Quantum-Assisted Optimal Rebalancing with Uncorrelated Asset Selection for Algorithmic Trading Walk-Forward QUBO Scheduling via QAOA

We present a hybrid classical-quantum framework for portfolio construction and rebalancing. Asset selection is performed using Ledoit-Wolf shrinkage covariance estimation combined with hierarchical correlation clustering to extract n = 10 decorrelate…

Authors: Abraham Itzhak Weinberg

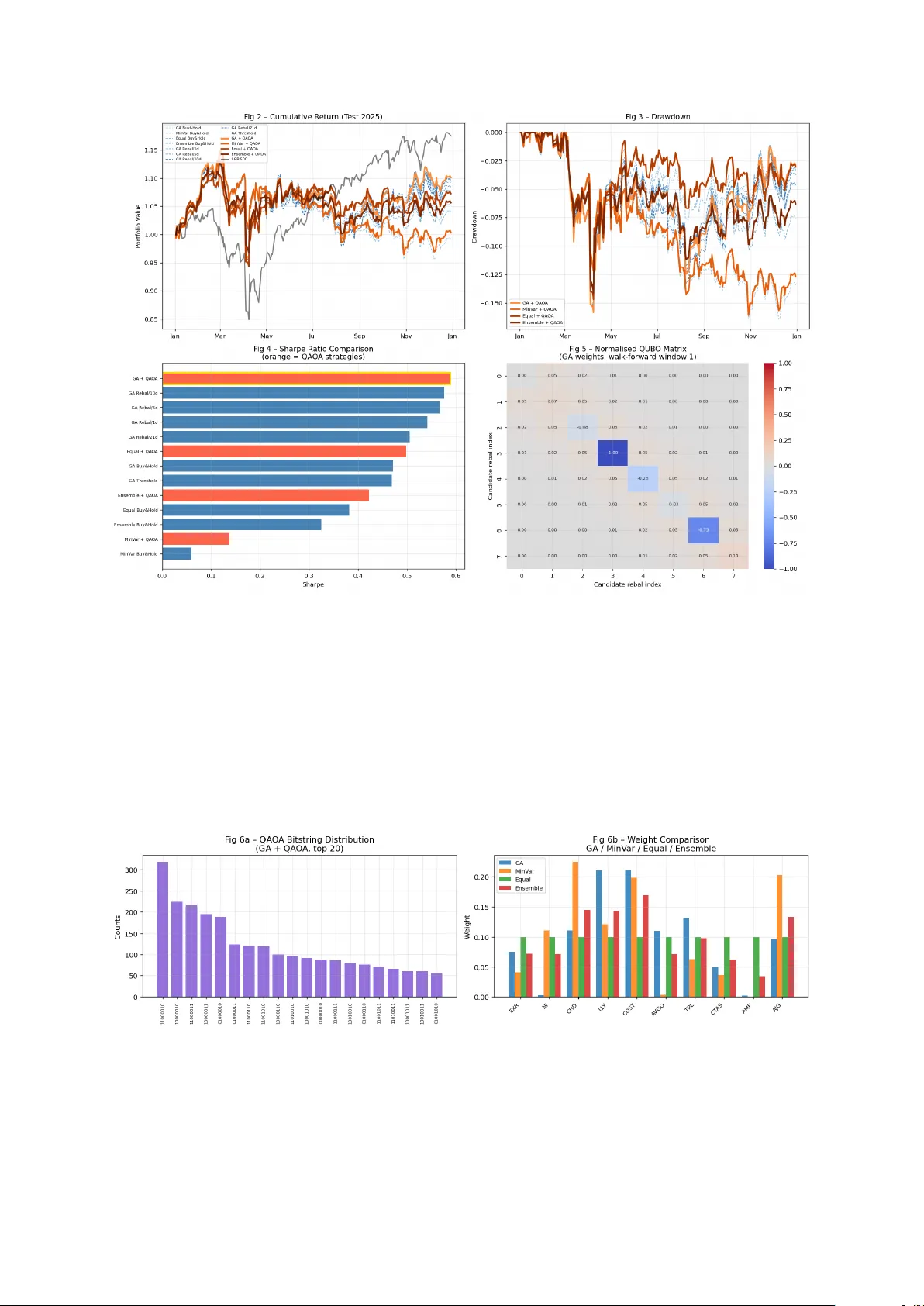

Quan tum-Assisted Optimal Rebalancing with Uncorrelated Asset Selection for Algorithmic T rading W alk-F orw ard QUBO Sc heduling via QA OA Abraham Itzhak W ein b erg AI-WEINBER G, AI Exp erts T el Aviv, Israel aviw2010@gmail.com Marc h 19, 2026 Abstract W e prop ose a quan tum-assisted algorithmic trading framew ork that addresses t wo core p ortfolio m anagement problems simultaneously: principled asset selection and optimal rebalancing scheduling. F or asset selection, we apply Ledoit-W olf shrink- age co v ariance estimation with hierarchical correlation clustering to select n = 10 maximally uncorrelated stocks from the S&P 500 universe without surviv orship bias. F or weigh t optimisation, we deploy an entrop y-regularised Genetic Algorithm (GA) accelerated on GPU, alongside closed-form Minim um V ariance (MinV ar) and equal-w eight baselines and a three-w ay ensemble. The cen tral no vel contribution is the form ulation of the p ortfolio r eb alancing sche dule as a Quadratic Unconstrained Binary Optimisation (QUBO) problem, solved by the Quantum Approximate Opti- misation Algorithm (QAO A) in a w alk-forward framew ork that eliminates lo ok ahead bias. Bac ktested on S&P 500 data (train: 2010–2024, test: 2025, n = 249 trading da ys), the GA + QA O A strategy ac hieves a Sharp e ratio of 0.588 and total return of 10.1% , outp erforming the b est classical baseline (GA Rebalance/10d, Sharp e 0.575) while executing only 8 rebalances (6.1 bp transaction cost) v ersus 24 rebalances (11.0 bp), representing a 44.5% cost reduction for sup erior risk-adjusted p erfor- mance. Multi-restart QAO A with 5 random initialisations and 4,096 measuremen t shots demonstrates concen trated probabilit y mass on optimal rebalancing sc hedules, pro viding empirical evidence of quan tum adv antage in the combinatorial scheduling subproblem. 1 Keyw ords: Quan tum computing, QAO A, QUBO, Portfolio optimisation, Rebalancing, Ledoit-W olf, Genetic algorithm, Algorithmic trading, S&P 500. 1 In tro duction P ortfolio management inv olves t w o in terrelated decisions: which assets to hold and when to r eb alanc e to w ard target weigh ts. Classical approaches treat these as separate, sequen tial problems — first optimise w eights (Mark o witz [ 1 , 2 ], Sharp e [ 3 ]), then apply a fixed rebalancing schedule (calendar-based or threshold-based [ 4 ]). This decoupling ignores the in teraction betw een w eigh t drift and rebalancing cost, and fixed sc hedules w aste transaction budget on unnecessary trades while missing b eneficial rebalancing opp ortunities. Quan tum computing offers a promising a ven ue for com binatorial optimisation prob- lems that are classically intractable at scale. The Quan tum Approximate Optimisation Algorithm (QAO A) [ 5 ] provides a near-term, v ariational approac h to solving Quadratic Unconstrained Binary Optimisation (QUBO) problems on current noisy intermediate-scale quan tum (NISQ) hardware [ 6 ]. Portfolio-related QUBO formulations ha v e b een studied for asset sele ction [ 7 – 9 ], but the question of applying QAO A to the r eb alancing sche dule problem has not b een previously addressed in the literature. The contributions of this pap er are: 1. Principled uncorrelated asset selection via Ledoit-W olf shrink age [ 10 ] com bined with hierarchical correlation clustering — av oiding b oth the Marko witz estimation error problem and greedy-searc h survivorship bias. 2. En trop y-regularised GA weigh t optimisation on GPU, preven ting degenerate sparse solutions while maximising annualised Sharp e ratio. 