ARTEMIS: A Neuro Symbolic Framework for Economically Constrained Market Dynamics

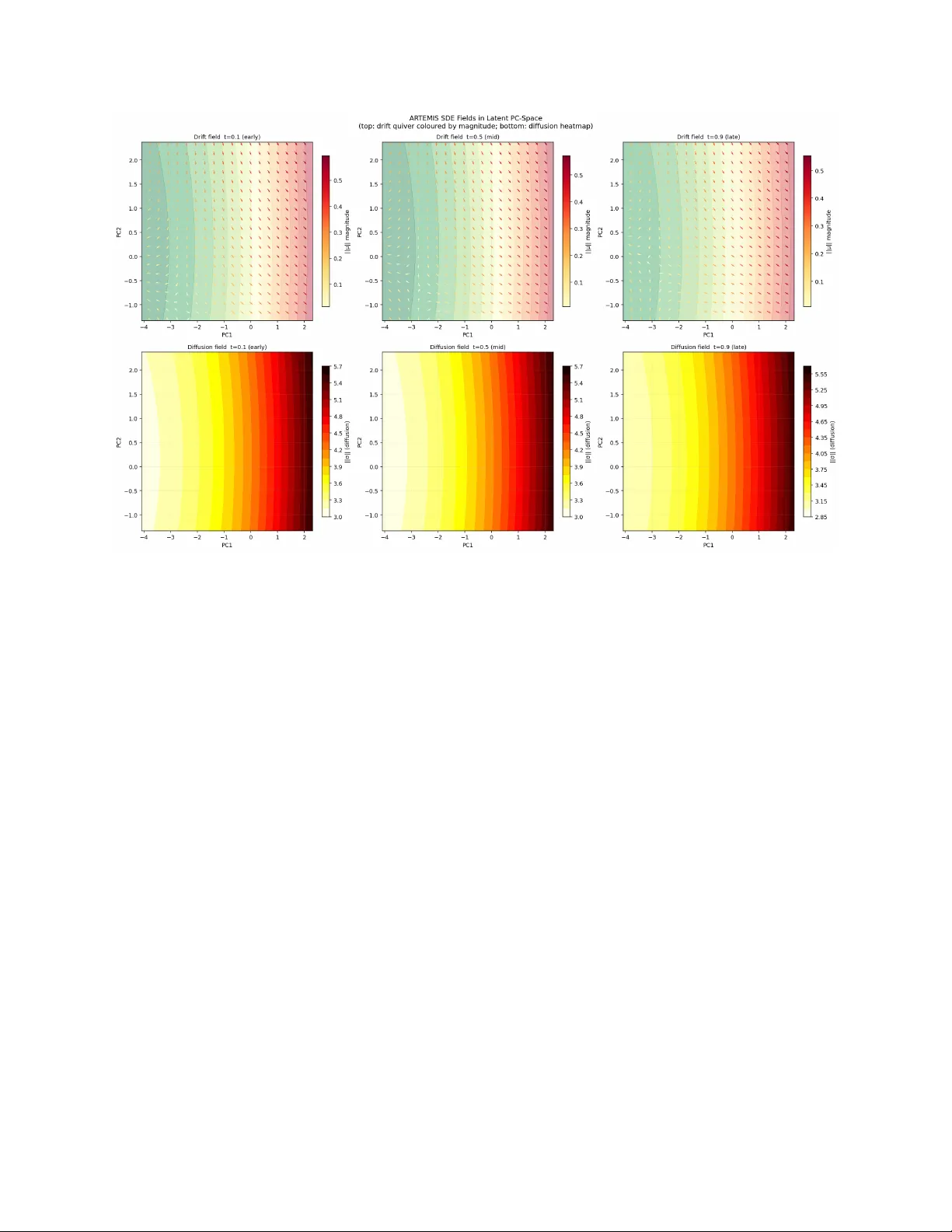

Deep learning models in quantitative finance often operate as black boxes, lacking interpretability and failing to incorporate fundamental economic principles such as no-arbitrage constraints. This paper introduces ARTEMIS (Arbitrage-free Representat…

Authors: Rahul D Ray