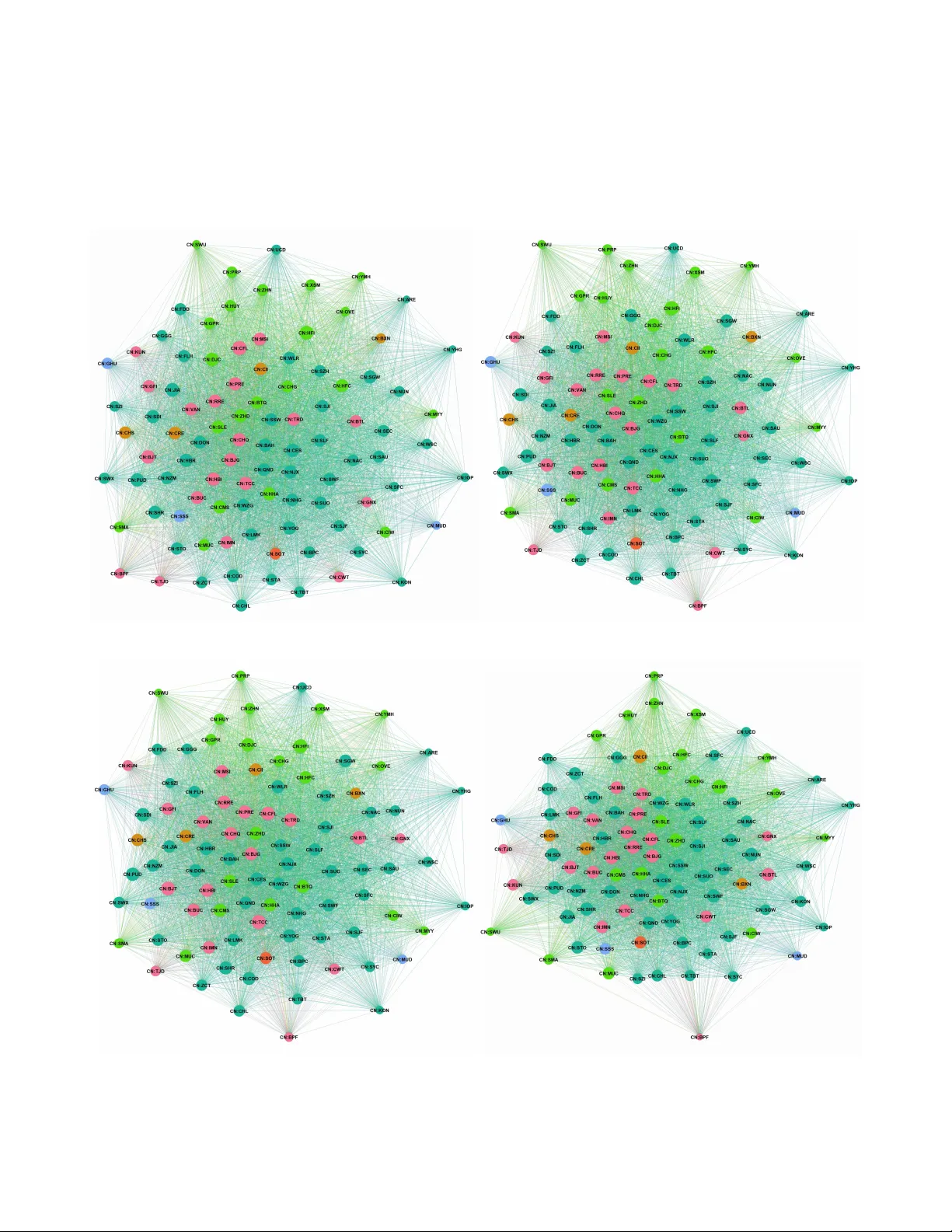

Volatility Spillovers in China's Real Estate Crisis: A Network Approach

Sentiment towards the Chinese real estate sector has deteriorated following the introduction of financing constraints in 2020 with the ''three red lines." Forcing developers to restructure their debt, the policy triggered a cascade of financing troub…

Authors: Julia Manso