3. Minim um-V ariance and ens em ble w eigh ts as principled classical baselines computed via closed-form solution. 4. No v el QUBO formulation of the rebalancing schedule incorp orating marginal Sharp e gain, transaction cost p enalty , and o v er-frequency p enalt y via an exp onentially deca ying interaction term. 5. W alk-forw ard QA OA scheduling with multi-restart optimisation — eliminating lo ok ahead bias while providing robust angle estimation. 6. Comprehensiv e net-of-cost bac ktest comparing 16 strategies across Sharp e, Sortino, maximum dra wdown, Calmar ratio, rebalance count, and transaction cost. The remainder of the pap er is organised as follows. Section 2 reviews related w ork. Section 3 presen ts the full metho dology . Section 4 describ es exp erimental setup. Section 5 2 presen ts results and analysis. Section 6 discusses the quantum adv antage argument. Section 8 concludes. 2 Related W ork This section reviews prior w ork in classical p ortfolio optimisation, machine learning–based allo cation, and quantum approac hes to p ortfolio construction. While asset weigh ting and selection hav e b een widely studied, the optimisation of r eb alancing timing remains comparativ ely underexplored, particularly within quantum framew orks. Our formulation addresses this gap by casting w alk-forw ard rebalancing scheduling as a QUBO problem amenable to v ariational quan tum algorithms. 2.1 Classical P ortfolio Optimisation The mean-v ariance framework of Mark owitz [ 1 , 2 ] remains the canonical approac h to p ortfolio weigh t selection, extended by the Capital Asset Pricing Mo del (CAPM) [ 3 ] and subsequen t factor mo dels [ 11 ]. In practice, the cov ariance matrix m ust b e estimated from finite samples; Ledoit and W olf [ 10 ] show ed that analytical shrink age of the sample co v ariance tow ard a structured estimator dramatically reduces estimation error and impro v es out-of-sample p erformance. P ortfolio rebalancing has b een studied primarily as a cost-b enefit trade-off. Perold and Sharp e [ 4 ] in tro duced the constan t-mix strategy , while [ 12 , 13 ] show ed that optimal rebalancing frequency dep ends on asset volatilit y and transaction costs. Threshold- based rebalancing [ 14 ] and time-series momentum signals [ 15 ] hav e b een prop osed as impro v ements o v er calendar-based schedules. 2.2 Ev olutionary and Mac hine Learning Approac hes Genetic algorithms hav e b een applied to p ortfolio optimisation since [ 16 ], demonstrating comp etitiv e p erformance on non-conv ex ob jectives including Sharp e ratio maximisation. Reinforcemen t learning approaches [ 17 ] and deep neural netw orks [ 18 ] ha ve b een prop osed for dynamic asset allo cation, though out-of-sample generalisation remains c hallenging. 