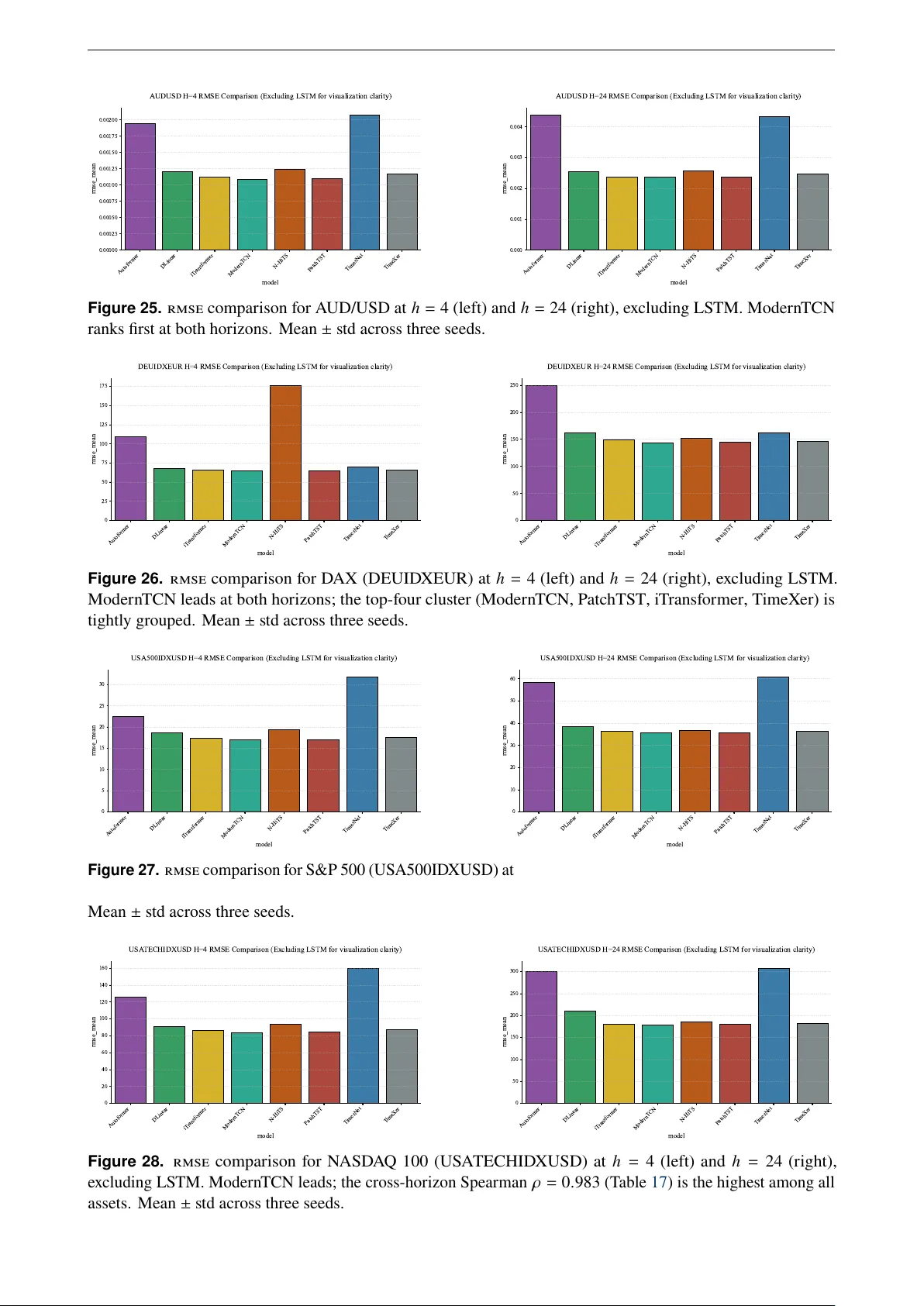

A Controlled Comparison of Deep Learning Architectures for Multi-Horizon Financial Forecasting: Evidence from 918 Experiments

Multi-horizon price forecasting is central to portfolio allocation, risk management, and algorithmic trading, yet deep learning architectures have proliferated faster than rigorous financial benchmarks can evaluate them. This study provides a control…

Authors: Nabeel Ahmad Saidd