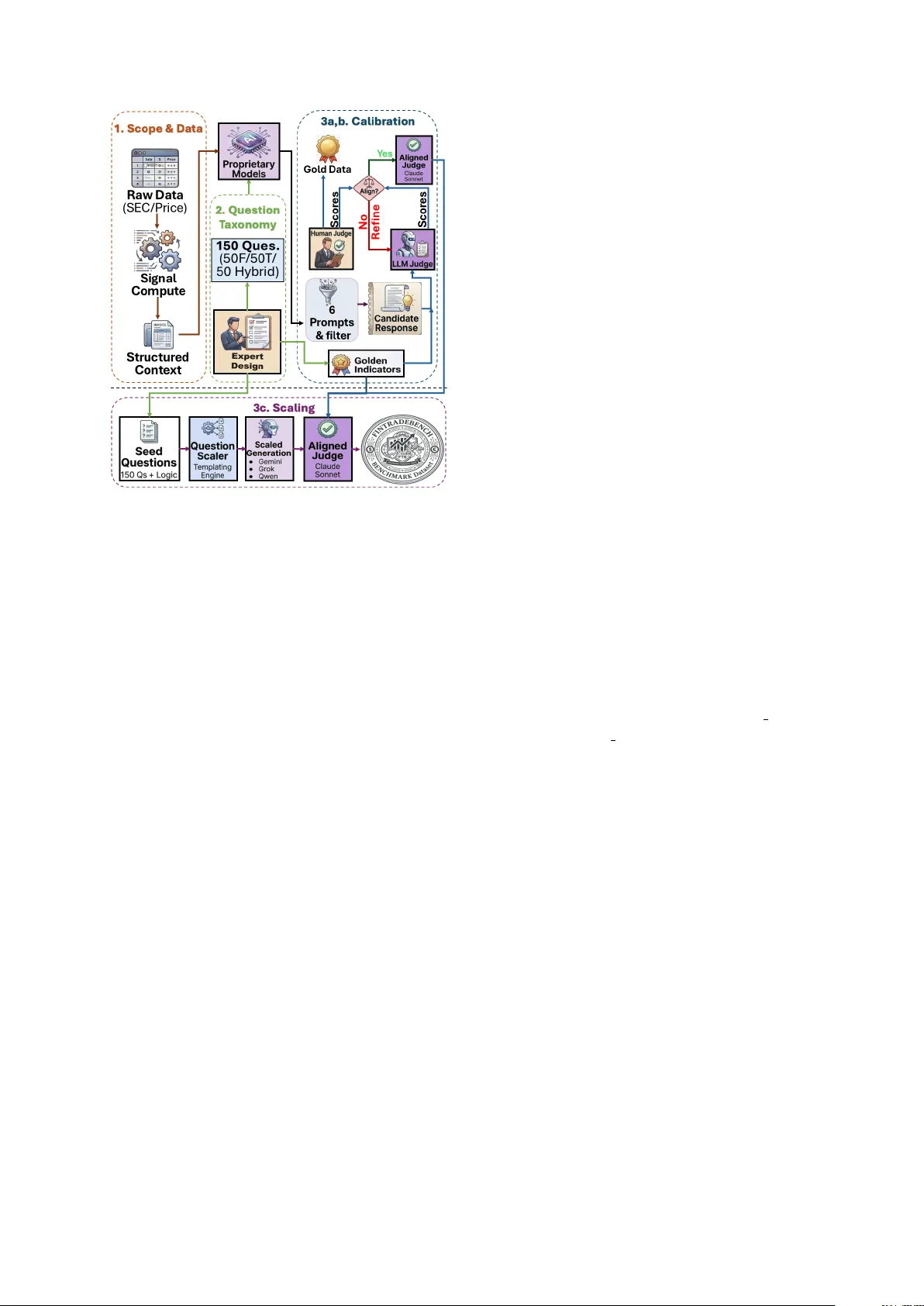

FinTradeBench: A Financial Reasoning Benchmark for LLMs

Real-world financial decision-making is a challenging problem that requires reasoning over heterogeneous signals, including company fundamentals derived from regulatory filings and trading signals computed from price dynamics. Recently, with the adva…

Authors: Yogesh Agrawal, Aniruddha Dutta, Md Mahadi Hasan