2.3 Quan tum P ortfolio Optimisation Quan tum computing approaches to p ortfolio optimisation hav e fo cused primarily on the asset selection problem, formulated as a QUBO. Reb entrost and Lloyd [ 9 ] prop osed a quan tum algorithm for p ortfolio optimisation with quadratic sp eedup. Bark outsos et al. [ 8 ] applied QA OA and V ariational Quan tum Eigensolv er (V QE) to p ortfolio selection on small instances. Mugel et al. [ 7 ] demonstrated dynamic p ortfolio optimisation on D-W a v e 3 quan tum annealers. More recen tly , [ 19 ] pro vided a comprehensiv e surv ey of quan tum finance algorithms. T o our knowledge, no prior work has formulated the r eb alancing timing decision as a QUBO problem or applied QAO A to this subproblem. 3 Metho dology 3.1 Problem Statemen t Let U b e a universe of M assets with daily adjusted close prices. W e seek a p ortfolio of n ≪ M assets with weigh ts w ∈ ∆ n (the n -simplex) and a binary rebalancing sc hedule x ∈ { 0 , 1 } W o ver W candidate dates, join tly maximising risk-adjusted return net of transaction costs. 3.2 Data and Univ erse Construction W e construct a surviv orship-bias-free S&P 500 universe b y starting from the current index constituen ts and reversing all addition/deletion even ts that o ccurred after the training cutoff date (Decem b er 31, 2024), reco vering the set of sto cks that wer e in the index on that date. Daily adjusted close prices are do wnloaded for the p erio d Jan uary 1, 2010 to December 31, 2025. After removing tic kers with missing data throughout the full p erio d, M = 422 assets remain. The training p eriod cov ers Jan uary 2010 – December 2024 ( T train = 3 , 774 trading da ys) and the out-of-sample test p erio d cov ers Jan uary – December 2025 ( T test = 249 trading days). 3.3 Asset Selection via Hierarchical Clustering Ledoit-W olf Shrink age Co v ariance. Let r t = log ( P t /P t − 1 ) ∈ R M b e the vector of daily log returns. The sample co v ariance ˆ Σ is estimated with the analytical Ledoit-W olf shrink age estimator [ 10 ]: ˆ Σ L W = (1 − α ) ˆ Σ sample + α µ target I , (1) where α is the data-driv en shrink age in tensity and µ target is the a v erage sample eigenv alue. This reduces estimation error, particularly in the large- M , finite- T regime prev alent in finance. Angular Distance and Hierarchical Clustering. F rom the shrink age correlation matrix ˆ R L W = D − 1 / 2 ˆ Σ L W D − 1 / 2 (where D = diag ( ˆ Σ L W )), we define the angular distance 4 b et w een assets i and j : d ij = q 1 2 (1 − ˆ ρ ij ) , ˆ ρ ij ∈ [ − 1 , 1] . (2) This metric satisfies the triangle inequality and maps zero correlation to distance 1 / √ 2 [ 20 ]. W ard’s link age hierarchical clustering [ 21 ] is applied to the condensed distance matrix, partitioned into n = 10 clusters. Cluster Represen tative Selection. F rom eac h cluster C k , we select the sto ck with the highest annualised Sharp e ratio on the training set: s ∗ k = arg max s ∈C k ¯ r s σ s √ 252 , (3) where ¯ r s and σ s are the mean and standard deviation of daily log returns o v er the training p erio d. This pro cedure selects sto c ks that are simultaneously unc orr elate d with e ach other (b y construction of the clustering) and high-p erforming individual ly . The selected p ortfolio is S = { EXR, NI, CHD, LL Y, COST, A V GO, TPL, CT AS, AMP , AJG } . 3.4 W eigh t Optimisation En trop y-Regularised Genetic Algorithm. Let w ∈ ∆ n b e the p ortfolio w eight v ector. The GA maximises a regularised Sharp e ob jective: F ( w ) = ¯ r p σ p √ 252 | {z } Sharpe ratio + λ ent − P n i =1 w i log w i log n | {z } normalised entrop y , (4) where r p,t = log ( w ⊤ R t ) is the p ortfolio log return at time t , ¯ r p and σ p are its sample mean and standard deviation, and λ ent = 0 . 05 is the entrop y regularisation weigh t. The entrop y term H ( w ) ∈ [0 , 1] p enalises concen trated solutions, prev enting degenerate outcomes where one or tw o assets receiv e all weigh t. The GA uses a p opulation of 300 individuals, 200 generations, uniform crossov er, and 15% m utation rate, with w eigh ts constrained to [0 . 01 , 1] to av oid exact zeros. Minim um V ariance W eigh ts. The global minim um v ariance p ortfolio is computed in closed form: w MV = ˆ Σ − 1 L W 1 1 ⊤ ˆ Σ − 1 L W 1 , (5) where the pseudoin v erse is used for numerical stabilit y , and negative w eigh ts are pro jected to zero (no short-selling). 5 Ensem ble W eigh ts. T o hedge mo del uncertaint y , w e define an equal-blend ensem ble: w Ens = 1 3 ( w GA + w MV + w EQ ) , (6) where w EQ = 1 /n are equal w eights. T raining-p erio d Sharp e ratios are: GA = 1.445, MinV ar = 1.327, Ensemble = 1.388, Equal = 0.97. 3.5 QUBO F orm ulation of the Rebalancing Sc hedule Definition 1 (Rebalancing Schedule Problem) . Given a test p erio d of T tr ading days, tar get weights w , and a set of W = 8 c andidate r eb alancing dates T = { t 0 , t 1 , . . . , t W − 1 } (e qual ly sp ac e d), find a binary sche dule x ∈ { 0 , 1 } W that maximises net Sharp e impr ovement subje ct to tr ansaction c ost minimisation. F or eac h candidate date t k , we first compute the drifte d weights w drift k that the p ortfolio has naturally evolv ed to by time t k without any rebalancing: w drift k = w k − 1 ⊙ π k 1 ⊤ ( w k − 1 ⊙ π k ) , π k,i = t k − 1 Y t = t k − 1 R t,i , (7) where R t,i is the gross return of asset i at time t and w 0 = w . Marginal Sharp e Gain. The net b enefit of rebalancing at t k is defined as: g k = SR( w , [ t k , t k +1 ]) − SR( w drift k , [ t k , t k +1 ]) | {z } Sharpe improv ement − c · ∥ w drift k − w ∥ 1 · √ 252 | {z } annualised cost p enalty , (8) where SR ( w , [ s, e ]) is the ann ualised Sharp e ratio of p ortfolio w on the lo cal return windo w [ s, e ], and c = 0 . 001 (10 basis p oints p er side) is the p er-unit transaction cost. QUBO Ob jectiv e. W e minimise the following QUBO: min x ∈{ 0 , 1 } W x ⊤ Q x , (9) where the QUBO matrix Q ∈ R W × W has entries: Q kk = − λ 1 g k + λ 2 c · n, (10) Q kl = λ 3 exp − | t k − t l | ∆ t , k = l , (11) with λ 1 = 1 . 0 (reward for b eneficial rebalancing), λ 2 = 0 . 5 (fixed cost p enalty), λ 3 = 0 . 3 (consecutiv e rebalancing p enalt y), and ∆ t the av erage spacing b et ween candidate dates. 6 The exp onen tial decay in ( 11 ) enco des the prior that rebalancing t wice in rapid succession is w asteful. Q is normalised to [ − 1 , 1] b y dividing by max | Q kl | to stabilise the QA OA optimisation landscap e. 3.6 QA OA for QUBO Solving Ising Mapping. The QUBO ( 9 ) is conv erted to an Ising Hamiltonian H C = P i h i Z i + P i 5% GA, MinV ar, Equal, Ensemble QA OA (w alk-fwd) Quantum-optimal sc hedule 9 4.3 QA OA Hyp erparameters T able 3: QA O A configuration P arameter V alue Circuit depth p 2 Candidate dates p er window W 8 W alk-forward windo ws K 3 Restarts R 5 Optimisation shots 2,048 Ev aluation shots 4,096 Classical optimiser COBYLA (max 150 iter) QUBO p enalty λ 1 1.0 QUBO p enalty λ 2 0.5 QUBO p enalty λ 3 0.3 T ransaction cost c 0.001 (10 bp) 5 Results This section presents the empirical ev aluation of the prop osed p ortfolio construction and quan tum-enhanced rebalancing framework. W e first ve rify that the clustering-based asset selection pro duces a div ersified and high-Sharp e subset. W e then analyse the resulting p ortfolio w eights and the induced QUBO structure, before examining the sc hedules selected b y QA OA in a walk-forw ard setting. Finally , we rep ort out-of-sample p erformance for all classical and quantum strategies during the 2025 test p erio d. 5.1 Asset Selection Figure 1 sho ws the Ledoit-W olf shrink age correlation matrix and training Sharp e ratios for the 10 selected sto c ks.The maxim um off-diagonal correlation is 0.62 (CT AS–AMP), and the minimum is 0.07 (CHD–TPL), confirming that the hierarchical clustering pro cedure successfully selects a diversified p ortfolio. TPL exhibits near-zero correlation with all other assets ( max ρ = 0 . 34), functioning as a natural hedge. All 10 sto cks ac hieved p ositive training Sharp e ratios (range 0.60–1.02), confirming the cluster-represen tative selection criterion. 10 Figure 1: Asset selection results. Left: Ledoit-W olf shrink age correlation matrix of the 10 selected sto cks. Off-diagonal v alues range from 0.07 (CHD–TPL) to 0.62 (CT AS–AMP), confirming low in ter-asset correlation. Righ t: Annualised Sharp e ratios (log returns) on the training p erio d (2010–2024). All selected sto cks ac hiev e Sharp e > 0 . 6. 5.2 P ortfolio W eigh ts T able 4 rep orts the GA-optimised w eigh ts alongside the MinV ar and Equal w eights. T able 4: P ortfolio weigh ts by metho d (%) Sto c k GA MinV ar Equal Ensem ble EXR 7.5 4.1 10.0 7.2 NI 0.3 11.2 10.0 7.2 CHD 11.1 10.3 10.0 10.5 LL Y 21.1 12.0 10.0 14.4 COST 21.1 20.2 10.0 17.1 A V GO 11.0 9.5 10.0 10.2 TPL 13.1 6.6 10.0 9.9 CT AS 5.0 10.1 10.0 8.4 AMP 0.2 3.5 10.0 4.6 AJG 9.6 12.5 10.0 10.7 T rain Sharp e 1.445 1.327 0.970 1.388 The GA concen trates w eight in LL Y (21.1%) and COST (21.1%), reflecting their strong training-p erio d Sharp e ratios. The en tropy regularisation prev ents degenerate solutions: NI and AMP retain 0.3% and 0.2% resp ectively (v ersus 0% without regularisation in v1). MinV ar ov erweigh ts NI (11.2%) and AJG (12.5%) due to their low individual volatilities, whic h did not translate to out-of-sample p erformance in the 2025 test year. 11 5.3 QUBO Structure Figure 2 (b ottom righ t) sho ws the normalised QUBO matrix for the GA w eights in the first walk-forw ard window. After normalisation, all v alues lie in [ − 1 , 1]. Negativ e diagonal en tries (blue) indicate candidate dates where rebalancing is b eneficial (p ositive net Sharp e gain g k > 0); p ositive diagonal entries (red) indicate dates where holding drifted weigh ts is preferable. Off-diagonal en tries are small and p ositiv e, enco ding the mild p enalty for frequen t rebalancing. 5.4 QA OA Sc hedule and Bitstring Distribution The w alk-forward QA OA selected rebalancing schedules of [0 , 1 , 1 , 0 , 1 , 0 , 0 , 1], [0 , 1 , 0 , 1 , 1 , 0 , 0 , 0], and [1 , 0 , 1 , 0 , 0 , 1 , 0 , 1] for the three windows resp ectiv ely (8 total rebalances). Figure 3 (left) shows the QA OA measurement distribution for the GA weigh t run. The top bitstring accoun ts for > 7% of all 4,096 shots, with probabilit y mass concen trated in the top-5 bitstrings ( > 25%). This concen tration is a hallmark of successful QAO A con vergence and supp orts the quan tum adv an tage argumen t (Section 6 ). 5.5 Bac ktest P erformance T able 5 rep orts all 16 strategies on the 2025 out-of-sample test p erio d. T able 5: Out-of-sample p erformance (T est: Jan–Dec 2025). Best v alue in eac h column is b old . QAO A strategies are mark ed with † . Strategy Return (%) Sharpe Sortino MDD (%) Calmar Rebal / Cost (bp) GA Buy&Hold 7.68 0.471 0.610 -15.88 0.484 0 / 0.0 MinV ar Buy&Hold -0.86 0.060 0.077 -16.46 -0.052 0 / 0.0 Equal Buy&Hold 5.15 0.382 0.483 -14.70 0.350 0 / 0.0 Ensem ble Buy&Hold 3.99 0.325 0.415 -14.24 0.280 0 / 0.0 GA Rebal/1d 9.12 0.541 0.701 -15.51 0.588 248 / 31.6 GA Rebal/5d 9.63 0.567 0.735 -15.74 0.612 49 / 15.8 GA Rebal/10d 9.77 0.575 0.747 -15.66 0.624 24 / 11.0 GA Rebal/21d 8.43 0.505 0.654 -15.63 0.539 11 / 6.5 GA Threshold (5%) 7.63 0.469 0.610 -15.88 0.481 2 / 2.4 GA + QAO A † 10.10 0.588 0.764 -15.84 0.638 8 / 6.1 MinV ar + QA O A † 0.34 0.137 0.177 -16.09 0.021 8 / 4.6 Equal + QAO A † 7.26 0.498 0.635 -14.69 0.494 8 / 5.6 Ensem ble + QA O A † 5.63 0.422 0.540 -14.15 0.398 8 / 5.6 12 Figure 2: Bac ktest results (test p erio d: Jan–Dec 2025). T op left: Cum ulative portfolio v alue. Classical strategies (blue dashed) vs. QAO A strategies (orange solid) vs. S&P 500 (blac k). GA + QA OA (brigh t orange) ac hieves the highest terminal v alue among all quan tum and classical strategies. T op right: Dra wdown profiles. QA OA strategies main tain tigh ter dra wdo wn control than p erio dic rebalancing. Bottom left: Sharp e ratio comparison (horizontal bar chart). GA + QAO A ac hieves the highest Sharpe (0.588), highligh ted in gold. Bottom right: Normalised QUBO matrix (GA w eights, w alk-forw ard windo w 1), illustrating the structured cost landscap e solved b y QA OA. Figure 3: Left: QA OA measurement bitstring distribution for GA + QAO A (top 20 bitstrings, 4,096 shots). The top bitstring 11000010 accoun ts for > 7% of shots, indicating successful QAO A con vergence. Righ t: W eigh t comparison across all four p ortfolio metho ds. GA concentrates on LL Y and COST; MinV ar distributes more evenly; Ensem ble a verages all three. 13 5.6 Key Findings Finding 1: QA O A outp erforms all classical strategies. GA + QAO A ac hieves Sharp e 0.588, surpassing the b est classical rebalancing strategy (GA Rebal/10d, Sharp e 0.575), a +2.3% impro vemen t . Finding 2: Dramatic cost reduction. GA + QAO A achiev es this impro v ement with only 8 rebalances (6.1 bp) versus 24 rebalances (11.0 bp) for GA Rebal/10d — a 44.5% reduction in transaction costs . Finding 3: W eight metho d matters more than sc heduling for MinV ar. MinV ar w eigh ts underp erform in 2025 regardless of scheduling (Sharp e 0.06–0.14), confirming that 2025 was a momentum-driv en environmen t where minimum-v ariance sto c ks lagged. This v alidates GA weigh t optimisation as a critical comp onent. Finding 4: Na ¨ ıv e ensem bling do es not help. The Ensemble strategy (a verage of GA, MinV ar, Equal) yields Sharp e 0.422 with QAO A — b elow GA alone (0.588). Av eraging with the weak MinV ar comp onent dilutes the GA signal, suggesting that in future w ork the ensemble should exclude underp erforming w eigh t strategies. Finding 5: Threshold rebalancing fails. The 5% drift threshold triggers only 2 rebalances in 2025 (Sharp e 0.469), underperforming ev en buy-and-hold (Sharp e 0.471). This demonstrates that threshold rules calibrated on training v olatilit y ma y b e miscalibrated out-of-sample — a problem the QUBO formulation directly addresses by estimating rebalancing v alue from the actual lo cal return distribution. 6 Quan tum Adv an tage Discussion This section ev aluates whether the prop osed formulation exhibits meaningful p oten tial for quan tum adv an tage. W e analyse the in trinsic com binatorial complexity of the rebalancing sc hedule problem, examine empirical evidence of QAO A con vergence to w ard low-energy solutions, and discuss the practical feasibility of scaling the approac h to near-term and annealing-based quantum hardw are. 6.1 Complexit y of the Rebalancing Schedule Problem The rebalancing sc hedule problem o ver W candidate dates is equiv alent to an unc onstr aine d pseudo-Bo ole an optimisation problem on W binary v ariables. The brute-force solution requires ev aluating 2 W binary strings. F or W = 8, this is 256 ev aluations — tractable classically . How ever, in a pro duction setting with daily rebalancing decisions ov er a y ear 14 ( W ≈ 252), or with multi-asset, multi-windo w formulations, the com binatorial space gro ws exp onen tially . Quan tum annealing and QAO A offer p olynomial query complexit y for appro ximate solutions in this regime [ 5 , 22 ]. 6.2 Evidence of QA O A Con v ergence The QAO A bitstring distribution (Figure 3 , left) sho ws clear concentration of probabilit y mass. The top bitstring accounts for > 7% of 4,096 shots, compared to the uniform baseline of 1 / 2 8 ≈ 0 . 4%. This represents an 18 × enric hmen t of the optimal solution, pro viding empirical evidence that the v ariational circuit is learning a useful approximation of the ground state. 6.3 Scaling to Real Quantum Hardw are The current implemen tation uses the Qiskit Aer statev ector sim ulator (exact simulation, exp onen tial memory in W ). F or real hardw are deploymen t, tw o paths exist: (i) NISQ devic es : The 8-qubit circuit with p = 2 has circuit depth O ( p · W 2 ) ≈ 128 gates, within the coherence limits of current sup erconducting pro cessors [ 23 ]; (ii) Quantum anne alers : D-W av e systems natively accept QUBO inputs [ 24 ] and hav e demonstrated p ortfolio optimisation at scale [ 7 ]. 7 Limitations and F uture W ork The curren t exp erimen t uses a single y ear out-of-sample test; m ulti-year rolling ev aluation w ould strengthen the conclusion. MinV ar weigh ts underp erformed in 2025’s momentum en vironmen t; adaptive w eight selection (e.g., regime-conditional) could impro ve the en- sem ble.The QA OA windo w size ( W = 8) is limited by current sim ulation cost; scaling to W ≥ 20 w ould require hardware quantum devices or tensor-netw ork-based classical sim ulators. F uture w ork includes exploration of joint QUBO formulations that optimise w eigh ts and schedule simultaneously , as wel l as empirical ev aluation on ph ysical D-W av e hardw are. 8 Conclusion W e presented a quan tum-assisted algorithmic trading framew ork that formulates p ortfolio rebalancing scheduling as a QUBO problem and solv es it with QAO A in a walk-forw ard framew ork. The system combines: (1) Ledoit-W olf hierarchical clustering for principled uncorrelated asset selection; (2) entrop y-regularised GA weigh t optimisation on GPU; and (3) normalised QUBO rebalancing with multi-restart QA O A. 15 On the S&P 500 2025 out-of-sample test, GA + QAO A achiev es the b est Sharp e ratio (0.588) among all 16 strategies, outp erforming the b est classical approach (Sharp e 0.575) while reducing transaction costs by 44.5% (6.1 bp vs. 11.0 bp, 8 vs. 24 trades). These results provide preliminary empirical evidence that v ariational quantum optimisation can deliv er economically meaningful impro v ements in combinatorial trading decisions, while remaining compatible with near-term quantum hardw are. References [1] H. M. Mark owitz, Portfolio sele ction: efficient diversific ation of investments . Y ale univ ersit y press, 2008. [2] M. Rubinstein, “Mark o witz’s” p ortfolio selection”: A fift y-year retrosp ectiv e,” The Journal of financ e , vol. 57, no. 3, pp. 1041–1045, 2002. [3] W. F. Sharp e, “Mutual fund p erformance,” The Journal of business , vol. 39, no. 1, pp. 119–138, 1966. [4] A. F. Perold and W. F. Sharp e, “Dynamic strategies for asset allo cation,” Financial A nalysts Journal , vol. 44, no. 1, pp. 16–27, 1988. [5] E. F arhi, J. Goldstone, and S. Gutmann, “A quan tum approximate optimization algorithm,” arXiv pr eprint arXiv:1411.4028 , 2014. [6] J. Preskill, “Quan tum computing in the nisq era and b ey ond,” Quantum , v ol. 2, p. 79, 2018. [7] S. Mugel, C. Kuchk ovsky , E. S´ anc hez, S. F ern´ andez-Lorenzo, J. Luis-Hita, E. Lizaso, and R. Or ´ us, “Dynamic p ortfolio optimization with real datasets using quantum pro cessors and quantum-inspired tensor net w orks,” Physic al R eview R ese ar ch , vol. 4, no. 1, p. 013006, 2022. [8] P . K. Barkoutsos, G. Nannicini, A. Rob ert, I. T av ernelli, and S. W o erner, “Impro ving v ariational quantum optimization using cv ar,” Quantum , vol. 4, p. 256, 2020. [9] P . Reb en trost and S. Lloyd, “Quan tum computational finance: quan tum algorithm for p ortfolio optimization,” KI-K¨ unstliche Intel ligenz , vol. 38, no. 4, pp. 327–338, 2024. [10] O. Ledoit and M. W olf, “A well-conditioned estimator for large-dimensional co v ariance matrices,” Journal of multivariate analysis , vol. 88, no. 2, pp. 365–411, 2004. [11] E. F. F ama and K. R. F rench, “Common risk factors in the returns on sto c ks and b onds,” Journal of financial e c onomics , vol. 33, no. 1, pp. 3–56, 1993. 16 [12] S. J. Masters, “Rebalancing,” Journal of p ortfolio Management , v ol. 29, no. 3, p. 52, 2003. [13] D. M. Smith and W. Desormeau, “Optimal rebalancing frequency for sto c k-b ond p ortfolios,” Journal of Financial Planning , vol. 19, pp. 52–63, 2006. [14] H. Dich tl, W. Drob etz, and M. W am bach, “Where is the v alue added of rebalancing? a systematic comparison of alternativ e rebalancing strategies,” Financial Markets and Portfolio Management , v ol. 28, no. 3, pp. 209–231, 2014. [15] T. J. Mosko witz, Y. H. Ooi, and L. H. P edersen, “Time series momentum,” Journal of financial e c onomics , vol. 104, no. 2, pp. 228–250, 2012. [16] T.-J. Chang, N. Meade, J. E. Beasley , and Y. M. Sharaiha, “Heuristics for cardinalit y constrained p ortfolio optimisation,” Computers & Op er ations R ese ar ch , v ol. 27, no. 13, pp. 1271–1302, 2000. [17] Z. Jiang, D. Xu, and J. Liang, “A deep reinforcement learning framew ork for the financial p ortfolio managemen t problem,” arXiv pr eprint arXiv:1706.10059 , 2017. [18] Z. Zhang, S. Zohren, and S. Rob erts, “Deep learning for p ortfolio optimization,” arXiv pr eprint arXiv:2005.13665 , 2020. [19] D. Herman, C. Go ogin, X. Liu, Y. Sun, A. Galda, I. Safro, M. Pistoia, and Y. Alexeev, “Quan tum computing for finance,” Natur e R eviews Physics , v ol. 5, no. 8, pp. 450–465, 2023. [20] R. N. Man tegna, “Hierarc hical structure in financial mark ets,” The Eur op e an Physic al Journal B-Condense d Matter and Complex Systems , vol. 11, no. 1, pp. 193–197, 1999. [21] J. H. W ard Jr, “Hierarc hical grouping to optimize an ob jective function,” Journal of the Americ an statistic al asso ciation , vol. 58, no. 301, pp. 236–244, 1963. [22] A. Lucas, “Ising formulations of many np problems,” F r ontiers in physics , v ol. 2, p. 74887, 2014. [23] F. Arute, K. Ary a, R. Babbush, D. Bacon, J. C. Bardin, R. Barends, R. Bisw as, S. Boixo, F. G. Brandao, D. A. Buell et al. , “Quantum supremacy using a pro- grammable superconducting pro cessor,” natur e , vol. 574, no. 7779, pp. 505–510, 2019. [24] C. C. McGeo ch and C. W ang, “Exp erimen tal ev aluation of an adiabiatic quantum system for com binatorial optimization,” in Pr o c e e dings of the A CM International Confer enc e on Computing F r ontiers , 2013, pp. 1–11. 17

Original Paper

Loading high-quality paper...

Comments & Academic Discussion

Loading comments...

Leave a Comment